Africa Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

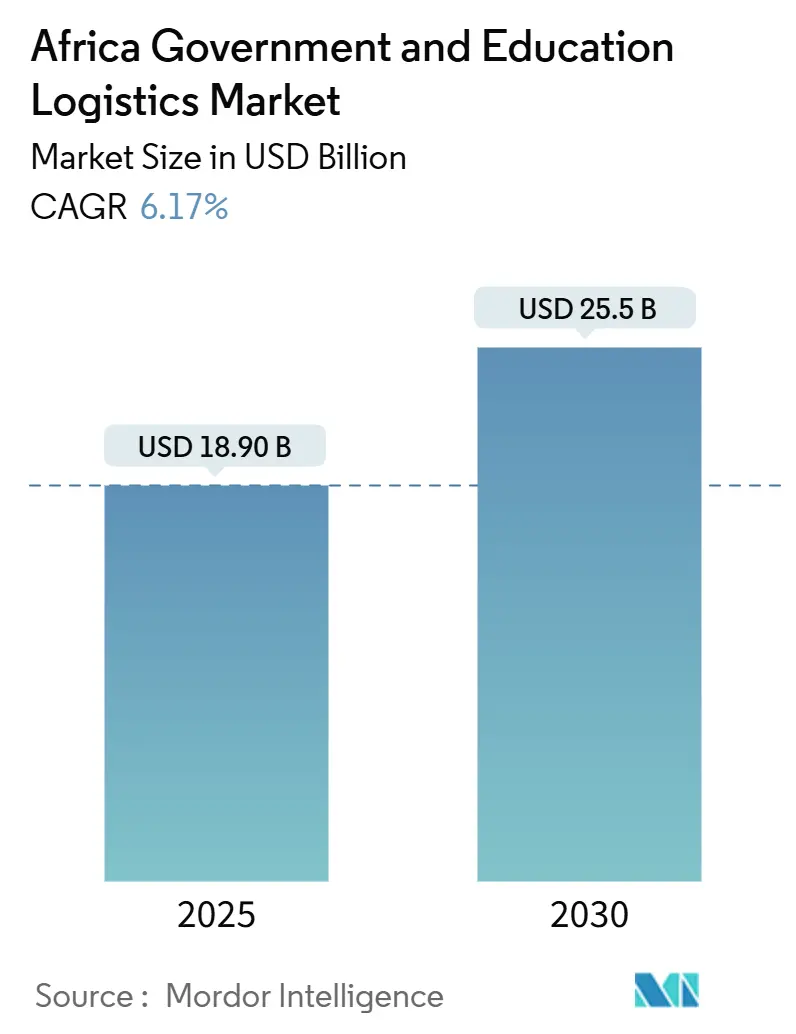

| Market Size (2025) | USD 18.90 Billion |

| Market Size (2030) | USD 25.5 Billion |

| Growth Rate (2025 - 2030) | 6.17% CAGR |

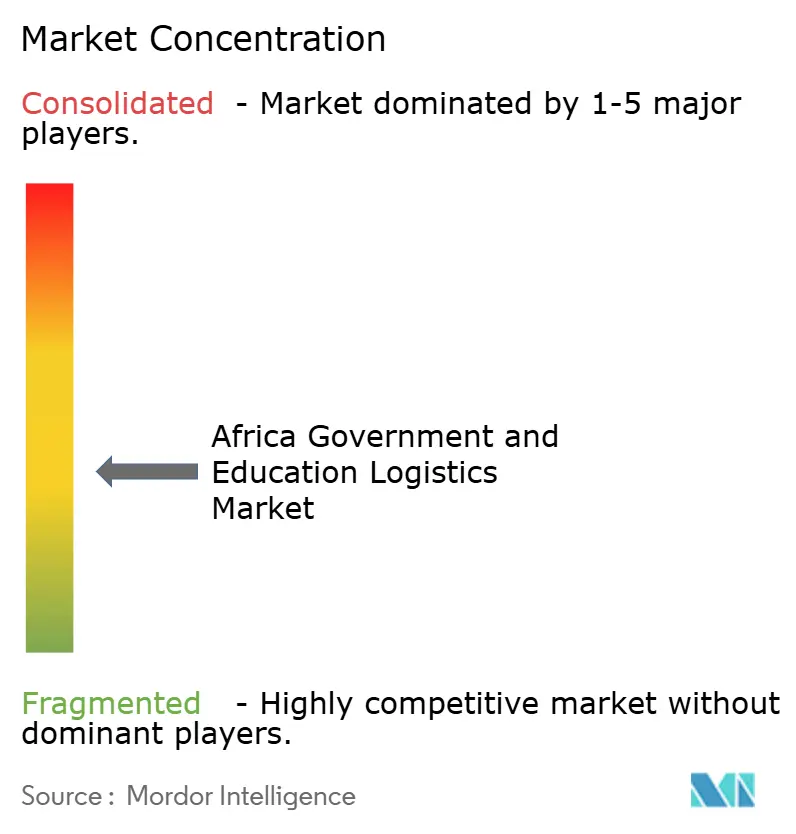

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Government And Education Logistics Market Analysis by Mordor Intelligence

The Africa Government And Education Logistics Market size is estimated at USD 18.90 billion in 2025, and is expected to reach USD 25.5 billion by 2030, at a CAGR of 6.17% during the forecast period (2025-2030).

The current growth reflects increasing adoption of e-procurement platforms, steady funding flows from multilateral lenders, and trade-facilitation gains tied to the African Continental Free Trade Area. Transportation services hold the largest share because ministries and school systems still depend heavily on road and multimodal moves to reach dispersed locations. Renewed emphasis on cold-chain capability and micro-warehousing supports the rise of value-added services, while digital freight exchanges shorten tender cycles and open the door for smaller carriers. Competitive pressure is intensifying as global players acquire regional operators to secure contract scale and technology depth. At the same time, governments channel larger slices of education budgets toward device roll-outs and facility upgrades, lifting demand for integrated supply chain solutions.

Key Report Takeaways

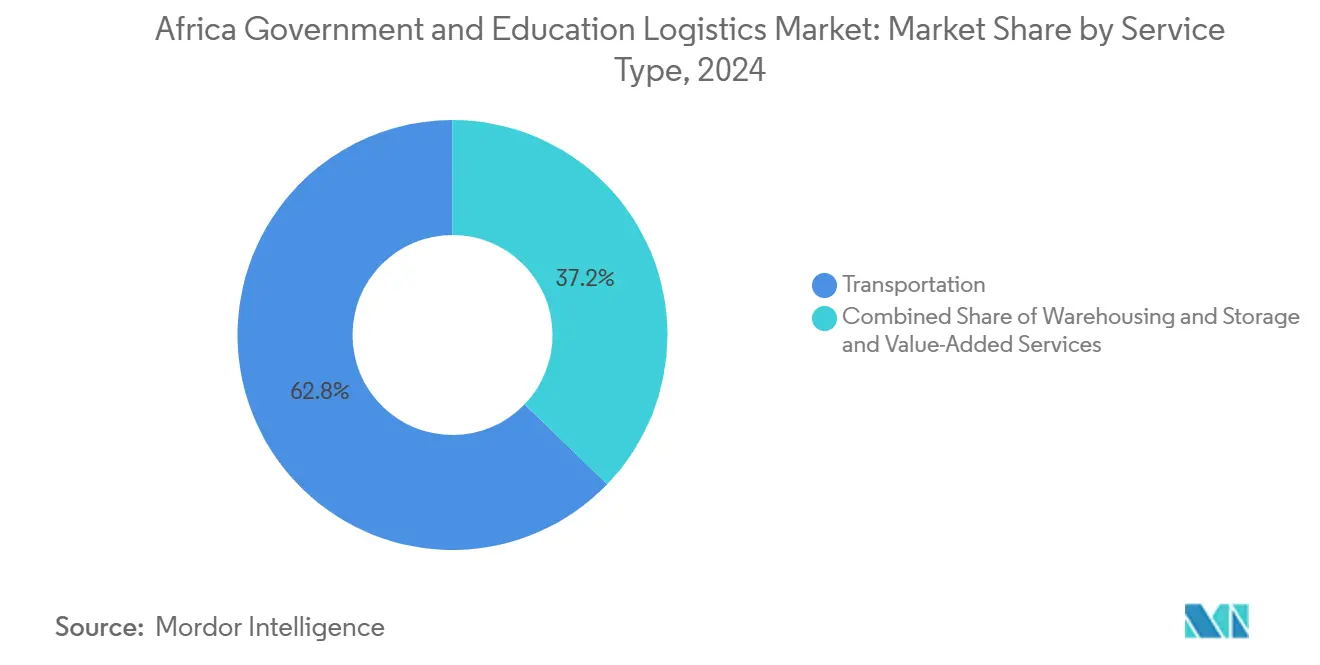

- By service type, transportation led with 62.80% of the Africa government and education logistics market share in 2024, while value-added services are projected to advance at a 12.80% CAGR through 2030.

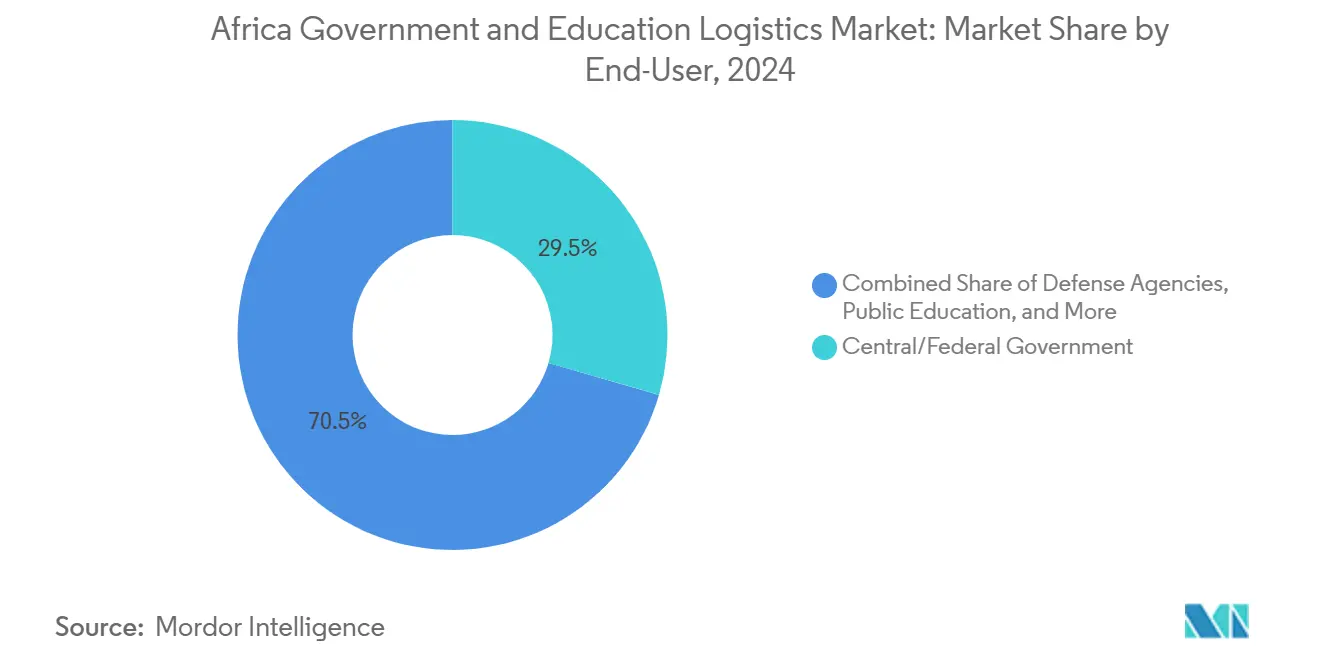

- By end-user, central and federal governments accounted for 29.50% of the Africa government and education logistics market size in 2024, and the public education K-12 segment is poised to expand at an 11.50% CAGR to 2030.

- By country, South Africa commanded a 23.67% share of the Africa government and education logistics market in 2024; Ethiopia is forecast to register the highest regional CAGR at 6.88% through 2030.

Dynamics observed within Africa present a holistic view when set against the broader international context. The government and education logistics market analysis by Mordor Intelligence provides that expanded global perspective.

Africa Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-sector outsourcing mandates accelerate 3PL uptake | +1.2% | South Africa, Nigeria, Kenya | Medium term (2-4 years) |

| AfCFTA trade-facilitation reforms cut border delays | +0.9% | ECOWAS and EAC corridors | Long term (≥ 4 years) |

| Booming EdTech roll-outs require device and content distribution | +1.5% | Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Expansion of AU Year of Education budgets lifts logistics spend | +0.8% | Least developed countries | Medium term (2-4 years) |

| Digital logistics marketplaces give ministries instant access to vetted carriers | +0.7% | Urban centers in major economies | Short term (≤ 2 years) |

| Solar-powered micro-warehouses at school hubs slash spoilage and diesel costs | +0.6% | Rural Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Public-sector Outsourcing Mandates Accelerate 3PL Uptake

Mandatory outsourcing rules in Ethiopia and Uganda require ministries to justify internal logistics operations that exceed cost thresholds, spurring steady shifts toward third-party logistics partnerships. Field studies in Uganda link technology-enabled 3PL use to measurable cost savings and higher on-time performance, prompting other governments to mirror the model. Providers with transport management systems and real-time visibility gain a clear preference during tender evaluations. Pilot projects in Tanzania’s education ministry show on-time textbook delivery rising sharply when private carriers replace in-house fleets[1]Africa Freedom of Information Centre et al., “Barriers and Solutions to Women's Participation in Public Procurement in Eastern Africa,” open-contracting.org.

AfCFTA Trade-Facilitation Reforms Cut Border Delays

Standardized customs procedures, electronic single windows, and harmonized documentation lower wait times along primary corridors, reducing freight dwell days for shipments of school supplies and laboratory equipment. As border processing falls, ministries can consolidate consignments and synchronize term start deliveries across several countries. UNECA estimates that faster crossings will lift intra-African freight demand significantly, placing fresh pressure on carriers to add capacity and to digitalize milestone reporting[2]United Nations Economic Commission for Africa, “Perspectives: The long winding road defining Africa's infrastructure development,” uneca.org.

Booming EdTech Roll-outs Require Device & Content Distribution

Tablet distribution campaigns under donor-financed projects multiply high-value, time-sensitive shipments that necessitate secure handling, tamper-evident packaging, and temperature-controlled storage. Ministries stipulate asset-tracking and proof-of-delivery integrations to monitor device flow to remote schools. The mix of electronics and printed materials elevates average shipment complexity and boosts revenue opportunities for providers that combine cross-dock, kitting, and reverse logistics services[3]World Bank, “World Bank Group Commits Record-Breaking Funding for Education,” worldbank.org.

Expansion of AU ‘Year of Education’ Budgets Lifts Logistics Spend

Higher allocations flow toward the least developed member states, earmarked for classroom refurbishment, library expansion, and teacher accommodation projects. Funders require robust supply chain audit trails, prompting ministries to adopt barcoding and warehouse management systems. Unified storage guidelines issued by the African Union in 2024 simplify vendor accreditation and align service-level metrics across borders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented tender cycles and slow payments to logistics vendors | -1.1% | West and Central Africa | Short term (≤ 2 years) |

| Chronic road-network gaps outside main corridors | -0.8% | Rural Sub-Saharan Africa | Long term (≥ 4 years) |

| Volatile FX controls inflate import-dependent logistics costs | -0.9% | Managed-rate economies | Medium term (2-4 years) |

| Shortage of certified cold-chain technicians for school-health programs | -0.4% | Rural healthcare zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Tender Cycles & Slow Payments to Logistics Vendors

Decentralized procurement schedules force carriers to juggle intermittent workloads and extended receivable days, driving up working capital needs. Kenyan state corporations still post compliance scores below optimal benchmarks, illustrating the persistence of manual steps that delay disbursements. Smaller regional operators struggle to finance operations over long payment horizons, limiting competition and raising service costs for ministries[4]John Muturi Waci et al., “Procurement practices and value for money in State Corporations in Kenya,” plos.org.

Chronic Road-Network Gaps Outside Main Corridors

Sparse rural road density inflates transit times and vehicle maintenance costs, especially where feeder roads to schools remain unpaved. Security incidents near isolated stretches of highway further increase risk premiums and insurance costs. Operators deploy specialized off-road fleets, but the capital intensity squeezes margins and restricts route coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Drives Modal Integration

Transportation services captured 62.80% of the Africa government and education logistics market share in 2024, reflecting entrenched reliance on road and multimodal routes that connect ministries, depots, and schools across vast territories. Within the Africa government and education logistics market size, road haulage handles the bulk of government consignments, while rail and air provide niche support for high-security or time-critical shipments. Value-added services register the fastest 12.80% CAGR through 2030 as tender documents routinely include kitting, packaging, and installation clauses. Operators expand micro-warehouse networks that combine solar power and real-time temperature monitoring to meet strict shelf-life requirements for school feeding programs. Cold-chain capabilities, in particular, underpin contracts linked to health initiatives that deliver fortified foods and medical kits to remote districts. Digital freight optimization tools integrate route planning across road and rail, ensuring balanced asset use and compliance with axle-load regulations.

Continuous investment in multimodal nodes supports a shift from pure trucking toward integrated solutions. Warehouse upgrades such as AGL Rwanda’s Kigali expansion add chilled chambers and cross-dock zones, positioning the site as a regional pivot for donor-financed education projects. Airfreight remains reserved for emergency textbooks and laboratory reagents when school calendars face disruption. Sea and inland waterways gain limited traction for bulky furniture and paper shipments, yet reliability gaps and port congestion temper wider adoption. As ministries streamline customs paperwork under AfCFTA protocols, modal diversification is expected to rise, with rail corridors absorbing heavier loads that once moved solely by road.

By End-User: Federal Governments Lead While K-12 Education Accelerates

Central and federal governments accounted for 29.50% of the Africa government and education logistics market size in 2024, sustaining large tender volumes for census kits, voting materials, and social program supplies. Their consolidated buying power supports multi-year framework agreements that anchor carrier revenue visibility. Defense agencies and state entities add steady work that often requires higher compliance levels and security vetting. Public education K-12 shows the strongest growth at 11.50% CAGR, fueled by national plans to raise enrollment and distribute digital learning tools. Device roll-outs and textbook replenishment cycles elevate shipment frequency and sharpen the need for track-and-trace capability down to the classroom level.

Higher education’s logistics spend grows at a slower pace yet features specialized requirements such as laboratory equipment imports and grant-funded research shipments. Colleges bundle volumes through central procurement offices, opening opportunities for 4PL-style orchestration across customs clearing, staging, and distribution. The “Others” category, which includes parastatals and public utilities, increasingly turns to private carriers to lower costs and meet audit standards. Shared service centers emerge within ministries, pooling purchase orders and harmonizing service-level metrics that carriers must meet to keep preferred-supplier status.

Geography Analysis

South Africa maintained the largest Africa government and education logistics market share at 23.67% in 2024, buoyed by dense transport infrastructure, automated customs systems, and stable regulatory frameworks. Carriers leverage integrated road-rail-port corridors to move curriculum materials swiftly between regional depots and township schools. Persistent inequalities in service coverage spur demand for rural last-mile innovations such as solar micro-hubs and drone trial corridors. Ongoing public-private investment, including multilateral financing for green hydrogen freight corridors, signals sustained infrastructure upgrades that will support higher volumes.

Nigeria follows as a high-potential market where population scale and large education budgets drive contract size despite congestion risk and fuel subsidy reforms. E-procurement gains shorten project cycles and improve shipment scheduling, yet FX volatility and port bottlenecks challenge cost management. Kenya capitalizes on its corridor position to handle cross-border aid cargo bound for neighboring states and integrates its Single Electronic Window with donor tracking systems. Morocco and Algeria diversify the regional picture by blending modernization drives with strict import licensing, nudging carriers to cultivate in-country partnerships for customs brokerage.

Ethiopia records the fastest 6.88% CAGR outlook as procurement reforms shift logistics tasks to private operators and as new dry ports extend the reach of sea-borne imports from Djibouti. Market entrants can secure growth by aligning with government digitalization programs that seek real-time visibility across supply chains. In the rest of Africa, Rwanda’s digital logistics credentials and Ghana’s e-commerce fulfillment parks illustrate how smaller economies advance technology adoption to overcome scale disadvantages. Overall, geographic prospects track with macroeconomic expansion, infrastructure investment, and the pace of procurement reform adoption.

Coverage of the government and education logistics market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia, North America, and Europe, alongside detailed country-level intelligence for Spain, India, Japan, United Kingdom, France, and China, each shaped by local operating conditions.

Competitive Landscape

The Africa government and education logistics market remains moderately fragmented but is consolidating as global logistics groups acquire regional specialists to unlock scale, technology depth, and contract eligibility. DHL Group, DSV, and Kuehne + Nagel deploy global networks, customs expertise, and financial strength to win multi-country framework deals. Regional champions such as Unitrans Africa and Transnet Freight Rail leverage familiarity with local regulations and corridor infrastructure to defend their share. Mid-tier players differentiate through value-added niches like solar-powered storage, secure document handling, and ECTN compliance advisory.

Strategic investments revolve around digital platforms that provide ministries with item-level shipment data and automated proof-of-delivery uploads. Providers that integrate with government e-procurement portals capture process efficiencies that translate into higher win rates. Cold-chain expansion accelerates as school feeding and health programs prioritize product integrity and temperature assurance. The African Union’s 2024 warehouse guideline update unifies operational benchmarks across member states, reducing duplication for multiregional providers while raising entry hurdles for small local firms.

Mergers and alliances shape competitive dynamics. The completed integration of Bolloré Logistics into CEVA extends multimodal coverage across 43 countries, positioning the firm for larger education and health tenders. DHL commits more than EUR 300 million (USD 312.5 million) to new SSA facilities, targeting e-commerce and perishables that overlap with school feeding contracts. DSV’s acquisition of DB Schenker expands compliance certifications and military-grade secure transport capacity, opening additional defense and education funding streams.

Africa Government And Education Logistics Industry Leaders

DHL Group

Limark Forwarding

Perseus Forwarders

Atrax Logistics

DSV A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: DHL Group announced a EUR 300 million (USD 312.5 million) multi-year investment plan to expand infrastructure and service capability across Sub-Saharan Africa, with a focus on e-commerce, perishables, energy, and healthcare.

- April 2025: DSV completed its acquisition of DB Schenker, creating an enlarged global logistics provider with expanded reach into government and education contracts.

- November 2024: CEVA Logistics finalized its acquisition of Bolloré Logistics, broadening multimodal coverage and reinforcing African contract performance.

- October 2024: Scan Global Logistics formed a dedicated government services division backed by USD 25 million and aimed at high-compliance agency contracts.

Africa Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| Nigeria |

| Morocco |

| Kenya |

| South Africa |

| Ethiopia |

| Algeria |

| Rest of Africa |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others | ||

| By Country | Nigeria | |

| Morocco | ||

| Kenya | ||

| South Africa | ||

| Ethiopia | ||

| Algeria | ||

| Rest of Africa |

Key Questions Answered in the Report

How large is the Africa government and education logistics market in 2025?

The market is valued at USD 18.9 billion in 2025.

What is the projected CAGR through 2030?

The market is expected to expand at a 6.17% CAGR to 2030.

Which service type holds the largest share?

Transportation services account for 62.80% of revenue in 2024.

Which end-user segment is growing fastest?

The public education K-12 segment shows an 11.50% CAGR through 2030.

Which country shows the highest growth potential?

Ethiopia is forecast to post a 6.88% CAGR between 2025 and 2030.

What is a key emerging logistics trend in rural areas?

Solar-powered micro-warehouses that cut spoilage and diesel costs are gaining traction.

Page last updated on: