United Kingdom Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

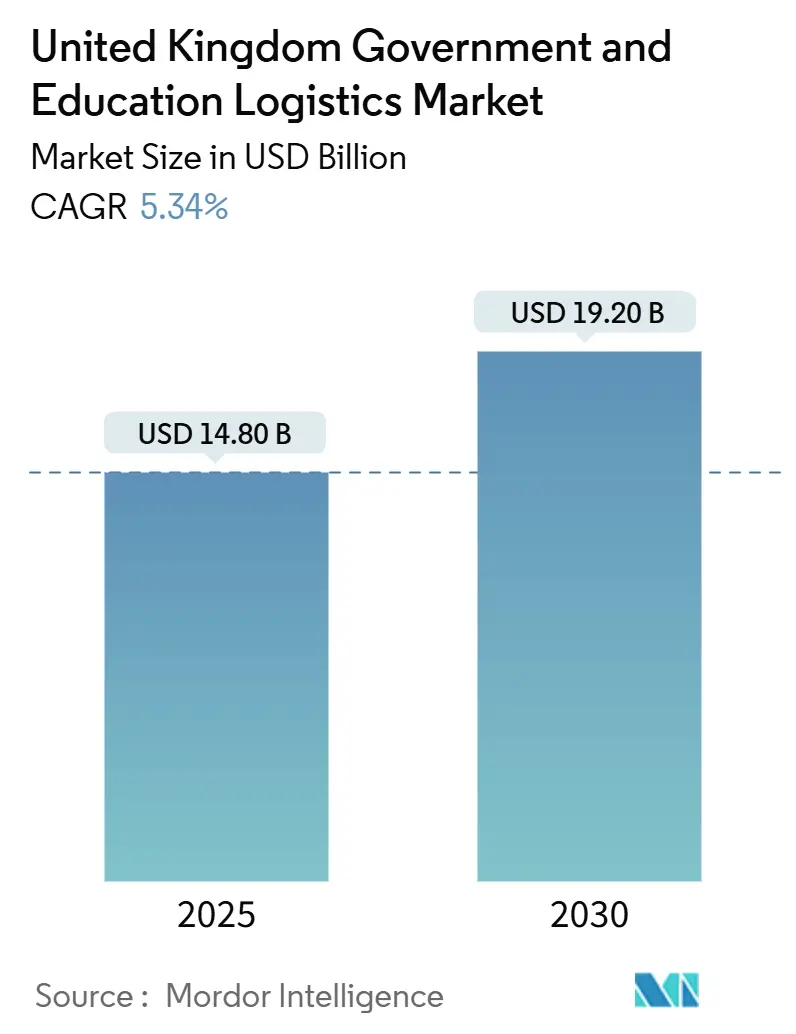

| Market Size (2025) | USD 14.80 Billion |

| Market Size (2030) | USD 19.20 Billion |

| Growth Rate (2025 - 2030) | 5.34% CAGR |

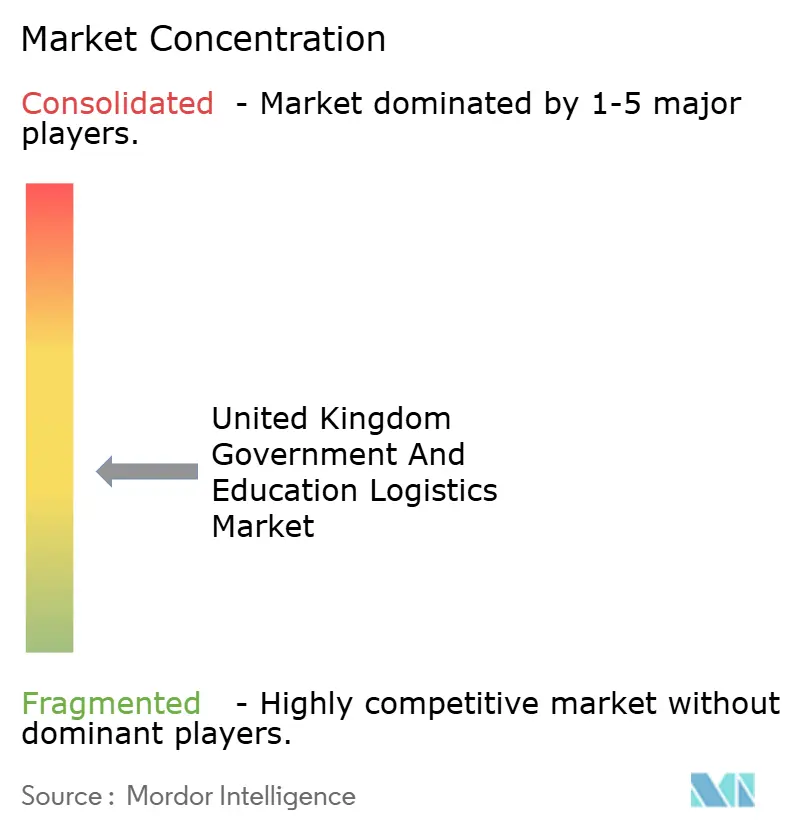

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Government And Education Logistics Market Analysis by Mordor Intelligence

The United Kingdom Government And Education Logistics Market size is estimated at USD 14.80 billion in 2025, and is expected to reach USD 19.20 billion by 2030, at a CAGR of 5.34% during the forecast period (2025-2030).

Robust digital-first public-service programs, continuing post-Brexit supply-chain realignment, and sustained campus-infrastructure upgrades keep demand elevated despite chronic labor shortages and fiscal constraints. Centralized procurement frameworks push shipment consolidation, favor integrators that combine transportation with data visibility, and reward providers that can satisfy NHS cold-chain, Ministry of Defence rapid-deployment, and university reverse-logistics requirements. The transportation component remains the volume backbone because road networks connect dense administrative clusters, while value-added services accelerate as clients seek inventory analytics, cyber-security compliance, and circular-economy reporting. Providers able to align technology investment with sector-specific compliance rules gain pricing power, particularly in contracts that link performance to transparency goals.

Key Report Takeaways

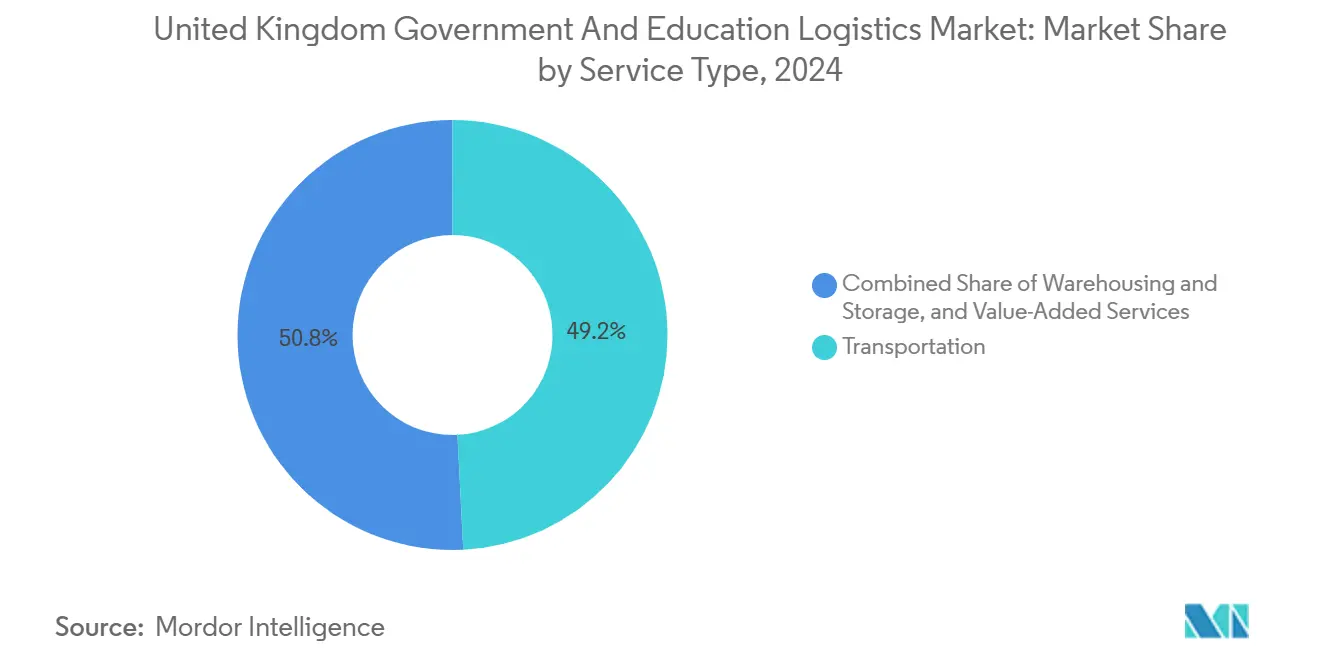

- By service type, transportation led with 49.2% of the United Kingdom government and education logistics market share in 2024; value-added services are projected to expand at a 7.1% CAGR through 2030.

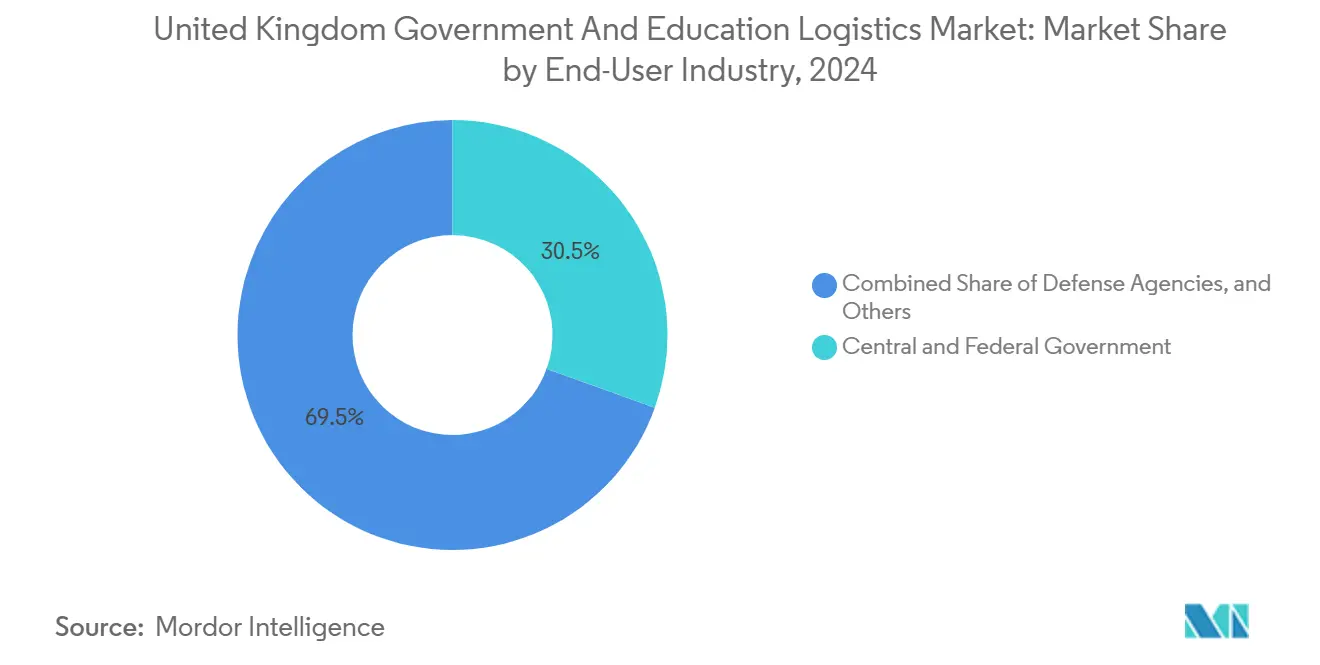

- By end-user, central and federal government agencies captured 30.5% of the United Kingdom government and education logistics market size in 2024, while higher-education institutions are forecast to grow at a 7.8% CAGR through 2030.

Figures recorded within United kingdom feed into a worldwide estimate while studying the global industry. Mordor Intelligence's government and education logistics market size captures this aggregation.

United Kingdom Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded digital-first public-service delivery | +1.2% | England core, extending to Scotland and Wales | Medium term (2-4 years) |

| NHS and departmental stockpile refresh post-COVID-19 | +0.9% | National, concentrated in England healthcare regions | Short term (≤ 2 years) |

| Growing adoption of Smart Campus initiatives | +0.8% | England andScotland higher education clusters | Medium term (2-4 years) |

| Post-Brexit re-shoring of educational supplies | +0.7% | National, with manufacturing concentration in Midlands | Long term (≥ 4 years) |

| Defence-sector surge in rapid-deployment logistics | +0.6% | Strategic locations: Aldershot, Portsmouth, Scotland bases | Short term (≤ 2 years) |

| Circular-economy compliance driving reverse logistics | +0.5% | National, early adoption in London and Manchester | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanded Digital-First Public-Service Delivery

The Procurement Act 2023 mandates system-to-system connectivity between suppliers and government platforms, accelerating shipment transparency and shrinking manual paperwork. Nearly 40% of citizen-facing services already run through digital channels, so logistics providers must synchronize barcode data, electronic proof-of-delivery, and audit trails with departmental dashboards. Order aggregation raises individual drop-size by 18%, reducing urban congestion fees yet increasing parcel weight variability that rewards fleets equipped with adjustable shelving. Carriers that overlay geofencing, two-factor driver authentication, and tamper-proof digital seals secure advantage on contracts tied to cyber-security key performance indicators. Smaller subcontractors risk exclusion if they cannot finance API integration or 24/7 monitoring, pushing them toward niche education contracts where compliance thresholds remain slightly lower[1]“Government Transformation Strategy,” Government Digital Service, gov.uk.

NHS and Departmental Stockpile Refresh Post-COVID-19

The National Emergency Stockpile requires 90-day coverage of priority pharmaceuticals and personal-protective equipment, generating warehousing demand that now exceeds pre-pandemic levels by 35%. Annual logistics spend attached to medical stock-rotation, dating, and temperature compliance reaches GBP 2.1 billion (USD 2.6 billion). Providers must hold MHRA licences, deploy continuous cold-chain telematics, and run validated pick-and-pack zones that can convert from ambient to chilled within four hours. Rapid-deployment clauses specify 12-hour call-off windows for emergency transfers into field hospitals, favoring integrators with cross-docking nodes near motorway junctions. High gantt-chart certainty shields margins, yet the capital costs of GDP-compliant facilities deter new entrants without healthcare pedigree[2]“Supply Chain Resilience Guidelines,” Department for Education, gov.uk.

Growing Adoption of Smart Campus Initiatives

Universities such as Birmingham consolidated 15 individual contracts into a unified logistics platform that cut on-campus delivery frequency by 25% while pushing inventory accuracy to 99.2%. Predictive dashboards align purchasing cycles with semester peaks, lowering emergency orders and supporting sustainability targets under the Environment Act 2021. Contracts pay premiums of 15-20% above standard tariff because providers must mesh IoT locker systems, AI route engines, and carbon-reporting dashboards into legacy enterprise-resource-planning suites. Research labs add complexity through hazardous-material handling and just-in-time reagent delivery that tolerates ±30-minute windows only. Vendors able to orchestrate forward logistics, valorize packaging, and manage reverse-flows for electronics earn long-term preferred-supplier status and gain upsell potential in document digitization or furniture refurbishment.

Post-Brexit Re-Shoring of Educational Supplies

Department for Education guidelines instruct schools to source at least 60% of non-specialized materials domestically by 2026, redirecting volumes toward Midlands and Northwest distribution hubs. Route density rises because inbound shipments from continental Europe decline, yet cost-per-unit may climb as domestic manufacturers lack scale efficiencies. Logistics partners cushion the rise by adopting multi-school consolidation runs and shared-user warehousing that offsets supplier fragmentation. Customs friction reduction allows faster lead-times, increasing agility during curriculum changes or sudden enrollment spikes. Nevertheless, contract clauses now stipulate proof of UK origin, compelling carriers to integrate blockchain-style traceability modules and collaborate with rail freight operators that feed coastal port hinterlands.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic driver and warehouse-labour shortages | -0.8% | National, acute in Southeast and Northwest England | Medium term (2-4 years) |

| Fiscal tightening of departmental budgets | -0.6% | National government departments | Short term (≤ 2 years) |

| Aging estate with limited loading infrastructure | -0.4% | Legacy government buildings, concentrated in London | Long term (≥ 4 years) |

| Cyber-security compliance burden for 3PLs | -0.3% | National, affecting all government contractors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Driver and Warehouse-Labor Shortages

National driver-vacancy rates hover near 14%, forcing providers to raise wages and introduce flexible scheduling, yet absenteeism still disrupts sensitive timed slots at Westminster and university labs. Warehouse attrition above 20% challenges order accuracy, especially for serialized medical kits, prompting accelerated investment in autonomous forklifts and goods-to-person robotics. Southeastern depots contend with housing costs that limit workforce availability, while Northwest hubs face skill gaps in temperature-validated operations. High vacancy encourages subcontracting, but government contracts demand security-cleared personnel, narrowing the talent pool and pressuring margins. Logistics companies that introduce apprenticeship programs, cross-train staff across picking and driving, and subsidize certification retain a competitive edge despite escalating labor costs[3]“Public Sector Procurement Strategy,” HM Treasury, gov.uk.

Fiscal Tightening of Departmental Budgets

HM Treasury cost-containment directives cap year-on-year logistics spending increases at 2%, compelling departments to renegotiate framework rates and demand performance-based pricing. Providers must demonstrate savings through consolidation, mode shift to rail, or packaging reduction before contract extensions receive sign-off. Budget uncertainty delays tender cycles, creating revenue troughs and procurement backlogs that squeeze smaller carriers reliant on short-term call-offs. Although value-based evaluation metrics broaden away from lowest price, upfront investment in data reporting and electric-vehicle fleets still faces elongated payback because index-linked inflation adjustments lag wage growth. Vendors with diversified client mixes across education and defense offset cash-flow risk, yet exposure to single-department frameworks raises vulnerability to annual spending reviews[4]“Planning for the Future,” Transport for London, tfl.gov.uk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Faces Value-Added Disruption

Transportation services retained 49.2% of the United Kingdom government and education logistics market share in 2024, reflecting the legacy priority placed on timely physical delivery of documents, pharmaceuticals, and laboratory materials. Road haulage underpins 75% of that figure because Motorway M1–M6 corridors link London ministries with Midlands warehousing clusters. Yet driver shortages and urban emissions caps encourage selective modal shift to consolidated rail runs between Southampton and Birmingham, followed by last-mile electric vans that satisfy Low Emission Zone rules. The value-added segment is projected to climb at a 7.1% CAGR, outpacing traditional transport thanks to rising demand for inventory analytics, API-enabled proof-of-delivery, and secure data interchange mandated by Cabinet Office cyber-standards. Providers that overlay temperature tracking, chain-of-custody scanning, and circular-economy scorecards transform commoditized drop-rates into solutions priced on outcomes rather than distance.

NHS stockpile policies stimulate sustained warehousing revenue, with ambient and chilled capacity expansion concentrated within 90 minutes of England’s major trauma centers. Universities consolidate satellite store rooms into automated central hubs that shorten internal pick times and free on-campus space for research labs. Simultaneously, reverse-logistics lines become integral as the Environment Act 2021 imposes extended producer responsibility on IT equipment and furniture, pushing integrated service contracts that combine forward flow with asset recovery. Consequently, transportation incumbents digitize fleet operations, embed driver safety telematics, and partner with robotics firms to keep share even as margin contribution increasingly shifts toward high-service bundles.

By End-User: Government Scale Versus Education Innovation

Central and federal agencies accounted for 30.5% of the United Kingdom government and education logistics market size in 2024, leveraging consolidated Crown Commercial Service frameworks that aggregate volumes across health, defense, and citizen-service departments. These structures guarantee minimum throughput, ease multi-year investment in cyber-secure track-and-trace platforms, and stipulate 98% first-time-delivery performance. Fiscal scrutiny intensifies, so carriers differentiate on demonstrable cost avoidance, such as network redesign that shaved 12% travel mileage for Cabinet Office print-to-post flows. Higher-education institutions deliver the fastest trajectory, expanding at a 7.8% CAGR through 2030, as international student recovery, laboratory modernization, and competitive sustainability rankings spur logistics outsourcing.

University consortia negotiate joint procurement, pooling dormitory furniture, science reagents, and e-learning hardware to achieve volume rebates that mirror government leverage but maintain appetite for innovation pilots. Smart-campus contracts incorporate IoT lockers, autonomous delivery carts, and AI inventory optimization, lifting service margins while compressing pure transportation revenue share. State and local bodies in Scotland and Wales favor regional providers versed in devolved compliance requirements, creating micro-tender ecosystems where agility trumps footprint scale. Defence agencies inject premium contract value through rapid-deployment specifications and security clearance thresholds, yet budget cyclicality linked to geopolitical events introduces demand volatility that carriers balance with steadier education flows.

Geography Analysis

England maintained roughly 75% of overall expenditure in 2024 as London ministries, Midlands manufacturing universities, and dense NHS trust networks combined to produce the highest shipment volume. Westminster and Whitehall buildings, many predating large-format loading bays, impose strict window deliveries and mandate electric vehicles within congestion zones, rewarding carriers with modular fleet composition and micro-fulfilment nodes on the city’s periphery. Southern corridors leading to Channel ports still handle residual cross-border educational supplies, but rising customs processing times encourage modal rebalancing toward domestic manufacturing hubs inside Birmingham’s logistics “golden triangle.”

Scotland represents the fastest regional growth at 6.8% CAGR through 2030 because devolved procurement allows adaptation to local research cluster needs, especially in life-science campuses near Edinburgh and Glasgow. NHS Scotland manages a separate distribution model, offering market entry for providers able to navigate region-specific tender rules and Gaelic language labeling. Defense bases such as Her Majesty’s Naval Base Clyde increase secure freight flows that must comply with radiation-monitoring and classified-material transport codes, elevating barrier-to-entry yet raising yield on each pallet moved.

Wales and Northern Ireland sustain smaller but stable contributions. Welsh government infrastructure funds upgrade A55 and South-Wales Metro links, improving freight reliability to Bangor and Cardiff universities. Post-Brexit Northern Ireland Protocol adjustments necessitate dual regulatory compliance, so providers integrate EU and UK customs data into a single visibility layer, safeguarding lead-times on cross-border library materials and medical supplies. Regional universities exploit this dual access by sourcing lab consumables from Irish suppliers, demanding carriers with customs brokerage expertise positioned near Belfast port.

Mordor Intelligence evaluates the government and education logistics market across all key regional markets, including Europe, Asia, and North America, with deeper country-level insights covering Russia, Germany, China, Canada, Spain, and India.

Competitive Landscape

The sector shows moderate fragmentation as multinational integrators DHL, Kuehne+Nagel, GXO, UPS Healthcare compete with niche domestic specialists such as Eddie Stobart, Unipart Group, and Davies Turner. Crown Commercial Service frameworks favor contractors who can demonstrate nationwide reach, ISO 27001 data security, and audited environment-social-governance reporting, steering substantial volume toward larger players. Simultaneously, university consortia and devolved bodies create procurement lots that encourage regional providers adept at tailored service and rapid configuration.

Technology capability now outweighs pure fleet volume in bid scoring. DHL’s API integration with NHS electronic medical record platforms, Kuehne+Nagel’s education-specific track-and-trace portal, and Unipart’s predictive analytics suite illustrate how investment in software becomes a prerequisite for securing multi-year renewals. Circular-economy mandates further advantage vendors owning refurbishment partnerships; for example, GXO’s reverse-logistics hub processes end-of-life IT equipment for ten universities, recovering residual value and satisfying asset-disposal clauses. Brexit-prompted reshoring opens share for domestic operators, yet euro-zone carriers retaining UK depots maintain relevance on defense airfreight corridors, preserving a competitive balance that restrains excessive consolidation.

Margin pressure from labor shortages nudges providers toward automation alliances. UPS Healthcare rolled out robotic picking to offset overtime costs, while Eddie Stobart’s restructuring injected capital that funds route-optimization software slashing fuel burn. Collaborative networks emerge, with smaller firms accessing integrator warehouse management systems in exchange for last-mile capacity during quarterly exam-paper peaks. Although the top five firms together command meaningful volume, specialized niches in healthcare cold-chain, hazardous research logistics, and secured defense freight remain open, anchoring a landscape best characterized as balanced rather than oligopolistic.

United Kingdom Government And Education Logistics Industry Leaders

DHL Group

Kuehne + Nagel

GXO Logistics

DPD Group

Eddie Stobart Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DHL Supply Chain secured a five-year, GBP 120 million (USD 149 million) NHS England contract focused on pharmaceutical distribution with real-time cold-chain telemetry.

- December 2024: GXO Logistics invested GBP 45 million (USD 56 million) in automated Birmingham and Manchester warehouses aimed at public-sector frameworks.

- November 2024: Kuehne+Nagel launched a dedicated Education Logistics division, allocating GBP 25 million (USD 31 million) to smart-campus integration across 15 universities.

- October 2024: Eddie Stobart Logistics completed restructuring with GBP 150 million (USD 186 million) funding to sustain education contracts while driving a 12% delivery cost reduction.

United Kingdom Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing and Storage | |

| Value-Added Services |

| Central/Federal Government |

| State and Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State and Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

What is the projected value of the United Kingdom government and education logistics market by 2030?

The market is expected to reach USD 19.2 billion by 2030, advancing at a 5.34% CAGR.

Which service type is expanding fastest in public-sector logistics contracts?

Value-added services, such as inventory analytics and reverse logistics, are forecast to grow at a 7.1% CAGR through 2030.

Which end-user group shows the highest growth momentum?

Higher-education institutions lead with a projected 7.8% CAGR as smart-campus programs scale nationwide.

Why are value-added services gaining traction among UK universities?

Smart-campus initiatives require integrated technology platforms that combine delivery, inventory management, and sustainability reporting under single contracts.

How is Brexit reshaping education-sector supply chains?

Department for Education guidelines drive sourcing reshoring, boosting demand for domestic warehousing and last-mile delivery while requiring carriers to prove UK origin traceability.

What challenges do logistics providers face when serving government departments?

Chronic driver shortages, stringent cyber-security compliance, and fiscal budget caps add cost pressure and elevate the need for automation and data-driven efficiencies.

Page last updated on: