Canada Data Center GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

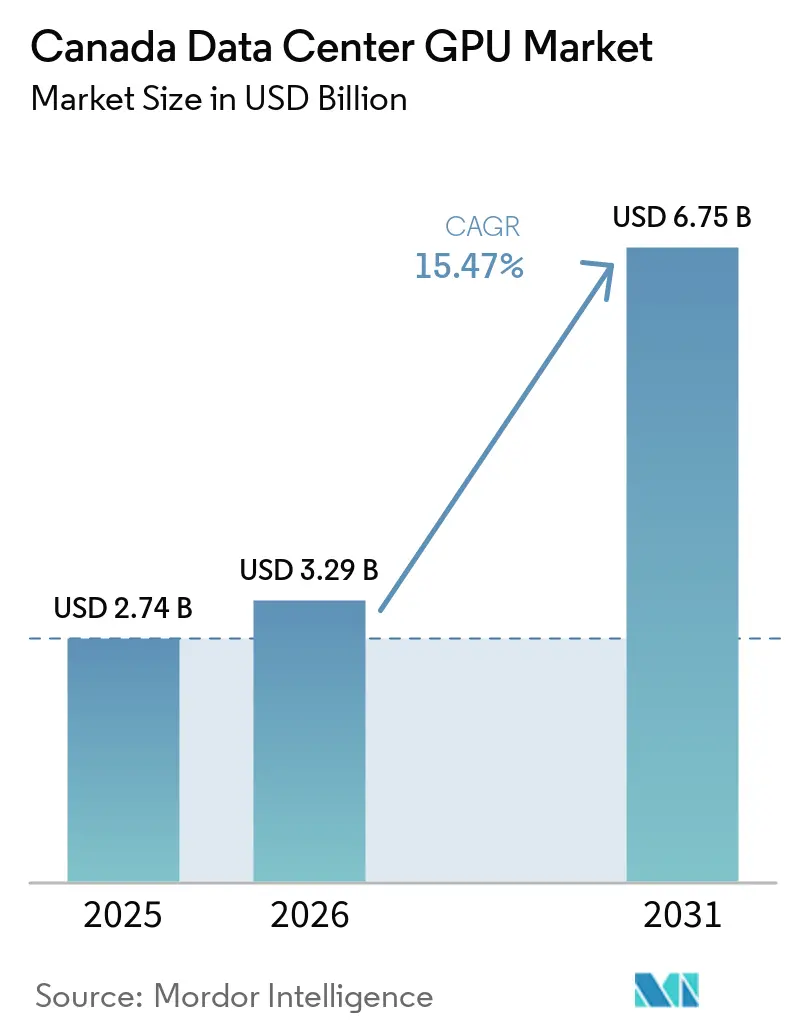

| Base Year Market Size (2025) | USD 2.74 Billion |

| Market Size (2026) | USD 3.29 Billion |

| Market Size (2031) | USD 6.75 Billion |

| Growth Rate (2026 - 2031) | 15.47% CAGR |

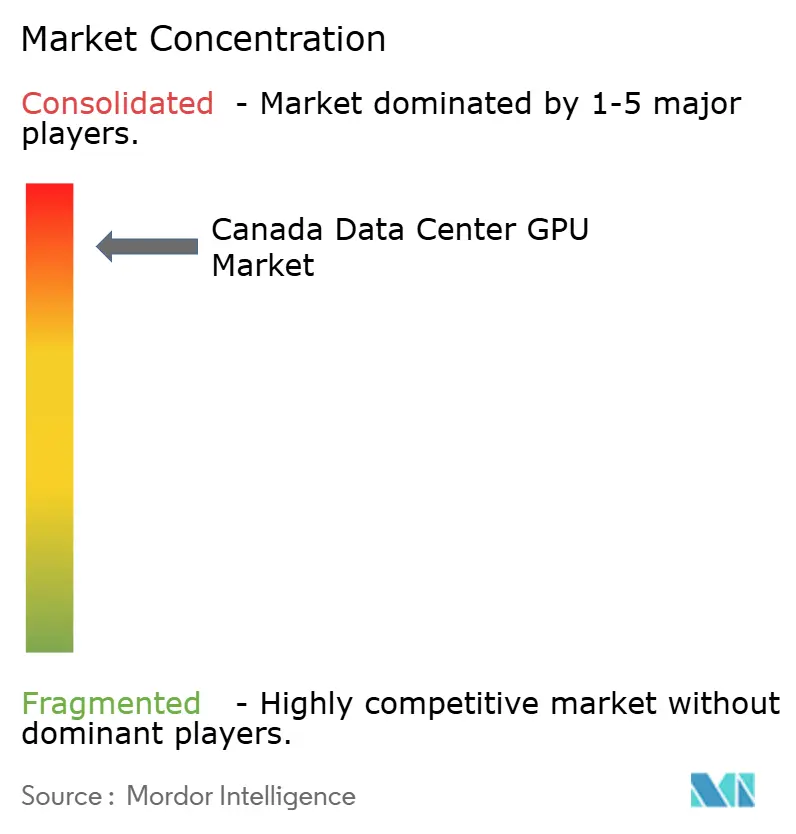

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center GPU Market Analysis by Mordor Intelligence

The Canada data center GPU market size is expected to be USD 2.74 billion in 2025, USD 3.29 billion in 2026, and reach USD 6.75 billion by 2031, growing at a CAGR of 15.47% from 2026 to 2031. Hyperscalers continue to anchor demand, yet Ottawa’s sovereign AI compute plan signals that public procurement will match private spending within five years. Enterprises are bringing inference closer to users to meet strict privacy rules, while liquid cooling and hydro-sourced power temper operating costs. Capital now chases provinces with inexpensive hydroelectricity and streamlined permitting because power prices outside those corridors erode the total cost of ownership. Meanwhile, supply-chain risks around advanced GPUs remain unresolved, creating delivery windows that can stretch to 9 months.

Key Report Takeaways

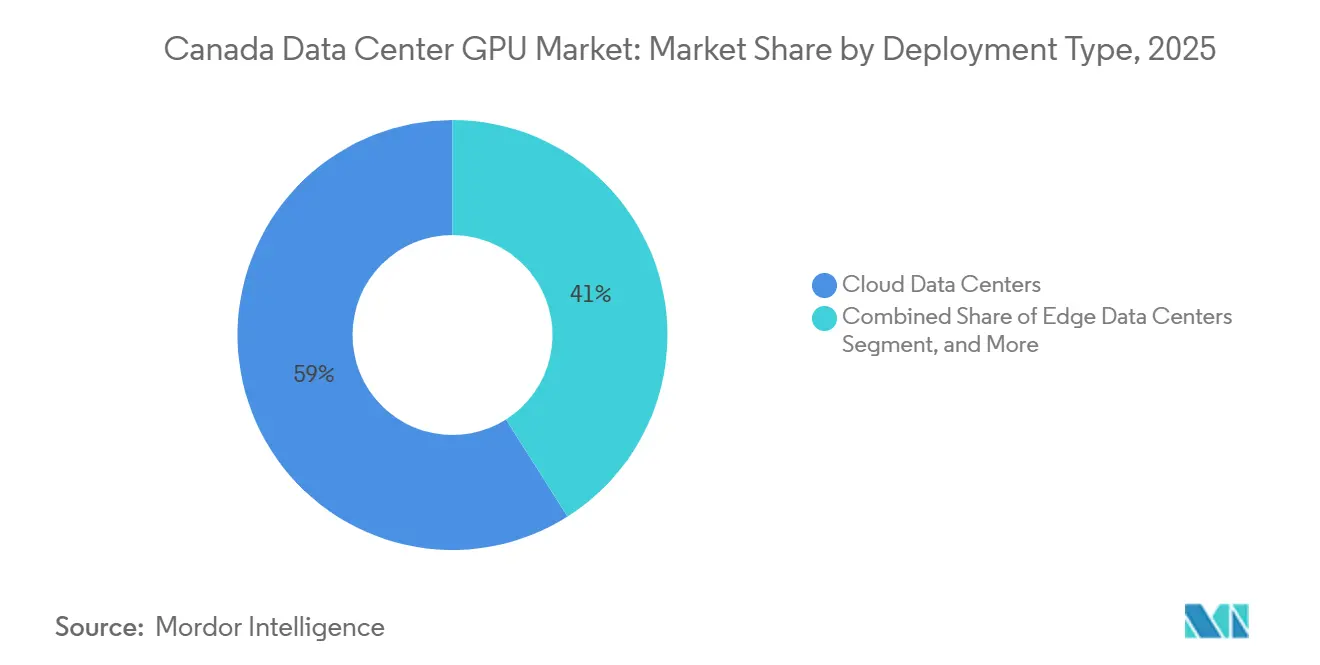

- By deployment type, cloud facilities accounted for 58.99% of revenue in 2025. Edge data centers are forecast to expand at a 16.82% CAGR through 2031, the fastest among deployment models.

- By GPU type, Inference GPUs accounted for 54.89% of the Canada data center GPU market share in 2025 and are projected to grow at 16.55% CAGR over 2026-2031.

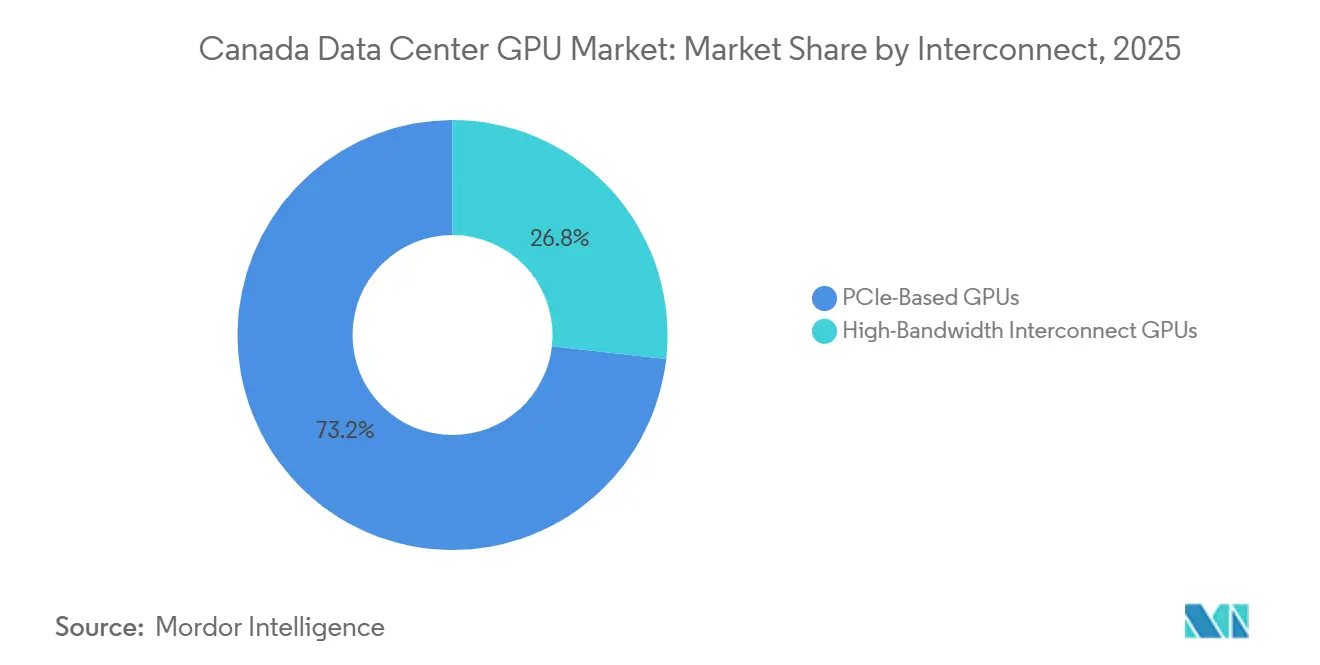

- By interconnect, high-bandwidth GPUs are expected to grow at a 16.33% CAGR, outpacing PCIe-based cards during the forecast period.

- By workload type, data analytics workloads are projected to post a 17.11% CAGR, the quickest among application categories.

- By end user, government and research institutions are set to grow at a 17.31% CAGR, the highest among end users.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Growth of AI Workloads in Canadian Cloud Regions | +4.2% | National, led by Québec, Ontario, British Columbia | Short term (≤ 2 years) |

| Expansion of Hyperscaler Data Centers in Québec and Ontario | +3.8% | Québec and Ontario, spillover to British Columbia | Medium term (2–4 years) |

| Federal Investments in High-Performance Computing Infrastructure | +2.9% | National, early focus on Alliance host sites | Medium term (2–4 years) |

| Data Residency Regulations Driving In-Country GPU Deployments | +2.1% | National, strongest in regulated sectors | Long term (≥ 4 years) |

| Rising Adoption of Immersion Cooling for High-Density GPU Racks | +1.3% | Québec, British Columbia, Saskatchewan | Medium term (2–4 years) |

| Emergence of Indigenous Language AI Models Requiring Local Training | +0.8% | Northern territories and academic hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of AI Workloads in Canadian Cloud Regions

Hyperscalers continue routing generative AI traffic to domestic regions to comply with privacy laws and reduce latency for North American users. Microsoft directed USD 7.5 billion toward its Azure Canada Central and Canada East expansions, with a large portion earmarked for GPU capacity that powers OpenAI, Cognitive Services, and managed ML tools.[1]Microsoft Corp., “Microsoft Announces $19 Billion Investment in Canadian Cloud Infrastructure,” microsoft.com Amazon’s Calgary region, launched in late 2023, delivers Bedrock and SageMaker, enabling enterprises to fine-tune models without cross-border transfers.[2] Amazon Web Services, “AWS Canada West Region Launch,” amazon.com Domestic carriers also add capacity, with TELUS installing 500 Hopper GPUs in Rimouski, Québec, to build a sovereign inference hub. Enterprises that once accepted U.S. hosting now demand in-country compute as insurance against geopolitical or legal risk, turning regional cloud zones into critical growth nodes for the Canada data center GPU market.

Expansion of Hyperscaler Data Centers in Québec and Ontario

Vast hydro power, dense fiber, and incentives keep Québec and Ontario at the center of new builds. Bell is constructing a 300 MW Saskatchewan complex, spending about USD 1.25 billion and lining up CoreWeave and Cerebras as anchor tenants.[3]BCE Inc., “Bell AI Fabric Saskatchewan AI Data Centre,” bce.ca Six additional hydro-backed sites in British Columbia will boost Bell’s national capacity to 500 MW, while HIVE Digital Technologies and BUZZ HPC deploy fresh GPU clusters into Québec installations. Projects coalesce in provinces where electricity still costs under USD 0.10 per kWh, deepening a two-tier Canada data center GPU market that sidelines Alberta and the Maritimes.

Federal Investments in High-Performance Computing Infrastructure

Ottawa’s USD 2 billion Sovereign AI Compute Strategy allocates funds across private, public, and access programs, matching levels typically seen only in the United States or the European Union.[4]Innovation, Science and Economic Development Canada, “Sovereign AI Compute Strategy,” ic.gc.ca In parallel, the Digital Research Alliance injected roughly USD 190 million into five national host sites, doubling or tripling academic GPU capacity. Simon Fraser University’s Fir system debuted in 2025, ranking inside the global top 100 and supporting more than 17,000 users.[5]Simon Fraser University, “Fir Supercomputer Online,” sfu.ca Such public purchases validate supply chains and cultivate talent that later migrates to commercial operators, reinforcing the growth path for the Canada data center GPU market.

Data Residency Regulations Driving In-Country GPU Deployments

Québec’s Law 25 and federal PIPEDA rules restrict personal-data exports, while the U.S. CLOUD Act heightens legal exposure when data sits in U.S. jurisdictions. As a response, Bell AI Fabric markets full provincial sovereignty, Oracle Cloud promotes GPUs in Montreal and Toronto that stay under Canadian law, and regulated enterprises re-architect workflows to avoid foreign processors. The regulatory premium is now smaller than potential fines or reputational loss, making domestic capacity the default for many workloads and directly boosting the Canada data center GPU market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited Domestic Semiconductor Supply Chain Capacity | -1.9% | Nationwide, hits delivery schedules | Long term (≥ 4 years) |

| High Electricity Costs Outside Hydro-Powered Provinces | -2.3% | Alberta, Saskatchewan, Maritimes, parts of Ontario | Medium term (2–4 years) |

| Talent Shortage In Advanced GPU Cluster Management | -1.1% | Major metro labor pools | Medium term (2–4 years) |

| Environmental Permitting Delays For New Mega-Data Centers | -1.6% | Provinces lacking streamlined rules | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Semiconductor Supply Chain Capacity

Canada relies entirely on imports for advanced GPUs because no local fabs or advanced packaging plants exist. NVIDIA, AMD, and Intel source wafers from Taiwan and the United States, while Tenstorrent tapes out at TSMC, leaving domestic buyers exposed to global logistics and shifting export controls. Lead times for Blackwell GPUs now range from 6 to 9 months, and OEMs urge customers to place orders multiple quarters in advance. Without a CHIPS-style incentive scheme, the Canada data center GPU market faces persistent scheduling risk and pricing volatility.

High Electricity Costs Outside Hydro-Powered Provinces

Energy tariffs diverge sharply across the country. Hydro-Québec proposed USD 0.13 per kWh for new centers, still cheaper than Alberta’s residential rate of USD 0.258 per kWh and Ontario’s peak-time-of-use rates above USD 0.20. A 100 MW facility in Alberta could pay USD 141.9 million more each year in power than a counterpart on legacy Québec rates. The Alberta grid also slapped a 1,200 MW cap on fresh data-center hookups, shrinking near-term headroom and slowing the Canada data center GPU market, where gas-fired electricity dominates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Growth Outpaces Core Expansion

Edge sites generated the quickest growth because carriers embed inference at 5G aggregation points. In 2025, cloud facilities captured 58.99% of revenue, yet the Canada data center GPU market for edge deployments is projected to grow at a 16.82% CAGR through 2031. Carriers such as Bell and TELUS deploy liquid-cooled racks near population centers to achieve sub-10-millisecond latency, crucial for autonomous vehicles and real-time analytics. The approach reduces backhaul traffic and meets privacy mandates. As provincial hydro assets remain concentrated in British Columbia and Québec, future edge nodes will likely cluster in those same corridors, cementing their role as growth engines of the Canadian data center GPU market.

Large enterprises still run private rooms for proprietary training jobs that handle sensitive medical or financial data. Although this slice is smaller than public cloud, its workloads are sticky and justify an on-premise investment. Meanwhile, mega-scale cloud zones expand in parallel to sustain long-run training clusters. Together, these three footprints create a hybrid topology where data gravity, latency, and compliance jointly dictate GPU placement rather than price alone.

By GPU Type: Inference Cards Capture Production Demand

Inference units have already delivered 54.89% of revenue in 2025, reflecting the shift from experimentation to live AI services. That share widens as transformer models move into customer-facing applications, boosting the Canada data center GPU market share for inference hardware. Training boards remain vital for foundation runs, yet the utilization mix tilts strongly toward serving tokens. NVIDIA’s Blackwell silicon lifts throughput for both phases, but operators still right-size clusters by mixing inference-optimized cards with smaller pools of training silicon.

Domestic providers such as Tenstorrent and Groq target this inference tier because customers value cost per request over the depth of CUDA software. Bell’s Kamloops edge site runs Groq LPUs to bypass GPU bottlenecks in conversational AI. These alternatives may erode NVIDIA’s share at the network edge, though the core cloud remains CUDA-centric for now.

By Interconnect: High-Bandwidth Fabrics Remove Scale Bottlenecks

PCIe models accounted for 73.22% of revenue in 2025, anchoring mainstream inference and small training tasks. Yet scale-out clusters need NVLink 5, NVSwitch, or InfiniBand to keep hundreds of GPUs synchronized. The Canada data center GPU market size for high-bandwidth interconnect boards is forecast to expand at 16.33% CAGR as foundation model sizes double nearly every year. Rack-level systems such as NVIDIA’s NVL72 expose 130 TB/s of NVLink bandwidth to slash gradient lag during 100-billion-parameter training.

Hyperscalers have also standardized on RoCEv2 over 400 GbE and are moving toward co-packaged optics to curb power draw. Canadian operators mirror this trend because electricity savings offset higher acquisition costs. Vendors that bundle liquid cooling with fast fabrics, including Dell and Supermicro, now win most large tenders in the Canada data center GPU market.

By Workload Type: Analytics Leads Growth Curve

AI training and inference still accounted for 64.33% of 2025 revenue, yet GPU-accelerated analytics is growing fastest at a 17.11% CAGR. Enterprises speed up SQL queries on terabyte datasets by offloading scans to GPUs, trimming runtime from minutes to seconds. IBM’s watsonx.data prototype cut Nestlé query time by 80%, illustrating payback potential. Graphics rendering, VDI, and digital twins add steady incremental demand as dispersed workforces need remote design tools.

Scientific computing remains a constant, driven by climate research and drug discovery. However, analytics growth broadens the customer base beyond AI labs, embedding GPUs deep inside finance, retail, and logistics workflows. This diffusion underpins a more diversified Canada data center GPU market.

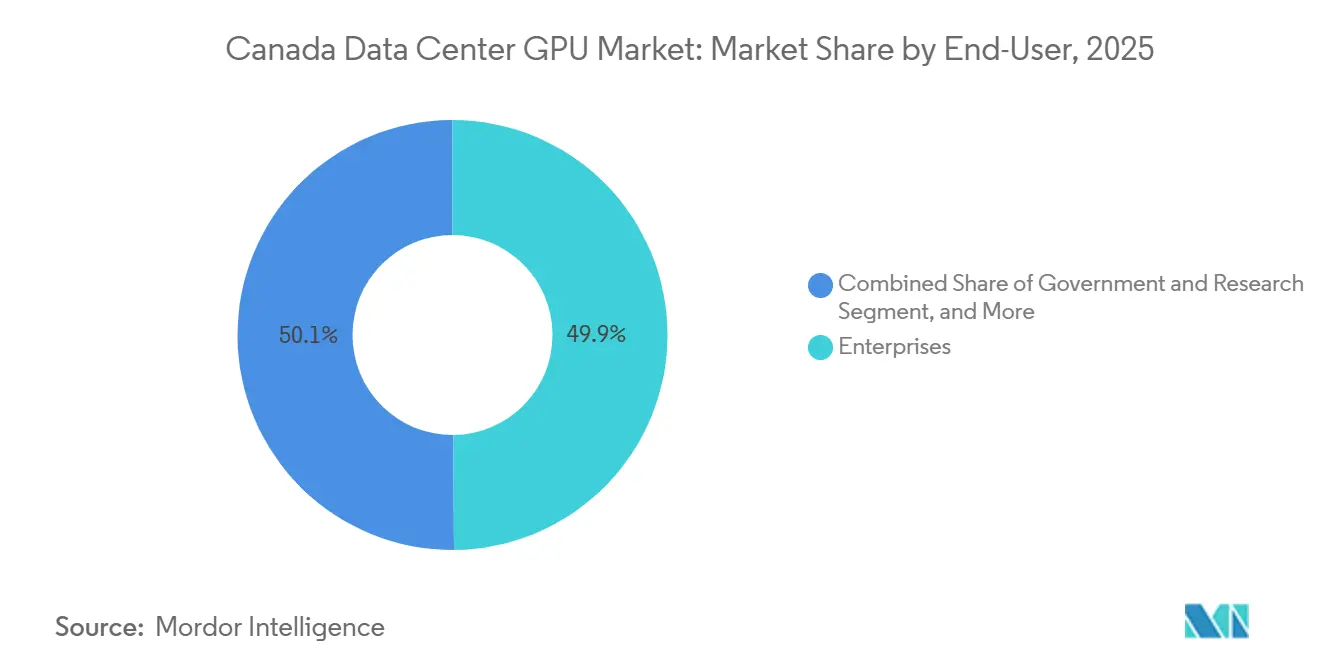

By End-User: Public Sector Emerges as Fastest-Growing Buyer

Enterprises still formed 49.88% of revenue in 2025, but government and academic users will log the strongest 17.31% CAGR through 2031. The Digital Research Alliance upgrade doubled capacity at five host universities, and Ottawa earmarked USD 1 billion for public supercomputers plus USD 300 million for access programs. Such commitments guarantee base-load demand, carrying a weight similar to that of hyperscaler orders.

Regulated sectors also shift workloads into sovereign clouds, generating overlap between public and private demand. As a result, system integrators bundle compliance features, Key Management Services, and chain-of-custody tools, embedding them as standard elements in Canada data center GPU market offerings.

Geography Analysis

Québec and Ontario host the majority of current capacity because hydroelectric rates remain below USD 0.10 per kWh, enabling operators to control operating expense even as rack densities climb. Montréal and Québec City campuses already aggregate more than 500 MW of installed power, and proposed builds would push the provincial total above 1 GW by 2028. Ontario’s Niagara corridor leverages legacy hydro stations, yet new Bill 40 approval hurdles introduce timing risks that cloud providers now weigh carefully.

British Columbia benefits from similarly cheap hydro and cool ambient temperatures that favor liquid cooling. Bell’s twin Kamloops sites and Merritt build plan to draw 26 MW each for training operations and export waste heat to adjacent university buildings. The province’s supportive municipal zoning accelerates approvals, providing an alternate growth corridor should eastern grids tighten.

Prairie provinces and the Maritimes face an uphill battle with their cost structures. Alberta’s spot-price volatility and a 1,200 MW connection cap slow large-scale GPU adoption. Saskatchewan’s new 300 MW project is viable only because tenants are locked in long-term energy contracts and will reuse heat for greenhouse agriculture. Unless additional hydro or nuclear options emerge, most incremental Canada data center GPU market investment will continue to cluster in hydro-rich regions.

Competitive Landscape

NVIDIA remains the dominant vendor, shipping roughly four out of every five GPUs that enter Canadian racks. The company's Blackwell launch further locks in CUDA, although inference rivals carve out edge niches. AMD’s MI450 and MI355X offer competitive throughput, but limited software maturity slows adoption. Domestic hopeful Tenstorrent raised USD 693 million and positioned its Wormhole chip for cost-sensitive inference tasks, yet production volumes trail far behind NVIDIA's. Groq supplies linear-processing units that Bell already uses for ultra-low-latency chat-bot serving, showing that specialty silicon can coexist with GPUs when latency trumps versatility.

System integrators compete on rack-level efficiency. Dell shipped 504 liquid-cooled XE9680L GPUs to BUZZ HPC, citing 73% energy savings over prior A100 racks, while HPE and Lenovo court hyperscalers with pre-configured NVL72 pods. Cooling vendors such as CoolIT Systems, headquartered in Calgary, supply direct-to-chip loops that allow 100 kW racks without hot-aisle containment, becoming enablers rather than afterthoughts.

Colocation and cloud players race to secure power permits. Microsoft’s USD 19 billion program spans three provinces, and Bell’s 300 MW Saskatchewan build will be the largest AI-dedicated campus in the country. CoreWeave, IBM Cloud, and Oracle Cloud each localize services to satisfy data-residency rules. Together, these moves form a moderately concentrated Canada data center GPU market.

Canada Data Center GPU Industry Leaders

Graphcore Limited

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Tenstorrent Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bell Canada broke ground on a 300 MW AI center near Regina, with CoreWeave and Cerebras as anchor tenants and first-phase completion targeted for H1 2027.

- March 2026: IBM and NVIDIA expanded collaboration, bringing Blackwell Ultra GPUs to IBM Cloud in Q2 2026 and integrating IBM Sovereign Core for regulated workloads.

- March 2026: Alberta Utilities Commission rejected Synapse Data Centre’s 1.4 GW proposal, while the AESO maintained its 1,200 MW cap on new data-center interconnections.

- February 2026: NVIDIA confirmed Blackwell shipments reached 9 GW by fiscal Q4 2026 and named Canada among its top sovereign customers.

Canada Data Center GPU Market Report Scope

The Canada Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and Graphics and Visualization), and End-User (Hyperscalers/CSPs, Enterprises, and Government and Research). The Market Forecasts are Provided in Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions |

Key Questions Answered in the Report

How large is the Canada data center GPU market in terms of value today?

The Canada data center GPU market is projected to reach USD 3.29 billion in 2026 and USD 6.75 billion by 2031.

What is the expected growth rate for Canadian edge data centers that host GPUs?

Edge facilities are forecast to expand at a 16.82% CAGR during 2026-2031 as carriers embed low-latency inference in 5G and content-delivery nodes.

Which GPU type holds the largest revenue share in Canada?

Inference GPUs commanded 54.89% of 2025 revenue and are expected to keep growing faster than training GPUs across the forecast window.

Why are Québec and British Columbia emerging as preferred locations for GPU clusters?

Both provinces supply inexpensive hydroelectric power and have streamlined permitting, allowing operators to manage operating expenses while meeting sustainability goals.

How will public-sector spending influence GPU demand in Canada?

Ottawa's USD 2 billion Sovereign AI Compute Strategy and the Digital Research Alliance's upgrades are driving the fastest 17.31% CAGR among government and research users, indicating that public purchases will rival those of hyperscalers.

Page last updated on: