India Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

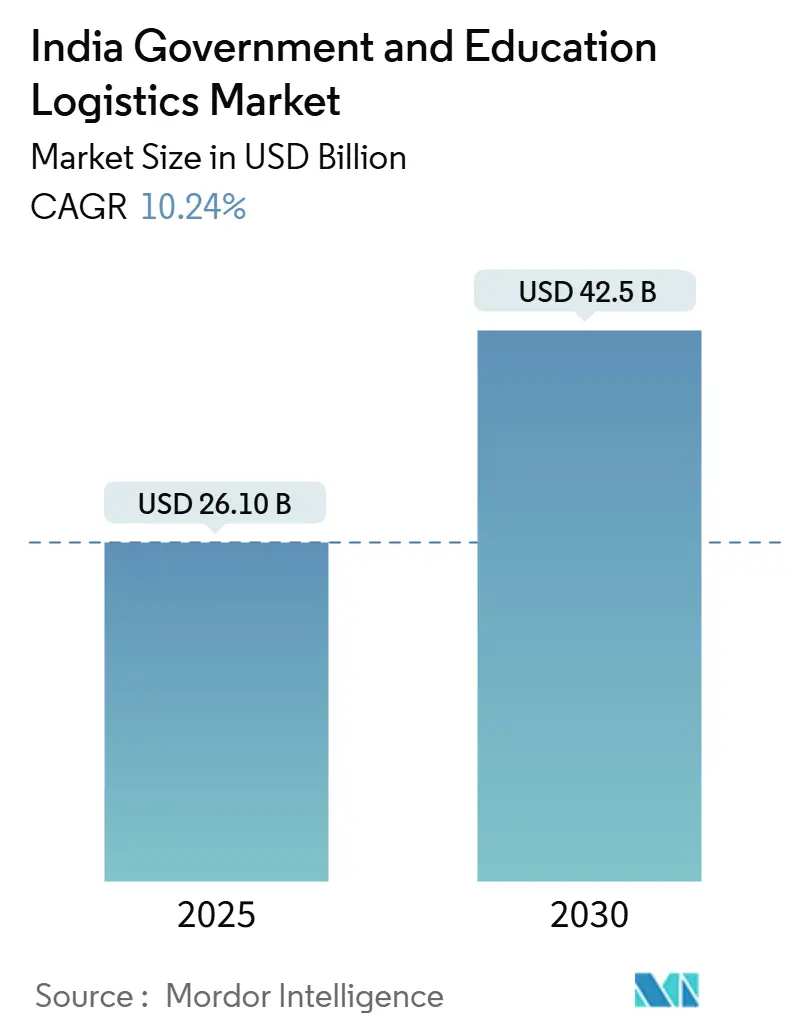

| Market Size (2025) | USD 26.10 Billion |

| Market Size (2030) | USD 42.5 Billion |

| Growth Rate (2025 - 2030) | 10.24% CAGR |

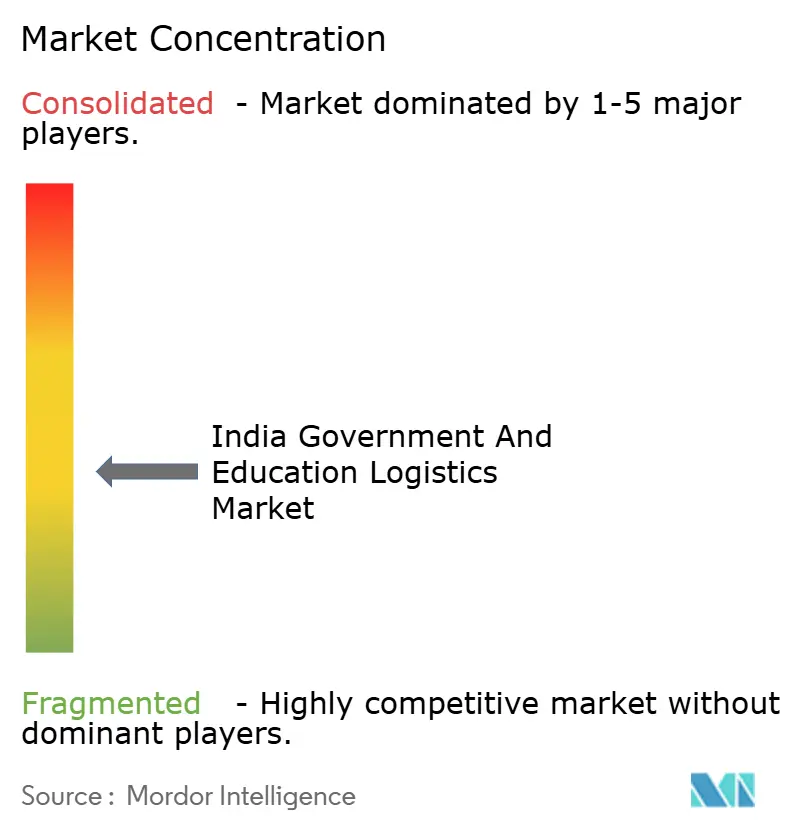

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Government And Education Logistics Market Analysis by Mordor Intelligence

The India Government And Education Logistics Market size is estimated at USD 26.10 billion in 2025, and is expected to reach USD 42.5 billion by 2030, at a CAGR of 10.24% during the forecast period (2025-2030).

Intensifying digital governance programs, record public-sector capital expenditure, and the National Education Policy 2020 (NEP 2020) have converged to reshape how ministries, state departments, and schools source, store, and move critical supplies. Procurement digitalization through the Government e-Marketplace (GeM) has triggered a step-change in demand for compliant third-party logistics, especially for sensitive defense consignments and classroom technology. Rapid highway, rail-freight, and port upgrades are compressing transit times; this connectivity is decisive for scaling mid-day meal cold-chains, secure examination material flows, and domestic defense manufacturing supply lines. Technology-driven services such as GPS tracking, RFID tagging, and temperature-controlled warehousing are moving from optional to mandatory as transparency clauses proliferate across government tenders. Competitive intensity is rising as private integrators, public sector undertakings, and start-ups race to prove compliance prowess, handle complex documentation, and keep working capital intact despite prolonged payment cycles.

Key Report Takeaways

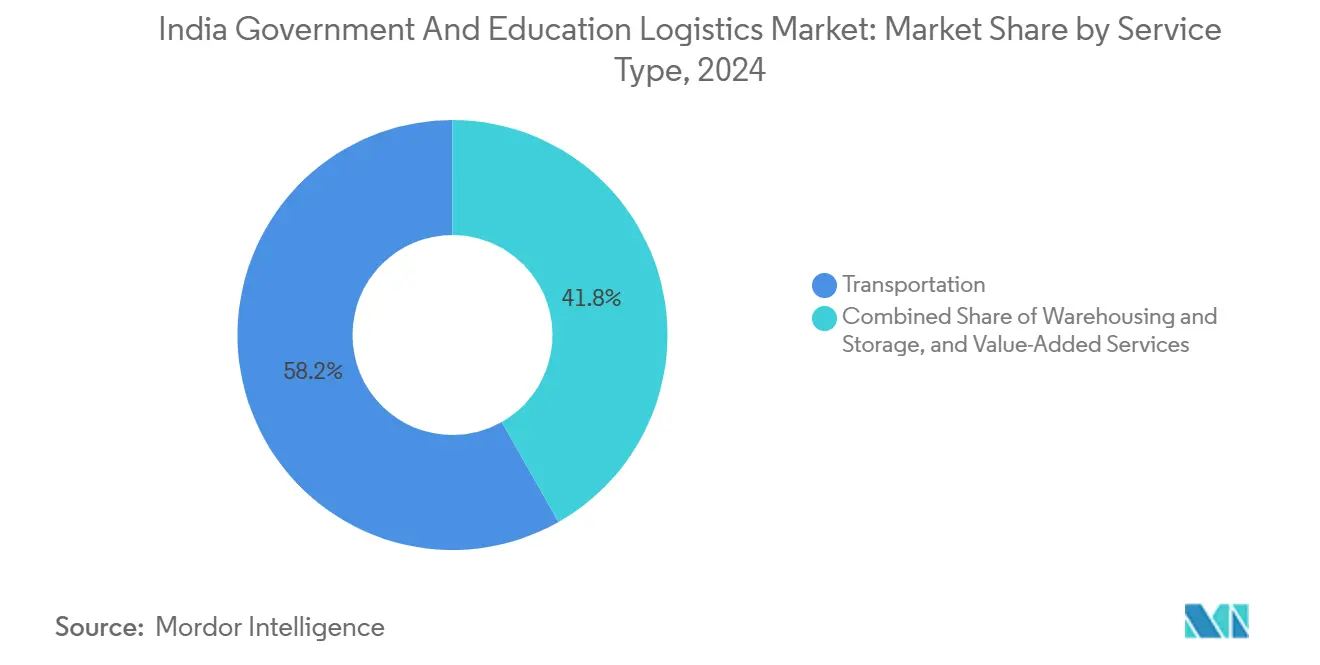

- By service type, transportation held 58.2% of india government and education logistics market share in 2024 while value-added services are advancing at a 13.5% CAGR through 2030.

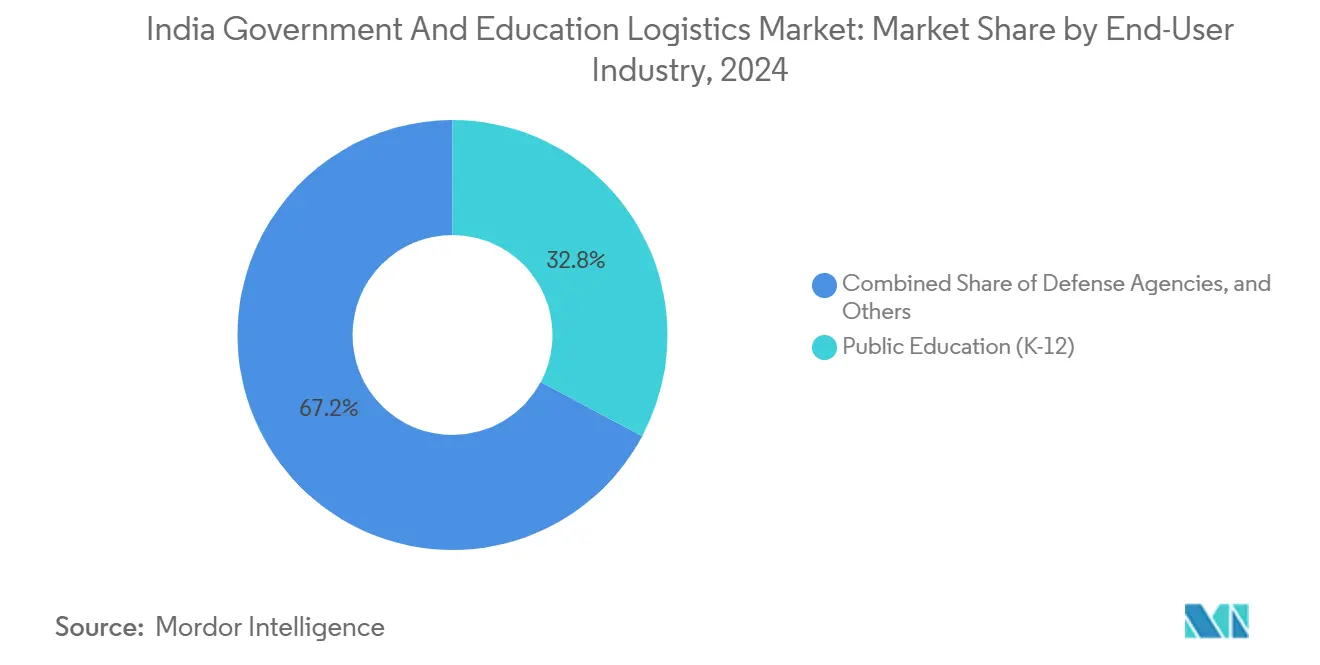

- By end user, public education (K-12) accounted for 32.8% share of the india government and education logistics market size in 2024, and higher education institutions are projected to expand at a 12.5% CAGR between 2025-2030.

India operates as part of an interconnected international environment rather than as a self-contained country level unit. The government and education logistics market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

India Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NEP-driven digital learning surge | +2.1% | National; early movers Karnataka, Tamil Nadu, Maharashtra | Medium term (2-4 years) |

| Public procurement reforms (GeM, e-tendering) | +1.8% | Delhi NCR, Mumbai, Bangalore | Short term (≤ 2 years) |

| Infrastructure build-out (Bharatmala, DFCC) | +2.3% | Gujarat, Maharashtra, Punjab | Long term (≥ 4 years) |

| Defense and public-sector capex expansion | +1.5% | Border states and key manufacturing hubs | Medium term (2-4 years) |

| Secure movement of examination material | +0.9% | National; peak in exam months | Short term (≤ 2 years) |

| Cold-chain for nutrition and immunization | +1.2% | Rural Uttar Pradesh, Bihar, Rajasthan, Madhya Pradesh | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Education Policy-driven Digital Learning Surge

NEP 2020 set aside Rs 1.04 lakh crore (USD 12.5 billion) for school infrastructure in FY 2024-25, widening logistics scope from textbook drops to temperature-controlled storage and fragile handling for 1.5 million schools. PM e-VIDYA device roll-outs have multiplied demand for secure, high-value cargo services; Karnataka alone shipped 1 million tablets in 2024, a 340% surge over 2023. Region-specific content distribution calls for multilingual labelling and granular inventory control, driving adoption of warehouse management systems tailored to India’s 22 official languages. Logistics providers able to mesh last-mile reach with tamper-proof packaging standards are gaining premium contracts. Overall, the driver lifts utilization of integrated road-rail solutions, boosting revenue density across the india government and education logistics market[1]“GeM Crosses Rs 5 Lakh Crore GMV Milestone,” Press Information Bureau, pib.gov.in.

Public Procurement Reforms (GeM, e-tendering)

GeM processed over 1.2 million orders per month in 2024, 45% higher than 2023, and surpassed Rs 5 lakh crore (USD 60 billion) cumulative GMV in March 2025. The marketplace’s dynamic pricing algorithm and real-time inventory visibility have cut procurement lead times by 35%, obliging logistics firms to sustain rapid pick-pack-dispatch cycles. Defense purchases through GeM hit Rs 16,000 crore (USD 1.9 billion) in 2024, underscoring the need for secure fleets fitted with real-time tracking and geo-fencing. Continuous compliance audits and API-linked documentation are now embedded in tender pre-qualification, rewarding operators that invested early in ISO 27001 and blockchain traceability[2]“National Education Policy 2020 Implementation Guidelines,” Ministry of Education, education.gov.in .

Infrastructure Build-out (Bharatmala, Sagarmala, DFCC)

Dedicated Freight Corridors (DFCs) are over 90% complete, trimming government cargo transit times by up to 40% and unlocking modal shift from road to cost-efficient rail. Bharatmala’s 13,000 km of new highways facilitate year-round truck access to hinterland schools and military depots. Sagarmala 2.0 funnels Rs 40,000 crore (USD 4.8 billion) into port upgrades, expediting import clearance of simulators, lab gear, and defense components. The PM Gati Shakti master plan links DFC freight stations with container depots, reducing spoilage in mid-day meal supply chains by 18% according to education ministry audits. The result is a tangible expansion of addressable lanes for the india government and education logistics market.

Defense and Public-sector Capex Expansion

Defense capex rose 4.79% year on year to Rs 1.72 lakh crore (USD 20.6 billion) in FY 2024-25, accelerating requirements for secure material flow across newly indigenized component lists. Public-sector enterprises lifted capital outlay by 23% to Rs 11.6 lakh crore (USD 139 billion), widening demand for heavy-haul, over-dimensional cargo, and bonded warehousing. Logistics partners must pass stringent security screening, integrate with defense ERP systems, and guarantee tamper-evident custody transfers. Firms offering encrypted data exchange and dual-use fleet segregation command higher margins within the india government and education logistics market.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-layer regulatory compliance and GST issues | -1.4% | National; complex in federal procurement | Short term (≤ 2 years) |

| Budgetary constraints and delayed payments | -1.7% | Financially stressed states | Medium term (2-4 years) |

| Rural last-mile infrastructure gaps | -0.8% | UP, Bihar, Odisha, Northeast | Long term (≥ 4 years) |

| Data-security concerns limiting outsourcing | -0.6% | Sensitive defense and examination flows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-layer Regulatory Compliance and GST Complexities

Post-GST, average administrative cost for logistics providers rose 15-20%, driven by e-way bill filings and multi-state reconciliations. Educational consignments that cross state lines must navigate varying GST slabs for books, devices, and lab chemicals, often delaying school year readiness. Reverse-charge provisions extend working-capital lock-up to 90–120 days for small firms. Compliance fatigue prompts consolidation, narrowing vendor pools and potentially limiting service innovation inside the india government and education logistics market[3]“Defence Budget 2024-25 Allocation Details,” Ministry of Defence, indiabudget.gov.in.

Budgetary Constraints and Delayed Government Payments

Government pay cycles stretched to 75–90 days in 2024, double typical private-sector terms, squeezing liquidity for transporters and warehouse operators. State coffers under stress defer mid-day meal and textbook logistics bills, forcing operators to raise financing at higher rates or exit tenders. Performance-based penalty clauses add further risk, dampening appetite for expansion into new geographies. Consequently, capital-light digital platforms gain traction by mediating between government demand and asset owners, reshaping competition in the india government and education logistics market[4]“GST Impact on Logistics Sector Analysis,” GST Council Secretariat, gstcouncil.gov.in.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates Amid Value-Added Growth

Transportation services generated 58.2% of india government and education logistics market revenue in 2024, buttressed by DFC-enabled rail haulage and Bharatmala’s highway throughput gains. Road still carries 75% of government loads, but rail now attracts bulk textbook and device cargo bound for state depots, shaving costs by 18%. The india government and education logistics market size for transportation services is projected to advance at 9.6% CAGR to 2030 as port-led coastal shipping and inland waterways complement trunk corridors.

Value-added services are on a 13.5% CAGR trajectory, reflecting demand for barcode-based inventory control, IoT temperature logging, kitting, and reverse logistics. Ministries require tamper-proof tagging, digital proof-of-delivery, and shelf-life analytics for nutritional commodities. Operators integrating warehouse management systems with GeM APIs capture higher wallet share. The india government and education logistics industry is witnessing early adoption of drone stock-taking and AI-assisted route planning inside secure depots, gradually redefining service contract scopes.

Warehousing and storage retains a stable foothold as state-run depots retrofit cold rooms for milk, eggs, and vaccines. Examination boards contract humidity-controlled vaults for question papers, spawning niche micro-warehousing hubs near printing presses. Airfreight commands a premium for emergency device replacements and strategic defense imports. Coastal shipping’s share remains modest but will rise once Sagarmala berths finish automation upgrades. Blended multimodal packages stand out as ministries emphasize door-to-door visibility across all shipment legs of the india government and education logistics market.

By End-User: Education Sector Leads Digital Transformation

Public education holds 32.8% revenue share, underpinned by a 250 million-student base and fiscal 2024-25’s Rs 1.04 lakh crore infrastructure allocation. The india government and education logistics market size for K-12 supplies will keep pace as tablet, science-kit, and language-lab roll-outs deepen. State textbook corporations now contract end-to-end vendor-managed inventory, boosting annualized throughput for integrated 3PLs.

Higher education is the fastest mover with 12.5% CAGR to 2030. Research labs need cold-chain reagents, and international collaborations drive inbound instrument traffic that must clear customs rapidly. Universities outsource campus store replenishment, e-library device servicing, and reverse logistics for e-waste, expanding wallet share for tech-savvy operators. The india government and education logistics market share captured by higher-ed consignments could climb past 20% by decade-end if NEP-mandated multidisciplinary universities meet construction timelines.

Central and state government departments combine steady but intricate flows ranging from file digitization drives to strategic raw material transfers for public-sector undertakings. Defense agencies sustain high-margin volumes owing to secure fleet prerequisites and classified routing. Other segments, including public health and judiciary, rely increasingly on resilient cold-chains and tamper-evident pouches, illustrating the widening perimeter of the india government and education logistics market.

Geography Analysis

Northern India leads by value, with Delhi NCR accounting for 18% of 2024 turnover as ministries consolidate procurement on GeM and defense establishments demand round-the-clock secure shuttles. Punjab and Haryana leverage industrial corridors to turn transit depots into hub-and-spoke nodes that feed remote cantonments. Western India benefits from Gujarat’s DFC integration and Maharashtra’s port-rail connectivity, cutting reload dwell times by 35% and enhancing competitiveness across the india government and education logistics market.

Southern states register the fastest expansion. Karnataka’s one-million-tablet distribution exemplifies NEP acceleration, while Tamil Nadu’s free laptop scheme pushes asset-light operators to scale reverse logistics for warranty swaps. Andhra Pradesh ports handle rising inbound lab equipment linked to global university tie-ups, driving coastal-railage synergies. Average fulfillment lead time in the south is 20% shorter than national norms, fostering early adoption of just-in-time contracts.

Eastern and northeastern regions lag on paved-road density yet reap incremental gains from PM Gati Shakti multimodal projects. New bridges over the Brahmaputra and rail conversions in Odisha are shaving days off school-kit deliveries. Last-mile gaps persist, with 15,000 rural schools still accessible only via unpaved routes, limiting cold-chain reliability. Addressing these structural deficits remains pivotal for broad-based growth of the india government and education logistics market.

The government and education logistics market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as North America, Europe, and Middle East, along with detailed country-level analysis for China, South Korea, Canada, Russia, Mexico, and France.

Competitive Landscape

The India government and education logistics market exhibits moderate fragmentation with ongoing consolidation. Container Corporation of India (CONCOR) leverages rail terminals and an INR 2,500 crore expansion plan on inland container depots tailored for government cargo. India Post modernized automated sorting worth INR 200 crore, preserving unrivaled rural reach while upgrading track-and-trace. Private integrators Delhivery and TCI Express gain ground on secure device distribution and mid-day meal cold-chains, aided by Spoton’s acquisition and an INR 800 crore digital-device contract, respectively.

Technology is the fault line. ISO 27001 compliance, blockchain proofs, and API links to GeM now decide tender outcomes. Mahindra Logistics’ dedicated 500-vehicle government fleet with onboard CCTV and temperature sensors shows specialization payoff.

TVS Supply Chain’s rail-road program with Indian Railways illustrates the push toward multimodal resilience. Smaller regionals lacking GST analytics, e-way-bill automation, or working-capital headroom face acquisition or exit, tilting share toward digitally fluent operators inside the india government and education logistics market.

India Government And Education Logistics Industry Leaders

Container Corporation of India

TCI Express

Blue Dart Express

India Post

Safexpress

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Container Corporation of India unveiled a Rs 2,500 crore (USD 3 billion) multimodal program adding 15 inland depots with high-security zones and live tracking to serve defense and education flows.

- December 2024: Delhivery bought Spoton Logistics for Rs 450 crore (USD 54 million), gaining cold-chain assets and state education contracts for mid-day meal distribution.

- November 2024: TCI Express secured a Rs 800 crore (USD 96 million) nationwide PM e-VIDYA device delivery contract.

- October 2024: TVS Supply Chain partnered Indian Railways, investing Rs 350 crore (USD 42 million) in DFC-linked cargo parks for defense and education consignments.

India Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing and Storage | |

| Value-Added Services |

| Central/Federal Government |

| State and Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State and Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

What is the projected value of the india government and education logistics market by 2030?

The market is expected to reach USD 42.5 billion by 2030, growing at a 10.24% CAGR.

Which service type currently dominates public-sector logistics spending?

Transportation services hold 58.2% share, driven by expanded highway and rail-freight corridors.

Why are value-added services growing faster than core transportation?

Ministries increasingly demand inventory management, cold-chain monitoring, and real-time visibility, pushing this segment to a 13.5% CAGR.

How does GeM influence logistics contract awards?

The platform’s real-time pricing and compliance checks favor operators with digitized documentation and secure tracking capabilities.

What bottlenecks affect rural education logistics?

Unpaved roads and bridge deficits in eastern and northeastern states hinder last-mile delivery of mid-day meals and learning devices. Which states lead in NEP-driven digital device deployment? Karnataka, Tamil Nadu, and Maharashtra top the list, with Karnataka distributing 1 million student tablets in 2024.

Page last updated on: