Canada Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

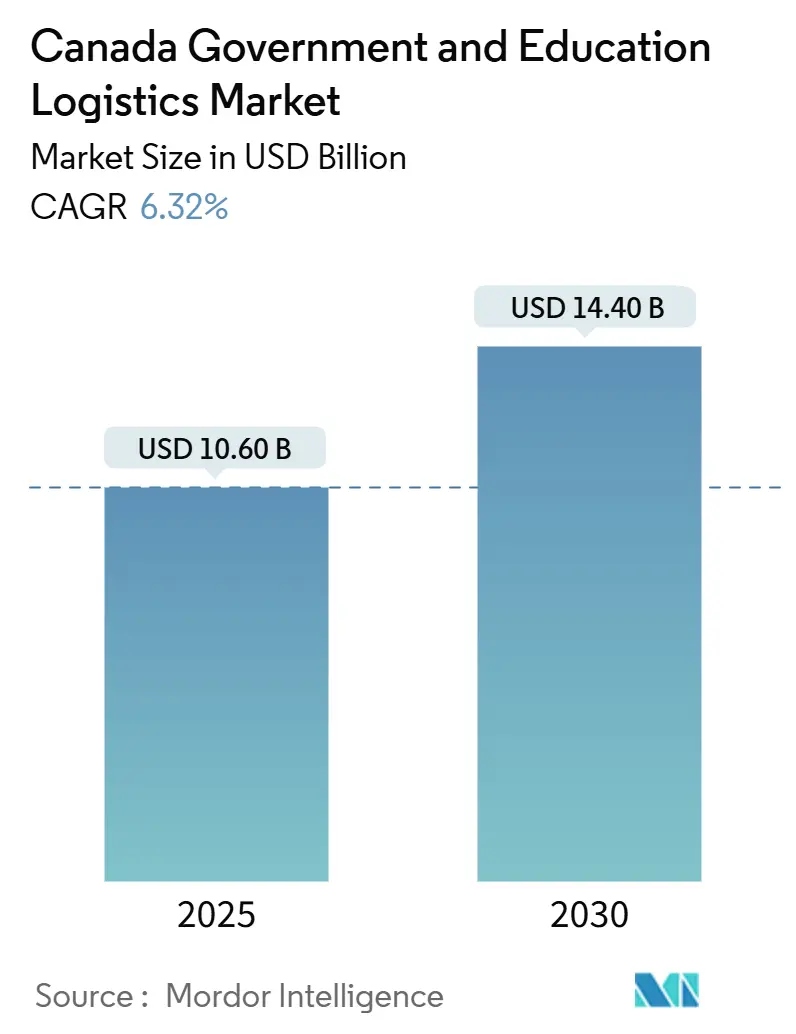

| Market Size (2025) | USD 10.60 Billion |

| Market Size (2030) | USD 14.40 Billion |

| Growth Rate (2025 - 2030) | 6.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Government And Education Logistics Market Analysis by Mordor Intelligence

The Canada Government And Education Logistics Market size is estimated at USD 10.60 billion in 2025, and is expected to reach USD 14.40 billion by 2030, at a CAGR of 6.32% during the forecast period (2025-2030).

The expansion emerges from concurrent federal infrastructure modernization, accelerated defense procurement, and province-wide school-facility upgrades. Housing-accelerator funds, student-housing GST relief, and a pledge to construct 4 million homes by 2031 amplify construction-materials flows, while defense programs such as the Logistics Vehicle Modernization initiative raise demand for oversized and classified freight. Frequent restocking of strategic medical reserves further fuels temperature-controlled warehousing, and energy-efficiency retrofits of public buildings add steady volumes of sustainable construction supplies.

Key Report Takeaways

- By service type, transportation led with 43.20% of the Canada government and education logistics market share in 2024; value-added services are projected to expand at an 8.50% CAGR through 2030.

- By end-user, the Central/Federal government held 29% of the Canada government and education logistics market size in 2024, while higher-education institutions are expected to record the highest projected 8.90% CAGR to 2030.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Canada. The government and education logistics market share in our global report expresses these relative weights.

Canada Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Defence capital-equipment freight surge | +1.8% | Ontario, Quebec, national corridors | Medium term (2-4 years) |

| Infrastructure Bank project-cargo demand | +1.4% | Western provinces | Long term (≥4 years) |

| School-modernisation FF&E logistics | +1.1% | Alberta, Ontario | Medium term (2-4 years) |

| Remote modular-classroom transport | +0.9% | Northern territories, rural regions | Short term (≤2 years) |

| Secure cold-chain for defence R&D | +0.7% | National | Long term (≥4 years) |

| Rural broadband gear last-mile | +0.6% | Rural Canada, northern territories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Defence Capital-Equipment Freight Surge

The CAD 19 billion (USD 13.2 billion) Canadian Surface Combatant program, CAD 1.5 billion (USD 1.04 billion) Logistics Vehicle Modernization project, and rising Arctic surveillance initiatives have combined to create unprecedented movement of armored vehicles, radar systems, and satellite components. Controlled Goods Program mandates limit foreign ownership participation, which elevates pricing for qualified domestic providers[1]Department of National Defence, “Government of Canada announces Logistics Vehicle Modernization Project,” canada.ca. Temperature-controlled, electromagnetically shielded transport for classified electronics deepens value-added demand, while the drive to lift defense outlays to 2% of GDP by 2032 assures multi-year project backlogs. Oversized equipment moving to remote bases proceeds mostly by rail and heavy-haul road convoys, forcing schedule coordination with intermittent bridge-repair closures on legacy corridors.

Infrastructure Bank Project-Cargo Demand

The CAD 35 billion (USD 24.3 billion) mandate of the Canada Infrastructure Bank funnels ongoing streams of turbines, transmission towers, and modular bridge segments toward renewable-energy and port-expansion sites. Specialized trailers, route-survey crews, and tandem-lift cranes lift per-move costs well above basic freight rates[2]Canada Infrastructure Bank, “Investments,” cib-bic.ca. Differing provincial escort and permit rules for oversize loads necessitate multi-jurisdictional compliance teams. Indigenous partnership requirements unlock opportunities for Indigenous-owned carriers, particularly along northern railheads where conventional integrators lack presence.

School-Modernisation FF&E Logistics

Alberta’s CAD 8.6 billion (USD 6 billion) school-construction budget and comparable programs in Ontario generate scheduled waves of classroom furniture, lab equipment, and interactive displays. Many tenders now bundle installation, packaging-waste removal, and phased deliveries that mirror construction milestones[3]Government of Alberta, “School Capital Planning,” alberta.ca. Sensitive cargo, such as science instrumentation, commands white-glove handling, and modular furniture yields repeat movements as districts reconfigure learning spaces. Sustainability benchmarks and local-labor quotas favor carriers that can document carbon-footprint reductions and community hiring.

Remote Modular-Classroom Transport

Remote and First Nations communities require fully outfitted prefabricated classrooms shipped on specialized low-bed trailers, each unit measuring roughly 24 ft × 60 ft. Komatik-ice road seasonality and unpaved stretches create tight delivery windows, often supported by helicopter lifts for final placement. Providers must coordinate crane rentals, foundation crews, and power hookups, creating opportunities for turnkey logistics contracts. Repeat demand stems from federal Indigenous-education plans scheduled through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing transportation infrastructure bottlenecks | -1.2% | Eastern provinces, national | Long term (≥4 years) |

| Procurement-cycle rigidity limiting agile sourcing | -0.8% | Federal, provincial | Medium term (2-4 years) |

| Scarcity of cold-chain capacity in northern territories | -0.6% | Northern territories | Short term (≤2 years) |

| Data-sovereignty concerns hindering 4PL integration | -0.4% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Ageing Transportation Infrastructure Bottlenecks

Thirty-five percent of Canadian roads and 40-year-old bridges rate fair to very poor, forcing detours and elevating maintenance costs[4]Canadian Construction Association, “Canadian Infrastructure Report Card 2019,” cca-acc.com. Lock dimensions on the St. Lawrence Seaway restrict vessel size, leading to cargo transshipment surcharges during peak project-cargo seasons. Rail channel constraints complicate secure routes for defense loads that cannot transit populous corridors. The federal infrastructure deficit of CAD 150 billion (USD 104.3 billion) burdens carriers, prompting the adoption of dynamic route-planning software and modal diversification to sustain reliability.

Procurement-Cycle Rigidity Limiting Agile Sourcing

Average 18-month federal tender cycles cause a mismatch between contract awards and fleet-investment timelines. Lowest-cost selection criteria underweight service quality, hindering the adoption of specialized capacity such as armored reefers. Provincial variants impose unique insurance floors, spurring compliance overhead that discourages small carriers from entering the Canada government and education logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates Through Modal Diversity

Transportation accounted for 43.2% of the Canada government and education logistics market share in 2024, propelled by wide modal requirements spanning road, rail, air, and sea. Road remains indispensable for last-mile access to remote school sites and isolated defense outposts, while rail offers cost advantages for heavy armor and construction materials. Airlift bridges winter freezes in Nunavut and Yukon, carrying textbooks, vaccines, and electronic components that cannot wait for thaw. The sector’s robustness is expected to maintain its lead even as specialized services grow, supported by federal bridge-rehabilitation funding that will gradually ease corridor congestion.

Value-added services, growing at an 8.5% CAGR to 2030, reflect rising demand for customs brokerage, configuration, and installation under unified contracts. White-glove deliveries of research microscopes and forensic DNA sequencers illustrate the shift toward integrated solutions. Warehousing & Storage follows, buoyed by strategic stockpiling mandates for medical supplies and emergency shelters that require temperature-control and inventory-tracking technology. Together, these developments cement transportation’s foundational role yet signal accelerating diversification of revenue streams within the Canada government and education logistics market.

By End-User: Federal Leadership Drives Institutional Adoption

The Central/Federal Government consumed 29% of the Canada government and education logistics market size in 2024, leveraging procurement scale to dictate service standards. Defense agencies within this cohort stipulate armored truck fleets, classified-network connectivity, and personnel security clearances, heightening barriers to entry. State & Local Government displays heterogeneous demand patterns: Alberta’s hydrocarbon prosperity underwrites high per-capita spend, whereas Atlantic provinces prioritize maintenance over expansion.

Public Education (K-12) delivers steady baseline freight cycles tied to academic calendars, while Higher Education Institutions accelerate at an 8.9% CAGR as campus research complexes import precision instruments. The Others segment—spanning Crown corporations and Indigenous governments—gains prominence through the federal 5% Indigenous-procurement quota, motivating joint ventures that expand geographic reach. Collectively, these end-users reinforce the Canada government and education logistics market’s resilience, distributing risk across multiple budgetary streams.

Geography Analysis

Ontario and Quebec together anchor the Canada government and education logistics market with dense government nodes and legacy defense installations. Ottawa-Gatineau’s procurement agencies spawn continuous paperwork and vetting journeys that culminate in physical deliveries to secure warehouses and labs. Montreal and Toronto ports funnel imported tech gear and naval components, though bridge repairs on Highway 401 often dictate nocturnal convoy scheduling to avoid daytime congestion.

Western provinces exhibit the swiftest growth, spearheaded by Alberta’s school-construction blitz and British Columbia’s modular-classroom program. Energy-sector royalties finance robust infrastructure spending, catalyzing large-volume freight of rebar, HVAC units, and seismic-grade concrete. Rocky-Mountain passes necessitate engineered routing and winter traction gear, while coastal inlets invite barge deliveries of pre-assembled housing kits to First Nations villages.

Northern territories show the highest percentage expansion, albeit from a low base. Arctic sovereignty missions, universal broadband roll-outs, and Indigenous education investments drive specialized flows of generators, science labs, and fiber spools. Seasonal road reliance means air and sealift are dominant during freeze-up and break-up, pushing logistics costs per kilogram to national highs. However, premium margins attract carriers that can deploy ice-class vessels or maintain bush-plane fleets, underscoring untapped potential for the Canada government and education logistics market.

Mordor Intelligence examines the government and education logistics market across diverse other regional markets as well, including Middle East, Africa, and Asia, while also offering granular country-level perspectives for Mexico, China, India, Japan, United Kingdom, and France and more.

Competitive Landscape

The market remains moderately fragmented as Canada Post Corporation leverages its universal-service mandate for small-parcel government mail, while Canadian National Railway and Canadian Pacific Kansas City dominate bulk and heavy-haul corridors. Market concentration is tempered by security rules that favor Canadian-owned entities and stipulate indigenous procurement thresholds. International integrators such as FedEx, UPS, and DHL target time-critical air cargo and urban educational consignments, employing technology platforms that handle customs pre-clearance and track sensitive assets in real time.

The value-added segment fosters differentiation: CN’s Smart Yard program integrates IoT sensors for rail-borne defense crates; Canada Post pilots electric vehicles paired with secure locker banks for school-tablet roll-outs. Indigenous-owned joint ventures, notably Arctic Gateway Group, gain traction through northern warehousing concessions that multinational firms cannot competitively enter due to content restrictions.

Sustainability expectations add another competitive layer. Carriers with ISO 14001 certifications score higher in tender evaluations, and those employing renewable-diesel mixes or rail-intermodal solutions gain cost advantages when fuel surcharges spike. As procurement modernization embeds emissions and community-benefit metrics, providers lacking green pathways risk exclusion from future contracts within the Canada government and education logistics market.

Canada Government And Education Logistics Industry Leaders

Canada Post Corporation

Metro Supply Chain Inc.

Canadian National Railway (CN)

Canadian Pacific Kansas City (CPKC)

Eastern Door Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Canadian National Railway committed CAD 3.4 billion (USD 2.36 billion) to 2025 capital projects, adding track sidings and yard automation that bolster government freight velocity.

- April 2025: UPS completed a USD 1.6 billion acquisition of Andlauer Healthcare Group, expanding cold-chain capacity for defense R&D materials and temperature-sensitive educational equipment.

- April 2025: DSV finalized its takeover of DB Schenker, scaling global reach and innovation budgets that enhance service depth in Canadian government contracts.

- January 2025: The federal government extended a USD 1 billion loan facility to Canada Post, ensuring continuity of public-sector parcel services amid volume volatility.

Canada Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

How large is the Canada government and education logistics market in 2025?

It is valued at USD 10.6 billion in 2025, advancing toward USD 14.4 billion by 2030.

Which service type holds the biggest share?

Transportation services lead with a 43.2% share in 2024, covering road, rail, air, and maritime modes.

Which segment records the fastest growth?

Value-added services grow at an 8.5% CAGR through 2030 as agencies seek specialized handling and integrated solutions.

What regional markets are expanding quickest?

Alberta and British Columbia outpace others thanks to infrastructure spending and modular classroom programs.

What are the key growth drivers?

Defense equipment modernization, Infrastructure Bank project cargo, and school-modernization FF&E logistics elevate demand.

Who are the leading companies?

Canada Post Corporation, Canadian National Railway, FedEx, UPS, and DHL stand out, with domestic security rules shaping competition.

Page last updated on: