Saudi Arabia Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

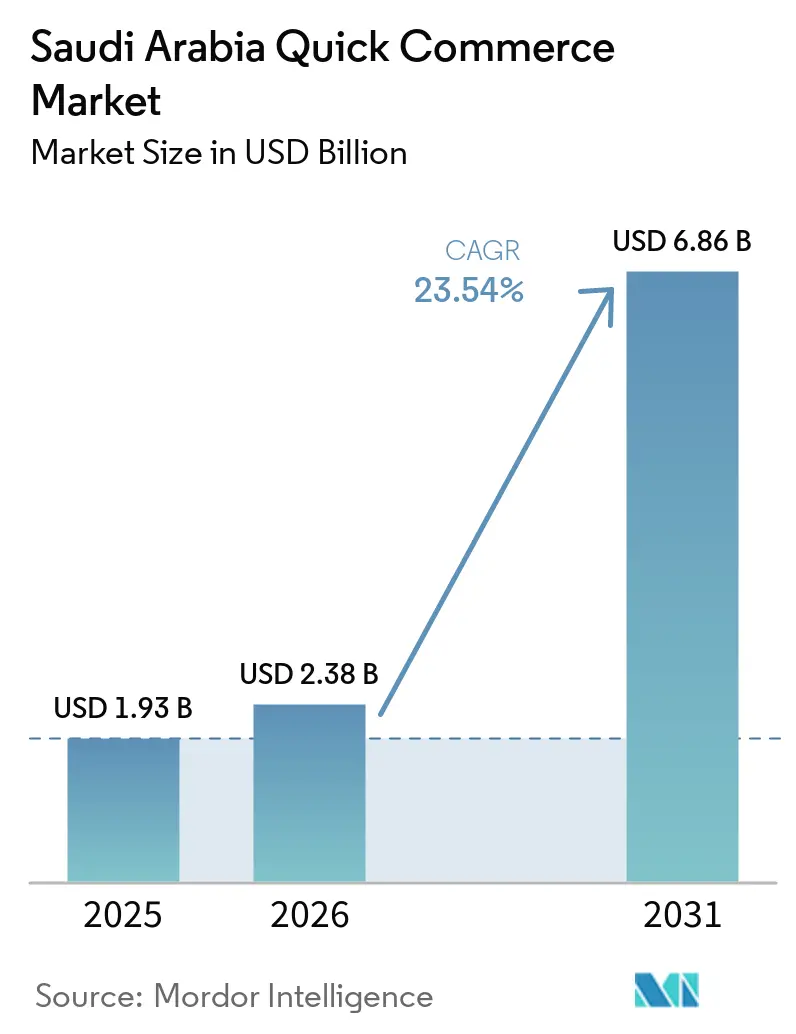

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 6.86 Billion |

| Growth Rate (2026 - 2031) | 23.54% CAGR |

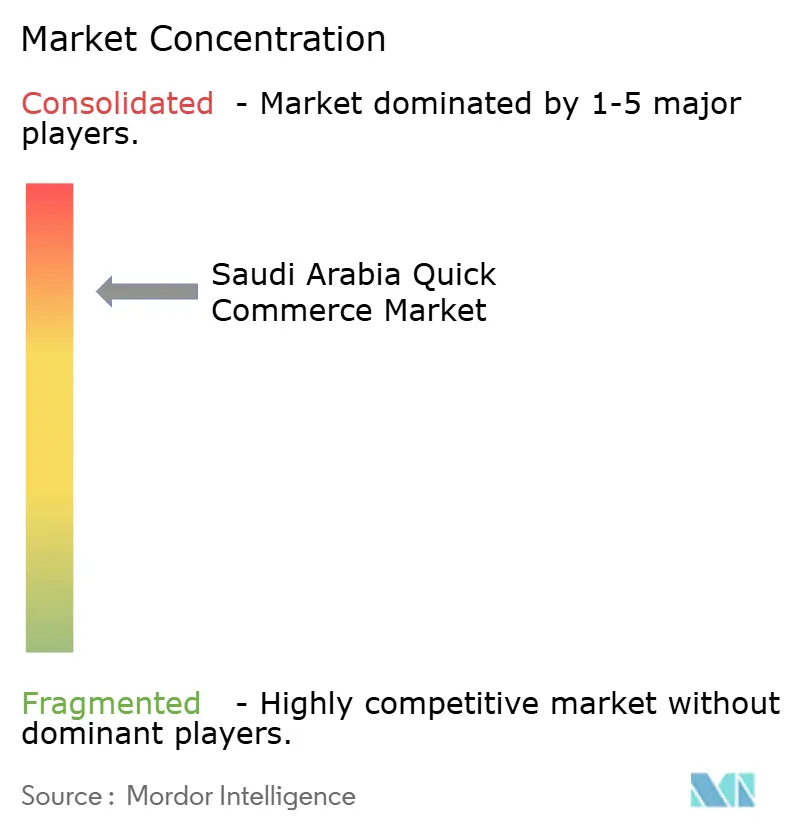

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Quick Commerce Market Analysis by Mordor Intelligence

The Saudi Arabia quick commerce market size expanded from USD 1.93 billion in 2025 to USD 2.38 billion in 2026 and is projected to reach USD 6.86 billion by 2031, registering a 23.54% CAGR across 2026-2031. Growth is accelerating because dark-store density now places inventory within a two-kilometer radius of most urban shoppers, while smartphone penetration above 95% and digital payment adoption near 80% have removed checkout friction. AI-driven forecasting systems lower stockouts by 80% and overstock by 35%, helping operators defend slender contribution margins. Autonomous delivery pilots, already approved in regulatory sandboxes, signal a future in which labor availability is less of a bottleneck. Ongoing Vision 2030 investments in 5G and last-mile infrastructure extend the serviceable footprint beyond the three largest cities, supporting scale without eroding delivery-time promises.

Key Report Takeaways

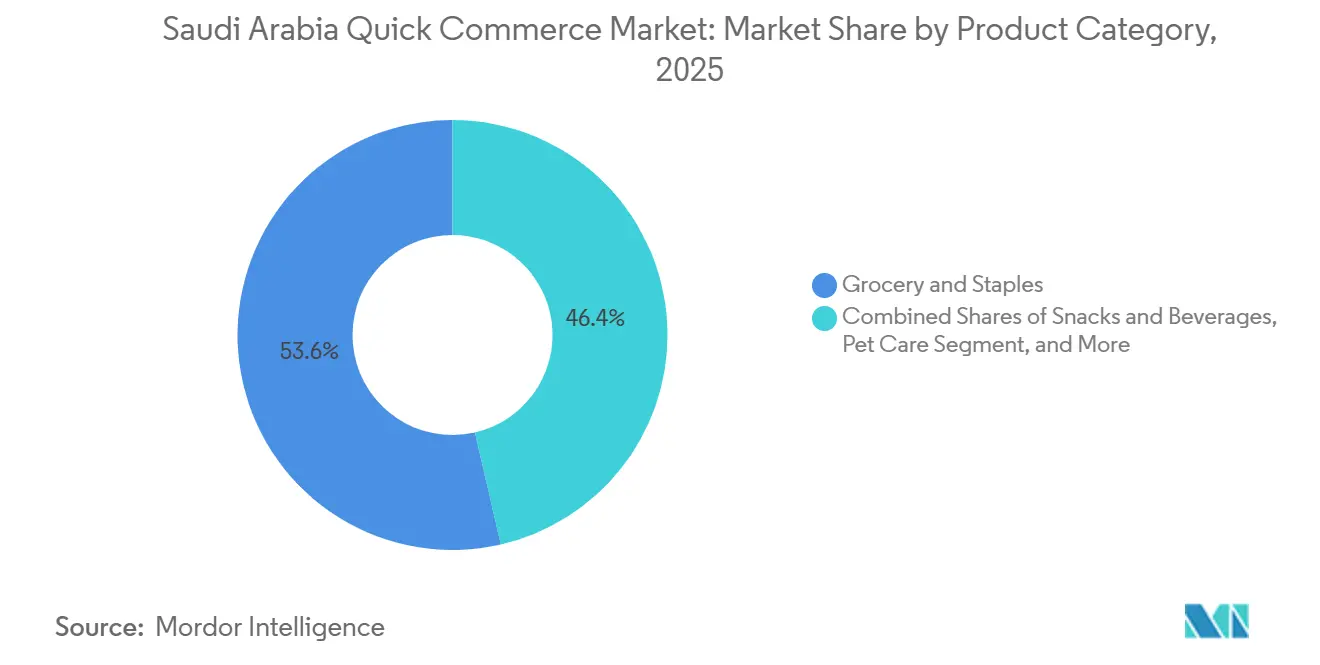

- By product category, Grocery and Staples held 53.61% of the Saudi Arabia quick commerce market share in 2025, while Pet Care is forecast to advance at a 23.78% CAGR through 2031.

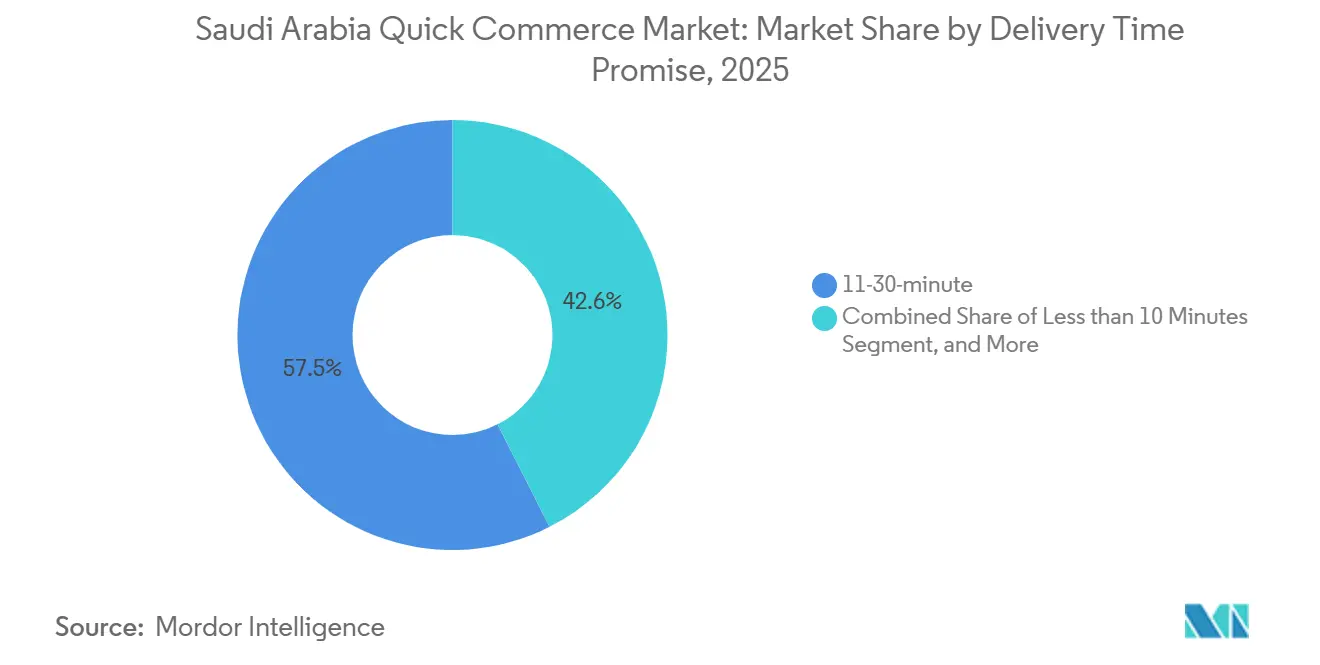

- By delivery time promise, the 11-30 Minutes segment accounted for 57.45% of the Saudi Arabia quick commerce market size in 2025, whereas the Less than 10 Minutes segment is predicted to grow at 24.05% across the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Dark-Store Networks | +6.8% | Riyadh, Jeddah, Dammam, spillover to Khobar and Makkah | Short term (≤ 2 years) |

| Increasing Smartphone Penetration and Digital Payments | +5.2% | National, strongest in Tier I metros | Medium term (2-4 years) |

| Mainstream Adoption of AI-Driven Demand Forecasting | +4.6% | National, led by Tier I and Tier II cities | Medium term (2-4 years) |

| Government Support for E-commerce Under Vision 2030 | +3.9% | National, infrastructure gains in Tier II and Tier III cities | Long term (≥ 4 years) |

| Rising Female Workforce Participation | +2.1% | Riyadh, Jeddah, Eastern Province | Long term (≥ 4 years) |

| Emergence of Ultra-Fast Last-Mile Start-ups | +1.8% | Tier I metros, pilot expansion into Tier II cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Dark-Store Networks

Operators continue to fund purpose-built micro-fulfillment hubs that compress delivery radii to under two kilometers, creating 10-30-minute service windows that traditional supermarkets cannot match. A leading grocery chain invested USD 390 million in automated facilities equipped with more than 250 mobile robots, while another third-party logistics firm committed SAR 100 million (USD 26.7 million) to a 400,000-square-foot center able to process 3.6 million orders monthly. A pure-play quick-commerce brand now runs more than 100 dark stores across 28 cities and targets USD 1 billion in 2026 revenue, showing that scale now depends on network reach rather than brand novelty. Hyper-local density slices last-mile costs by up to 40%, protects chilled and perishable categories, and pushes inventory turnover toward daily cycles.

Fintech Boom Enabling Cash-Less Instant Checkout

By 2025, 95-96% of residents owned smartphones and 99% enjoyed nationwide broadband coverage. Digital wallets embedded in Mada, Visa, and MasterCard rails drove mobile payments close to 80% of total digital transactions, cutting checkout times to under 30 seconds. Biometric security and one-click flows support impulse ordering, leading to app sessions averaging two to three purchases per week in Tier I cities. The result is a fundamental shift from planned weekly shops to on-demand top-ups, reinforcing the frequency advantage that underpins the Saudi Arabia quick commerce market.

Mainstream Adoption of AI-Driven Demand Forecasting

Machine-learning engines, now standard in inventory planning, integrate weather, traffic, local events, and social-media sentiment into SKU-level forecasts. Several operators recorded 80% stockout reductions and 35% overstock cuts after deployment, instantly improving unit economics in baskets that average SAR 50-150 (USD 13-40). A multinational technology firm rolled out a cuOpt-based platform in November 2025, targeting an USD 8.7 billion inventory gap across fast-moving goods. These capabilities allow real-time substitution suggestions and dynamic route optimization that sustain delivery-time promises during demand spikes.

Government Support for E-Commerce Under Vision 2030

More than USD 30 billion has been allocated to digital-economy infrastructure. The National Address System, fully enforced from January 2026, lowered failed deliveries by up to 20%. 5G coverage reached 78% in 2025 and is on track for 90% by 2027, enabling edge computing for autonomous fleets. Low-interest credit lines totaling SAR 500 million (USD 133 million) supported logistics start-ups that filled service white spaces in Tier II and Tier III cities. Transport regulators granted sandbox approvals for autonomous robots, signaling a policy environment that rewards technology adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Customer Acquisition Costs Amid Price Wars | -3.2% | National, most acute in Tier I metros | Short term (≤ 2 years) |

| Regulatory Uncertainty Around Gig-Economy Rules | -2.4% | National, enforcement variability by region | Medium term (2-4 years) |

| Supply-Chain Disruptions For Fresh Produce | -1.6% | Riyadh, Jeddah, Eastern Province | Short term (≤ 2 years) |

| Limited Profitability Due To Small Basket Sizes | -1.9% | National, severe in dense urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Customer Acquisition Costs Amid Intense Price Wars

Free delivery became table stakes during 2025, with discount campaigns pushing contribution margins to USD 0.36 on a USD 18 order. One challenger exited in October 2025 and another entered court-approved reorganization in April 2026 after raising more than USD 200 million. Subscription programs slashed annual fees from SAR 228 to SAR 58 (USD 60.80 to USD 15.50) to slow churn, yet escalating promotions failed to deter shoppers from testing rival apps. Draft anti-predatory pricing guidelines issued in February 2026 indicate regulators may intervene if unsustainable incentives threaten long-term market health.

Regulatory Uncertainty Around Gig-Economy Labor Rules

The Unified Employment Contract Initiative, active since October 2025, requires wage disclosure through Najiz and shifts riders toward formal employment. Initial estimates show per-delivery labor costs rose 20-25% as operators absorbed social insurance and compliance overhead. A concurrent ban on non-Saudi self-employment in delivery roles phased in over 14 months, creating short-term capacity gaps. Although large platforms can scale recruitment programs, smaller start-ups face rising fixed costs and administrative complexity that may delay break-even timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Staples Lead While Pet Care Accelerates

Grocery and Staples generated 53.61% of 2025 revenue, confirming that bulk-buy items anchor repeat purchase behavior in the Saudi Arabia quick commerce market size. Perishables such as Fresh Produce and Dairy benefit from sub-30-minute fulfillment, mitigating spoilage during peak summer temperatures that exceed 45°C. Snacks and Beverages continue to thrive on impulse orders set off by in-app push notifications.

Pet Care has emerged as the fastest growing category, poised for a 23.78% CAGR through 2031 as dual-income households adopt premium nutrition and home-delivery of veterinary supplies. Personal Care and OTC Pharma gained traction after streamlined over-the-counter approvals in 2025. Niche verticals like Electronics and Accessories, Flowers and Gifts, and Home Cleaning Supplies display smaller bases yet deliver higher margins, providing a path to diversify beyond low-margin staples in the Saudi Arabia quick commerce market.

By Delivery Time Promise: 11-30 Minutes Dominates, Sub-Ten Minutes Gains Pace

The 11-30-minute window claimed 57.45% of 2025 orders, balancing customer expectations with fleet utilization. Operators often colocate dark stores with mixed-use developments, allowing couriers to batch multiple drops per run. This model includes costs without diluting the speed proposition at the heart of Saudi Arabia's quick commerce market share.

Less than 10 minutes is scaling at a 24.05% CAGR, powered by dense micro-fulfillment footprints and AI-driven dispatch that positions riders within two kilometers of live demand clusters. Sub-urban and Tier II markets gravitate to 31-60 minute slots where lower population density would otherwise inflate delivery fees. Autonomous robots deployed in gated commercial areas are now testing high-frequency lanes to shave additional minutes from pick-up to drop-off.

Geography Analysis

Riyadh, Jeddah, and Dammam together generated more than 60% of the 2025 demand. Riyadh stands out for swift market-entry strategies, including one new entrant that secured 50% citywide coverage within six weeks of launch by leveraging predictive heat maps and real-time route optimization. Jeddah’s role as a logistics gateway to Makkah and Madinah produces seasonal spikes of up to 40% during religious events, testing the cold chain's integrity for fresh categories.[1]Saudi Food and Drug Authority, “Cold Chain Requirements for Perishables,” sfda.gov.sa Dammam benefits from higher expatriate earnings, which translate into larger basket sizes, while the January 2026 enforcement of standardized addresses improved on-time delivery accuracy across all three metros.

Tier II cities such as Khobar, Makkah, Madinah, Tabuk, and Buraidah are expanding rapidly, thanks to 78% 5G coverage reached in 2025, expected to climb to 90% by 2027. Low-interest financing of SAR 500 million (USD 133 million) helped logistics start-ups seed dark stores in areas where population density is just half that of Riyadh. Religious tourism accounts for as much as 50% of annual volume in Makkah and Madinah, compelling platforms to design pop-up micro-fulfillment hubs that scale capacity in line with pilgrimage calendars.

Tier III and smaller municipalities, Najran, Jizan, and Hail among them, face sparse densities and lower digital payment uptake, yet the Saudi Arabia quick commerce market now reaches these zones as the National Address System edges final-mile clarity. Sandbox approvals for autonomous robots create opportunities to leapfrog labor shortages, and state-backed lines of credit support cold-chain upgrades required to handle fresh produce during summers when external temperatures soar above 50°C. These advances position smaller cities as the next frontier of value creation.

Competitive Landscape

The Saudi Arabia quick commerce market remains highly concentrated: the three largest platforms, Keeta, Jahez, and HungerStation, commanded more than 90% share in Q3 2025.[2]Bloomberg News, “Ninja Raises USD 250 Million at USD 1.5 Billion Valuation,” bloomberg.com Intense price pressure forced one mid-tier brand to exit in October 2025 and pushed another into court-supervised restructuring by April 2026. In contrast, Ninja secured USD 250 million in Series C funding at a USD 1.5 billion valuation and reported core operating profitability by July 2025, aided by 100 dark stores and AI-enabled inventory planning.

Jahez strengthened its 32% market position through two 2025 moves: acquiring 76.56% of Qatar-based Snoonu for USD 245 million and integrating noon Minutes into its application stack, a reciprocal linkage that routed orders through the nearest fulfillment node regardless of brand.[3]Jahez International Company, “Investor Presentation 2025,” jahez.com A grocery retailer investing USD 390 million in robotics-driven dark stores signaled traditional chains will compete head-on with app-native operators.

Strategic differentiation now hinges on technology adoption. Autonomous delivery pilots under Transport General Authority oversight showcase Level 4 robots equipped with 20+ sensors and 6 cameras. A fintech-powered inventory platform rolled out in November 2025 uses GPU-accelerated solvers to close an USD 8.7 billion stock-level gap, demonstrating the importance of data science in squeezing margin from sub-USD 20 baskets. New entrants must therefore bring either proprietary software or specialized category depth to erode incumbent share in the Saudi Arabia quick commerce market.

Saudi Arabia Quick Commerce Industry Leaders

Jahez International Company

Nana Direct

HungerStation

Mrsool International Company

Noon Minutes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Nana Direct began financial reorganization after mounting customer-acquisition costs eroded unit economics even with SAR 50-150 (USD 13-40) average baskets.

- March 2026: Moroccan fresh-produce shipments were halted, forcing Kuwait to reroute via Saudi Arabian corridors and highlighting cold-chain stress during peak temperatures.

- February 2026: The General Authority for Competition published draft guidelines aimed at curbing predatory pricing and exclusivity clauses to protect long-term sector viability.

- January 2026: Mandatory compliance with the National Address System had reduced failed deliveries by up to 20% and had enabled tighter delivery-time guarantees nationwide.

Saudi Arabia Quick Commerce Market Report Scope

The Quick Commerce Market in Saudi Arabia represents a rapidly expanding segment within the country's retail and e-commerce industry. It is characterized by ultra-fast delivery of consumer goods, typically within 30 minutes to a few hours. This market leverages advanced technology platforms, strategically positioned warehouses, and highly efficient logistics networks to meet consumer demand.

The Saudi Arabia Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and More), Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the current value of the Saudi Arabia quick commerce market?

The Saudi Arabia quick commerce market size reached USD 2.38 billion in 2026 and is projected to hit USD 6.86 billion by 2031, according to Mordor Intelligence.

Which product segment is growing fastest within Saudi quick commerce?

Pet Care is the fastest growing category, expected to post a 23.78% CAGR through 2031 as urban households shift pet-supply purchases online.

How concentrated is competition among quick-commerce operators?

The top three platforms command more than 90% of market share, indicating an oligopoly with a market-concentration score of 7.

What delivery-time window holds the largest order share?

The 11-30-minute promise leads, capturing 57.45% of 2025 orders due to its balance between speed and cost efficiency.

How are new labor regulations affecting delivery platforms?

Formal wage contracts and nationality requirements introduced in 2025 have raised per-delivery labor costs by up to 25%, pressuring margins especially for smaller players.

Page last updated on: