Middle East Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

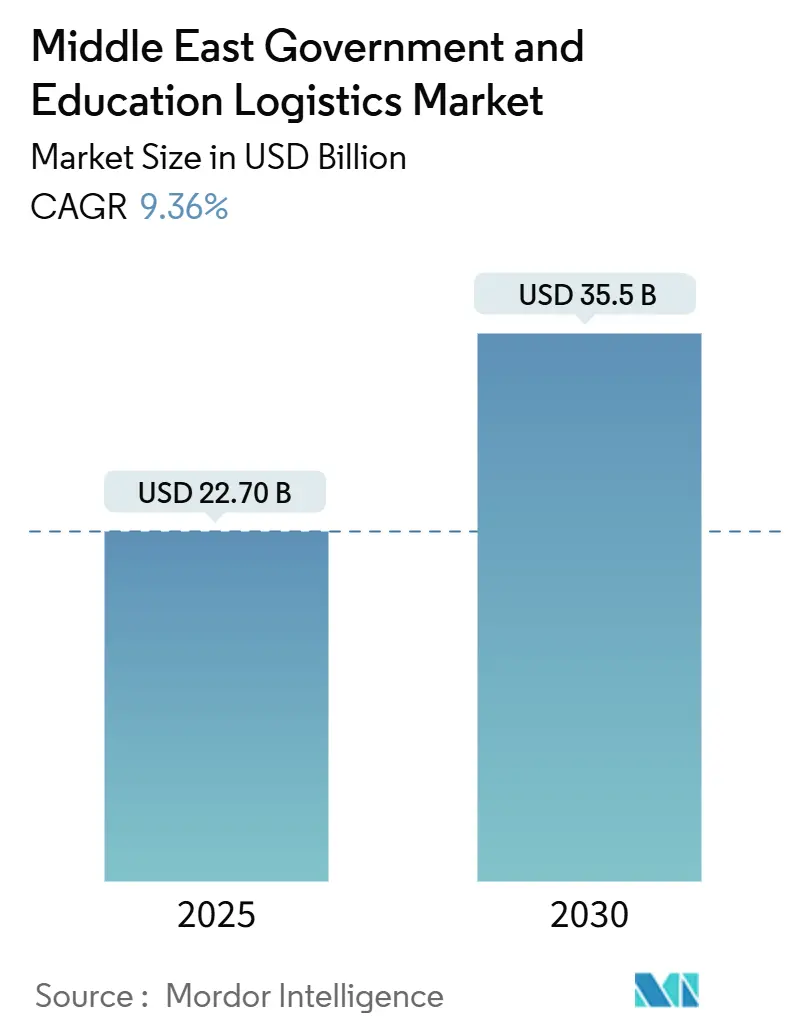

| Market Size (2025) | USD 22.70 Billion |

| Market Size (2030) | USD 35.5 Billion |

| Growth Rate (2025 - 2030) | 9.36% CAGR |

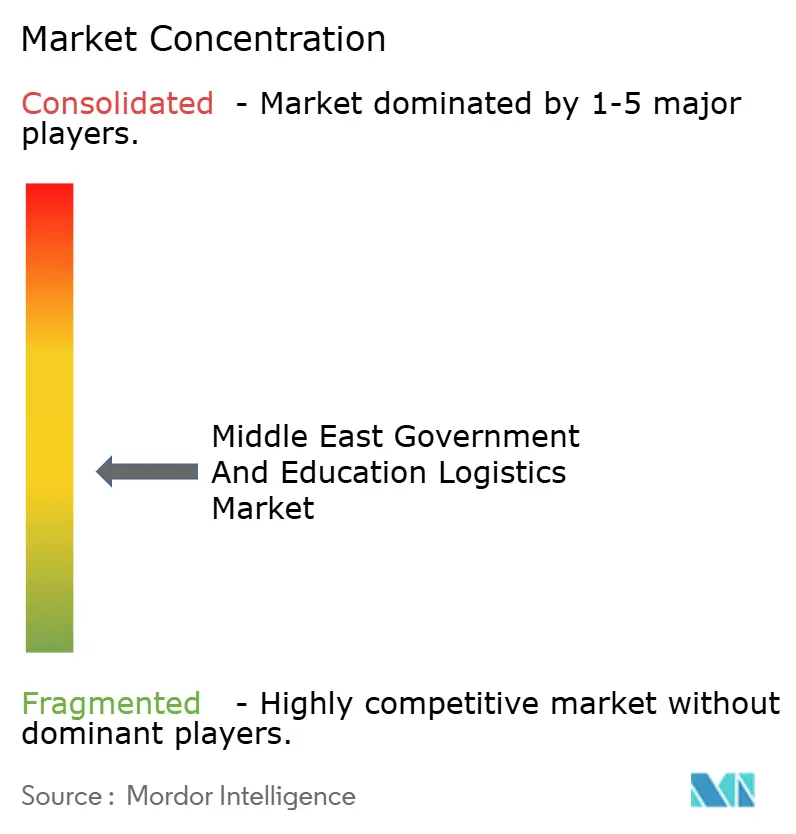

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Government And Education Logistics Market Analysis by Mordor Intelligence

The Middle East Government And Education Logistics Market size is estimated at USD 22.70 billion in 2025, and is expected to reach USD 35.5 billion by 2030, at a CAGR of 9.36% during the forecast period (2025-2030).

Continued Vision-2030 digital-government programs, sweeping school-building plans, and expanding defense procurement pipelines sustain this upward trajectory. Governments are embedding blockchain into purchase workflows, increasing real-time tracking requirements; smart-city projects in the United Arab Emirates (UAE) are pulling sophisticated reverse-logistics and temperature-controlled storage deeper into the service mix. Saudi Arabia’s NEOM build-out drives high-volume movements of construction and technology assets, while Red Sea disruptions accelerate demand for resilient multi-modal corridors. Intensifying humanitarian-aid activity and large-scale e-learning hardware roll-outs further boost specialized handling, positioning value-added services as a critical growth lever.

Key Report Takeaways

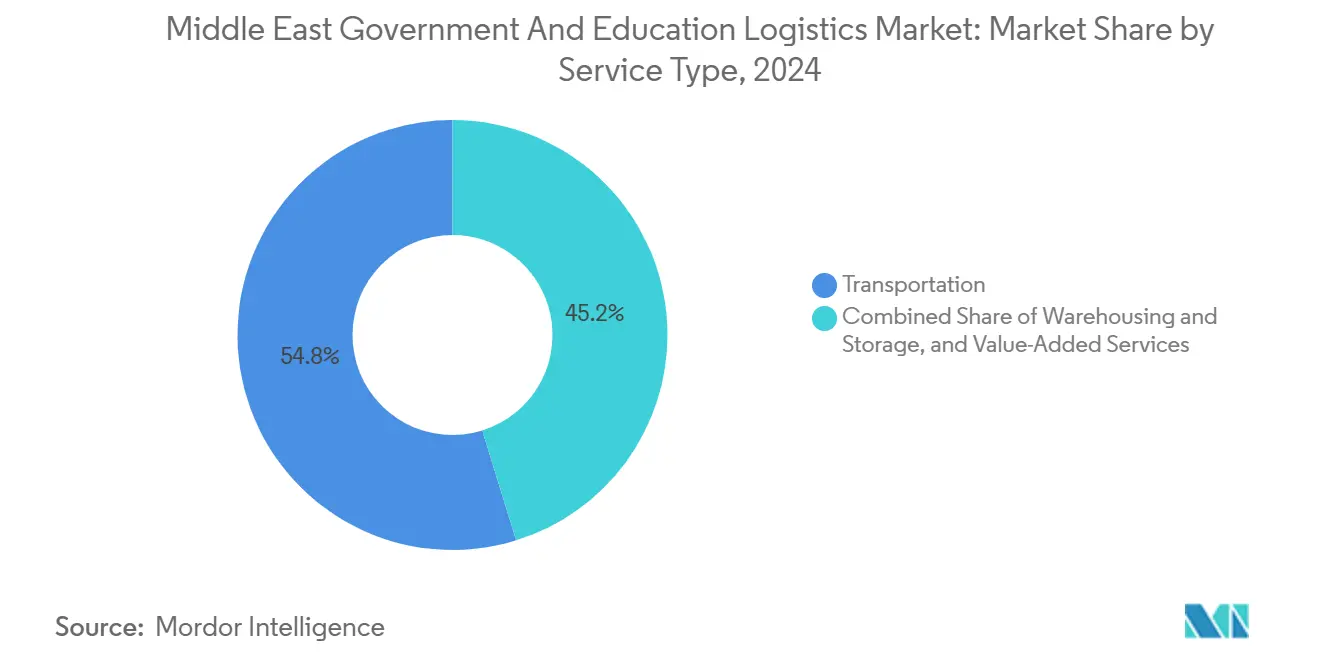

- By service type, transportation held 54.80% of Middle East government and education logistics market share in 2024, whereas value-added services are advancing at an 11.20% CAGR through 2030.

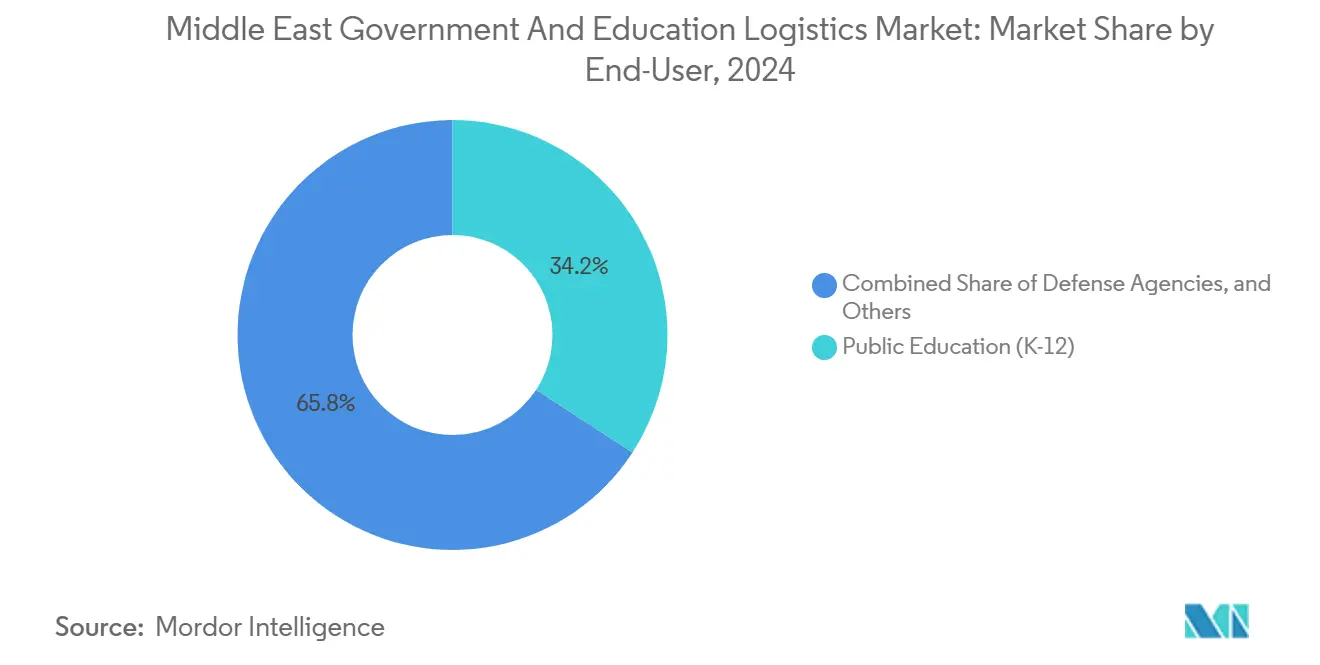

- By end-user, public education (K-12) accounted for 34.20% of the Middle East government and education logistics market size in 2024; defense agencies post the fastest 10.50% CAGR to 2030.

- By geography, Saudi Arabia led with 36.35% share in 2024, while the UAE is set to expand at a 10.22% CAGR through 2030.

Middle east holds a defined position within a broader international distribution. The government and education logistics market share data by Mordor Intelligence maps that allocation across all contributing regions, globally.

Middle East Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 digital-government mandates | +2.8% | Saudi Arabia primary; UAE, Qatar follow | Medium term (2-4 years) |

| E-learning hardware roll-outs | +2.1% | Global focus with MENA concentration | Short term (≤ 2 years) |

| GCC logistics-zone infrastructure build-out | +1.9% | GCC core; wider Middle East spill-over | Long term (≥ 4 years) |

| Reverse-logistics for EdTech donation | +0.9% | UAE & Saudi Arabia primary | Medium term (2-4 years) |

| Blockchain for public-sector transparency | +1.2% | UAE & Saudi Arabia leading | Long term (≥ 4 years) |

| Humanitarian-aid corridor demand | +0.7% | Conflict-adjacent areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Digital-Government Supply-Chain Mandates Drive Procurement Revolution

Saudi Arabia and the UAE now integrate blockchain and IoT across public procurement, obliging logistics partners to provide end-to-end digital visibility. In 2024, Dubai’s fully automated declarations hit 1.13 million, showcasing higher throughput under paperless customs workflows. Large ministries require AI-enabled route optimization and instant compliance documentation, effectively raising the minimum technological standard for service providers. These mandates foster demand for value-added services ranging from automated document generation to tamper-proof asset tracking, shifting competitive advantage toward operators with robust data-integration suites. Logistics firms that previously specialized in basic freight now find profitable niches in compliance consulting and system integration as government clients insist on demonstrable transparency[1]“Gulf Cooperation Council: Pursuing Visions Amid Geopolitical Turbulence,” International Monetary Fund, imf.org.

E-Learning Hardware Roll-Outs Accelerate Educational Infrastructure Logistics

Rapid student-population growth—projected to add 25 million learners by 2030—pushes ministries to ship classroom devices, interactive panels, and networking gear on compressed schedules. Saudi Arabia’s annual construction of hundreds of schools amplifies inbound volumes of structural components and technology kits. In the UAE, simultaneous smart-classroom upgrades create complex coordination between construction and IT supply chains. Cargoes often combine fragile electronics with heavy building materials, necessitating multimodal bundles and strict temperature-control protocols. As refresh cycles shorten to three-year intervals, reverse-logistics loops form, allowing certified refurbishment and redeployment into disadvantaged districts, deepening market diversification[2]“United Arab Emirates: 2024 Article IV Consultation,” International Monetary Fund, imf.org.

GCC Logistics-Zone Infrastructure Build-Out Creates Regional Connectivity Hub

Free-zone investments such as Jebel Ali Free Zone, which facilitated USD 169 billion in trade during 2023, deliver streamlined customs, robotics-based container handling, and bonded warehousing that shorten lead times for government tenders. BOXBAY high-bay storage reduces land use, allowing dense throughput of education hardware within ports. Saudi Arabia’s dry-ports network and rail connectivity upgrades further integrate inland cities into the Gulf supply grid. This infrastructure underpins cost-effective staging for regional public-sector contracts, bolstering the Middle East government and education logistics market by lowering the total landed cost of imported learning technologies and defense supplies.

Reverse-Logistics for EdTech Donation Programs Establishes Circular Economy Framework

The Royal-court-certified Ertiqa program processed 223,504 devices by late 2024, redistributing 97,430 refurbished units to schools, demonstrating scalable reverse-logistics models. Compliance with Blancco data-wiping standards secures donor confidence, making device turnover predictable and auditable. Similar schemes operated by Emirates Red Crescent—now active in all seven emirates centralize collection and refurbishment, creating repeatable volume for specialized 3PLs. Service layers include secure chain-of-custody, component-level testing, and targeted redistribution routes into North Africa and South Asia, broadening regional market exposure for temperature-controlled and vault-secured transport niches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical route disruptions | -1.8% | Region-wide, global supply impact | Short term (≤ 2 years) |

| Complex non-GCC customs procedures | -1.2% | Non-GCC Middle East | Medium term (2-4 years) |

| Shortage of secure temperature-controlled sites | -0.9% | Secondary cities | Long term (≥ 4 years) |

| Volatile oil revenue curbing budgets | -1.4% | Oil-dependent GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Route Disruptions Force Supply-Chain Reconfiguration

Red Sea attacks slashed Suez Canal throughput by 42% in 2024, pushing 40-foot container rates up and elongating transits by 10-14 days. Government tenders for school openings and defense spares incurred penalties when handover dates slipped. Rerouting via the Cape of Good Hope drove insurance surcharges and spurred Gulf ports to accelerate rail links to Levant markets. Operators now lock in dual-routing contracts and forward-depots to buffer volatility, but capital tied up in inventory tempers overall market expansion[3]“Are These Five Trends Disrupting or Driving Logistics Growth?,” World Economic Forum, weforum.org.

Complex Non-GCC Customs Procedures Create Operational Bottlenecks

Turkey’s multi-agency inspections, often adding 3-5 days, and Egypt’s overlapping equipment licensing slow cross-border educational-kit deliveries. Logistics providers manage separate document stacks for each non-GCC state, raising administrative overhead. Absence of mutual recognition for school-lab equipment forces redundant safety certifications. These frictions inflate cost-to-serve and deter smaller vendors from bidding on regional education tenders, trimming attainable volume for the Middle East government and education logistics market[4]“Debt and Fiscal Outlook Report for the Arab Region,” United Nations ESCWA, unescwa.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Emerge as Growth Engine

Transportation accounted for 54.80% of Middle East government and education logistics market share in 2024, underscoring the centrality of road and sea networks for moving school materials and government assets. Road freight dominates last-mile runs into remote provinces, while sea lanes move bulk construction inputs. Airfreight volumes rise when ministries fast-track e-learning kits ahead of academic terms. The Middle East government and education logistics market size tied to value-added services is projected to grow at 11.20% CAGR to 2030, reflecting heightened demand for blockchain-enabled documentation, secure data-wiping operations, and temperature-controlled storage.

Digitization pushes providers to stack analytics, customs-bonded warehousing, and refurbishment labs alongside freight offerings. Automated storage at Gulf free-zones shortens pick-and-pack cycles for replacement tablets, reducing downtime in smart classrooms. Reverse-logistics chains mature as refurbished devices re-enter public schools, turning disposal into a revenue stream. Government RFPs now bundle freight with compliance portals and sustainability reporting, making integrated value-added services decisive for contract awards.

By End-User: Defense Agencies Accelerate Amid Regional Security Concerns

Public education retained 34.20% share of Middle East government and education logistics market size in 2024, a result of extensive school construction and rapid technology deployments. Shipments include desks, textbooks, smart-boards, and nutritional supplies. Higher-education institutions add lab equipment and research reagents, deepening complexity. Defense agencies, however, register a 10.50% CAGR to 2030, the fastest among all end-users, as geopolitical tensions boost demand for armored transport, classified warehousing, and rapid humanitarian-aid lifts.

Specialized corridors servicing defense orders often overlap with NGO relief routes, creating hybrid flows that require strict segregation, chain-of-custody, and export-control compliance. Central and local government units modernize procurement, channeling more spend through digital marketplaces that pre-qualify logistics partners on transparency criteria. NGOs and international organizations capitalize on these certified networks to route educational kits into conflict-impacted districts, further diversifying end-user cargo mixes.

Geography Analysis

Saudi Arabia held 36.35% of the Middle East government and education logistics market share in 2024, powered by NEOM mega-project imports, nationwide school builds, and mandatory digital procurement. The kingdom’s human-capability program, targeting 1.7 million participants, drives bulk shipments of training equipment and learning materials. Blockchain pilots in Riyadh procured 50,000 smart tablets with end-to-end digital tagging, showcasing rising service sophistication. Rural provinces still rely on road caravans, making expansion of rail links a government priority.

The UAE posts the strongest 10.22% CAGR through 2030, leveraging Jebel Ali’s USD 169 billion trade platform and BOXBAY automation that compresses land use while doubling stack density. Dubai Customs’ digital portals cut clearance times for education imports to hours, cementing the emirate’s hub role. Emirates Red Crescent’s nationwide collection centers generate circular flows of refurbished devices, sustaining reverse-logistics lanes into broader MENA. Abu Dhabi’s AI-enabled procurement dashboards integrate carrier performance data, incentivizing on-time-delivery and transparent carbon reporting.

Turkey and Egypt capitalize on strategic geography, connecting European suppliers to Gulf classrooms and defense buyers. Turkey’s rail improvements shorten transit from Istanbul factories to GCC ports, though customs layers still add delays. Egypt’s dual ports at Alexandria and Sokhna funnel educational hardware into North Africa, with donor-funded programs stimulating steady inbound volumes. Smaller GCC states—Qatar, Bahrain, Kuwait, and Oman—share free-zone synergies, allowing pooled warehousing for regional tenders. Outside the GCC, emerging markets such as Jordan and Iraq display incremental growth, albeit capped by security risks and infrastructure gaps.

Mordor Intelligence delivers a comprehensive view of the government and education logistics market across all major regions such as North America, Europe, and Africa, alongside country-level analysis for Germany, Canada, Spain, United Kingdom, France, and Russia, each offering a view of the local market realities.

Competitive Landscape

Regional champions and global integrators share a moderately concentrated playing field. Market leaders combine deep Gulf relationships with advanced technology stacks, positioning them for large-volume government contracts. DP World leverages port automation and bonded warehousing to offer door-to-door visibility, while its economic zones provide one-stop customs and compliance solutions. DHL’s joint venture with Aramco, ASMO, melds global process excellence with local regulatory knowledge, enabling sophisticated procurement fulfillment for ministries and defense customers.

Aramex exploits last-mile dominance within urban Saudi and Emirati centers, integrating digital lockers and mobile app tracking demanded by public-school ICT projects. Bahri Logistics extends its fleet beyond energy to government cargo, deploying roll-on-roll-off vessels that handle armored vehicles and emergency shelters. Smaller 3PLs compete on niche services such as Blancco-certified data erasure or temperature--controlled micro-fulfillment.

Barriers to entry hinge on ISO security certifications, government-approved blockchain integrations, and the ability to stage inventory inside free-zones. Mergers and technology-focused partnerships are intensifying as participants seek scale and capability breadth.

Middle East Government And Education Logistics Industry Leaders

Aramex

Bahri Logistics

Saudi Post (SPL)

DHL Group

DSV A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DP World added new economic zones, with Jebel Ali Free Zone hitting USD 169 billion trade value and rolling out blockchain-enabled compliance dashboards.

- December 2024: ASMO, the DHL–Saudi Aramco venture, began regional operations centered on automation, robotics, and AI for public-sector logistics.

- October 2024: Aramex expanded its government-services portfolio at Saudi Aramco’s annual exhibition, boosting specialized education-infrastructure support.

- September 2024: DP World unveiled the BOXBAY high-bay system, stacking containers 11 stories high and cutting land use by two-thirds.

Middle East Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing and Storage | |

| Value-Added Services |

| Central/Federal Government |

| State and Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| United Arab Emirates |

| Saudi Arabia |

| Turkey |

| Egypt |

| Qatar |

| Bahrain |

| Kuwait |

| Oman |

| Rest of Middle East |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State and Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| Qatar | ||

| Bahrain | ||

| Kuwait | ||

| Oman | ||

| Rest of Middle East |

Key Questions Answered in the Report

What is the current value of the Middle East government and education logistics market?

The market stands at USD 22.7 billion in 2025 and is on track to reach USD 35.5 billion by 2030.

Which service type is expanding fastest?

Value-added services, encompassing blockchain-based documentation, temperature-controlled storage, and device refurbishment, are growing at an 11.20% CAGR.

Why are defense agencies a high-growth end-user?

Heightened regional tensions and humanitarian-aid missions demand secure, rapid, and transparent logistics, driving a 10.50% CAGR in defense-related volumes.

How do Vision 2030 initiatives influence logistics requirements?

These mandates enforce end-to-end digital visibility and blockchain compliance, raising demand for integrated technology-driven logistics solutions.

What infrastructure gaps limit market expansion?

Secondary cities lack sufficient temperature-controlled warehouses, constraining the movement of sensitive education and government materials.

Which country shows the fastest market growth to 2030?

The United Arab Emirates is set to expand at a 10.22% CAGR, propelled by Dubai’s smart-city and free-zone advantages.

Page last updated on: