Germany Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

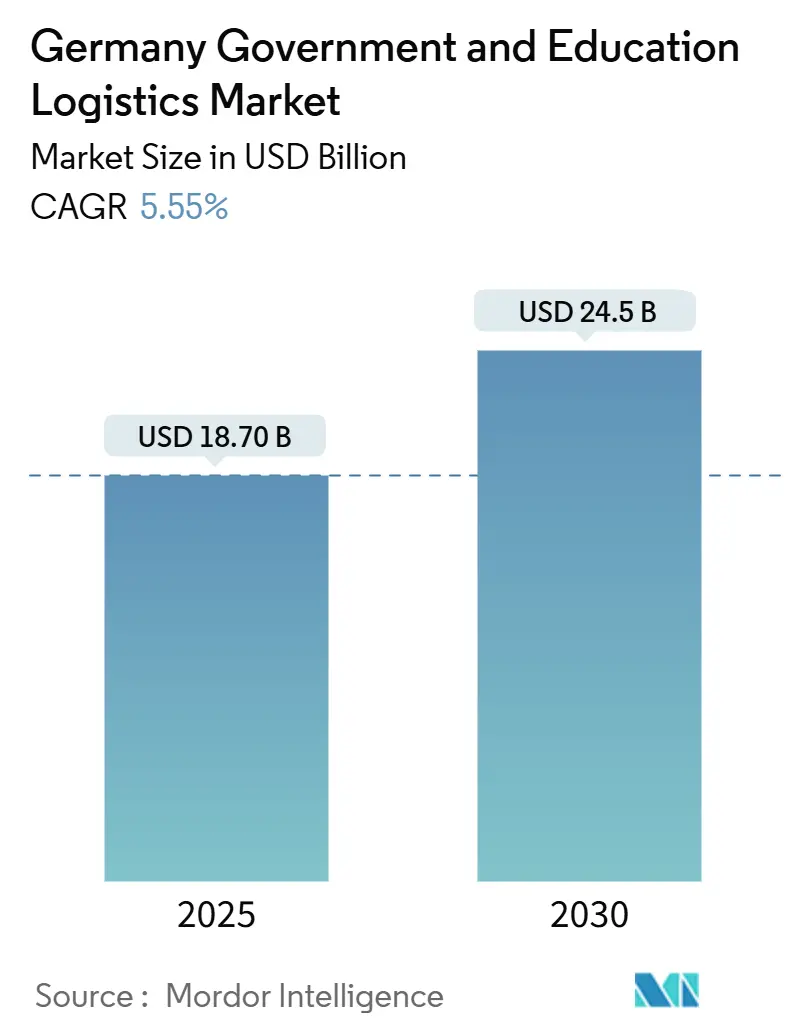

| Market Size (2025) | USD 18.70 Billion |

| Market Size (2030) | USD 24.5 Billion |

| Growth Rate (2025 - 2030) | 5.55% CAGR |

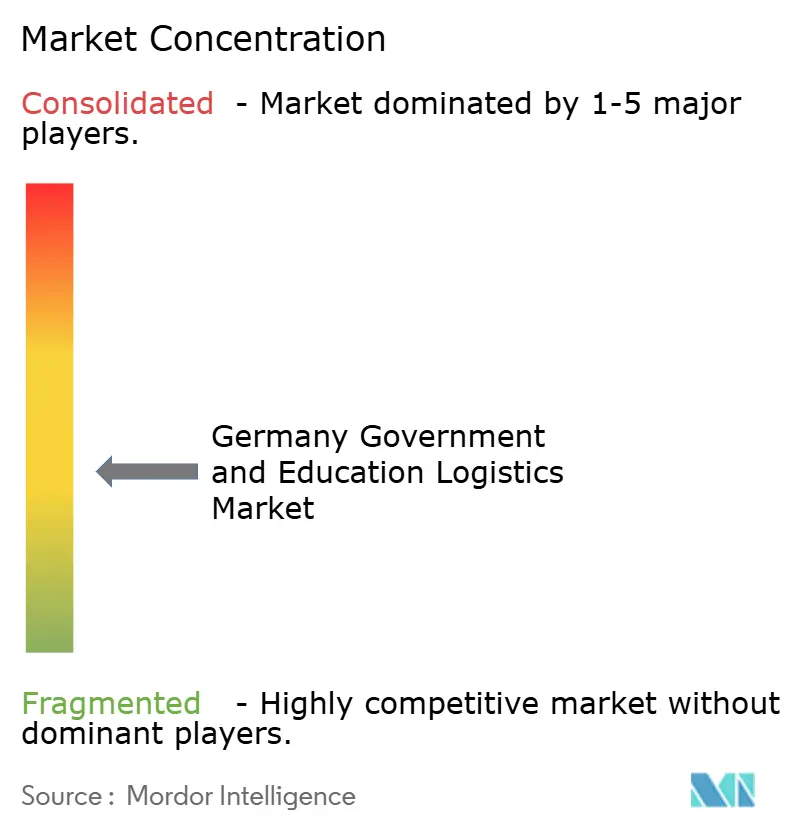

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Government And Education Logistics Market Analysis by Mordor Intelligence

The Germany Government And Education Logistics Market size is estimated at USD 18.70 billion in 2025, and is expected to reach USD 24.5 billion by 2030, at a CAGR of 5.55% during the forecast period (2025-2030).

Rising defense procurement, nationwide educational digitization, and large-scale public-infrastructure retrofits shape demand for specialized services that traditional commercial fleets cannot fulfill. Transport contracts linked to the Leopard 2A8 tanks, F-35 jets, and CH-47 Chinook helicopters command premium rates because freight corridors must support oversize loads and classified material. At the same time, the DigitalPakt Schule hardware rollout drives predictable semester-based distribution waves, while strategic medical-stockpile replenishment intensifies cold-chain requirements. Infrastructure renovation programs and NATO pre-positioning projects further expand the Germany government and education logistics market as federal, state, and municipal agencies lock in multiyear frameworks with providers that hold security clearances and temperature-controlled capacity.

Key Report Takeaways

- By service type, transportation led with 44.70% of the Germany government and education logistics market share in 2024; value-added services are projected to expand at a 6.10% CAGR through 2030.

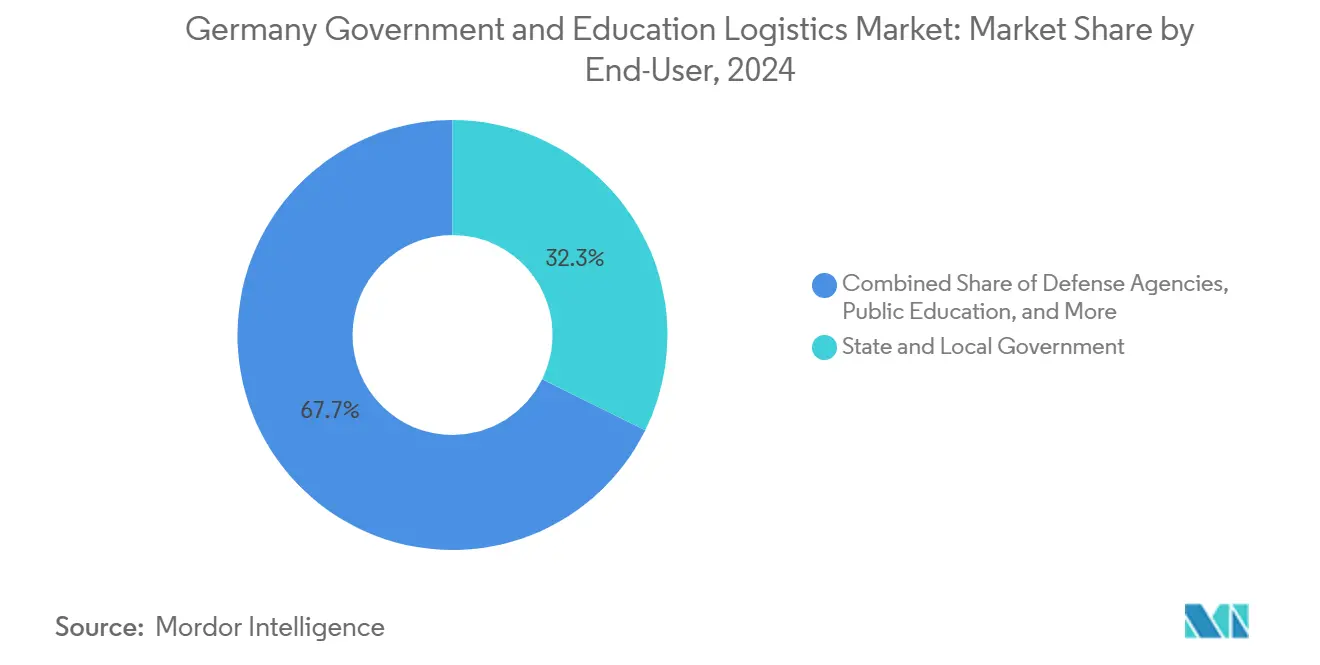

- By end-user, state and local government held 32.30% of the Germany government and education logistics market size in 2024, while higher-education institutions are expected to record the highest projected 7.20% CAGR to 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with Germany being one of the contributors. Our global government and education logistics market size represents that cumulative total.

Germany Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid procurement of Leopard 2A8 tanks, F-35 jets and CH-47 Chinook helicopters drives oversized and classified freight demand | +1.2% | National, concentrated in Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Nationwide roll-out of Schulcloud/Bildungslogin platforms triggers bulk networking-hardware distribution to ~40,000 schools | +0.9% | National, with priority in rural Baden-Württemberg, Saxony | Short term (≤ 2 years) |

| Replenishment of federal/state strategic medical stockpiles boosts temperature-controlled warehousing | +0.7% | National, concentrated in Berlin, Hamburg, Munich | Short term (≤ 2 years) |

| Energy-efficiency retrofits of public buildings accelerate construction-materials logistics | +0.6% | National, early gains in North Rhine-Westphalia, Bavaria | Long term (≥ 4 years) |

| NATO pre-positioned stock site expansion in Germany creates dedicated military warehousing | +0.5% | Regional, focused on Lower Saxony, Rhineland-Palatinate | Medium term (2-4 years) |

| Hybrid-learning university models spur frequent small-batch lab-equipment courier flows | +0.4% | National, concentrated in university cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Defense-Procurement Modernization Accelerates Specialized Logistics Demand

Germany’s accelerated defense program centers on 18 Leopard 2A8 tanks, F-35 jets, and CH-47F Chinook helicopters, each requiring heavy-haul trailers, military-grade airfreight, and classified-material handling that only cleared operators can provide[1]German Federal Ministry of Defence, “Defense Procurement Programs 2024-2030,” BMVG.DE. Premium contracts run 30-40% above commercial lanes because carriers must meet NATO STANAG 4280 guidelines and sustain spare-parts flows for decades. The Germany government and education logistics market, therefore, benefits from long-tail maintenance shipments that stabilize fleet utilization even after headline deliveries conclude.

Educational Digitization Creates Sustained Technology-Distribution Networks

The EUR 6.5 billion (USD 6.8 billion) DigitalPakt Schule investment obliges vendors to deliver tablets, Wi-Fi switches, and fiber components to roughly 40,000 schools on rigid semester deadlines[2]Federal Ministry of Education and Research, “DigitalPakt Schule Implementation Report 2024,” BMBF.DE. Hardware replacements must travel in sealed crates and be wiped under GDPR rules, fostering demand for value-added services such as secure de-installation and certified data destruction. Predictable project calendars allow providers to pre-position inventory and run milk-run routes that trim empty miles, bolstering margins inside the Germany government and education logistics market.

Medical Stockpile Replenishment Drives Temperature-Controlled Infrastructure Expansion

Federal guidelines mandate six-month national reserves of critical drugs and devices stored at 2-8 °C, while selected vaccines need -70 °C freezers[3]German Federal Institute for Drugs and Medical Devices, “Strategic Medical Stockpile Guidelines 2024,” BFARM.DE. These parameters narrow the supplier pool to GDP-compliant warehouses, pushing cold-chain fees 25-35% above ambient storage. Continuous rotation protocols produce monthly outbound and reverse-logistics cycles, enhancing warehouse revenue density.

Public-Building Energy Retrofits Generate Construction-Materials-Logistics Surge

A EUR 14 billion (USD 14.6 billion) budget targets insulation, heat-pump, and solar-panel retrofits across thousands of city halls, police stations, and schools[4]German Energy Agency, “Public Building Energy Efficiency Program Status 2024,” DENA.DE. Projects favor just-in-time deliveries because public facilities lack laydown yards. Consequently, forward-stocked consolidation hubs emerge near dense metropolitan clusters, unlocking route-optimization savings for carriers active in the Germany government and education logistics industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver and warehouse labour shortages inflate contract rates | -0.8% | National, acute in Hamburg, Bremen, Stuttgart | Short term (≤ 2 years) |

| Aging road-bridge / rail nodes create schedule unpredictability | -0.6% | National, critical in Ruhr Valley, eastern states | Long term (≥ 4 years) |

| Rising penalty clauses in PSO and school-bus contracts deter bidder participation | -0.4% | National, concentrated in rural states | Medium term (2-4 years) |

| GDPR-level cybersecurity requirements lengthen IT-logistics roll-outs | -0.3% | National, acute in federal government contracts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor Shortages Inflate Operational Costs across Service Categories

Germany lacks 120,000 licensed drivers, and clearances for defense hauling intensify scarcity, pushing line-haul rates 15-20% higher year-on-year. Warehouses compete for technicians to maintain automated systems, while 35% of current drivers near retirement. Consequently, some tenders in the Germany government and education logistics market attract only one or two bids, reducing price competition and elongating lead times.

Infrastructure Deterioration Creates Operational Unpredictability

Weight-restricted bridges impede 60-ton tank carriers, forcing detours that add mileage and risk schedule penalties. Deutsche Bahn maintenance shutdowns constrain overnight wagon slots needed for bulk hardware to rural schools, undermining on-time metrics embedded in public-sector contracts. High penalty clauses discourage smaller firms, curbing capacity elasticity within the Germany government and education logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates Yet Value-Added Services Surge

Transportation captured 44.70% of 2024 revenue as defense oversize loads, semester-based tech shipments, and construction materials keep road fleets fully employed. Rail brings lower cost per ton-kilometer for palletized routers headed to Saxony schools, and air handles classified spares for the F-35 fleet. The Germany government and education logistics market size for transportation thus remains the anchor revenue pillar even as carrier margins tighten around fuel and labor inputs.

Value-added services post a 6.10% CAGR through 2030, reflecting demand for in-school device installation, GDPR-compliant asset recovery, and NATO paperwork management. Providers integrate these tasks to lift yield per stop, reinforcing cross-selling within the Germany government and education logistics market. Project-based contracts also cushion seasonality, stabilizing asset utilization between defense convoy surges and educational peak windows.

By End-User: State Governments Lead While Universities Drive Growth

State and local administrations control 32.30% of 2024 spending because Germany’s Länder procure police vehicles, municipal IT, and public-building upgrades on separate budgets. Their distributed facilities require granular route planning and multi-stop drops that favor operators with nationwide depot arrays.

Higher-education institutions exhibit a 7.20% CAGR as hybrid learning expands small-batch lab shipments that recur every quarter, spreading volumes beyond semester peaks. Research-grant cycles inject high-value instrumentation with tight delivery tolerances, lifting the Germany government and education logistics market size tied to university campuses. Federal ministries concentrate fewer but larger consignments, mainly armaments and medical stockpiles, sustaining premium security-grade revenue.

Geography Analysis

Berlin anchors federal agency flows, with daily sealed-truck corridors to Bonn, Munich, and Hamburg that consolidate classified mail and diplomatic cargo. Bavaria and North Rhine-Westphalia combine dense defense factories, flagship universities, and retrofit construction sites, generating multi-category demand. Rhine ports at Hamburg and Bremen channel imported educational electronics and vaccine syringes, while inland Saxony leverages rail for school-cloud rollouts.

Eastern states face infrastructure backlogs, yet fiber-optic buildouts and public-building restorations create rising loads that propel local carriers into the Germany government and education logistics market. NATO hubs in Rhineland-Palatinate require bilingual documentation and 24-hour guarded yards, forcing operators to co-locate warehouses near U.S. airbases. Rural districts compel milk-run models for K-12 deliveries, but predictable school calendars permit carriers to pool orders and slash per-unit costs. The geographic mosaic thus rewards fleet flexibility and embedded state-level relationships.

Coverage of the government and education logistics market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, Middle East, and Africa, alongside detailed country-level intelligence for United Kingdom, France, Spain, India, Japan, and Mexico, each shaped by local operating conditions.

Competitive Landscape

The market tilts toward incumbents with security credentials and temperature-controlled space. DHL Group exploits its nationwide depot grid and Bundeswehr clearances to secure multiyear framework deals covering armored-vehicle parts, while Rhenus Group pairs bonded warehousing with in-house customs agents for NATO consignments. Dachser SE leverages university-city road hubs to bundle quarterly lab-equipment routes, enhancing load factors across southern Germany.

Midsize specialists target niches within the Germany government and education logistics market, such as ultra-cold vaccine storage or GDPR data-destruction logistics. Technology capabilities—real-time IoT trackers that feed ministries’ dashboards—differentiate bids more than rate cuts.

Recent mergers, including DSV’s acquisition of DB Schenker, signal consolidation around capital-intensive assets and cyber-secure IT stacks. Competitive intensity stays moderate because clearance renewals, driver vetting, and dedicated yards impose entry barriers that restrain commoditization.

Germany Government And Education Logistics Industry Leaders

DHL Group

Rhenus Group

Dachser SE

Kuehne + Nagel

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its takeover of DB Schenker, adding 38 German depots geared toward defense and public-sector clients.

- February 2025: Yusen Logistics opened a USD 100 million Bottrop hub co-funded by municipal authorities to handle educational-technology rollouts.

- February 2025: Dachser expanded its AI research partnership with Fraunhofer IAIS to optimize security-cleared route planning.

- November 2024: CEVA Logistics acquired Bolloré Logistics, strengthening multimodal capacity for emergency-supply contracts with the Federal Transport Ministry.

Germany Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

How big is the Germany government and education logistics market in 2025?

The Germany government and education logistics market size is USD 18.7 billion in 2025.

What is the forecast CAGR for this logistics segment through 2030?

The market is expected to post a 5.55% CAGR between 2025 and 2030.

Which service type holds the largest revenue share?

Transportation services lead with 44.70% share in 2024.

Which end-user category is growing fastest?

Higher-education institutions record the highest 7.20% CAGR through 2030.

What factor drives premium freight rates in defense logistics?

Oversize and classified consignments tied to Leopard 2A8 tanks, F-35 jets, and CH-47 helicopters require security-cleared heavy-haul corridors, inflating contract rates by 30-40%.

Page last updated on: