North America Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

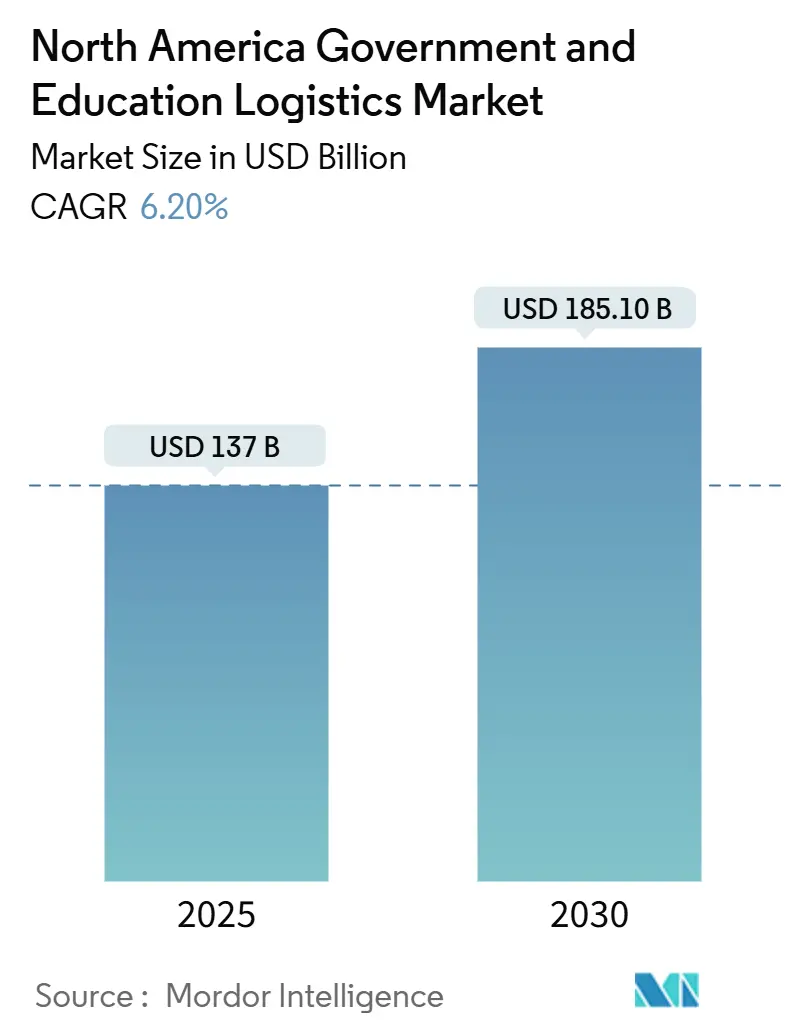

| Market Size (2025) | USD 137 Billion |

| Market Size (2030) | USD 185.10 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

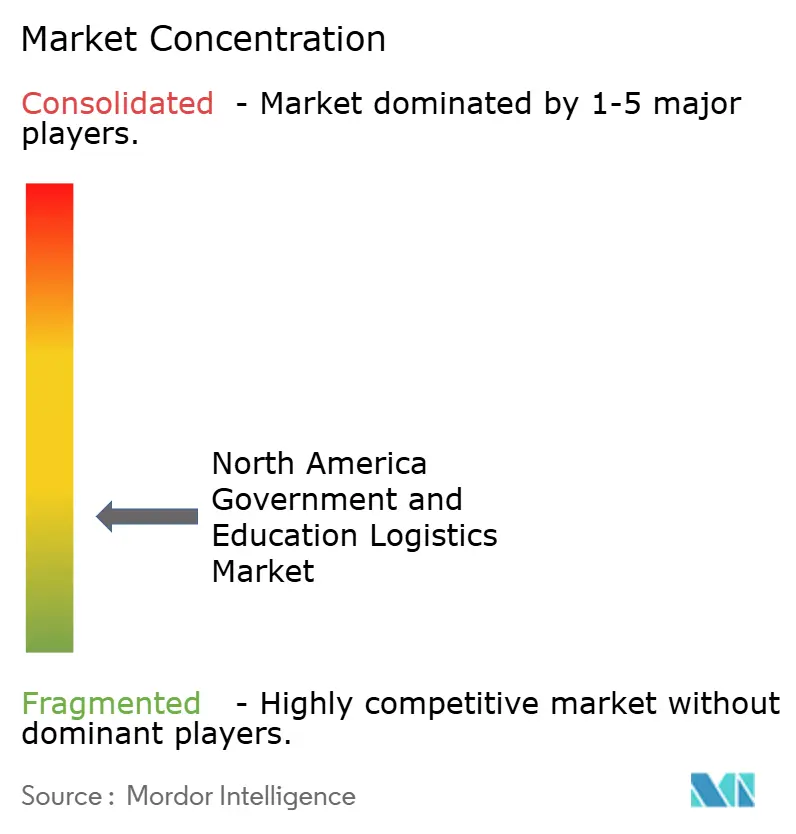

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Government And Education Logistics Market Analysis by Mordor Intelligence

The North America Government And Education Logistics Market size is estimated at USD 137 billion in 2025, and is expected to reach USD 185.10 billion by 2030, at a CAGR of 6.20% during the forecast period (2025-2030).

Growth is propelled by federal infrastructure funding, accelerating Department of Defense (DoD) outsourcing, and rapid digital procurement adoption that together upgrade transportation corridors, inject new compliance requirements, and shorten bid-to-award cycles. Providers that combine physical networks with real-time data visibility benefit from security-driven demand by federal agencies, state governments, and more than 5,300 higher-education institutions. At the same time labor shortages, particularly for drivers with security clearances, and the risk of FY-2026 budget sequestration create cost and capacity pressures that temper near-term expansion. Mexico’s procurement modernization and Canada’s green-fleet incentives further diversify regional growth levers, making multijurisdictional regulatory expertise a core differentiator in the North America Government and Education Logistics market.

Key Report Takeaways

- By service type, transportation held 45.8% of the North America Government and Education Logistics market share in 2024, while value-added services are projected to post the fastest 8.10% CAGR through 2030.

- By end-user, defense agencies led with 32.9% of the North America Government and Education Logistics market size in 2024; higher-education institutions are forecast to advance at a 7.90% CAGR to 2030.

- By country, the United States commanded 85.1% of 2024 revenues; Mexico is set to deliver the highest 8.25% CAGR through 2030.

North america contributes to a system defined not by any single geography but by the interaction of many. The global government and education logistics market data by Mordor Intelligence represents that combined structure.

North America Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-upgrade funding inflow | +1.2% | United States, spillover to Canada | Medium term (2-4 years) |

| Accelerated DoD outsourcing | +0.9% | United States, limited Canada defense cooperation | Short term (≤ 2 years) |

| K-12 meal-kit logistics mandates | +0.6% | United States, expanding to Canada | Medium term (2-4 years) |

| Surge in e-procurement platforms | +0.8% | North America-wide, Mexico adoption accelerating | Long term (≥ 4 years) |

| Campus micro-fulfillment pilots | +0.4% | United States and Canada university systems | Long term (≥ 4 years) |

| Green-fleet adoption incentives | +0.7% | United States and Canada, Mexico following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal Infrastructure Funding Accelerates Logistics Modernization

The Infrastructure Investment and Jobs Act allocates USD 110 billion to road and bridge upgrades that underpin government freight corridors, cutting transit times to remote federal sites and rural campuses, and stimulating facility relocations toward newly improved routes[1]U.S. Department of Transportation, “Infrastructure Investment and Jobs Act Implementation,” transportation.gov. Smart-highway mandates embedded in the funding tie eligibility to connected-vehicle systems and automated traffic management, pushing carriers to deploy IoT sensors and telematics that satisfy real-time tracking clauses in federal contracts. Road condition data issued by the Federal Highway Administration show double-digit reductions in congestion across corridors serving bases in the American South and research hubs in the Midwest. Logistics providers that align distribution centers with these corridors report freight-cost savings that they reinvest in cybersecurity upgrades, reinforcing the feedback loop between infrastructure and compliance.

DoD Outsourcing Strategy Reshapes Defense Logistics

The 2024 Strategic Logistics Transformation initiative shifts non-combat supply functions from in-house units to private providers, opening multi-year contracts that reward carriers already certified at CMMC Level 3. The Defense Logistics Agency has increased third-party involvement in base-level warehousing and global replenishment programs, creating addressable revenue pools that exceed commercial margins by 250 basis points[2]Defense Logistics Agency, “Strategic Logistics Transformation Initiative,” dla.mil. Barriers to entry intensify because bidders must demonstrate chain-of-custody encryption and 24-hour incident-response teams. NATO allies are duplicating the framework, positioning qualified North American vendors for incremental cross-border volume. Consequently, established integrators strengthen their lead, yet niche specialists with deep cyber competencies also find profitable footholds, driving competitive churn within the North America Government and Education Logistics market.

K-12 Nutrition Program Mandates Drive Specialized Food Logistics

Revised U.S. Department of Agriculture standards require districts to source fresher, locally grown produce, pushing logistics firms to establish micro-cold-chains and consolidate shipments from multiple small farms[3]U.S. Department of Agriculture, “School Nutrition Program Reforms 2024,” usda.gov. The School Nutrition Association reports that more than 60 districts added refrigerated trucks in 2025 to meet same-day delivery windows. Compliance demands robust temperature-monitoring and traceability, triggering deployment of passive RFID tags and blockchain registries. Logistics companies that can balance density economics with rural delivery obligations gain preferred-supplier status under multi-state cooperative contracts. Over the medium term these mandates will enlarge the per-pupil logistics spend and deepen service differentiation in the North America Government and Education Logistics market.

E-Procurement Platform Adoption Transforms Government Contracting

The General Services Administration’s transition to end-to-end electronic tendering shrinks bid cycles from weeks to days and integrates carrier performance dashboards directly into award algorithms[4]General Services Administration, “E-Procurement Platform Migration Report,” gsa.gov. State procurement authorities echo this shift; NASPO cites administrative cost reductions topping 17% after digital rollout. Artificial-intelligence matching engines quickly pair agency requirements with carrier capabilities, rewarding firms that invest in metadata standards and API connectivity. Mexico’s 2024 procurement modernization law mirrors the U.S. model and includes cross-border data-exchange provisions, enabling a seamless logistics spine across the USMCA region. This digital migration therefore enhances transparency, compresses onboarding hurdles, and enlarges the accessible pool of tenders in the North America Government and Education Logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget sequestration risk FY-2026 | −1.1% | U.S. federal agencies, limited state impact | Short term (≤ 2 years) |

| Skilled driver and warehouse labor shortage | −0.8% | North America-wide, acute in rural areas | Medium term (2-4 years) |

| Cyber-security compliance costs | −0.5% | United States and Canada, Mexico adopting | Long term (≥ 4 years) |

| Rural campus last-mile density challenge | −0.3% | Rural United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Sequestration Threatens Logistics Spending

The Congressional Budget Office projects automatic spending reductions in FY-2026 that could slash non-essential federal procurement outlays by double-digit percentages. Logistics contracts serving administrative offices, research grants, and community programs are particularly sensitive because agencies prioritize mission-critical deliverables under constrained budgets. Carriers prepare by embedding renegotiation clauses and scaling variable-cost models so they can flex down quickly without breaching service-level agreements. Although state and local governments remain outside federal sequestration, they rely on federal grant flows; thus ripple effects may dampen statewide contract volumes for at least two budget cycles. The uncertainty places a temporary headwind on capital-expenditure decisions within the North America Government and Education Logistics market.

Labor Shortage Crisis Constrains Operational Capacity

The American Trucking Associations note a 78,000-driver gap in 2025, compounded by clearance requirements that disqualify roughly 30% of otherwise qualified applicants. Specialized training for government cargo adds six to eight weeks and raises wage expectations, resulting in cost inflation that exceeds commercial averages. Warehousing faces parallel scarcities, especially for personnel certified in controlled-government-property handling. Remote campuses feel the pinch first, as lower freight density erodes economies of scale. Carriers counter with sign-on bonuses, accelerated clearance processing, and autonomous-vehicle pilots, yet tightness persists and restrains volume scalability in the North America Government and Education Logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates while Value-Added Services Accelerate

Transportation captured 45.8% of 2024 revenue in the North America Government and Education Logistics market, underscoring the non-negotiable need for secure movement. Within this umbrella, road haulage handles the bulk of daily loads, rail advances for non-urgent education consignments, and airlift supports time-critical defense shipments. Sea and inland waterways address niche flows such as international student lab equipment exchanges but remain capacity-limited by customs and security protocols.

Value-added services are expected to rise at an 8.10% CAGR (2025-2030) as agencies embed cybersecurity audits, regulatory documentation, and advanced track-and-trace into performance clauses. Providers differentiate by offering automated compliance portals that sync with e-procurement systems and by deploying prefabricated “clean rooms” inside warehouses for sensitive research assets. This premium capability mix elevates margins and gradually increases the service-mix weight in the North America Government and Education Logistics market size projection.

By End-User: Defense Leads, Education Outpaces

Defense agencies contributed 32.9% of 2024 billings, leveraging the DoD outsourcing wave for non-combat supply chains. Contract scopes span munitions transport, base pantry replenishment, and classified-material warehousing. Stringent vetting cements long-term supplier relationships, stabilizing baseline volumes in the North America Government and Education Logistics market.

Higher-education institutions are the fastest riser with a 7.90% CAGR (2025-2030) driven by campus expansions, laboratory build-outs, and micro-fulfillment pilots that aim to minimize in-house stockholding. K-12 systems add steady, policy-linked demand for meal-kit and instructional-material logistics, while state and local governments vary according to fiscal health and urbanization trends. Quasi-government entities and public-private partnerships emerge as a small but innovative cohort, often pioneering sustainability pilots that later migrate to mainstream segments of the North America Government and Education Logistics market.

Geography Analysis

The United States retains 85.1% of 2024 turnover thanks to the world’s largest defense budget, 430 federal agencies, and a postsecondary network serving more than 20 million students. USD 110 billion in federal infrastructure funds lower freight bottlenecks on Strategic Highway Network routes, prompting carriers to reposition hubs nearer to upgraded interstates and ports. Procurement diversity across 50 states obliges carriers to master a mosaic of regulations, but the volume reward offsets compliance costs in the North America Government and Education Logistics market.

Canada delivers stable mid-single-digit growth, buoyed by bilingual federal procurement, green-fleet incentives, and NORAD logistics integration that channels defense freight through shared corridors. Provincial education authorities, spread across vast geography, demand multimodal solutions that stitch together road, rail, and air to serve campuses from Vancouver Island to Newfoundland.

Mexico advances at an 8.25% CAGR through 2030 thanks to a 2024 digital-government overhaul and deeper university partnerships under USMCA frameworks. Cross-border flows of research equipment, textbooks, and e-learning hardware accelerate, increasing demand for bilingual documentation and CTPAT-aligned security. Combined, these dynamics diversify growth vectors and broaden addressable value in the North America Government and Education Logistics market size forecast.

The government and education logistics market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Middle East, and Africa. This is complemented by country-specific insights for Canada, Germany, Spain, United Kingdom, France, and Russia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The North America Government and Education Logistics market demonstrates fragmented competition with numerous specialized providers competing across different service segments and geographic regions. UPS, FedEx, and DHL leverage global fleets and ISO 28000 certifications to secure high-value contracts, while C.H. Robinson and XPO Logistics specialize in technology-rich value-added services. Regional carriers carve out niches in rural education routes or cross-border corridors, often partnering with integrators for nationwide reach.

Technology investment separates leaders from laggards. AI-driven route optimization, blockchain chain-of-custody ledgers, and warehouse robotics deliver quantifiable compliance and punctuality benefits that resonate with agency scorecards. Providers unable to finance continuous cyber upgrades gradually exit the federal arena, reallocating assets to commercial markets.

White-space opportunities persist in last-mile rural logistics and cybersecurity consulting, where margins exceed the broader North America Government and Education Logistics market average by 200–300 basis points.

North America Government And Education Logistics Industry Leaders

United Parcel Service, Inc. (UPS)

FedEx

DHL Group

C.H. Robinson Worldwide, Inc.

Ryder System

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kuehne + Nagel opened a 432,000 sq ft road-logistics complex in Laredo, Texas, consolidating three cross-docks and doubling U.S.–Mexico capacity.

- January 2025: BDP International partnered with Microsoft to embed AI logistics optimization across federal contracts, targeting a 25% delivery-efficiency uplift.

- October 2024: Scan Global Logistics launched a USD 25 million government-services unit targeting clearance-intensive contracts.

- September 2024: J.B. Hunt added 20 Nikola Tre fuel-cell electric vehicles to West Coast lanes supporting defense and education freight.

North America Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services and Others |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| United States |

| Canada |

| Mexico |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services and Others | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others | ||

| By Country | United States | |

| Canada | ||

| Mexico |

Key Questions Answered in the Report

How large is the North America Government and Education Logistics market in 2025?

The market is valued at USD 137 billion in 2025 and is projected to reach USD 185.1 billion by 2030.

Which service type generates the most revenue?

Transportation services contribute 45.8% of 2024 revenue, reflecting their central role in secure material movement.

Which end-user segment is expected to grow fastest?

Higher-education institutions are forecast to expand at a 7.90% CAGR through 2030 as campuses add research and micro-fulfillment projects.

What is the main growth driver across the region?

Federal infrastructure funding that modernizes highways and smart-corridor technologies is the single largest growth catalyst.

Which country in North America will grow the quickest?

Mexico is expected to post an 8.25% CAGR to 2030 owing to procurement digitalization and expanding cross-border education partnerships.

Page last updated on: