China Testing Inspection And Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

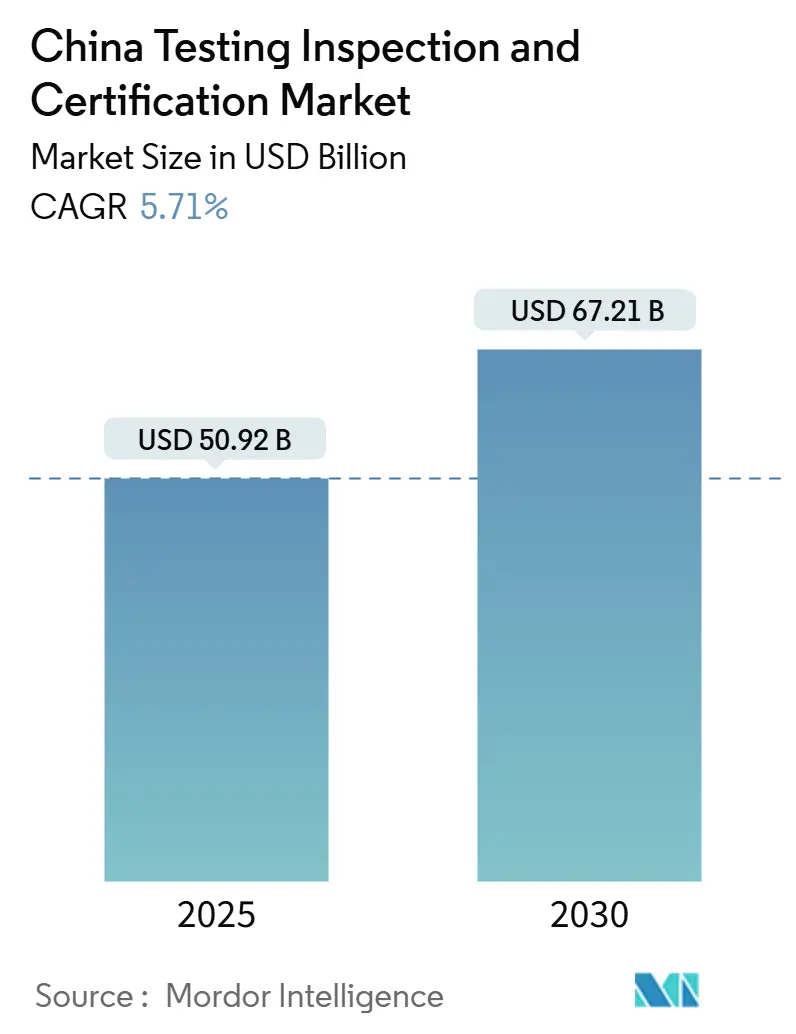

| Market Size (2025) | USD 50.92 Billion |

| Market Size (2030) | USD 67.21 Billion |

| Growth Rate (2025 - 2030) | 5.71% CAGR |

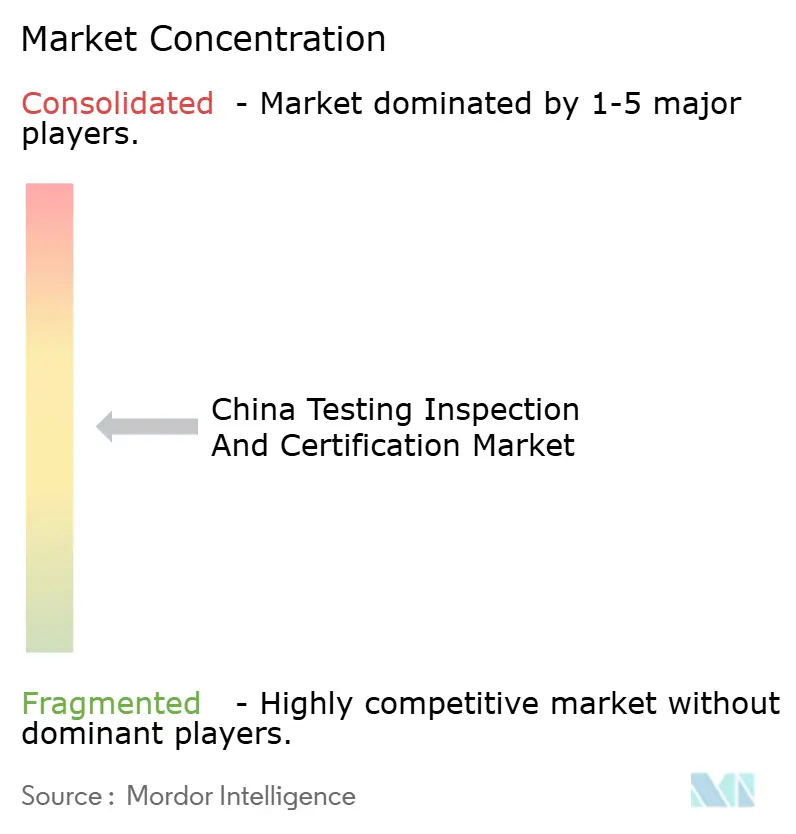

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Testing Inspection And Certification Market Analysis by Mordor Intelligence

The China testing inspection and certification market size stood at USD 50.92 billion in 2025 and is forecast to reach USD 67.21 billion by 2030, reflecting a 5.71% CAGR. Regulatory enforcement of GB and CCC product-safety rules, surging demand for carbon-neutrality verification, and rapid growth in new-energy vehicle testing keep the China testing inspection and certification market on a steady growth path. Intensified oversight of export consignments via cross-border e-commerce channels, together with digital-government programs that embed e-certificate APIs into business platforms, further expand addressable opportunities. Domestic providers invest in hydrogen, cybersecurity, and AI-driven laboratories, while multinational leaders pursue acquisitions in digital trust and sustainability to deepen presence. Fragmented provincial accreditation systems and a tight labor pool in advanced domains temper growth but have not derailed the upward momentum of the China testing inspection and certification market.

Key Report Takeaways

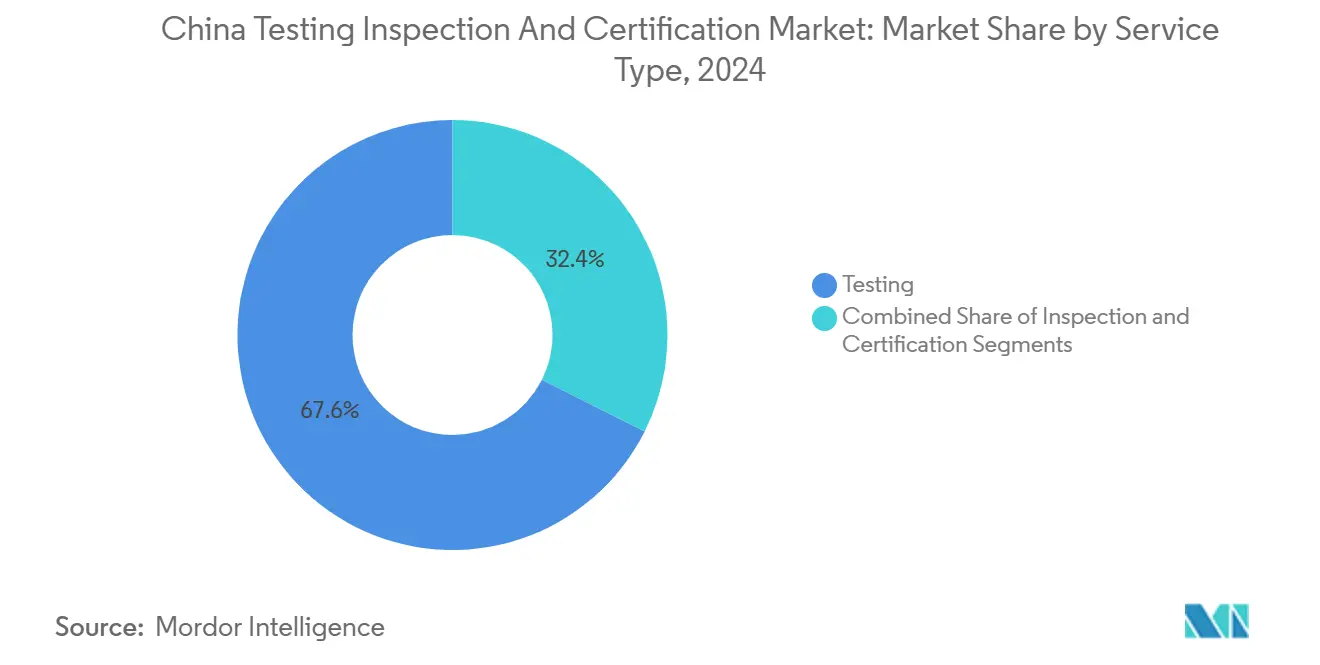

- By service type, Testing held a 67.6% China testing inspection and certification market share in 2024; Certification is expected to post the fastest 6.2% CAGR through 2030.

- By sourcing type, outsourced services commanded 62.5% of the China testing inspection and certification market size in 2024 while in-house operations are forecast to trail at a 4.3% CAGR.

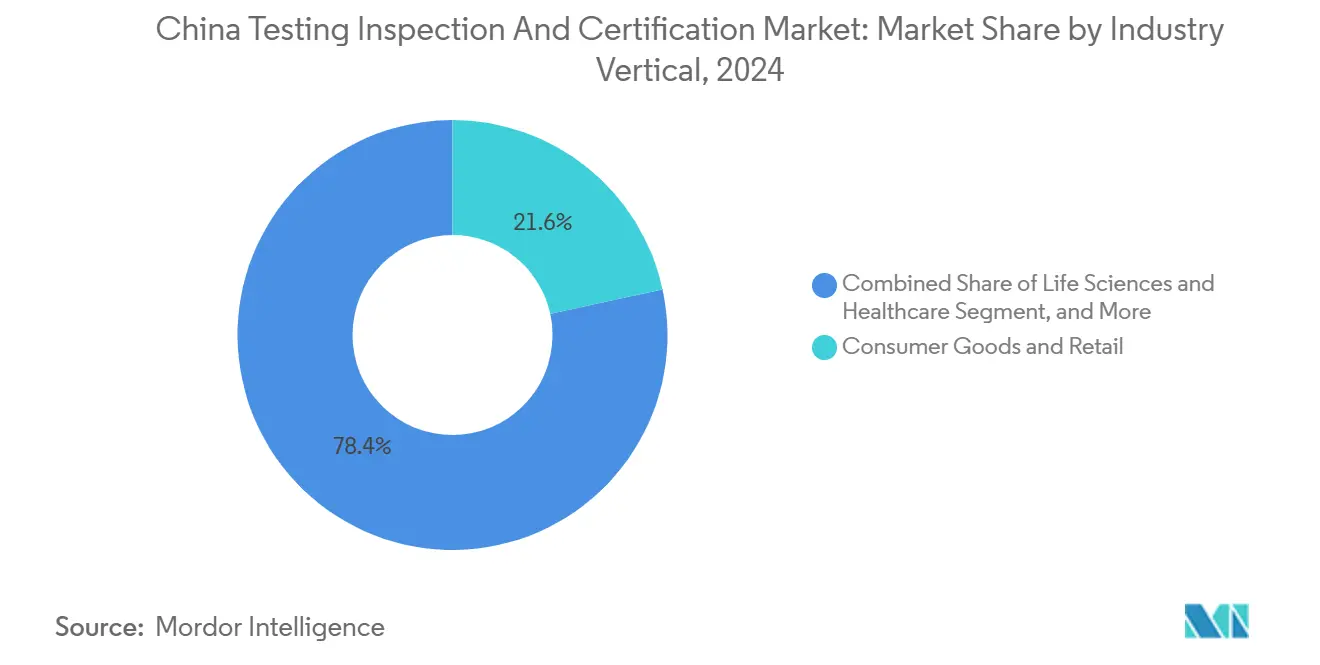

- By industry vertical, Consumer Goods and Retail led with 21.6% revenue share in 2024; Life Sciences and Healthcare is advancing at a 6.5% CAGR to 2030.

- By mode of delivery, off-site laboratories accounted for 57.3% of the China testing inspection and certification market in 2024 and Remote / Digital services are set to grow at a 6.9% CAGR through 2030.

China Testing Inspection And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensified enforcement of GB and CCC product-safety standards | +1.80% | National - Shanghai, Guangzhou, Shenzhen lead | Medium term (2-4 years) |

| Mandatory carbon-neutrality verifications under the 2060 pledge | +1.50% | National with Belt and Road spillover | Long term (≥ 4 years) |

| Rapid expansion of the EV / NEV sector | +2.10% | Beijing, Shanghai, Guangdong focus | Short term (≤ 2 years) |

| Cross-border e-commerce growth driving pre-shipment inspection | +1.20% | Guangdong, Zhejiang, Jiangsu hubs | Medium term (2-4 years) |

| Provincial digital-government e-certificate initiatives | +0.80% | Guangdong and Zhejiang cores | Long term (≥ 4 years) |

| Algorithm conformity assessments for exported industrial software | +0.60% | National technology clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensified GB and CCC Standards Enforcement Accelerates Demand

The State Administration for Market Regulation added lithium-ion batteries and 15 other categories to the CCC catalog in July 2024, lifting the count to 107 products. New EV battery rule GB 38031-2020 mandates thermal-propagation testing, causing laboratories to expand equipment lines. Household-appliance standard GB/T 4706.1-2024 requires certificate conversion by July 2027, immediately filling testing pipelines. In 2026, Beijing will apply the world’s strictest EV battery safety rule that bans fires for two hours after thermal runaway, thereby positioning local labs as global standard-setters. Collectively, these measures drive continuous throughput for the China testing inspection and certification market.

Carbon Neutrality Pledge Spurs ESG Verification

China’s 2060 carbon-neutrality target has made third-party greenhouse-gas audits a boardroom priority. CTI Certification has scaled carbon-management assessments under T/CIECCPA 002-2021, while TÜV SÜD and SGS have ramped up PAS 2060 services.[1]Katharina Li, “Carbon Neutrality Certification Services,” TÜV SÜD, tuv-sud.cn The national carbon-trading system and the EU Carbon Border Adjustment Mechanism push exporters to secure verified carbon footprints, intensifying Certification demand. Over 18,500 suppliers have published PRTR data via the Blue EcoChain disclosure platform, underscoring corporate appetite for trusted ESG validation. These forces embed sustainability into the long-run revenue engine of the China testing, inspection, and certification market.

EV Industry Boom Requires Advanced Testing

New-energy vehicle sales rose 50.4% year-on-year to 3.08 million units in Q1 2025, straining existing test capacity. Shanghai’s Hydrogen and Fuel Cell Inspection Testing Base now houses the country’s largest 3,000 m³ vehicle EMC chamber and a 400 kW stack bench, enabling hydrogen-mobility validations down to –40 °C. Cybersecurity standard GB/T 45181-2024, effective April 2025, introduces mandatory abnormal-behavior detection certification for connected vehicles. As automakers chase compliance, the China testing inspection and certification market gains high-margin business in battery, EMC, and cyber-resilience testing.

Cross-Border E-Commerce Quality Assurance Expands

Record overseas attendance at the 137th Canton Fair signals sustained export momentum that relies on pre-shipment quality certificates. Dongguan’s public e-commerce service platform integrates customs data and lab reports via APIs, letting merchants obtain inspection documents in real time. The fully digitalized national e-fapiao system launched in December 2024 harmonizes invoice validation and certification workflows. Together these logistics and fintech advances stimulate inspection volumes and deepen digital-verification uptake across the China testing inspection and certification market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented provincial accreditation regimes | -0.90% | National, multi-provincial operations | Medium term (2-4 years) |

| Shortage of qualified TIC professionals in advanced domains | -1.20% | Acute in tier-1 cities | Short term (≤ 2 years) |

| Domestic preference clauses in public procurement | -0.60% | Strategic sectors nationwide | Long term (≥ 4 years) |

| Slow harmonization of remote-inspection standards | -0.40% | Pilot provinces only | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Gaps Curtail High-End Testing Capacity

China may need 6 million AI specialists by 2030, yet current supply could cover only one-third of demand. Cybersecurity labs compete for PhD graduates at annual salaries of CNY 800,000–1,000,000 (USD 112,000–140,000). Hydrogen facilities, such as the new Jiading center, struggle to recruit staff certified for 70 MPa cylinder testing. Unless skill pipelines improve, labor scarcity will restrain the upscale trajectory of the China testing inspection and certification market.

Fragmented Accreditation Drives Duplicate Audits

Different provincial bodies impose diverging requirements, forcing testing inspection and certification firms to repeat site audits and paperwork. Guangdong Quality Testing CTC operates under a separate technical-leadership scheme, adding compliance steps for nation-wide providers. Remote inspections are accepted in some provinces but not others, despite pilot successes at CSEI. These inconsistencies shave nearly one percentage point off projected CAGR and raise operating costs across the China testing inspection and certification market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Holds Sway While Certification Accelerates

Testing delivered 67.6% of 2024 revenue, reflecting compulsory conformity for 107 CCC-listed goods. Certification, however, is the growth pacesetter at 6.2% CAGR through 2030 as firms chase carbon neutrality and digital-trust seals. Inspection sits between the two, buoyed by cross-border merchandise flows. The expanded CCC scope and harder EV battery rules guarantee large recurring volumes, keeping the China testing inspection and certification market size for Testing ahead, while Certification gains strategic relevance as corporations face ESG disclosure mandates.

Laboratory investments reinforce segment dynamics. The Jiading hydrogen facility offers 400 kW fuel-cell load testing and a minus-40 °C chamber, underscoring capital depth required for leading-edge Testing. Certification players pivot to cloud platforms: SGS purchased digital-trust auditor CertX and GHG verifier Aster Global, embedding climate analytics into its suite. This dual track of heavy-asset labs and data-centric Certification positions the China testing inspection and certification market for balanced expansion.

By Sourcing Type: Outsourcing Becomes the Norm

Outsourced work accounted for 62.5% of the China testing inspection and certification market share in 2024 as manufacturers focus on core R&D rather than regulatory minutiae. China Leon Inspection’s HKD 1.26 billion (USD 161.3 million) 2024 turnover, powered by AI-enabled Smart Testing Laboratory 3.0, exemplifies outsourcing’s appeal. In-house labs persist in pharmaceuticals and defense but often lack breadth across GB updates, UN GTR13 hydrogen norms, and IEC cyber standards. Outsourcers achieve scale by pooling engineers and equipment, helping the China testing inspection and certification market size in outsourced services rise 5.9% annually despite wage inflation.

Digitalization amplifies outsourcing gains. Blockchain certificates and remote-video audits slash cycle times, letting third-party labs integrate directly with the national e-fapiao ledger for automated billing. While talent shortages apply upward pressure on fees, volume expansion outweighs cost escalation, cementing the outsourced advantage.

By Industry Vertical: Consumer Dominance Gives Way to Healthcare Momentum

Consumer Goods and Retail commanded a 21.6% slice of China testing inspection and certification market revenue in 2024, propelled by tighter toy and appliance standards that oblige certificate renewal by 2027. Life Sciences and Healthcare, growing 6.5% annually, benefits from new medical-device cybersecurity checks and bio-manufacturing GMP upgrades. Automotive and Transportation enjoys robust orders for battery, EMC, and vehicle-network testing as NEV output surges. Energy and Utilities emerge as a specialty niche on the back of hydrogen cylinder and battery-energy-storage regulations, yet require high-capex labs that only a handful of players can finance.

Diverse vertical momentum stabilizes aggregate growth. Consumer testing generates predictable volumes, while Life Sciences offers premium margins backed by stringent CFDA requirements. This balance underpins the resilience of the China testing inspection and certification market even amid sector-specific cycles.

By Mode of Service Delivery: Laboratories Dominate as Digital Gains Speed

Off-site laboratories held 57.3% of 2024 revenue, reflecting entrenched need for environmental chambers, EMC halls, and chemical benches that cannot be virtualized. Remote / Digital delivery, however, shows the fastest 6.9% CAGR, catalyzed by Guangdong and Zhejiang’s e-certificate APIs. TÜV Rheinland’s Virtual Expert app and China Leon Inspection’s blockchain portal cut downtime, letting inspectors handle more jobs per day. On-site services remain indispensable for heavy-equipment and construction audits but face stagnating demand outside megaprojects.

The synergy of IoT sensors, AR headsets, and real-time video helps remote modalities equal laboratory confidence levels, pushing the China testing inspection and certification market toward a hybrid model where digital tools pre-screen products before final lab confirmation.

Geography Analysis

Guangdong leads provincial revenue thanks to export-oriented manufacturers and the 35,000 m² STC lab that services Pearl River Delta exporters.[2]STC Group, “STC Guangdong Facility,” stc.group Shanghai ranks second, anchored by hydrogen, semiconductor, and biotech testing clusters plus the new 3,000 m³ vehicle EMC chamber. Beijing excels in software and cybersecurity certification, leveraging a concentration of AI talent despite salary premiums of up to USD 140,000. Zhejiang pioneers digital-government linkages that automate e-certificates, providing a field test for nationwide rollout.

Tier-two cities such as Chengdu, Wuhan, and Hangzhou attract investment via incentives for semiconductor and intelligent-manufacturing labs, spreading the China testing inspection and certification market beyond coastal hubs. Cross-border hot spots like Dongguan fuse customs data and QC reports through API gateways, substantially reducing clearance time. Provincial disparities in accreditation still require duplicate audits, yet overall regional competition fosters innovation and keeps service prices in check.

Competitive Landscape

Global majors, domestic innovators, and private-equity backed roll-ups create a dynamic but moderately concentrated field. SGS added digital trust, sustainability, and radio-chem labs via three acquisitions between 2024 and 2025, sharpening its edge in high-growth niches.[3]SGS, “Acquisitions 2024-2025,” sgs.com Bureau Veritas characterizes the worldwide arena as fragmented, which applies equally in China, where no firm controls an overwhelming share.[4]Bureau Veritas, “The TIC Market,” group.bureauveritas.com

Local champions differentiate through technology. China Leon Inspection uses AI vision to elevate throughput and blockchain to lock data integrity, securing double-digit growth. Niche specialists emerge in hydrogen storage and software similarity, areas left underserved by legacy players. Foreign entrants must navigate domestic preference clauses and multi-layered accreditation, whereas local firms still seek international credibility for exports. M&A is likely to continue as both global and Chinese players jockey for scale and new capabilities, shaping the next phase of the China testing, inspection, and certification market.

China Testing Inspection And Certification Industry Leaders

SGS-CSTC Standards Technical Services

Centre Testing International (CTI)

Pony Testing International

Intertek Testing Services Shanghai

China Certification and Inspection Group (CCIC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SAMR lab completes first 70 MPa hydrogen-cylinder fire test, closing a global standards gap

- January 2025: SGS acquires RTI Laboratories, Aster Global, and CertX to deepen environmental, GHG, and cybersecurity services

- December 2024: Nationwide e-fapiao platform goes live, integrating automated certification workflows

- October 2024: Certania buys MPR China Certification, signaling sustained foreign interest in Chinese market-access expertise

China Testing Inspection And Certification Market Report Scope

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

How large is the China testing inspection and certification market in 2025?

The China testing inspection and certification market size reached USD 50.92 billion in 2025.

What is the expected CAGR for China’s testing inspection and certification services through 2030?

The market is forecast to grow at a 5.71% CAGR between 2025 and 2030.

Which segment is expanding fastest within China’s testing inspection and certification services?

Certification services are projected to rise at a 6.2% CAGR through 2030.

Why are ESG audits growing quickly in China?

China’s pledge to achieve carbon neutrality by 2060 has prompted companies to seek third-party verification of emissions and sustainability data.

What regions dominate testing inspection and certification activity in China?

Guangdong, Shanghai, and Beijing collectively hold the largest revenue shares due to export intensity, hydrogen-testing investment, and cybersecurity specialization.

How fragmented is competition among testing inspection and certification providers in China?

No single player controls more than 15% of revenue, leading to a moderate fragmentation score of 5 out of 10.

Page last updated on: