South Korea Testing, Inspection, And Certification (TIC) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

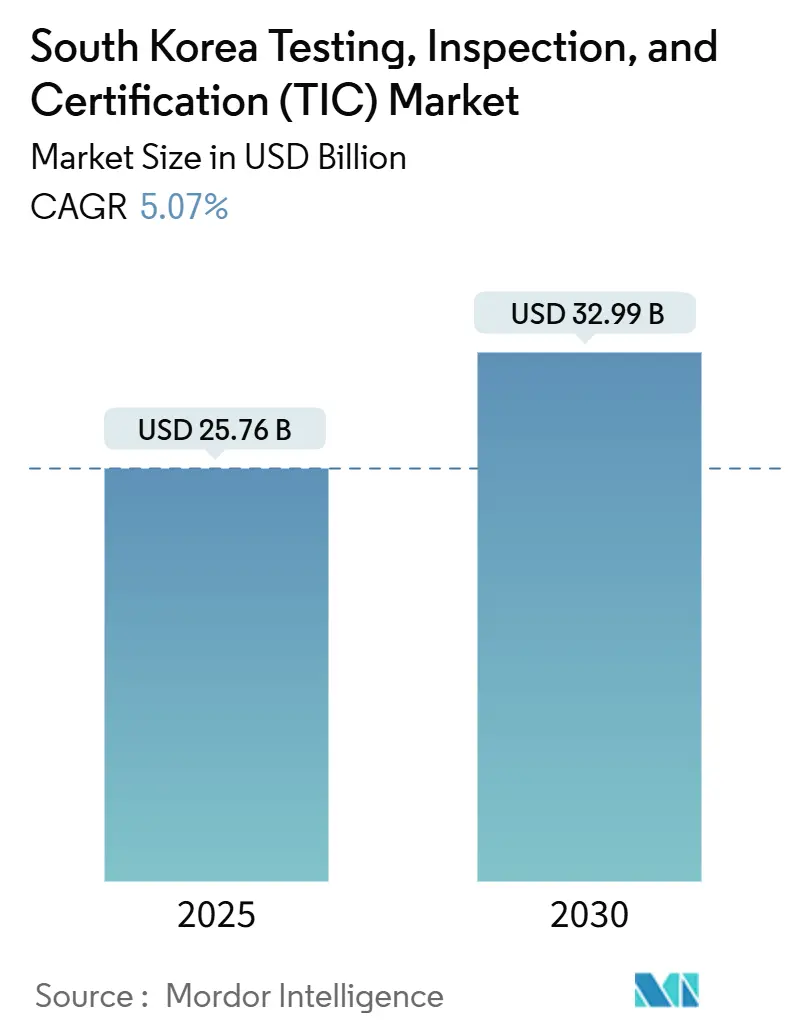

| Market Size (2025) | USD 25.76 Billion |

| Market Size (2030) | USD 32.99 Billion |

| Growth Rate (2025 - 2030) | 5.07% CAGR |

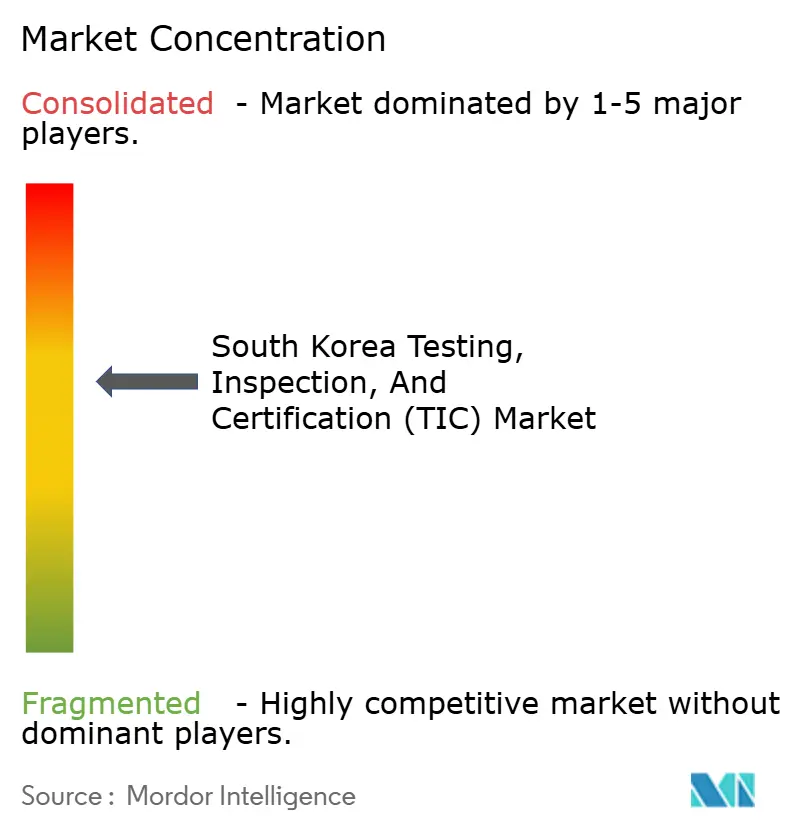

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Testing, Inspection, And Certification (TIC) Market Analysis by Mordor Intelligence

The South Korea Testing, Inspection, and Certification market size reached USD 25.76 billion in 2025 and is forecast to climb to USD 32.99 billion by 2030, translating into a 5.07% CAGR over the period. Robust export activity, ongoing semiconductor investment and the government’s low-carbon transition collectively sustain double-digit annual spending increases on quality-assurance programs, while accelerated digitalization creates new demand for software, cybersecurity and AI-device testing. Stricter multi-sector regulations, notably in healthcare, chemicals and construction, are lengthening certification timelines and raising the bar for technical documentation, which further boosts third-party inspection and audit requirements. Battery and hydrogen value chains add specialized safety and performance protocols that favor providers with deep materials science expertise. Simultaneously, e-commerce exporters, particularly beauty, food and consumer electronics brands, must clear multiple overseas conformity schemes, driving growth for firms that can deliver multi-jurisdictional compliance from a single service window.

Key Report Takeaways

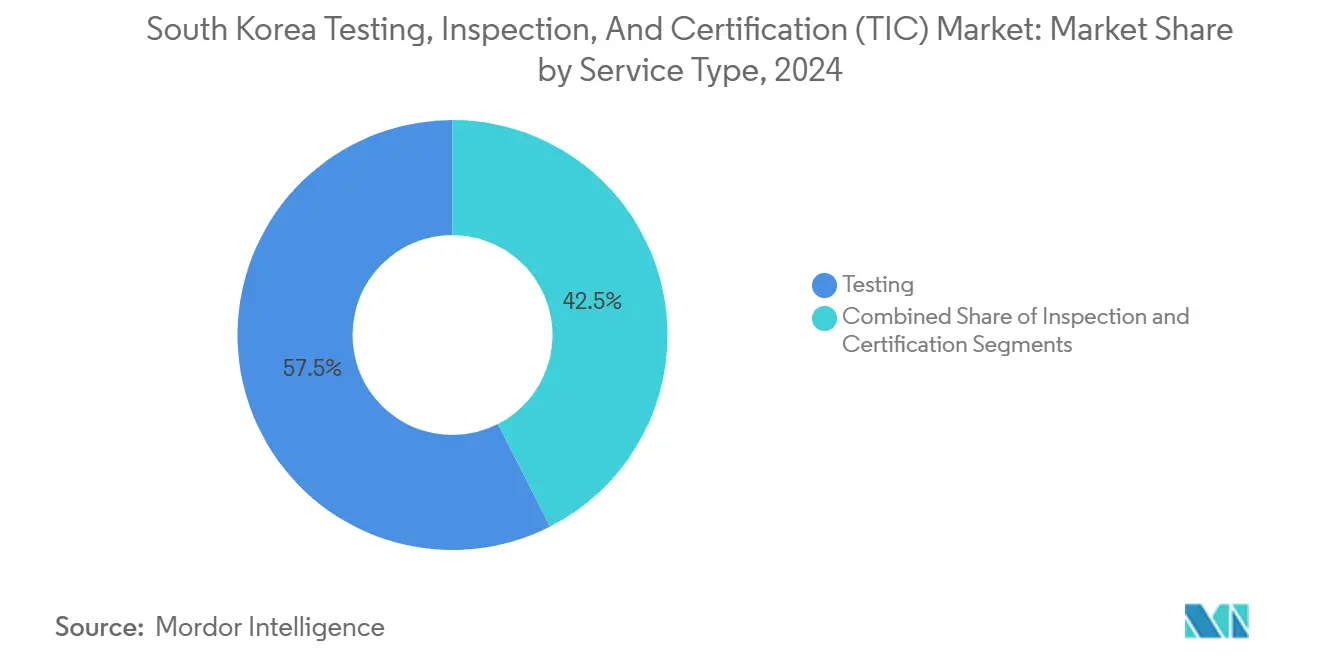

- By service type, testing services held 57.5% of the South Korea Testing, Inspection, and Certification market share in 2024, while certification services are projected to register the fastest 5.5% CAGR through 2030.

- By sourcing model, outsourced services accounted for 62.6% of the South Korea Testing, Inspection, and Certification market size in 2024 and are anticipated to expand at a 5.7% CAGR between 2025-2030.

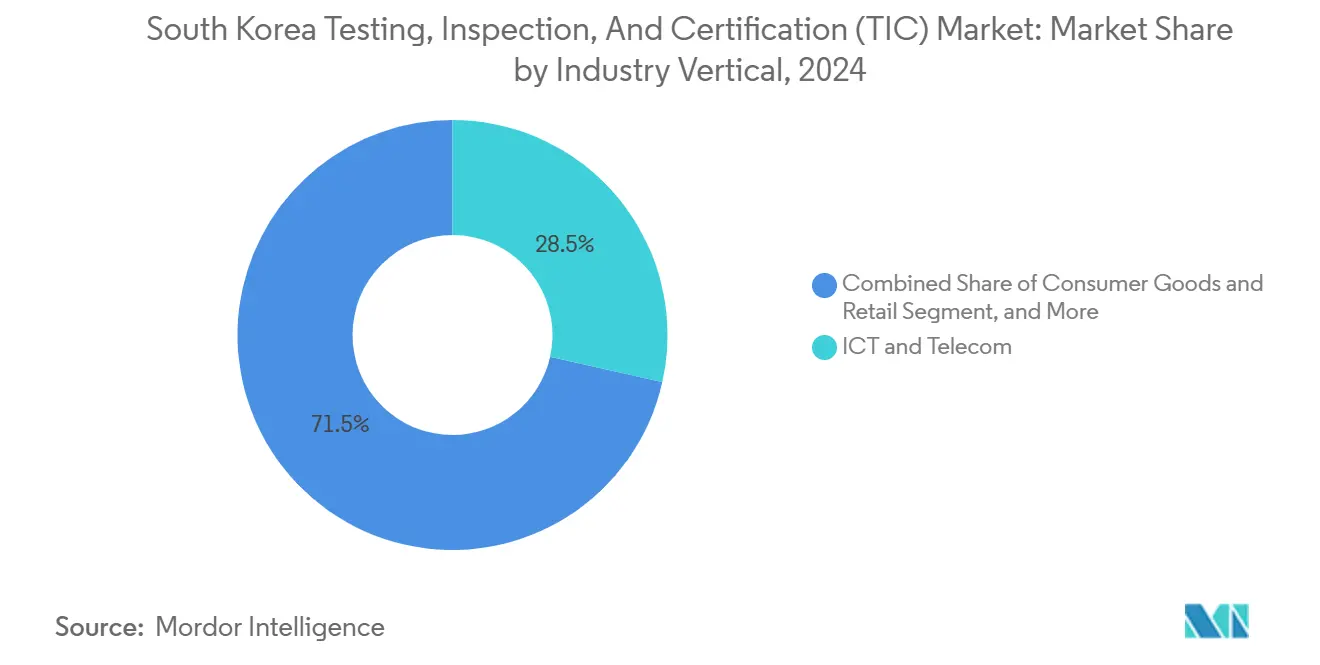

- By industry vertical, ICT and telecom captured 28.5% revenue share in 2024; life sciences and healthcare is tracking a 6.3% CAGR to 2030.

- By mode of delivery, on-site services represented 48.2% of the South Korea Testing, Inspection, and Certification market size in 2024, whereas remote and digital solutions are advancing at a 6.5% CAGR over the same period.

South Korea Testing, Inspection, And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter multi-sector regulations | +1.3% | National with export spillovers | Medium term (2-4 years) |

| Semiconductor and battery capacity boom | +1.2% | Gyeonggi and Chungcheong provinces | Short term (≤ 2 years) |

| Cross-border e-commerce export surge | +0.9% | National with North American and EU focus | Short term (≤ 2 years) |

| ESG and carbon-neutral mandates | +0.8% | Seoul and Busan early adopters | Medium term (2-4 years) |

| Hydrogen-economy safety pilots | +0.6% | Ulsan and Pohang | Long term (≥ 4 years) |

| AI-medical-device cybersecurity rules | +0.4% | Seoul metropolitan area | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Multi-Sector Regulations Drive Compliance Testing Demand

The Ministry of Food and Drug Safety broadened the Digital Medical Products Act in January 2025, extending pre-review to classification files and setting a 55-day approval clock at a KRW 524,000 (USD 400) fee, which compels device makers to undertake additional performance and cybersecurity evaluations before launch. The Korea Agency for Technology and Standards currently lists 207 certification schemes across 23 ministries, underscoring the complexity manufacturers must navigate. Mandatory construction-quality reports to the Construction Safety Information portal since July 2024 add another inspection layer for infrastructure contractors. Combined, these evolving statutes make external Testing, Inspection, and Certification expertise indispensable for timely market access.

Semiconductor and Battery Capacity Boom Accelerates Advanced Testing Needs

Samsung, LG and SK groups have collectively earmarked tens of billions of USD for new wafer fabs and battery lines through 2028, sharply increasing demand for contamination, reliability and functional safety testing. UL responded by opening an advanced battery laboratory in Gyeonggi province to support local electric-vehicle cell makers.[1]UL Solutions, “Advanced Battery Laboratory Opens in Korea,” ul.com Korea Testing Laboratory signed a cooperation pact with Germany’s VDE in April 2024 to jointly certify industrial AI applications and EV charging systems, highlighting how domestic providers leverage international alliances to cover emerging test items. These investments reinforce a virtuous cycle in which equipment upgrades at fabs translate into recurring verification contracts for Testing, Inspection, and Certification firms.

Cross-Border E-Commerce Export Surge Multiplies Certification Requirements

The Korea Customs Service’s Authorized Economic Operator program and export-voucher subsidies simplify logistics but heighten documentation checks, pushing beauty, food and consumer electronics brands to secure multiple destination-market certificates. MFDS export guidance on imported food safety obliges online sellers to furnish residue tests and hazard analyses before shipment. At the same time, Korea’s plan to restrict inbound goods lacking KC labels underscores reciprocity: domestic exporters must now prove equivalent compliance overseas. TIC providers with globally accredited labs therefore enjoy a competitive edge in winning bundled product, packaging and labelling assignments across North America and Europe.

ESG and Carbon-Neutral Mandates Create New Testing Categories

Revisions to K-REACH in August 2025 broadened disclosure obligations for chronic toxicity and eco-toxicity, requiring companies to submit additional analytical data for roughly 350 chemical substances. The updated Chemical Control Act introduces new volume thresholds for acute toxicity testing, driving a surge in outsourced environmental analytics. The Korea Environmental Preservation Institute gained authority to chair information-review committees, signaling a systematic ramp-up of compliance oversight. As firms pursue carbon neutrality by 2050, life-cycle assessments, greenhouse-gas verification and product-carbon-footprint labels form a growing slice of the South Korea Testing, Inspection, and Certification market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented accreditation landscape | -0.7% | National with recognition gaps | Medium term (2-4 years) |

| Costly advanced test equipment and talent gap | -0.5% | High-tech hubs nationwide | Short term (≤ 2 years) |

| EU Digital Product Passport mis-alignment | -0.3% | Export-oriented firms | Long term (≥ 4 years) |

| Data-localization burdens on remote Testing, Inspection, and Certification | -0.2% | Sensitive sectors countrywide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Accreditation Landscape Complicates Market Access

The Korea Laboratory Accreditation Scheme operates alongside industry-specific issuers such as KGS for gas equipment and KMA for medical analysis, forcing labs to pursue multiple certificates to serve a single client portfolio. Limited mutual-recognition agreements with overseas bodies mean parallel audits are often required before results are accepted in North America or the EU. The resulting duplication inflates costs and extends project lead times, posing a hurdle for medium-sized domestic providers that lack global office networks.

Costly Advanced Test Equipment and Talent Gap Constrain Capacity Expansion

High-frequency electromagnetic chambers, hydrogen explosion vessels and AI-red-team penetration rigs all demand multi-million-USD outlays. Smaller laboratories hesitate to invest without firm visibility on payback periods. Simultaneously, South Korea faces a shortage of certified functional-safety engineers and toxicologists, inflating wages and heightening staff turnover. This dual constraint slows the pace at which incremental capacity can come online, particularly in next-generation semiconductors, medical robotics and hydrogen applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Services Retain Core Volume while Certification Outpaces

Testing accounted for 57.5% of South Korea Testing, Inspection, and Certification market share in 2024, reflecting entrenched demand for destructive and nondestructive evaluations across automotive powertrain, smartphone components and petrochemical feedstocks. Certification, although only 15.2% of revenue, is forecast to record the fastest 5.5% CAGR through 2030 as policymakers embed third-party attestations deeper into export, ESG and safety statutes. The South Korea Testing, Inspection, and Certification market size linked to certification activities is projected to add over USD 2.1 billion during the outlook period, lifted by MFDS acceptance of Medical Device Single Audit Program certificates that shorten on-site factory audits and free manufacturer budgets for wider approval scopes. Inspection remains indispensable for cranes, pressure vessels and civil-works projects, yet its growth plateaus as digital-twin models replace some visual tasks with sensor-based monitoring.

Across all three services, the adoption of AI-assisted image analytics and remote-witness platforms accelerates turnaround times by up to 30%, encouraging clients to consolidate work with Testing, Inspection, and Certification firms offering end-to-end laboratory, field and system certification from a unified portal. Providers that couple legacy destructive testing with simulation-grade digital twins stand to capture disproportionate wallet share as complex assemblies such as solid-state batteries demand lifetime performance validation under accelerated-aging profiles.

By Sourcing Type: Outsourcing Gains Momentum as Compliance Requirements Multiply

Outsourced solutions represented 62.6% of the South Korea Testing, Inspection, and Certification market size in 2024 and are on track for a 5.7% CAGR through 2030 as companies prioritize variable-cost arrangements over in-house laboratory maintenance. Semiconductor fabs increasingly contract third-party particle-contamination audits because uptime penalties outweigh potential savings from internal staffing. Pharmaceutical and med-tech start-ups also outsource validation protocols to navigate MFDS quality-system expectations without building dedicated regulatory teams.

In-house departments remain widespread in top-tier chaebol groups, often covering routine incoming-materials checks and final assembly inspections. Nevertheless, even these vertically integrated conglomerates now tender specialized modules – for example, hydrogen embrittlement testing – to external experts due to equipment cost escalation. Testing, Inspection, and Certification providers that can issue globally recognized certificates, handle multi-language technical files and manage cross-border sample logistics rank highest in preferred supplier lists.

By Industry Vertical: ICT Dominance Persists while Healthcare Leads Growth

The ICT and telecom segment captured 28.5% of revenue in 2024, driven by continuous 5G antenna roll-outs, server-grade DRAM upgrades and consumer-device refresh cycles. Yet life sciences and healthcare is forecast to post the strongest 6.3% CAGR through 2030, adding close to USD 1 billion in incremental opportunity as population aging spurs implantable and diagnostic kit demand. The Digital Medical Products Act widens the definition of software-as-a-medical-device, requiring penetration and privacy testing for AI-driven algorithms before commercialization.[2]Ministry of Food and Drug Safety, “Digital Medical Products Act Enforcement,” mfds.go.kr

Automotive and transportation maintain double-digit test volumes amid rising EV penetration and the forthcoming United Nations Regulation No. 155 on cyber-security management. Petrochemicals, construction and consumer goods each supply steady project flows, though growth paces trail the national average as their regulatory frameworks stabilize. The South Korea Testing, Inspection, and Certification market size allocated to aerospace and defense is modest but strategic, benefiting from public-funded space-launch programs that must certify payload vibration, radiation and thermal tolerance.

By Mode of Service Delivery: Digital Models Scale Faster than On-Site Visits

On-site activities still produced 48.2% of revenue in 2024 because pressure vessel, bridge and fabrication inspections mandate human visual checks. However, remote and digital solutions are expanding 6.5% annually as optical-fiber sensors, IoT gateways and laboratory-information-management systems enable real-time data streams. Automated platforms cut manpower requirements for repetitive reliability testing and shorten root-cause analysis cycles by integrating metrology outputs with enterprise resource-planning data.

Off-site laboratories remain essential for high-precision chromatography, bio-burden assays and materials destructive testing that require tightly controlled environments. Hybrid delivery, combining edge-device monitoring with periodic human audit, stands out in smart-factory deployments where clients demand continuous oversight without daily site presence. As 5G private networks proliferate, video-witness protocols will further reduce engineer travel costs and extend Testing, Inspection, and Certification coverage to rural plants at competitive price points.

Geography Analysis

The South Korea Testing, Inspection, and Certification market is inherently national in scope because KATS, MFDS and other central agencies implement uniform regulations across all provinces. Nonetheless, industrial clustering produces distinct demand hot-spots. Seoul, Incheon and Gyeonggi harbor the bulk of ICT and medical-device test orders, benefiting from academic, design-center and venture-capital ecosystems. Ulsan and southeastern coastal zones generate steady petrochemical, shipbuilding and hydrogen-pilot inspection work, leveraging extensive port infrastructure. Chungcheong’s wafer and battery corridor depends on accredited micro-contamination and electro-chemical testing as fabs ramp 3-nanometer process nodes and high-nickel cathode lines.

In the southwest, the Jeolla provinces cultivate agritech and food-processing facilities, leading to concentrated microbiology, pesticide and labeling verification needs linked to rising agri-exports to ASEAN. Gangwon, though less industrialized, hosts renewable-energy projects that adopt remote condition-monitoring service bundles. Overall, the absence of regional regulatory variation keeps service offerings largely consistent, enabling Testing, Inspection, and Certification firms to scale centralized digital platforms without redesign for local statutes.

Competitive Landscape

The South Korea Testing, Inspection, and Certification market hosts a balanced mix of global majors and domestic specialists. SGS Korea, Bureau Veritas Korea and Intertek leverage global lab networks to service multinational OEMs, especially in ICT and automotive supply chains. Korea Testing Laboratory, Korea Testing and Research Institute and FITI Testing and Research Institute capitalize on government ties and local language support to secure public-tendered assignments and early access to new standards drafts. Market consolidation momentum is visible in high-capex verticals: VDE’s partnership with KTL accelerates mutual-recognition certificates for AI industrial systems and EV chargers, allowing both sides to share specialized chambers and algorithm benchmarking rigs.[3]VDE, “MoU with KTL on International AI Certification,” vde.com

Strategic themes include investment in AI-driven defect recognition, blockchain-secured certificate issuance and cloud LIMS. Domestic providers increasingly target Southeast Asian outposts to follow Korean manufacturing migration. International groups pursue bolt-on acquisitions – as seen in DKSH’s April 2025 purchase of MDxK – to embed life-science analytical capability locally. Meanwhile, the top ten players collectively control less than 55% of revenue, preserving moderate fragmentation even as technology hurdles rise.

South Korea Testing, Inspection, And Certification (TIC) Industry Leaders

SGS Korea Co., Ltd.

Bureau Veritas Korea Co., Ltd.

Korea Testing Laboratory (KTL)

Intertek Testing Services Korea Ltd.

Korea Testing & Research Institute (KTR)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DKSH Korea completed acquisition of MDxK, adding molecular-diagnostics and biobanking services to its portfolio.

- April 2025: VDE and Korea Testing Laboratory formed a pact to co-develop international certification for industrial AI and EV charging equipment.

- January 2025: MFDS implemented revised enforcement rules under the Digital Medical Products Act, extending pre-review coverage and adjusting fees.

- December 2024: Hyosung TNC acquired Hyosung Chemical’s specialty-gas division for KRW 920 billion (USD 642 million), increasing demand for ultra-high-purity gas verification.

South Korea Testing, Inspection, And Certification (TIC) Market Report Scope

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

How large is the South Korea Testing, Inspection, and Certification market in 2025?

It reached USD 25.76 billion in 2025, growing toward USD 32.99 billion by 2030 at a 5.07% CAGR.

Which service category generates the highest revenue?

Testing services lead with a 57.5% share, driven by semiconductor, automotive and chemical quality checks.

What is the fastest-growing service delivery model?

Remote and digital solutions are advancing at a 6.5% CAGR thanks to AI-powered analytics and lab automation.

Which industry vertical shows the strongest growth?

Life sciences and healthcare is projected to rise at a 6.3% CAGR due to stricter digital-health regulations.

Why are companies increasingly outsourcing Testing, Inspection, and Certification work?

Outsourcing offers access to specialized equipment and global accreditation without the fixed cost of in-house labs, supporting a 5.7% CAGR for external services.

How will carbon neutrality targets influence the market?

Expanded chemical-hazard disclosure and carbon-footprint labeling rules are generating new environmental testing streams, sustaining long-term demand growth.

Page last updated on: