France Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

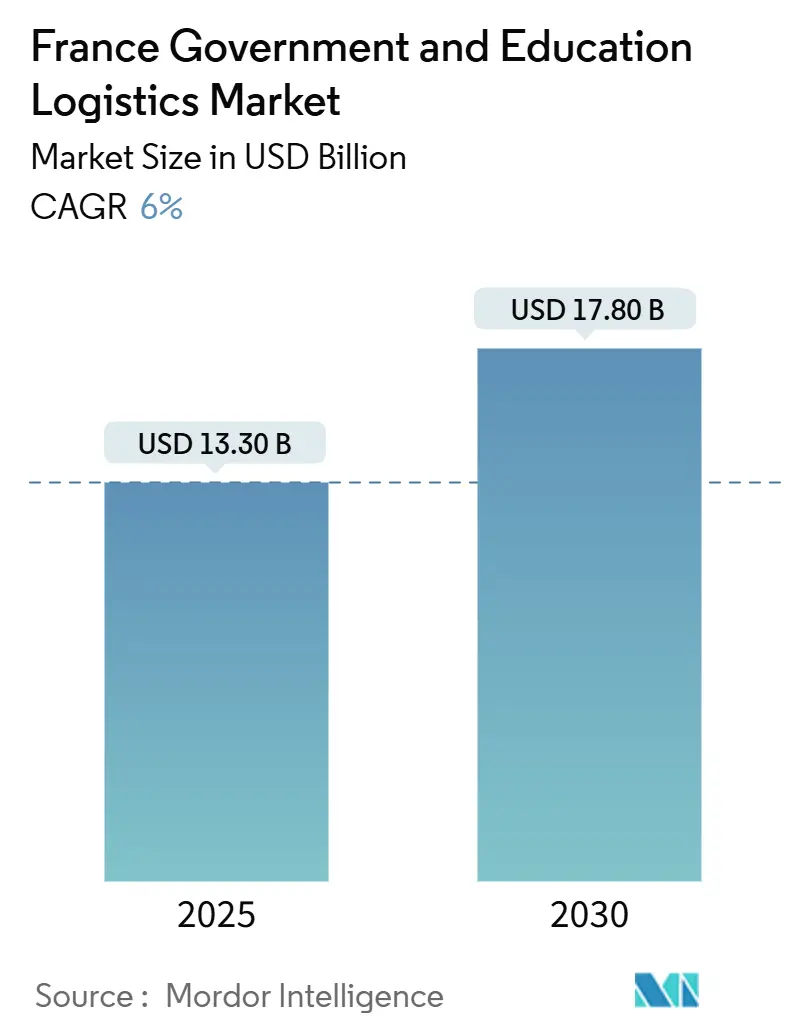

| Market Size (2025) | USD 13.30 Billion |

| Market Size (2030) | USD 17.80 Billion |

| Growth Rate (2025 - 2030) | 6.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Government And Education Logistics Market Analysis by Mordor Intelligence

The France Government And Education Logistics Market size is estimated at USD 13.30 billion in 2025, and is expected to reach USD 17.80 billion by 2030, at a CAGR of 6% during the forecast period (2025-2030).

The upward trajectory is buoyed by the France 2030 renovation plan, stricter decarbonization rules in expanding ZFE zones, and broader spillovers from Defense 4PL automation into civilian education flows. Steady outsourcing of non-core logistics by ministries and local authorities supplements demand, while open-data procurement feeds lower entry barriers for regional specialists. Yet data-sovereignty rules and cyber intrusion waves introduce compliance costs that reshape provider strategies.

Key Report Takeaways

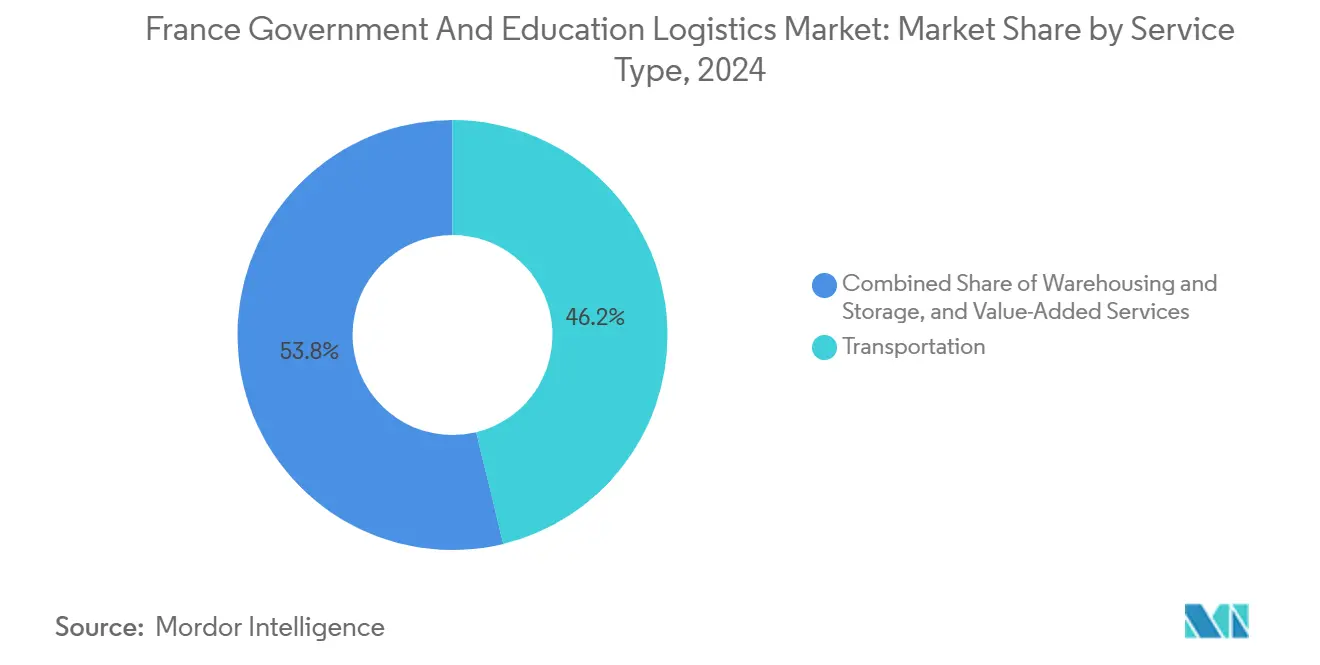

- Transportation services commanded 46.2% revenue share of the France Government and Education Logistics market in 2024, whereas value-added services are accelerating at a 7.5% CAGR to 2030.

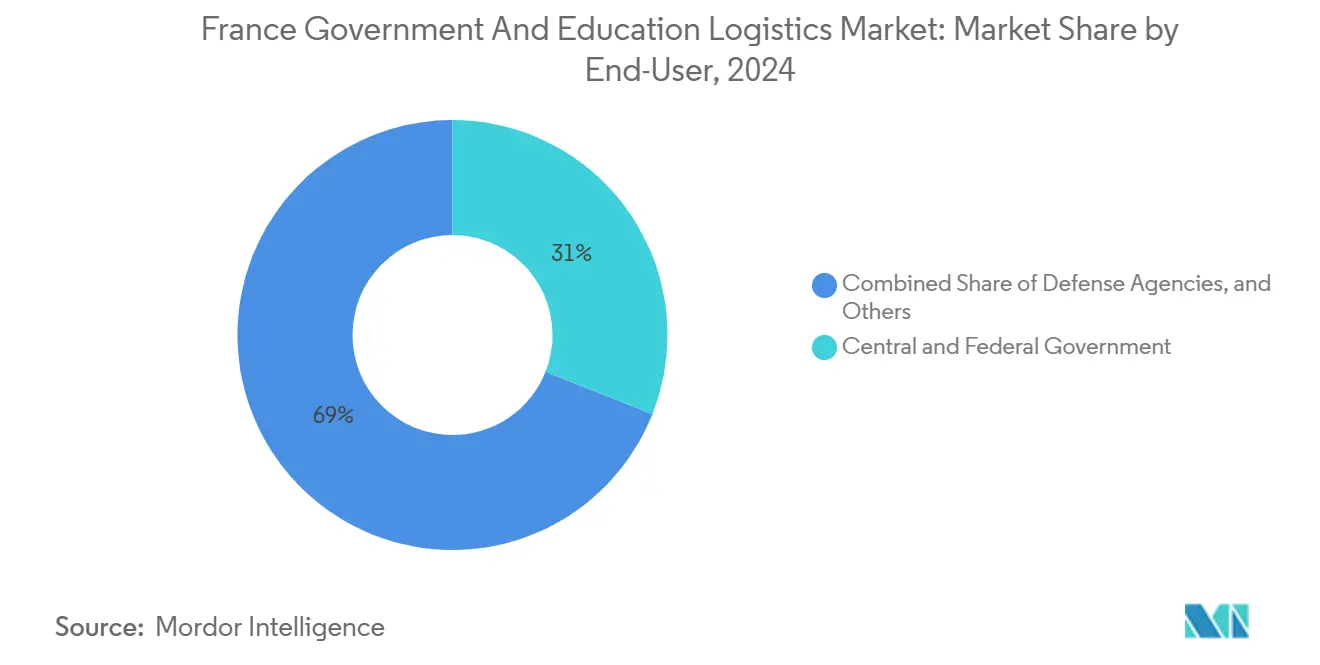

- Central/federal government held 31% of the France Government and Education Logistics market share in 2024, but higher-education institutions lead growth with an 8.1% CAGR through 2030.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide government and education logistics market outlook captures this forward trajectory.

France Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing of non-core logistics | +1.2% | National, high in Île-de-France | Medium term (2-4 years) |

| France 2030 renovation push | +1.4% | National, rural and aging urban sites | Long term (≥ 4 years) |

| Digital public procurement and ENT | +1.0% | National, Auvergne-Rhône-Alpes first-mover | Short term (≤ 2 years) |

| Decarbonization mandates | +1.5% | 43 metropolitan ZFE areas | Medium term (2-4 years) |

| Open-data micro-tenders | +0.7% | Rural & suburban communes | Short term (≤ 2 years) |

| Defense 4PL spillover | +0.6% | Near major bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing of Non-Core Logistics by Ministries and Local Authorities

Budget pressure pushes ministries to refocus on core mandates, prompting a steady hand-over of transport, warehousing, reverse logistics, and IT asset handling to private specialists. The DECP open-data platform gives mid-tier providers visibility of thousands of micro-contracts once monopolized by large incumbents. A 2024 Court of Accounts study found in-house logistics to cost 15-20% more than outsourced equivalents, motivating further externalization. Providers that can demonstrate GDPR compliance, carbon-tracking dashboards, and school-safe driver vetting now enjoy preferential scoring in tender awards. The trend is especially visible in Île-de-France, but regional capitals in Occitanie and Nouvelle-Aquitaine are following suit as their procurement portals replicate DECP interfaces[1]“Low Emission Zones—ZFE-m,” French Ministry of Ecological Transition, ECOLOGIE.GOUV.FR .

France 2030 "Plan de Renovation" Logistics Surge

The EUR 7 billion (USD 7.72 billion) investment stream earmarked for renovating 40,000 schools and public offices generates high-volume, high-complexity freight flows. HVAC units, insulation panels, and interactive boards move in tightly scheduled windows so classes can continue. Construction consortia increasingly mandate one coordinator to handle inbound materials, last-yard movement inside live campuses, and waste take-back. French-origin sourcing rules further favor domestic carriers with regional depots. Rural departments in Bourgogne-Franche-Comté, Nouvelle-Aquitaine, and Centre-Val de Loire see the largest uplift because many facilities date back to the 1960s. This long-tail demand underpins a robust pipeline through at least 2029, sustaining order books for mid-cap road haulers able to meet Eco-Class 6 fleet criteria[2]“Essential Public Procurement Data Platform,” French Public Procurement Directorate, ECONOMIE.GOUV.FR .

Digitalisation of Public Procurement and ENT Platforms

Nationwide ENT coverage now links 12 million learners and 1 million teachers to centralized ordering portals. Usage analytics improve demand forecasting for workbooks, tablets, and meal ingredients, cutting buffer stock by 18% in 2024. However, ransomware attacks on major platforms triggered 72-hour delivery backlogs and EUR 2.3 million (USD 2.53 million) in emergency purchasing costs, underlining the value of end-to-end cyber-secure logistics. Providers able to integrate SOC-grade monitoring and encrypted APIs into their transport management systems now win competitive advantage, particularly in Auvergne-Rhône-Alpes and Grand Est where ENT adoption is deepest.

Decarbonisation Mandates (ZFE, Fit-for-55)

Forty-three metropolitan areas impose phased restrictions on Euro 5 diesel vehicles. Logistic firms serving public contracts must now prove tangible emissions cuts, documented under the 2024 Green Logistics Fund’s reporting template. Electric school buses, cargo bikes for last-mile textbook runs, and intermodal pairings with upgraded rail services in SNCF’s “Rail Education” network become procurement differentiators. Yet charging infrastructure gaps in mountainous departments limit rapid fleet turnover, compelling operators to pair hybrid vans with route optimisation software to stay within carbon budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty clauses | -1.3% | Nationwide, higher for cross-border 3PLs | Medium term (2-4 years) |

| Fiscal squeeze on communes | -1.1% | Rural & overseas territories | Medium term (2-4 years) |

| Cyber-intrusion waves | -0.9% | Digitally advanced regions | Short term (≤ 2 years) |

| Rail-freight fragility | -0.6% | Rural consolidation corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty Clauses in Public Tenders

The 2024 public procurement code revision mandates all data processing within EU borders. Non-compliant bidders face disqualification, nudging multinationals to set up French cloud nodes or partner with OVHcloud. Estimated retrofitting costs range from EUR 50 million (USD 55.18 million) to EUR 200 million (USD 220.72 million) for major 3PLs. Smaller domestic firms gain temporary protection but also shoulder audit expenses to certify hosting arrangements[3]“Public Procurement Code Revisions 2024,” French National Assembly, ASSEMBLEE-NATIONALE.FR.

Fiscal Squeeze on Communes and Departements

Real-terms budget cuts averaging 8% over 2024-2026 limit capital spending on fleet renewal and depot upgrades. Some départements postpone bus replacement cycles or aggregate school routes, dampening new contract volumes even as efficiency needs rise[4]“Local Government Finance and Budget Analysis,” French Association of Departments, DEPARTEMENTS.FR .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Anchors Market Despite Value-Added Growth

Transportation services held 46.2% of the France Government and Education Logistics market in 2024, moving 3.2 million pupils daily under the Education Code’s guaranteed access provision. Road fleets cover 95% of journeys, with rail catering to specific rural-to-urban axes. Value-added services are expanding at 7.5% CAGR, reflecting a pivot from pure haulage to turnkey solutions that bundle temperature-controlled catering, IT device roll-out, and reverse logistics clean-ups. The France Government and Education Logistics market size allocated to warehousing also rises steadily as regional consolidation hubs support multi-campus distribution. Providers integrating circular-economy compliant refurbishment centers win institutional backing.

Digital lodgement portals increase uptake of specialist handling, pushing demand for barcode-level traceability and eco-certified packaging. The France Government and Education Logistics market share of air and sea transport remains niche but critical for overseas departments and medical emergencies. Inland waterway pilots on the Seine show promise for bulk delivery of renovation materials into dense urban cores where ZFE restrictions curb diesel truck access.

By End-User: Government Leadership Faces Higher-Education Challenge

Central government bodies commanded the largest France Government and Education Logistics market share at 31% in 2024 thanks to the UGAP framework aggregating orders for over 100,000 entities. Defense agencies contribute a steady slice through classified freight corridors. State and local governments sustain diversified demand, yet purchasing power pressures lengthen tender cycles. Higher-education institutions, benefitting from France 2030 research funds, showcase the fastest CAGR at 8.1%. Their appetite for lab supplies, international student relocation services, and campus expansion materials makes them prime targets for value-added logistics.

The France Government and Education Logistics market size dedicated to K-12 schooling remains stable but shifts from paper-heavy to device-heavy consignments as digital textbook programs roll out. Vocational centers and cultural establishments in the “Others” band increasingly require modular exhibition transport and specialized equipment moves, nudging growth despite smaller baseline volumes.

Geography Analysis

Ile-de-France generates 28% of the France Government and Education Logistics market by value, anchored by ministry headquarters, flagship universities, and corporate-public partnerships. Dense ZFE regulations accelerate EV deployment, while multimodal nodes at Gennevilliers and Rungis streamline cross-dock operations. The northern ZFE perimeter around Lille and the southern ring from Lyon to Grenoble follow similar decarbonization trajectories.

Nouvelle-Aquitaine, Occitanie, and Centre-Val de Loire illustrate the rural-renovation dynamic: dispersed campuses and aging facilities attract renovation freight, yet long distances inflate per-capita logistics costs. SMEs headquartered in these regions exploit DECP alerts to secure meal-delivery and exam-paper transport contracts previously lost to Paris-based giants.

Overseas territories present unique long-haul challenges, raising the France Government and Education Logistics market size allocated to air-sea multimodal chains. Grant-funded programs, such as the Equal Education Access Scheme, subsidize reliable monthly container runs for textbook and lab-chemical resupply. Seasonal cyclone risks spur stock-piling strategies, rewarding providers versed in contingency routing and local customs clearance.

The government and education logistics market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Africa, and Asia. This is complemented by country-specific insights for Germany, Spain, India, Japan, United Kingdom, and Mexico, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The France Government and Education Logistics market demonstrates moderate fragmentation. GEODIS advances a EUR 150 million (USD 165.54 million) carbon-neutral DC network and co-develops electric shuttles with Stellantis to bolster ZFE compliance. La Poste’s TransEco takeover expands temperature-controlled capacities, catering to school meal and pharma training labs. DHL Supply Chain leverages its EUR 200 million (USD 220.72 million) defense contract to spin off civilian education lanes, integrating blockchain custody tools first proven in ammo supply.

Digital differentiation matters: providers interfacing directly with DECP APIs cut order-processing times by 22%. ISO 27001 and SecNumCloud certifications become must-haves post-2024 cyber scares, allowing ID Logistics and Kuehne+Nagel to win sensitive device-configuration tenders. Start-ups like Woop pilot rural drone kits and autonomous last-mile vans, backed by Rhenus funding. The regulatory tilt toward sustainability and data-localization pressures incumbents to invest in local cloud stacking and low-carbon fleets, ingredients smaller challengers sometimes lack.

France Government And Education Logistics Industry Leaders

GEODIS

La Poste (Colissimo)

SNCF (Rail Logistics Europe)

DHL Group

Rhenus Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: GEODIS unveils a EUR 150 million (USD 165.54 million) program for 12 carbon-neutral DCs and 500 electric vans.

- December 2024: La Poste buys TransEco for EUR 85 million (USD 93.80 million), boosting temperature-controlled delivery.

- November 2024: DHL Supply Chain wins EUR 200 million (USD 220.72 million), 5-year defense logistics contract with civilian flow overlap.

- October 2024: SNCF Logistics launches EUR 75 million (USD 82.77 million) "Rail Education" refrigerated freight lanes.

France Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing and Storage | |

| Value-Added Services |

| Central/Federal Government |

| State and Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State and Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

How big is the France Government and Education Logistics market in 2025?

It is valued at USD 13.3 billion and is set to grow at 6% CAGR to 2030.

Which service type commands the largest share?

Transportation services account for 46.2% of sector revenue in 2024.

Which end-user group is expanding fastest?

Higher-education institutions are advancing at an 8.1% CAGR through 2030.

What regulations most influence provider selection?

ZFE low-emission mandates and EU-compliant data-sovereignty clauses dominate tender scoring.

Which region drives the highest logistics spend?

Ile-de-France contributes 28% of nationwide public-sector logistics outlays.

What technologies stand out in recent contracts?

Cyber-secure APIs, blockchain chain-of-custody, and autonomous rural delivery pilots are gaining traction.

Page last updated on: