Europe Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

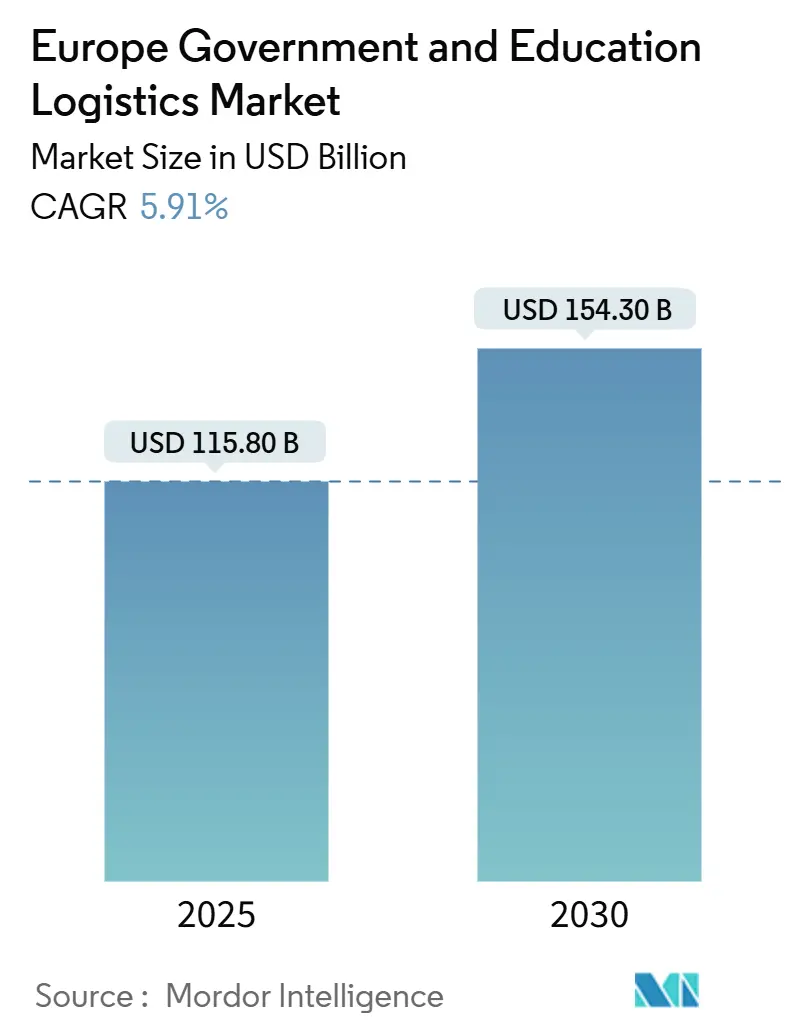

| Market Size (2025) | USD 115.80 Billion |

| Market Size (2030) | USD 154.30 Billion |

| Growth Rate (2025 - 2030) | 5.91% CAGR |

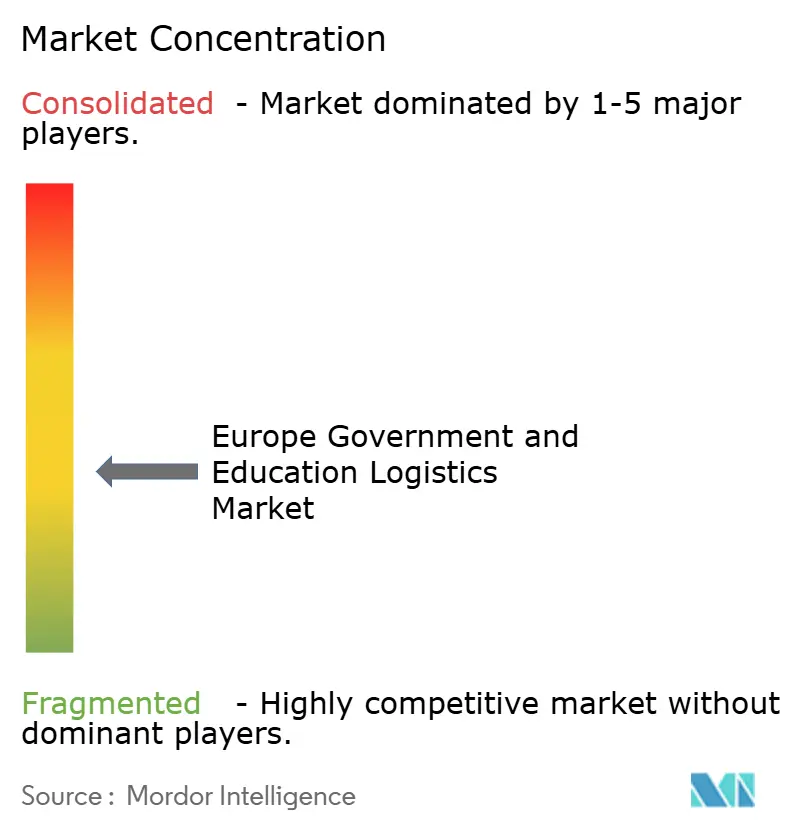

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Government And Education Logistics Market Analysis by Mordor Intelligence

The Europe Government And Education Logistics Market size is estimated at USD 115.80 billion in 2025, and is expected to reach USD 154.30 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

The steady expansion reflects the escalating digitization of public procurement workflows, the push for low-emission freight under EU Green Public Procurement rules, and a marked rise in cross-border educational mobility. Institutional customers are shifting from asset-heavy in-house fleets toward variable-cost contracts that bundle transportation with device configuration, secure packaging, and real-time chain-of-custody tracking, thereby widening the addressable opportunity for specialized providers. At the same time, defense-modernization programs are unlocking premium demand for temperature-controlled storage, classified-material handling, and ISO 27001-compliant information flows, enabling operators with security clearances to secure multi-year revenue streams.

Key Report Takeaways

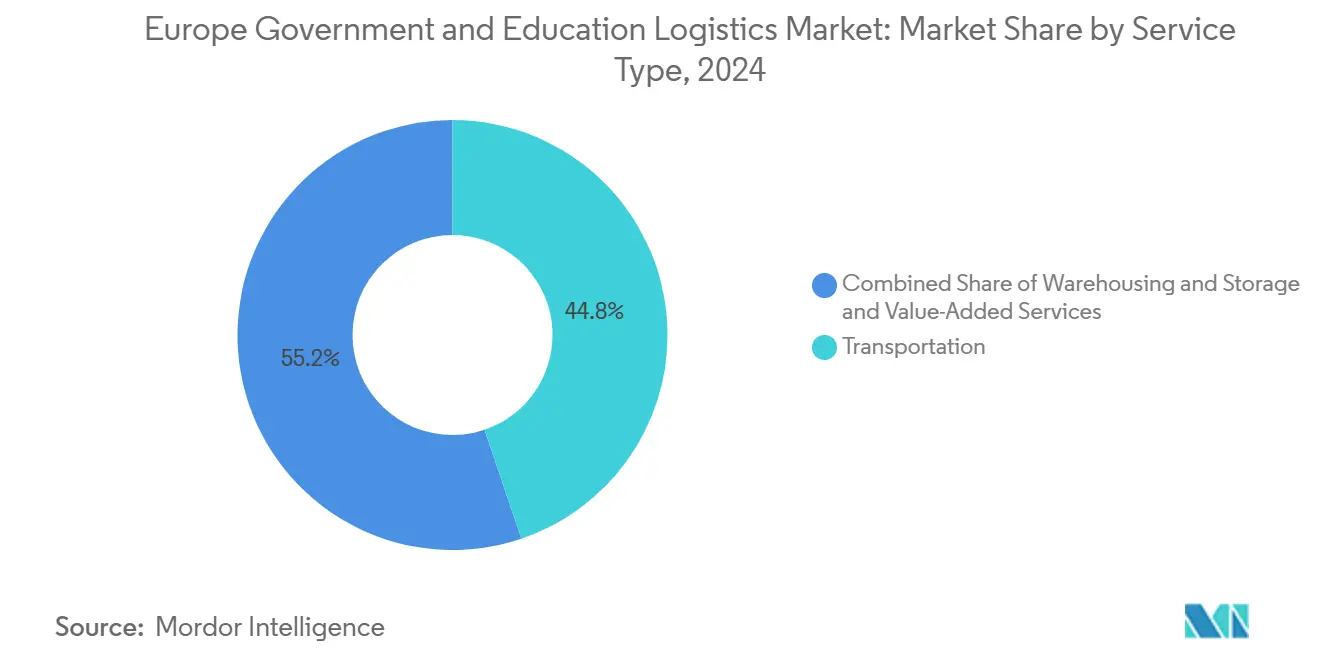

- By service type, transportation held 44.80% of Europe government and education logistics market share in 2024, while value-added services are projected to grow at a 7.80% CAGR through 2030.

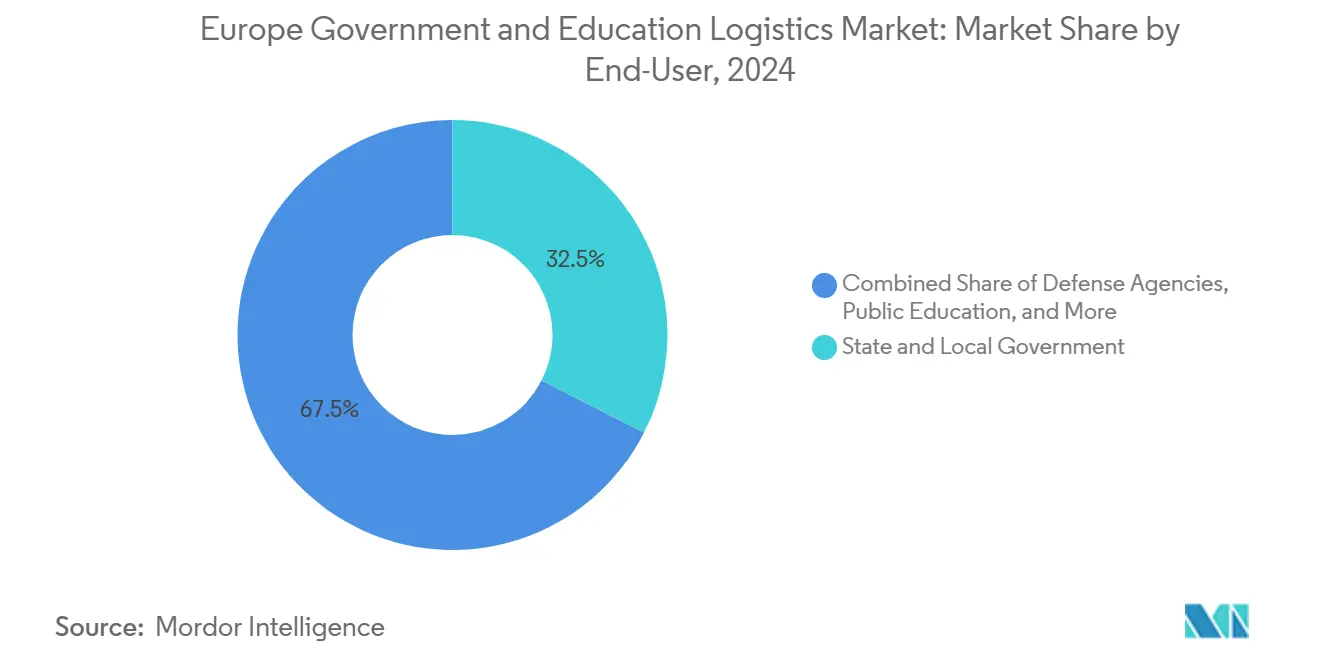

- By end-user, state & local governments accounted for 32.50% of Europe government and education logistics market size in 2024, whereas public education (K-12) is advancing at a 7.10% CAGR during 2025-2030.

- By country, Germany commanded a 16.14% share of the Europe government and education logistics market in 2024, while Italy is slated to post the fastest 7.45% CAGR up to 2030.

Competitive positioning in Europe includes both locally based firms and those operating across multiple regions. The market landscape in the global government and education logistics industry research shows how these players are arranged internationally.

Europe Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation mandates in procurement | +1.2% | EU-wide; strongest in Germany, Netherlands, Denmark | Medium term (2-4 years) |

| Outsourcing to improve cost efficiency | +0.9% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Defense-modernization programs | +0.8% | NATO states; notably Poland and the Baltic region | Long term (≥ 4 years) |

| Cross-border Erasmus & research mobility | +0.7% | Core EU and associated economies | Medium term (2-4 years) |

| EU Green Public Procurement standards | +0.6% | Nordic countries first movers; EU-wide rollout | Long term (≥ 4 years) |

| Hybrid-learning surge | +0.5% | Urban education hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Mandates in Public Procurement

Member-state adherence to the EU Once-Only Principle, enacted in 2024, compels agencies to digitize document flows, generating a need for ISO 27001-certified logistics partners capable of secure hardware roll-outs and encrypted data carriers[1]European Commission, “Digital Europe Programme,” digital-strategy.ec.europa.eu. Germany’s Digital Strategy 2025 funnels federal and Länder funding into cloud-ready data centers that demand climate-controlled last-mile delivery and on-site device commissioning. Consequently, value-added service bundles—ranging from imaging laptops to tamper-evident packaging—are outpacing basic freight in the Europe government and education logistics market. Providers able to combine secure chain-of-custody with end-point installation are carving defensible niches as ministries replace paper archives with digital repositories. Over the next 3 years, this compliance-driven spending is expected to keep average revenue per shipment on an upward trajectory despite price pressure in commoditized line-haul lanes.

Outsourcing to Improve Cost Efficiency

Budget ceilings across Southern and Eastern Europe motivate ministries to convert fixed warehouse assets into variable-priced contracts that smooth spending profiles. Spain’s education directorates, for example, shifted textbook distribution and tablet configuration to external carriers during the 2024/25 school year following national spending reviews. Outsourcing unlocks shared-fleet utilization and centralized procurement, lowering cost per delivered unit and accelerating shipment visibility gains. Crucially, public-sector tenders now weigh lifetime cost and CO₂ intensity equally, giving multi-client 3PLs a structural advantage over in-house fleets with poorer capacity fill. As competitive bids proliferate, small regional haulers struggle to finance the cybersecurity and insurance clauses embedded in newer contracts, prompting consolidation across the Europe government and education logistics industry.

Defense-Modernization Programs Needing Secure Logistics

Rising NATO expenditure—averaging 2.1% of GDP among EU members in 2024—injects fresh capital into specialized warehousing, munitions transport, and classified-material tracking[2]NATO, “Defence Expenditure of NATO Countries,” nato.int. Poland’s 2024 defense outlays reached 4.12% of GDP, requiring temperature-controlled hubs and secure convoys for Patriot missile batteries. The UK’s Defence Logistics Transformation Program likewise expands partnership scopes for private 3PLs with Category B security clearances. Premium margins on these contracts offset capital expenditures for armored vehicles, biometric access controls, and blockchain-verified custody logs, cushioning providers against volume volatility elsewhere in the Europe government and education logistics market.

Cross-Border Erasmus & Research Mobility

Erasmus+ recorded record participation in the 2024 academic cycle, lifting cross-border student flows that rely on seasonal freight of personal effects, laboratory specimens, and examination papers. Horizon Europe’s EUR 95.5 billion (USD 99.5 billion) funding window through 2027 spawns multinational consortia, each requiring time-definite transport of sensitive research equipment to dispersed labs. Logistics partners must master Carnet ATA documentation, micro-temperature monitoring, and reverse-logistics loops for reusable lab assets. Reliable transit performance improves grant compliance metrics, making on-time delivery a differentiator as universities bid for additional EU research funding. These dynamics underpin resilient volume growth in the Europe government and education logistics market throughout the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty limits on cloud platforms | −0.8% | Strictest in Germany and France | Medium term (2-4 years) |

| Public-budget austerity cycles | −0.6% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Aging customs IT in smaller states | −0.4% | Baltic and Balkan economies | Long term (≥ 4 years) |

| High insurance premiums for exam papers | −0.3% | High-stakes education markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty Limits on Cloud Logistics Platforms

The upcoming EU Data Act requires sensitive governmental supply-chain data to be processed on infrastructure located within the Union, adding compliance layers and licensing fees[3]European Parliament, “Data Act Adoption,” europarl.europa.eu. Germany’s Federal Office for Information Security further bans non-certified hyperscalers from public-sector logistics tenders. 3PLs must therefore co-locate servers or partner with sovereign clouds, inflating overheads and elongating deployment timelines. Smaller operators lacking IT budgets find market entry economically prohibitive, tempering competition yet restraining the overall digitization pace in the Europe government and education logistics market.

Public-Budget Austerity Cycles

Rising debt-service costs led several member states to cut discretionary spending in the 2024-2025 fiscal cycle, delaying non-essential tenders and compressing volumes for outsourced logistics[4]European Fiscal Board, “Fiscal Policy Coordination,” ec.europa.eu. Italy’s spending reviews, for instance, deferred IT roll-outs beyond 2026, producing shipment lulls that challenge capacity planning. Providers mitigate exposure through diversified contract portfolios, though margin swings remain an endemic feature of the Europe government and education logistics industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates Despite Value-Added Growth

Transportation generated 44.80% of Europe government and education logistics market share in 2024, underscoring its role as the backbone of intra-EU mobility initiatives. Road freight remains the workhorse due to extensive TEN-T corridors and doorstep accessibility, while rail’s modal share inches upward on the back of expanded night-freight services linking German, Dutch, and Italian hubs. Air transport keeps niche relevance for diplomatic pouches and time-critical research materials, whereas short-sea and inland waterways address bulk defense equipment and low-carbon objectives.

Value-added services are forecast to outstrip all other categories at 7.80% CAGR, reflecting heightened demand for device imaging, on-site installation, customs brokerage, and single-window compliance reporting. Warehousing & storage, representing the balance of the service mix, is transitioning toward secure micro-fulfillment nodes in city centers to meet same-day delivery service-level agreements for last-mile educational hardware.

By End-User: State Governments Lead While K-12 Education Accelerates

State & local governments contributed 32.50% to Europe government and education logistics market size in 2024, driven by decentralized administration of healthcare, mobility, and social services. These entities tender multi-year framework agreements that bundle transport, storage, and specialized packaging for IT roll-outs. Central/federal ministries, although fewer in number, generate high-margin classified shipments and international diplomatic moves demanding intricate customs coordination, thereby sustaining a premium segment for certified providers within the Europe government and education logistics market.

Public education (K-12) commands accelerating demand, expanding at a forecast 7.10% CAGR on the back of hybrid-learning programs and device-per-student mandates. Shipment volumes spike in Q2 and Q3 as schools prepare for the academic year, creating cyclical revenue waterfalls that sophisticated carriers monetize through dynamic pricing. Higher-education institutions retain a decent share, anchored by research grants and Erasmus mobility; their diversified freight profile—ranging from cold-chain reagents to high-value scientific instrumentation—necessitates multi-temperature assets and specialized insurance.

Geography Analysis

Germany led the Europe government and education logistics market in 2024 with a 16.14% revenue share, thanks to world-class Autobahns, Rhine waterway connectivity, and digital-ready 5G corridors enabling real-time cargo telemetry. Berlin’s Federal Logistics Strategy 2030 aligns with EU Green Deal imperatives, allocating subsidies for hydrogen trucking and paperless customs clearances, thereby reinforcing the country’s pole position. The robust supplier ecosystem—anchored by DHL, DB Schenker, and SAP logistics platforms—creates spillover efficiencies for smaller 3PLs riding shared capacity and collaborative IT stacks throughout the Europe government and education logistics market.

The United Kingdom sustains a notable presence despite post-Brexit customs frictions, leveraging London’s global air-cargo links and the Ministry of Defence’s sizable procurement footprint. Specialized operators in Cambridge’s research triangle support international lab collaboration, while universities in Scotland award regional contracts favoring multimodal rail-plus-ferry combinations to minimize emissions under institutional net-zero pledges. Customs complexity has lifted compliance costs, yet currency fluctuations occasionally advantage U.K. carriers in euro-denominated tenders, preserving competitive parity within the broader Europe government and education logistics market.

Italy is forecast to register the bloc’s highest 7.45% CAGR, propelled by the National Recovery and Resilience Plan for digital school infrastructure and e-government hubs. Milan-based 3PLs are scaling urban electromobility fleets ahead of municipal diesel bans, while southern regions capitalize on EU Cohesion Funds to upgrade port facilities in Bari and Palermo, shortening transit times for inbound learning-device shipments from Asia. Spain’s market trajectory parallels Italy’s, underpinned by LOMLOE reforms mandating digital competency that necessitate large-scale ICT deployments across 17 autonomous communities.

Mordor Intelligence tracks the government and education logistics market across other major regions such as Asia, North America, and Middle East, with additional country-level coverage spanning Germany, Spain, United Kingdom, France, Russia, and South Korea, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Competition is moderately fragmented, leaving ample space for mid-tier specialists. DHL Group leverages Pan-European air and road networks, ISO 27001 certifications, and a fleet of 27,000 electric vehicles to lock in multi-year frameworks with federal ministries in Germany and Scandinavia. Kuehne + Nagel exploits rail-freight corridors from Rotterdam to Milan, bundling customs brokerage and device staging to win digital-education contracts in Benelux and Northern Italy. The recent DSV acquisition of DB Schenker enlarges warehousing capacity, deepening bench strength for defense-grade logistics across NATO corridors.

Niche providers such as Global Defense Logistics concentrate on munitions and classified-document moves, cultivating scarce Category A security clearances that command 30-40% price premiums. Technology is the principal differentiator: blockchain custody ledgers, AI route optimizers, and IoT sensor grids determine tender scores as ministries elevate cyber-resilience metrics. Regulatory barriers—ranging from GDPR audits to proof of low-emission fleets—continue to deter extra-European entrants, preserving share for incumbents embedded within the Europe government and education logistics market.

Forward-looking players are piloting hydrogen fuel-cell trucks on the Rhine-Alpine corridor, aiming to pre-empt 2030 emission thresholds. Others partner with sovereign-cloud providers to launch EU-compliant data lakes enabling predictive ETA dashboards. Consolidation is likely to accelerate as capital requirements for fleet decarbonization and cybersecurity outstrip the financing capacity of small firms, nudging the Europe government and education logistics industry toward moderate concentration without tipping into oligopoly.

Europe Government And Education Logistics Industry Leaders

DHL Group

Kuehne + Nagel

DSV

CEVA Logistics

United Parcel Service, Inc. (UPS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its takeover of DB Schenker, creating a top-tier provider with enhanced reach in defense and education contract verticals.

- February 2025: Dachser broadened its AI research partnership with Fraunhofer-Gesellschaft to develop machine-learning route optimizers tailored for public-sector shipments.

- November 2024: CEVA Logistics finalized the acquisition of Bolloré Logistics to expand multimodal capability for EU infrastructure and emergency-response contracts.

- October 2024: Scan Global Logistics invested USD 25 million to launch a dedicated government services division focused on security-cleared freight and compliance consulting.

Europe Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| Germany |

| United Kingdom |

| Russia |

| Italy |

| Netherlands |

| Spain |

| Poland |

| France |

| Rest Of Europe |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others | ||

| By Country | Germany | |

| United Kingdom | ||

| Russia | ||

| Italy | ||

| Netherlands | ||

| Spain | ||

| Poland | ||

| France | ||

| Rest Of Europe |

Key Questions Answered in the Report

How large is the Europe government and education logistics market in 2025?

It is valued at USD115.8 billion and is projected to grow to USD154.3 billion by 2030 at a 5.91% CAGR.

Which service segment is growing fastest?

Value-added services, covering device configuration and secure packaging, are set to expand at a 7.80% CAGR.

Which country holds the largest market share?

Germany leads with 16.14% share, benefiting from advanced infrastructure and digital-ready procurement standards.

What drives the surge in K-12 logistics demand?

Hybrid-learning initiatives and device-per-student mandates are boosting shipments of laptops and tablets to schools throughout Europe.

How do EU Green Public Procurement rules affect logistics providers?

They require 30% emission cuts by 2030, favoring operators with electric or low-emission fleets and detailed carbon reporting.

What is the competitive outlook after recent mergers?

The DSV-DB Schenker merger raises top-tier capacity, yet moderate fragmentation persists, maintaining competitive contract tenders across the region.

Page last updated on: