China Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

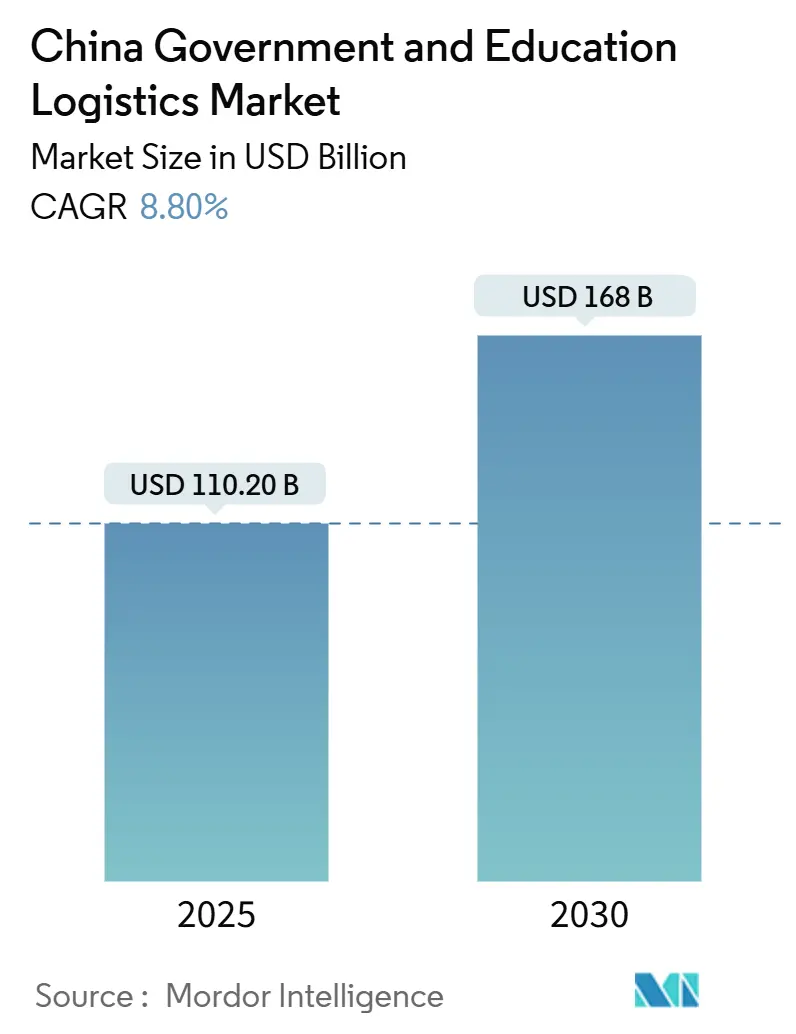

| Market Size (2025) | USD 110.20 Billion |

| Market Size (2030) | USD 168 Billion |

| Growth Rate (2025 - 2030) | 8.80% CAGR |

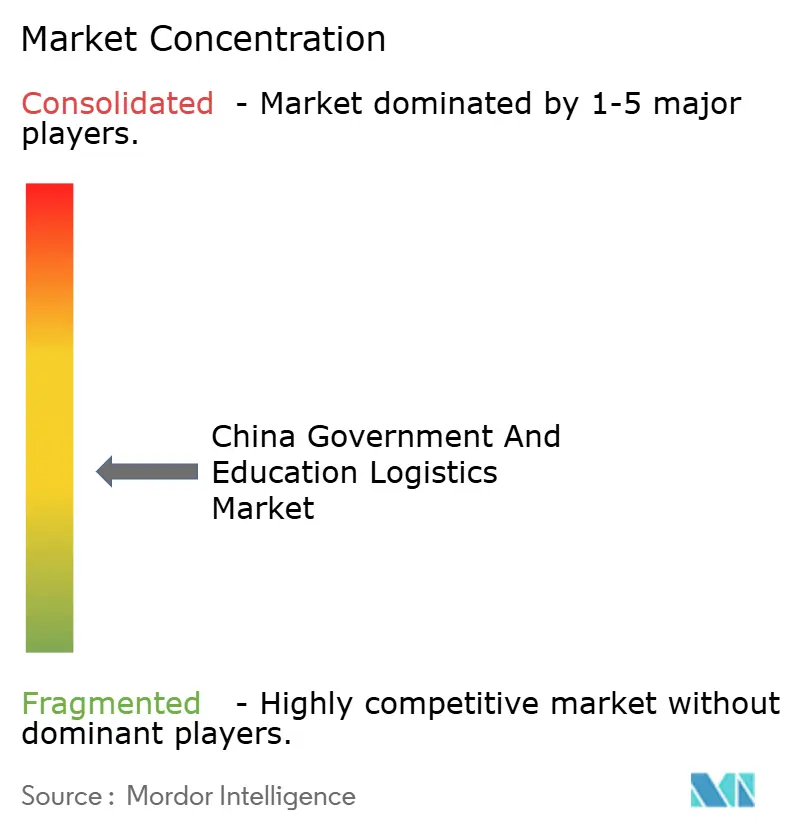

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Government And Education Logistics Market Analysis by Mordor Intelligence

The China Government And Education Logistics Market size is estimated at USD 110.20 billion in 2025, and is expected to reach USD 168 billion by 2030, at a CAGR of 8.80% during the forecast period (2025-2030).

Continuous digitalization of public procurement, large-scale smart-campus rollouts, and resilience mandates issued after the COVID-19 disruption collectively underpin this trajectory. Large third-party providers benefit from the State Council’s central purchasing rules that aggregate orders and require real-time shipment visibility, tightening the link between logistics performance and contract renewals for government agencies. Demand also rises from Ministry of Education programs that retrofit rural schools with networked devices and cold-chain assets for nutrition schemes, generating recurring opportunities for value-added services. Simultaneously, Beijing’s 2060 carbon-neutral roadmap nudges agencies toward greener fleets and multimodal routing, prompting providers to incorporate fuel-cell trucks and rail links to lower Scope 3 emissions.

Key Report Takeaways

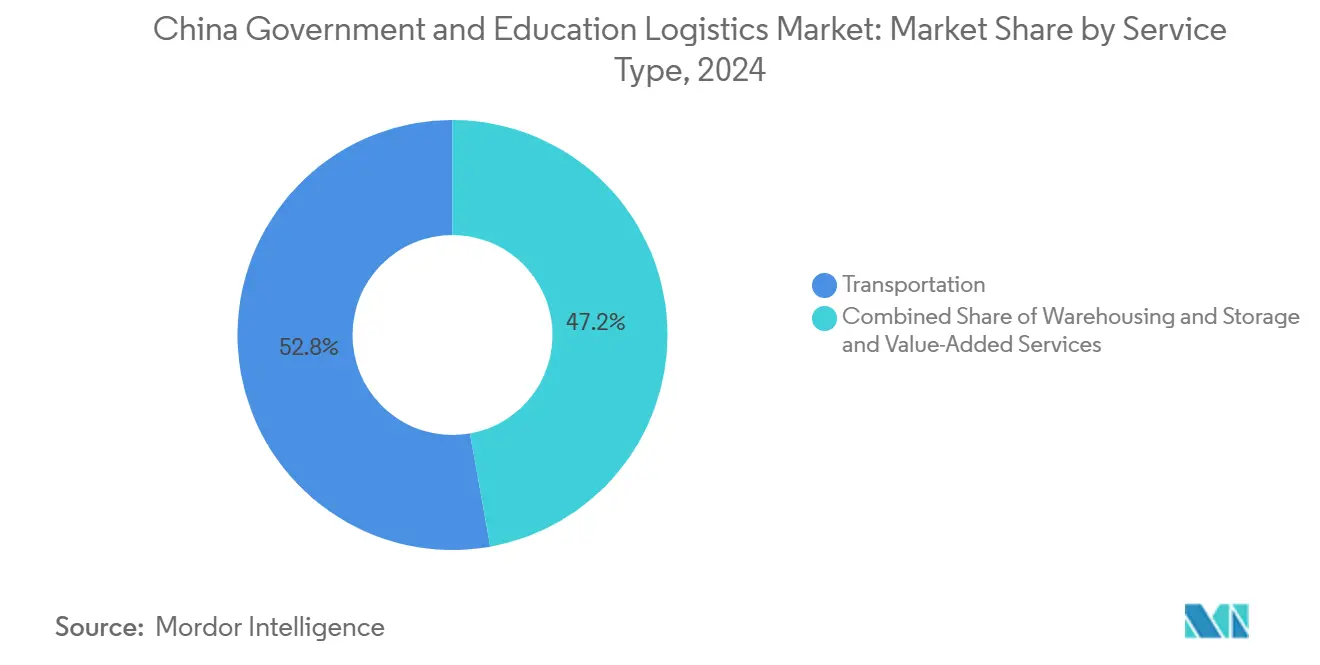

- By service type, transportation led with 52.80% of the China government and education logistics market share in 2024; value-added services are projected to expand at a 9.20% CAGR through 2030.

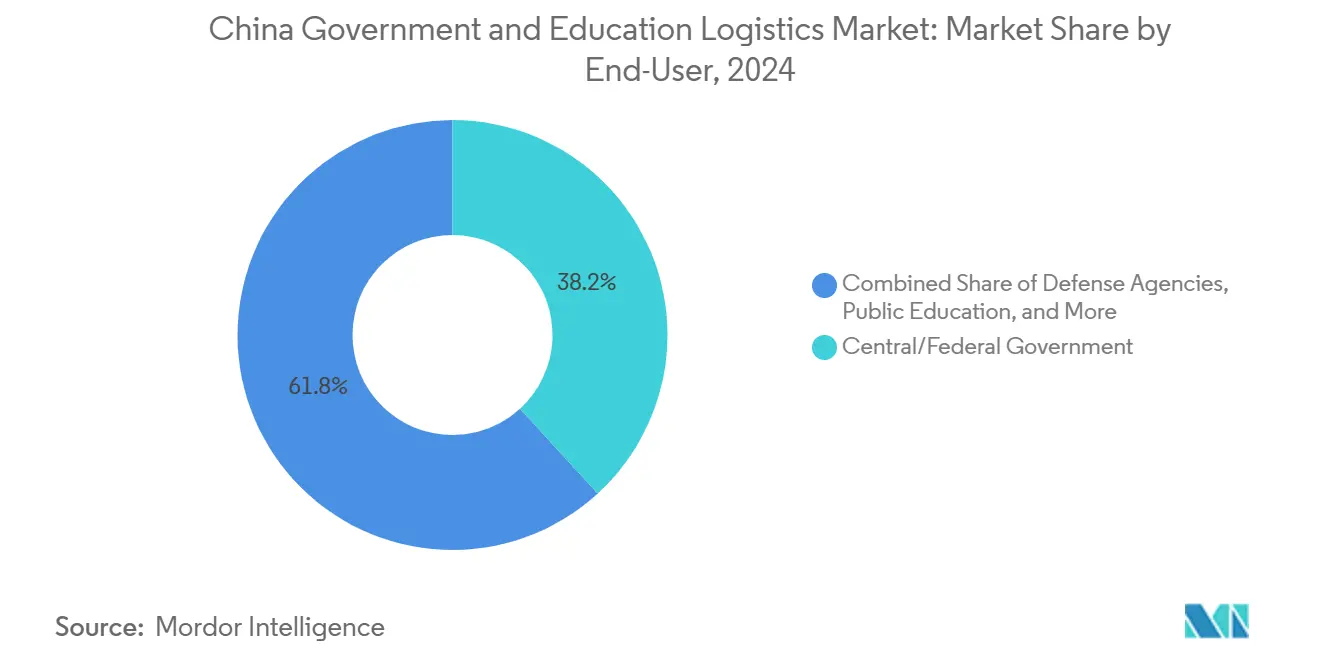

- By end-user, the Central/Federal government held 38.20% of the China government and education logistics market size in 2024, while public education (K-12) is expected to record the highest projected 9.70% CAGR to 2030.

Understanding the full system requires moving beyond China boundaries into a wider international view. Mordor Intelligence captures the global government and education logistics market scope in its worldwide coverage.

China Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first government procurement reform | +1.8% | National; early adoption in Beijing, Shanghai, Guangdong | Medium term (2-4 years) |

| Expansion of smart-campus infrastructure | +1.5% | National; Tier 1–2 cities | Long term (≥ 4 years) |

| Post-COVID public-sector resiliency mandates | +1.2% | National; remote and border regions | Short term (≤ 2 years) |

| Central-level push to outsource non-core logistics | +1.0% | National; central agencies | Medium term (2-4 years) |

| Carbon-neutral targets for public assets | +0.8% | National; metro pilots | Long term (≥ 4 years) |

| Field-deployment drill integration by defense & emergency | +0.7% | Border provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-first Government Procurement Reform

The State Council’s 2024-2026 Action Plan obliges every county-level agency to use unified e-tendering portals, consolidating shipments that were once fragmented among multiple vendors[1]State Council of China, “Government Procurement Action Plan 2024-2026,” GOV.CN. Larger shipment lots now favor providers equipped with API-integrated tracking, electronic proof-of-delivery, and automated compliance reporting. Performance-based contracts attach monetary penalties to late or damaged deliveries, shifting risk to logistics firms and forcing investment in predictive analytics for route planning. Smaller carriers lacking digital infrastructure face exit or acquisition pressure as agencies demand end-to-end visibility dashboards that interface directly with procurement systems.

Expansion of Smart-Campus Infrastructure

Over 200 universities and 7,500 K-12 schools upgraded to smart-campus standards in 2024, triggering high-frequency deliveries of IoT sensors, servers, and networking cabinets that must travel in temperature-controlled conditions. Logistics providers increasingly bundle white-glove installation, reverse logistics for obsolete hardware, and nationwide maintenance visits into multiyear contracts. The recurring nature of device refresh cycles ensures steady demand for providers that can coordinate phased rollouts during academic breaks, limiting class disruptions.

Post-COVID Public-Sector Resiliency Mandates

National Development and Reform Commission guidelines require critical public stock to cover 90 days of operations and be distributed across at least two warehousing nodes per region[2]National Development and Reform Commission, “Public Sector Supply Chain Resilience Guidelines,” NDRC.GOV.CN. Agencies now weigh network redundancy equal to cost in bid evaluations, boosting firms able to demonstrate continuity planning and emergency mobilization experience. Education bureaus particularly seek partners capable of last-mile deliveries to remote boarding schools during lockdowns or disasters, relying on distributed micro-fulfillment centers.

Central-Level Push to Outsource Non-Core Logistics

The move to outsource non-core logistics, mandated by SASAC efficiency targets, unlocks USD 10-15 billion in additional annual opportunities. Providers must pass security vetting, manage classified shipments, and deliver audit-ready spend analytics. Government buyers prefer single-vendor frameworks covering procurement planning through reverse logistics, rewarding integrators that complement freight operations with supply-chain consulting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent data-security & secrecy compliance | −1.5% | National; high-security zones | Short term (≤ 2 years) |

| Multi-year budget-cycle volatility | −1.2% | National; stronger at local level | Medium term (2-4 years) |

| Limited cold-chain infrastructure in rural schools | −0.8% | Western & northeastern rural counties | Long term (≥ 4 years) |

| Network-isolation rules blocking 3PL IT interfaces | −0.7% | National; central agencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Data-Security & Secrecy Compliance

China’s Cybersecurity Law mandates that any logistics data linked to government consumption remain on servers physically isolated from the public internet, forcing carriers to duplicate IT stacks and use manual air-gapped transfers[3]Cyberspace Administration of China, “Government Data Security Guidelines 2024,” CAC.GOV.CN. The ensuing 15-20% cost premium squeezes margins and disadvantages smaller operators, unable to fund separate facilities or meet ISO 27001 audits.

Multi-Year Budget-Cycle Volatility

Fiscal rules prompt a fourth-quarter surge when agencies rush to exhaust budgets before expiry, straining carrier capacity. Conversely, first-quarter volumes often slump, leaving fleets idle and warehouses under-utilized[4]Ministry of Finance, “Government Budget Cycle Management,” MOF.GOV.CN. The unpredictability complicates network-design investment and drives demand for flexible short-term leasing of vehicles and storage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates Multi-Modal Integration

Transportation accounted for 52.8% of the China government and education logistics market share in 2024. Within this umbrella, road freight remains indispensable for last-mile delivery to the nation’s 210,000 schools, many in mountainous or island zones unreachable by rail or air. Rail haulage handles volume moves such as textbooks and dormitory furniture across 1,500 km+ corridors at tariffs 30% below trucking, aided by the expansion of dedicated freight lines under the Belt and Road framework. Air cargo serves urgent ministry dispatches and humanitarian kits, while inland waterways move heavy machinery for campus construction along the Yangtze.

The segment advances via embedded telematics, dynamic routing, and green-fuel pilots like SF Express’s hydrogen fleet debut. Providers now package transport with IoT-based condition monitoring to comply with strict asset-tracking clauses in government contracts. This evolution feeds the uptake of value-added services, whose 9.2% CAGR to 2030 will lift their contribution to the China government and education logistics market size. Cold-chain management for student meals, secure carriage for sealed exam papers, and white-glove installation for smart-campus devices headline these offerings, carving a premium margin pocket shielded from pure-price competition.

By End-User: Public Education Drives Fastest Growth

Central and federal entities held 38.2% of the China government and education logistics market size in 2024 as ministries orchestrated nationwide procurement ranging from office consumables to defense-grade communications sets. These customers demand multilayer security clearance, fostering long-term contracts with state-linked carriers.

Public education emerges as the growth engine. K-12 projects run at a forecast 9.7% CAGR, fueled by multi-billion-dollar drives to digitize classrooms, retrofit rural boarding facilities, and enforce nationwide nutrition standards. Each policy milestone—from smart-blackboard rollouts to subsidized meal programs—creates sustained shipment waves of electronics, perishables, and teaching aids. Universities equally propel complexity: laboratory relocations, international student logistics, and research-grade cold storage intensify the call for integrated solutions.

Geography Analysis

Eastern seaboard provinces anchor demand, concentrating more than 55% of 2025 spending. Beijing’s ministerial complex requires continuous flows of sensitive documents and IT hardware, while Shanghai’s financial and educational ecosystem commands premium secure-delivery services. Pearl River Delta hubs such as Guangzhou act as nodal gateways for imported lab equipment used in national-level universities.

The Yangtze River Delta forms China’s largest education cluster, housing scores of science parks linked to universities. Logistics providers operate cross-docking centers along the Nanjing–Hangzhou–Shanghai axis, enabling 24-hour delivery windows for high-value research apparatus. Inland, Wuhan leverages its central location to serve as a staging ground connecting coastal suppliers with western schools, reducing lead times.

Western and northeastern provinces, historically underserved, now constitute the fastest-growing slices of the China government and education logistics market. Provincial stimulus programs upgrade rural campuses in Xinjiang, Tibet, and Heilongjiang, demanding multimodal strategies that blend rail trunking with off-road trucking to tackle rugged terrain. Government subsidies for depot construction in Lanzhou and Harbin invite carriers to plant cross-regional warehouses, ensuring consistent stock levels for emergency response drills led by the Ministry of Emergency Management.

Mordor Intelligence examines the government and education logistics market across diverse other regional markets as well, including Middle East, Africa, and Asia, while also offering granular country-level perspectives for India, Japan, Canada, Spain, United Kingdom, and Mexico and more.

Competitive Landscape

The market is moderately fragmented yet tightening. SF Express leverages a 90,000-vehicle fleet and AI-powered sortation to win multiyear education-sector deals, whereas Sinotrans exploits historical ties to the defense establishment for classified projects. International entrants DHL and UPS focus on niche value-added lanes, notably secure transport for foreign-funded joint research laboratories.

Technological capability forms a crucial differentiator. JD Logistics deploys autonomous ground vehicles across smart campuses during off-class hours, trimming in-campus delivery time by 40%. COSCO’s Tianjin headquarters integrates sea-rail services, giving it an edge in heavy lab-equipment moves that originate from overseas manufacturers. Partnerships proliferate: DHL’s tie-up with e-commerce platform Temu improves customs-cleared lead times for imported science kits destined for schools.

Environmental credentials grow in weighting. SF Express and local start-up Wuliu Auto unveiled 12 fuel-cell trucks in Foshan, capturing early points on green evaluation rubrics for government tenders. Newcomers without carbon strategies find themselves locked out when bids carry mandatory emission-reduction scoring. Barriers escalate further around data-segregation: only carriers with dual-stack IT conforming to CAC rules can serve central ministries, discouraging smaller private entrants and reinforcing incumbent dominance.

China Government And Education Logistics Industry Leaders

Sinotrans

COSCO Shipping Logistics

JD Logistics

Kerry Logistics Network Ltd

Deppon Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: SF Express and Shanghai Wuliu Auto commissioned 12 hydrogen fuel-cell heavy-duty trucks in Foshan for zero-emission public-sector deliveries.

- June 2025: Cosco Shipping inaugurated its North China headquarters in Tianjin to deepen sea-rail port integration and pursue public-sector logistics contracts.

- April 2025: DHL Express formed a strategic alliance with Temu to accelerate cross-border e-commerce flows, supporting government import programs.

- April 2025: DSV finalized its acquisition of DB Schenker, creating one of the world’s largest logistics groups with expanded service scope for Chinese public institutions.

China Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

What is the current value of the China government and education logistics market?

The market is valued at USD 110.2 billion in 2025.

What CAGR is forecast for this market through 2030?

An 8.8% CAGR is projected between 2025-2030.

Which service category holds the largest share?

Transportation services lead with 52.8% share.

Which end-user segment will grow fastest?

Public education K-12 is forecast to advance at a 9.7% CAGR.

What key regulation is reshaping procurement patterns?

The State Council’s digital-first Government Procurement Action Plan 2024-2026 mandates centralized e-bidding and shipment tracking.

Which driver adds the largest uplift to CAGR?

Digital-first procurement reform contributes a +1.8% boost to forecast CAGR.

Page last updated on: