Hong Kong Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

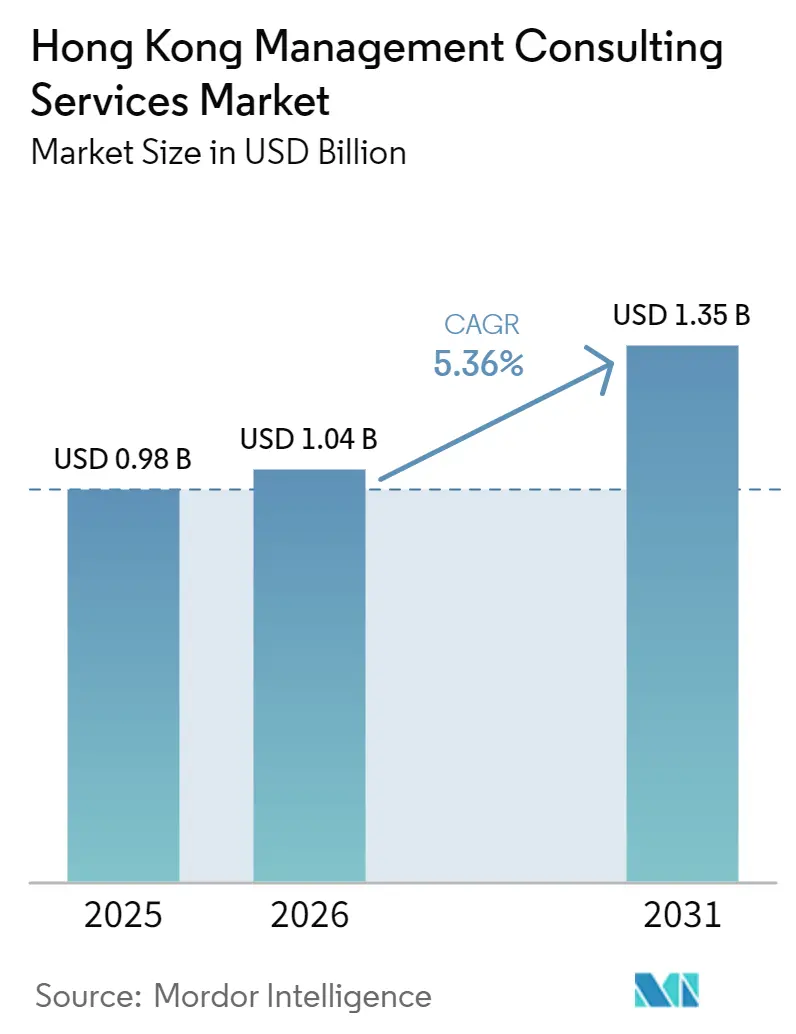

| Base Year Market Size (2025) | USD 0.98 Billion |

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

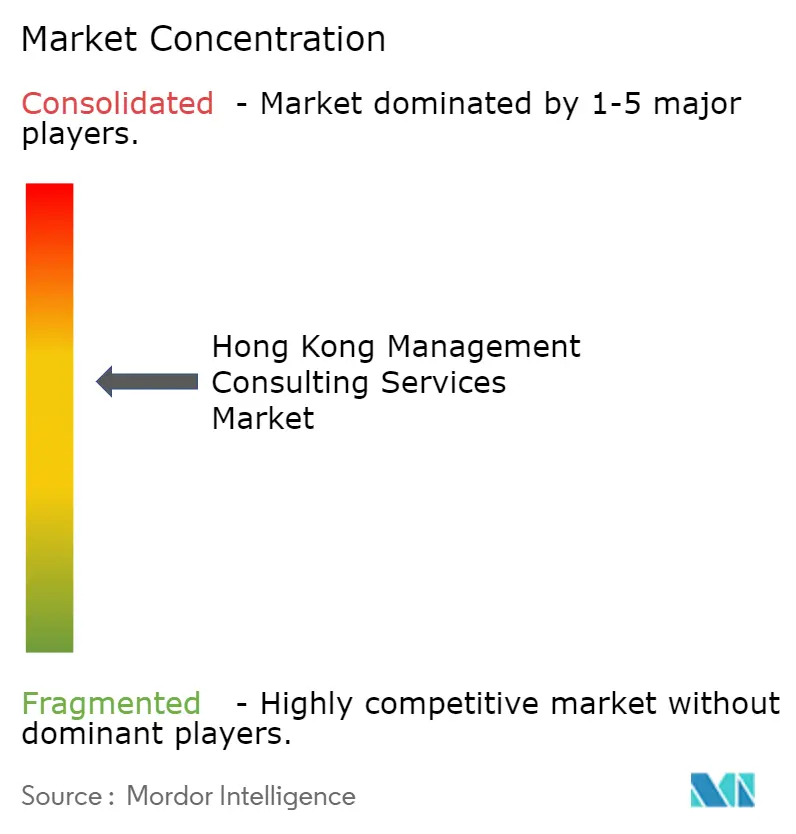

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Management Consulting Services Market Analysis by Mordor Intelligence

The Hong Kong management consulting services market size is expected to increase from USD 0.98 billion in 2025 to USD 1.04 billion in 2026 and reach USD 1.35 billion by 2031, growing at a CAGR of 5.36% over 2026-2031. Rising digital adoption, mounting regulatory obligations, and government subsidies continue to expand advisory demand across both multinational groups and local enterprises. Large banks and insurers still anchor spending, yet small and medium-size enterprises now enter the client pool in higher numbers thanks to public funding that offsets technology-upgrade costs. The pivot away from strategy-only mandates toward multi-year implementation work is visible in the rapid uptake of cloud migration, artificial intelligence model deployment, and real-time analytics dashboards. Intense talent scarcity and steep office rents sustain high billing rates, while Mainland policy volatility simultaneously creates episodic pauses in discretionary projects and new opportunities in restructuring and scenario planning.

Key Report Takeaways

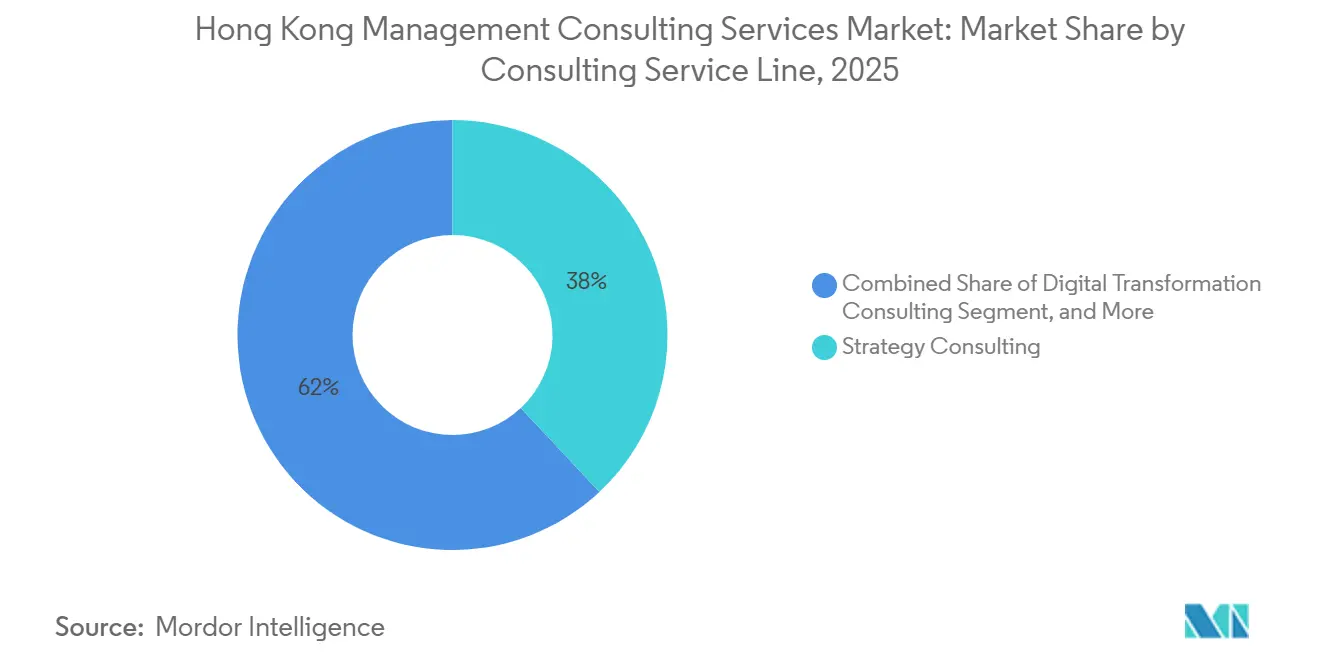

- By consulting service line, strategy consulting led with 38.02% share of the Hong Kong management consulting services market size in 2025, whereas digital transformation consulting is projected to post the fastest 5.89% CAGR through 2031.

- By organization size, large enterprises accounted for 62.89% of 2025 spending, while small and medium-size enterprises record the highest 5.67% CAGR on the back of subsidy-driven technology upgrades.

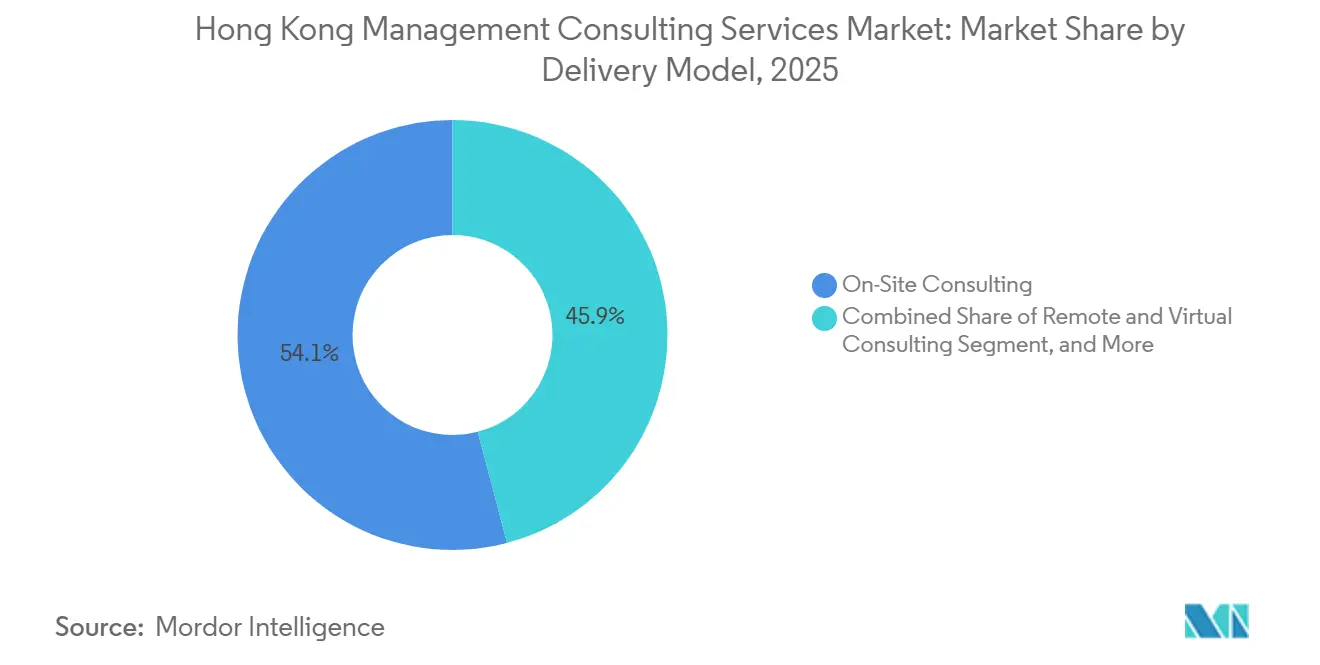

- By delivery model, on-site engagements retained 54.07% share of the Hong Kong management consulting services market share in 2025, but remote and virtual delivery is expanding at a 5.76% CAGR as secure collaboration platforms gain acceptance.

- By end user, banking and insurance contributed 21.82% of 2025 revenue of the Hong Kong management consulting services market, whereas healthcare is forecast to expand at a 5.92% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Hong Kong Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Backed Digital Transformation Incentives | +0.8% | Hong Kong, spillover to Greater Bay Area SMEs | Medium term (2-4 years) |

| Rising Demand for Operational Efficiency Amid High Business Costs | +0.7% | Hong Kong central business districts | Short term (≤ 2 years) |

| Regulatory Complexity in Hong Kong’s Financial Services Sector | +0.6% | Territory-wide, cross-border implications | Long term (≥ 4 years) |

| Post-Pandemic Restructuring and Mergers and Acquisitions Waves | +0.5% | Hong Kong regional M&A hub | Medium term (2-4 years) |

| Growing ESG Disclosure Mandates Driving Sustainability Consulting | +0.4% | Hong Kong-listed companies | Medium term (2-4 years) |

| Tokenization of Assets and Web3 Policy Sandbox Fueling Niche Advisory Demand | +0.3% | Financial services and fintech platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Digital Transformation Incentives

An initial HKD 500 million (USD 64 million) Digital Transformation Support Pilot Programme launched in 2024 offers one-to-one matching subsidies of up to HKD 50,000 (USD 6,400) per enterprise. By February 2026, 8,799 small and medium-size enterprises had secured grants, most of them in retail and food services.[1]Innovation and Technology Bureau, “LCQ2: Measures to Support Digital Transformation of Small and Medium Enterprises,” Hong Kong Government, info.gov.hk A further HKD 300 million (USD 38 million) top-up scheduled for late 2026 will add artificial intelligence and cybersecurity solutions to the eligible list, lowering price barriers for consultancies pitching cloud migration and data-security projects. The earlier Technology Voucher Programme, which closed in 2024 after 38,440 approvals, demonstrated strong appetite for digitization funding and set precedent for simplified paperwork. Advisory firms that bundle grant-application support with technical delivery capture larger fee pools and shorten sales cycles. Together, these incentives widen the Hong Kong management consulting services market by converting previously price-sensitive SMEs into active buyers.

Rising Demand for Operational Efficiency Amid High Business Costs

Monthly office rents topping HKD 150-200 (USD 19-26) per square foot in Central and salary inflation of 5-8% annually push enterprises to seek rapid cost wins. Hospitals install artificial intelligence diagnostics to shrink radiology queues, while banks leverage real-time credit data pipes that compress underwriting from weeks to days. Consultants respond by embedding robotic process automation and natural-language search into client workflows, shifting value from slide decks to hands-on build-and-run engagements. Acute hiring challenges, 97% of C-suite respondents struggled to fill specialist roles in late 2025, make external teams an attractive variable-cost alternative. This cost-efficiency priority sustains near-term demand even when discretionary budgets tighten.

Regulatory Complexity in Hong Kong’s Financial-Services Sector

Four separate regulators issued 1,152 actionable updates between August 2020 and February 2025, covering anti-money-laundering, climate risk, operational resilience, and virtual-asset licensing. A HKD 9 million (USD 1.2 million) fine in January 2026 underscored stricter enforcement, pushing banks and brokers to outsource rule-mapping, control design, and monitoring.[2]PwC Hong Kong, “Compliance Challenges and Solutions for Hong Kong’s Financial Services Sector,” PwC, pwchk.com Upcoming virtual-asset rules aligned with traditional licences create immediate advisory opportunities around custody architecture and financial-resource thresholds. Firms combining legal interpretation with systems integration translate these moving targets into multi-year managed-service retainers rather than episodic compliance gap checks.

Post-Pandemic Restructuring and Mergers and Acquisitions Waves

Mainland mergers and acquisitions surpassed USD 400 billion in 2025, and roughly three-quarters of Mainland corporates use Hong Kong as their offshore launchpad. The Hong Kong Stock Exchange expects about 150 new listings in 2026, sustaining demand for diligence, valuation, and post-merger integration work. Advisory firms deploy artificial-intelligence tools that review contracts and financials at scale, accelerating deal timelines and highlighting synergy risks. Investment commitments such as a HKD 500 million (USD 64 million) capacity-building initiative by a major Big Four network signal long-term confidence, even as policy swings occasionally pause transactions.[3]Alpha Intellect Limited, “Digital Transformation in 2025: Trends and Strategies for Hong Kong SMEs,” Alpha Intellect, alphaintellect.com.hk

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Shortage and Fee Inflation | -0.6% | Territory-wide with hotspot in AI and cybersecurity skills | Short term (≤ 2 years) |

| Expansion of In-House Strategy Teams | -0.5% | Large banks, insurers, conglomerates | Medium term (2-4 years) |

| Data-Residency and Cybersecurity Constraints on Cloud Tools | -0.3% | Regulated financial institutions | Medium term (2-4 years) |

| Volatile Mainland China Policy Shocks Raising Client Risk Aversion | -0.4% | Cross-border projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent Shortage and Fee Inflation

The 51,452 vacancies logged in late 2025 created a seller’s market for consultants versed in artificial intelligence, cybersecurity, and environmental risk. Salary expectations rose 15-25% above historical norms, pushing partner billing to HKD 5,000-15,000 (USD 640-1,920) per hour. Clients respond by trimming project scope or blending in-house staff with external experts.[4]Consultancy Asia Editors, “Deloitte China Launches HK LEAP Initiative with HKD 500 Million Investment,” Consultancy Asia, consultancy.asia Larger networks open offshore delivery hubs and invest in internal academies to soften wage pressure, but the short-term squeeze halves discretionary spend among cost-sensitive buyers and limits Hong Kong management consulting services market acceleration.

Expansion of In-House Strategy Teams

Survey evidence shows 67% of enterprises bolstering internal strategy benches to cut external fees by up to 40%. Tech titans and global banks already employ triple-digit strategist headcounts, handling routine transformation and regulatory tasks themselves. External advisers therefore must differentiate through proprietary data assets, advanced technology platforms, or niche domain depth. The hybrid model, internal execution plus external specialist input, shrinks addressable wallet share for generic process work, tempering market growth in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Outpaces Strategy

Strategy consulting captured 38.02% revenue in 2025, reflecting historic entry into C-suite agendas. Yet the Hong Kong management consulting services market size attached to digital transformation projects is set to compound at 5.89% annually as clients prioritize executable technology roadmaps. Artificial intelligence model deployment, cloud migration, and data-civilization initiatives dominate new statements of work, with consultants often contracted for end-to-end delivery rather than blueprint creation. Operations consulting also benefits because rising rents and wage inflation steer enterprises toward process automation that promises visible savings inside 12 months.

Risk and compliance engagements expand in tandem with the 1,152 regulatory updates issued since 2020. Automated rule-mapping tools and continuous-monitoring dashboards now sit alongside traditional control refresh projects, raising average deal values. Sustainability advisory grows quickly as International Financial Reporting Standards S1 and S2 reinforce Scope 3 disclosure deadlines. Firms bundling carbon accounting with investor-relations coaching win longer mandates, while tokenization and Web3 sandbox rules create boutique opportunities for lawyers-turned-technologists. Altogether, revenue concentration is tilting toward service lines able to combine domain knowledge with systems integration capability, reshaping the Hong Kong management consulting services market share landscape.

By Organization Size: Subsidized Digitization Lifts SMEs

Large enterprises generated 62.89% of 2025 fees as banks, insurers, and conglomerates steered complex cross-border programs. They remain top spenders on multi-year compliance, merger integration, and innovation-hub buildouts. However, the small and medium-size enterprise cohort is the fastest-growing slice of the Hong Kong management consulting services market size, advancing at a 5.67% CAGR thanks to grant schemes that cover up to half the bill for customer-relationship platforms, e-commerce systems, and cyber-defense tools. More than 8,700 SMEs have already collected subsidies, and a planned HKD 300 million (USD 38 million) extension will widen eligibility to artificial intelligence and cybersecurity projects.

Modular service packs, fixed-fee menus, and bundled grant paperwork lower friction for first-time consulting buyers. Boutique advisers with deep vertical know-how, such as reservation-system rollouts for food and beverage operators, often edge out global firms on cost and cultural fit. As subsidies expand, a growing long-tail of micro engagements fragments the market and challenges larger networks’ pyramidal staffing models. Nevertheless, spill-over benefits accrue to major players that form channel partnerships with software vendors courting subsidy-backed SMEs.

By Delivery Model: Hybrid Consulting Becomes Norm

On-site assignments continued to dominate with 54.07% share in 2025 because senior-executive workshops and regulatory fieldwork still demand face-to-face interaction. Yet remote engagements are advancing at a 5.76% CAGR, underpinned by secure video platforms and artificial-intelligence project trackers that compress review cycles. Hybrid structures, initial in-person alignment followed by virtual execution, now represent the default for mid-sized scopes, balancing relationship depth with cost efficiency.

Regulated sectors such as banking and healthcare still insist on some physical attendance for data-room inspections and board hearings. Conversely, tech startups and professional services clients accept fully remote advisory, accelerating delivery speeds. Investments in proprietary collaboration suites and encrypted file-sharing reinforce competitive differentiation, enabling firms to scale cross-border teams without incremental travel expense. As a result, remote capacity expands the total addressable client pool and redistributes Hong Kong management consulting services market share toward firms that mastered digital-first delivery.

By End-user Industry: Healthcare Transformation Spurs Advisory Demand

Banking and insurance remained the largest vertical with 21.82% of 2025 revenue, buoyed by tokenized-bond pilots, wholesale central-bank digital currency sandboxes, and virtual-asset licensing frameworks. Continuous anti-money-laundering upgrades and climate-risk stress tests ensure steady demand for compliance and data-engineering support. Healthcare, in contrast, is forecast to rise at a 5.92% CAGR through 2031 as the Hospital Authority executes a HKD 3 billion (USD 385 million) digital road map that spans telemedicine, artificial-intelligence diagnostics, and unified patient-record portals.

Information technology and telecom companies invest in network modernization and cybersecurity, while public-sector agencies pursue over 130 Smart City Blueprint 2.0 initiatives. Manufacturing clients tap re-industrialization funds to adopt robotics and Internet of Things solutions, opening project mandates for supply-chain digital twins and factory-floor analytics. The retail and logistics segments seek omnichannel upgrades and last-mile optimization, frequently leveraging matching grants to finance consultant engagement. This diversity of demand underpins stable growth across the Hong Kong management consulting services market despite macro uncertainty.

Geography Analysis

The Special Administrative Region serves as both a domestic market and a conduit for 77-80% of Mainland corporates expanding globally. Its common-law structure and free-capital regime make it the preferred headquarters for Asia-Pacific treasury and risk functions, sustaining consulting demand in banking, treasury, and tax structuring. At the same time, Greater Bay Area integration calls for supply-chain harmonization, workforce mobility schemes, and digital-identity interoperability encompassing Guangdong and Macau.

The HKD 150 billion (USD 19.2 billion) Northern Metropolis plan envisions an innovation corridor focused on artificial intelligence, life sciences, and advanced manufacturing. Associated infrastructure and research-cluster spending promises a multi-year pipeline of ecosystem-design, public-private partnership, and sector-mapping engagements. Fiscal reserves equal to 10 months of expenditure underpin these capital-intensive programmes, shielding advisory budgets from cyclical volatility.

Mainland policy swings, property-sector defaults or data-security crack-downs, occasionally delay discretionary projects but simultaneously stimulate restructuring and scenario-planning assignments. The relocation of about 50,000 professionals to Hong Kong under talent schemes supplies bilingual consultants adept at navigating civil-law and common-law frameworks. Firms operating dual offices in the SAR and Mainland tier-one cities therefore command an outsized portion of cross-border mandates, reinforcing the Hong Kong management consulting services market’s role as a regional hub.

Competitive Landscape

Global strategy houses, Big Four networks, and technology integrators collectively dominate large-ticket engagements, but boutique specialists continue to secure niche wins. The top five groups command a significant, though not overwhelming, slice of revenue, positioning the market in moderate-concentration territory. Brand equity, proprietary benchmarks, and entrenched C-suite relationships allow incumbents to defend premium pricing, yet rising client appetite for execution capability favors firms able to offer technology build-outs alongside strategy advice.

Acquisitions and lateral hiring remain the primary responses to talent shortages. A Big Four firm’s HKD 500 million (USD 64 million) LEAP program aims to create 1,000 digital roles over four years, while mid-tier entrants open Hong Kong branches to capture public-affairs and sustainability work. RegTech vendors embed automated compliance tools that cannibalize manual rule-mapping hours, prompting traditional advisors to license or acquire such platforms. Offshore delivery centers in lower-cost cities extend capacity and improve price competitiveness, but premium partner time in the SAR retains its price point due to client preference for local oversight.

White-space domains, tokenized-asset custody, Scope 3 supply-chain emissions tracking, quantum-safe encryption, are still under-served. Early movers build defensible positions by publishing reference architectures, training certification cohorts, and co-developing regulatory sandboxes with authorities. Overall, the competitive landscape evolves toward blended professional-services and technology-product offerings, driving re-segmentation within the Hong Kong management consulting services market.

Hong Kong Management Consulting Services Industry Leaders

McKinsey and Company, Inc.

Boston Consulting Group, Inc.

Bain and Company, Inc.

Deloitte Touche Tohmatsu Limited

PricewaterhouseCoopers Advisory Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Synpulse promoted Andreas Mettenberger and Adrien Thonet to partner in Hong Kong, bolstering leadership for financial-services transformation.

- March 2026: Roland Berger acquired Alexec Consulting to deepen battery-technology and electric-vehicle expertise for Asia-Pacific clients.

- January 2026: H/Advisors opened a Hong Kong office under Senior Director Candise Tang, adding strategic communications and public-affairs capability.

- January 2026: KPMG Hong Kong released guidance on OECD Crypto-Asset Reporting Framework compliance ahead of 2027 effectiveness.

Hong Kong Management Consulting Services Market Report Scope

The Hong Kong Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the 2031 forecast size of the Hong Kong management consulting services market?

The market is projected to reach USD 1.35 billion by 2031, reflecting a 5.36% CAGR over 2026-2031.

Which consulting service line is expanding the fastest?

Digital transformation consulting is forecast to grow at a 5.89% CAGR through 2031 as clients shift toward implementation-heavy mandates.

Why are small and medium-size enterprises driving new demand?

Government matching grants covering up to HKD 50,000 (USD 6.400) per project reduce financial barriers and encourage SMEs to hire consultants for cloud, customer-experience, and cybersecurity upgrades.

How are delivery models evolving in Hong Kong?

Hybrid structures combining brief on-site kick-offs with remote execution are becoming the norm, enabling faster turnaround and lower travel cost.

Which end-user industry shows the highest growth potential?

Healthcare leads future expansion at a 5.92% CAGR as the Hospital Authority executes a USD 385 million digital roadmap centered on telemedicine and artificial intelligence diagnostics.

What is the primary restraint limiting market acceleration?

Severe talent shortages inflate billing rates and lengthen project lead times, curbing near-term growth until new capacity comes online.

Page last updated on: