Middle East Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

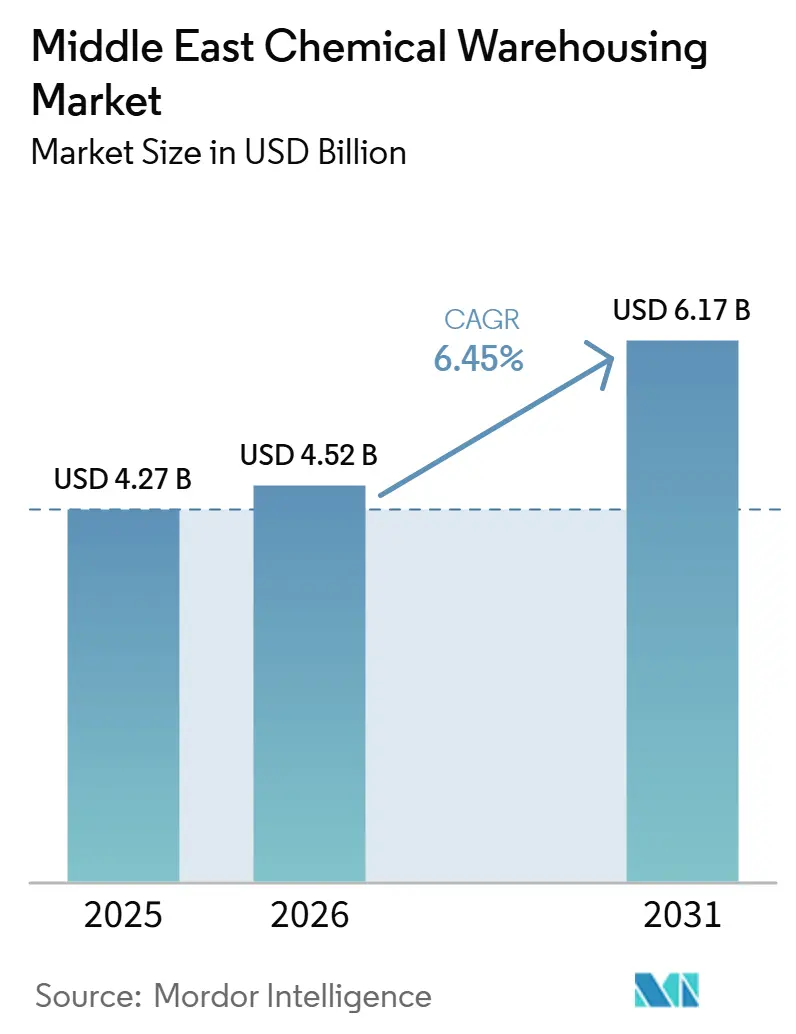

| Base Year Market Size (2025) | USD 4.27 Billion |

| Market Size (2026) | USD 4.52 Billion |

| Market Size (2031) | USD 6.17 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

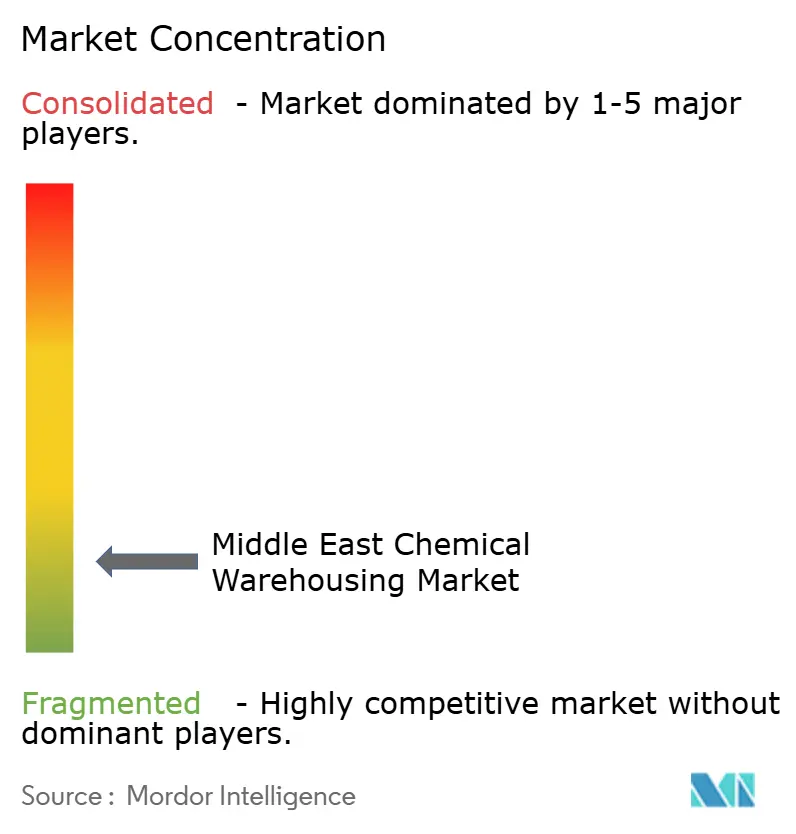

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Chemical Warehousing Market Analysis by Mordor Intelligence

The Middle East Chemical Warehousing Market size is expected to increase from USD 4.27 billion in 2025 to USD 4.52 billion in 2026 and reach USD 6.17 billion by 2031, growing at a CAGR of 6.45% over 2026-2031.

Purpose built inventory hubs continue to scale near petrochemical production clusters, as downstream integration increases the need for compliant storage of flammable, corrosive, toxic, and temperature sensitive materials. The Middle East chemical warehousing market benefits from new crackers and polymer capacity that is aligning warehousing footprints with feedstock and export nodes. Operators are also prioritizing upgrades that support hazardous materials controls and cold chain stability to meet customer audits in pharmaceuticals and high value intermediates. Exposure to shipping disruptions and climate extremes remains a planning factor, but expansion programs by national energy companies and free zones keep the Middle East chemical warehousing market on a steady multi year growth path. Fleet optimization and digital execution at new ports and logistics precincts are improving turnaround times and safety, which supports higher service levels across the Middle East chemical warehousing market.

Key Report Takeaways

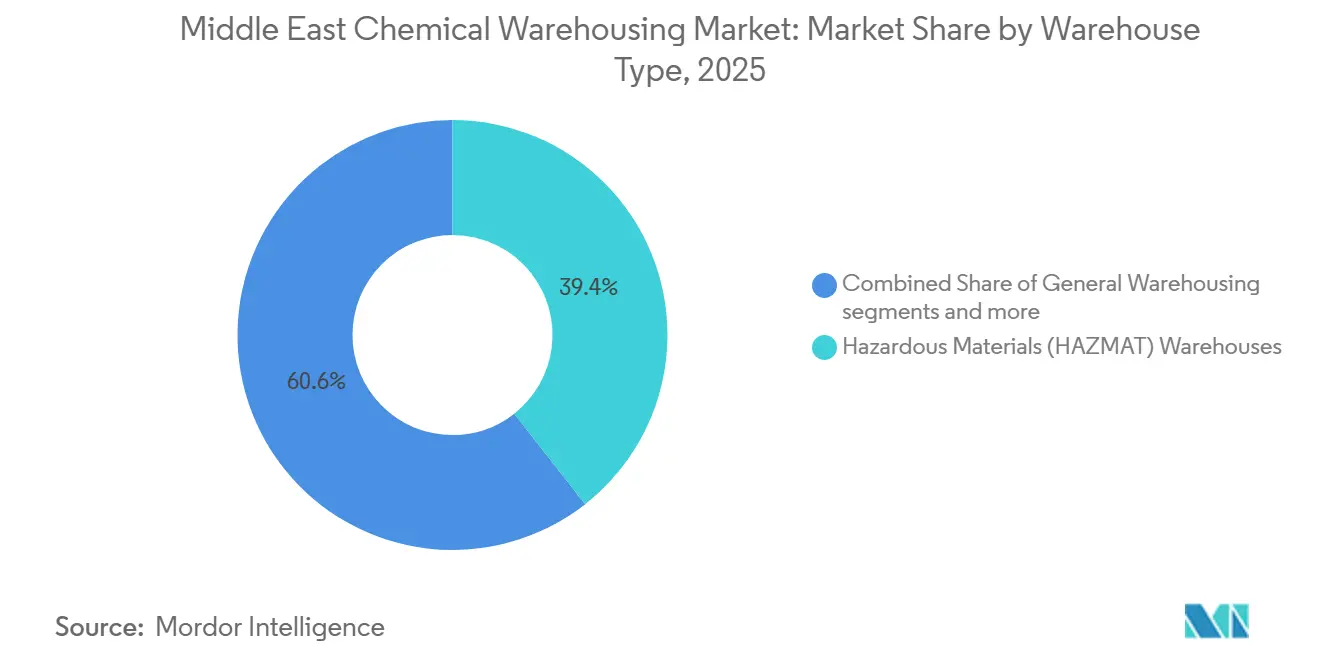

- By warehouse type, hazardous materials facilities led with 39.41% of the Middle East chemical warehousing market share in 2025; temperature-controlled warehouses are forecast to expand at a 7.14% CAGR through 2031.

- By chemical type, flammable liquids accounted for 47.61% in the Middle East chemical warehousing market size in 2025; toxic substances are projected to grow at a 6.87% CAGR through 2031.

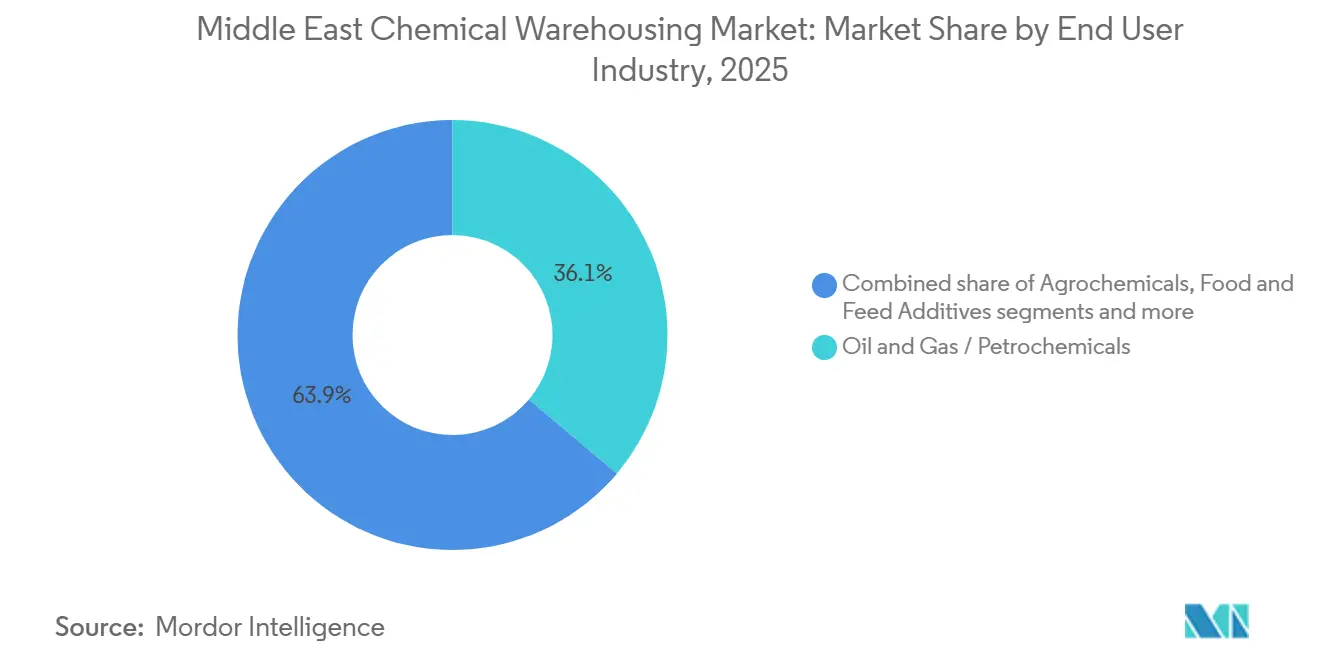

- By end user industry, oil and gas and petrochemicals represented 36.14% in 2025; pharmaceuticals and life sciences are forecast to expand at a 7.26% CAGR through 2031.

- By geography, Saudi Arabia held the largest share in 2025; Oman is identified as the fastest-growing geography through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Future direction is shaped by developments occurring across multiple regions, with Middle east contributing to the overall trajectory. The outlook on worldwide chemical warehousing market reflects how these are expected to evolve collectively.

Middle East Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical Industry Leadership | + 2.1% | Saudi Arabia, UAE core, spillover to Qatar, Oman | Medium term (2-4 years) |

| Free Zone and Economic City Development | + 1.3% | UAE (KEZAD, JAFZA), Saudi Arabia (NEOM Oxagon), Qatar Free Zones | Short term (≤ 2 years) |

| Downstream Chemical Integration | + 1.6% | Saudi Arabia, UAE, and rising Oman nodes | Medium term (2-4 years) |

| Vision 2030 Economic Diversification | + 0.9% | Saudi Arabia is primarily aligned with the UAE, Oman, and Qatar alignment | Long term (≥ 4 years) |

| Strategic Geographic Position | + 0.8% | Global trade lanes via GCC ports | Long term (≥ 4 years) |

| Oil and Gas Production Chemical Demand | + 1.4% | Saudi Arabia, UAE, Qatar, Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Petrochemical Industry Leadership Drives Specialized Storage Demand

Large integrated complexes commissioning across the Gulf are translating into sustained throughput of feedstocks and polymers, which lifts demand for compliant bulk and packaged chemical storage. In Saudi Arabia, new mixed feed cracking and downstream units under joint ventures are scheduled to bring high volume ethylene and polyethylene capacity online, which adds steady flows of flammable liquids and finished resins that need hazardous and segregated warehousing near port and rail links. In Qatar, the Ras Laffan petrochemicals project will supply ethylene and polyethylene volumes to export markets, which creates a requirement for tankage, containerized resin storage, and handling areas that meet hazardous classification standards. The Middle East chemical warehousing market is responding with higher fire suppression densities, vapor control, and road rail interface upgrades to handle two way flows between plants and ports. Third party storage providers are also adding bonded zones and packaging lines to support resin bagging and drumming that align with export documentation and global customer specs. These actions ensure the Middle East chemical warehousing market stays synchronized with the region’s core petrochemical investment cycle.

Free Zone and Economic City Development Accelerates Infrastructure Build Out

Purpose-built logistics precincts are compressing project timelines for new storage capacity by providing ready utilities, simplified licensing, and direct access to berth and yard space. In Saudi Arabia, Oxagon at NEOM is building a unified supply chain platform that combines forwarding, warehousing, and fulfillment with automated handling and digital visibility, which reduces interface friction for chemical cargo flows. The Port of NEOM’s T1 terminal, targeted for 2026, will introduce automated cranes and temperature-controlled storage areas, creating an anchor node for high-value and sensitive shipments that need stable conditions and fast gate moves. In Qatar, the free zones authority has expanded its logistics ecosystem by onboarding global freight integrators to Ras Bufontas, which raises the available options for chemical handlers seeking cross-border reach and reliable belly capacity for time-sensitive consignments.[1] Qatar Free Zones Authority, “All News,” QFZ, qfz.gov.qa These initiatives encourage the co-location of blending, repacking, and testing capabilities inside free zones, which is a favorable setup for the Middle East chemical warehousing market.

Downstream Chemical Integration Creates Captive Warehousing Demand

As national energy companies move deeper into chemicals, captive logistics contracts are consolidating with specialized operators that can meet industrial service benchmarks at scale. In the UAE, a long-term logistics agreement covers port operations, container handling, and feeder services for a large polymer producer, aligning marine moves and yard flows with planned production curves and seasonal demand. In Saudi Arabia, new petrochemical complexes are building out unit trains of polyethylene and other derivatives, which requires nearby HAZMAT-compliant storage, resin bagging facilities, and quality inspection areas to keep shipments aligned with end-market specs. These tie-ups reduce handoffs between plant, storage, and terminal, cutting dwell time and incident risk in the Middle East chemical warehousing market. Co-located warehouses are also integrating tank farms with warehouse management systems, which supports near real time reconciliation for bulk and packaged inventory. This integrated approach anchors steady utilization rates for the Middle East chemical warehousing market across cycles.

Vision 2030 Economic Diversification Underpins Long Term Policy Support

Industrial diversification agendas continue to favor downstream chemicals, advanced materials, and life sciences, which broadens the customer mix that relies on compliant storage and handling. Port and industrial city programs are aligning physical infrastructure with digitized workflows to manage safety-critical cargo with traceability and auditable controls. In Oman, large-scale energy investments and storage terminals in Duqm have created a new node for refining, petrochemicals, and future low-carbon molecules, which is drawing incremental warehouse projects next to tank farms and marine berths. These steps reduce execution risk for private logistics investors by providing policy stability and access to expanding customer bases in chemicals and adjacent sectors. The Middle East chemical warehousing market, therefore, benefits from government-backed industrial clusters that co-locate utilities, security, and customs support. This foundation is an enabling factor for safety upgrades and automation across the Middle East chemical warehousing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme Climate Conditions | - 1.2% | Saudi Arabia, UAE, Qatar, Kuwait, with summer peaks | Short term (≤ 2 years) |

| Water Scarcity and Desalination Dependency | - 0.7% | GCC‑wide, high exposure in small coastal states | Medium term (2-4 years) |

| Expatriate Labor Dependency and Nationalization Policies | - 0.9% | Saudi Arabia, UAE, and Oman alignment | Medium term (2-4 years) |

| Port Congestion and Infrastructure Bottlenecks | - 1.1% | UAE, Oman, spillover to nearby corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extreme Climate Conditions Compromise Storage Integrity and Escalate Cooling Costs

Compound heat and dryness events intensified across the region in 2025, with anomalies above historical baselines and concurrent precipitation deficits that stressed cooling systems and power grids.[2]NASA GMAO, “2025 Compound Weather Extremes in the Middle East,” NASA, gmao.gsfc.nasa.gov For warehouse operators, persistent heat increases vapor pressure risks for flammable liquids and accelerates corrosion in storage vessels, which raises inspection frequency and maintenance scope. Temperature-controlled rooms for pharmaceutical intermediates and specialty agrochemicals must hold tight bands, which lift energy draw and require redundancy planning for peak months. Risk controls now place greater emphasis on insulation, vapor management, and active monitoring for gas detection across HAZMAT zones. Geopolitical events that disrupt fuel and power supply compound climate stress, as seen with the March 2026 incident in Oman that reduced terminal operations and rerouted cargo. These dynamics increase the operating baseline for safety critical storage and push the Middle East chemical warehousing market to invest in resilient cooling and protection systems.

Water Scarcity and Desalination Dependency Inflate Industrial Operating Costs

Regional dryness and limited freshwater reserves heighten dependence on reliable industrial water for fire suppression, tank cleaning, and cooling tower operation. During seasonal heatwaves, fire safety water reserves face higher readiness demands, which influence pump sizing, reservoir planning, and periodic testing in HAZMAT facilities. Operators are evaluating closed-loop cleaning options and water-efficient processes to control utility spend without compromising safety and compliance. In zones where grid resilience and water conveyance are constrained, contingency planning now includes on-site storage, vendor backup, and response protocols to keep safety systems online. These measures add upfront and recurring costs but strengthen readiness in the Middle East chemical warehousing market. Climate-linked precipitation deficits underscore the need for coordinated utility planning around industrial clusters that handle hazardous cargo.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: HAZMAT Facilities Lead, Temperature Controlled Sees Fastest Adoption

Hazardous materials facilities commanded 39.41% in 2025, supported by safety requirements for flammables, corrosives, oxidizers, and toxic substances that define the region’s product mix. Within this category, the Middle East chemical warehousing market size for temperature-controlled facilities is projected to expand at a 7.14% CAGR between 2026 and 2031 as life sciences and specialty inputs scale in the region. New container terminals are incorporating large temperature-controlled zones, electric equipment, and shore power, which supports the handling of sensitive cargo with lower emissions. Third-party logistics providers are adding bonded cold rooms and qualification protocols to meet audit trails for pharmaceutical intermediates and high-purity chemicals. HAZMAT sites continue to invest in foam-based fire suppression, gas detection, and segregated containment to maintain compliance against ignition and exposure risks. These upgrades reinforce premium service tiers in the Middle East chemical warehousing market and reduce incident probability in high-hazard zones.

General chemical warehouses serve bulk non-hazardous chemicals, packaging inputs, and lower-risk formulations, while specialty chemical facilities cater to coatings, adhesives, and electronic-grade solvents with contamination controls and traceability. Operators pursuing temperature-controlled business are expanding mapping, validation, and alarm management to sustain narrow bands across zones. For multinational producers that cluster near ports and free zones, integrated HAZMAT campuses with cold rooms, resin bagging, and quality labs improve flow from plant to export channels. This integrated setup aligns with new production in Saudi Arabia and Qatar, where ethylene and polyethylene output will move through compliant storage nodes before export. The hazardous materials segment will remain the anchor of the Middle East chemical warehousing market as product portfolios diversify into higher value, safety-critical intermediates.

By Chemical Type: Flammable Liquids Dominate, Toxic Substances Grow Fastest

Flammable liquids accounted for 47.61% in 2025, reflecting steady movement of ethane, naphtha, methanol, and LPG through refining and cracker systems. Large Saudi complexes under construction will add feedstock and derivative volumes that require vapor recovery, explosion-proof systems, and compliant loading bays at nearby terminals. Toxic substances are projected to grow at a 6.87% CAGR from 2026 to 2031, driven by higher-value intermediates that need strict segregation and exposure control. Warehouse specifications are evolving with dedicated ventilation, continuous monitoring, and secondary containment for these high-hazard inventories. As production footprints expand, the Middle East chemical warehousing market is extending tank and packaged storage capacity along road and marine corridors to balance inbound and outbound flows. These adaptations strengthen the service mix that producers need as they pivot into higher margin portfolios.

Cross-category storage plans must avoid cross-contamination and reaction hazards, which increases the emphasis on zoning, labeling, and training. The Middle East chemical warehousing market is also adding resilience measures, including redundant power supply and emergency response coordination, to manage incidents that can escalate with toxic substances. Polymer projects in Qatar will feed resin flows that require bagging, containerization, and clean handling areas before export. Flammable cargo benefits from robust pipeline and berth infrastructure, while toxic cargo commands premium warehousing due to liability and skill intensity. These differences underpin pricing power and investment priorities across chemical type categories in the Middle East chemical warehousing market.

By End User Industry: Oil & Gas Anchors Demand, Pharma & Life Sciences Surge

Oil, gas, and petrochemicals represented 36.14% in 2025 as national energy companies drive sustained chemical output and trade. Pharmaceuticals and life sciences are projected to grow at a 7.26% CAGR through 2031 as R&D, clinical logistics, and biologics inputs scale, which pushes temperature-controlled and cGMP-aligned storage requirements. Free zones in Qatar have added leading global partners and project pipelines that support expansion in life sciences, which adds cold chain and compliance workstreams to warehousing scopes. In parallel, nitrogen fertilizers and ammonia supply under integrated ownership models support steady agrochemical and industrial shipments that rely on HAZMAT storage near marine berths. These dynamics diversify demand across end users and strengthen utilization rates in the Middle East chemical warehousing market.

Basic and specialty chemical customers need contamination-free spaces with robust batch traceability and audit-ready documentation. Pharmaceutical clients require GDP-aligned handling, calibrated sensors, and alarm management across zones to sustain controlled temperatures and humidity. As warehouse campuses co-locate next to cracker and polymer units, shared utilities and digital twins are reducing downtime and improving asset turns. For operators, alignment with producer schedules and terminal slots reduces dwell and shrinkage while improving service reliability. The Middle East chemical warehousing industry is adding training and certification paths to lift workforce readiness for toxic and temperature-controlled cargo. These efforts keep service levels high and incident rates low across end-user verticals in the Middle East chemical warehousing market.

Geography Analysis

Saudi Arabia held 58.74% of the Middle East chemical warehousing market share in 2025, anchored by large integrated complexes and growing downstream capacity that require proximate HAZMAT and resin storage. Two coastal industrial cities continue to concentrate feedstock processing, polymerization, and export operations that translate into stable storage demand for bulk and packaged chemicals. New mixed feed cracking and advanced polymer units are expanding throughput and lifting requirements for vapor controls, foam systems, and rail-ready yards adjacent to port gates. The United Arab Emirates leverages integrated energy and logistics assets to support polymer flows and chemical handling, including a long term logistics partnership that covers port operations, container handling, and feeder services for a major resin producer.[3]ADNOC Logistics & Services, “Borouge Partnership,” ADNOC L&S, adnocls.ae These programs reinforce the Middle East chemical warehousing market by linking production schedules to marine capacity and compliant yard space.

Qatar’s project pipeline adds ethylene and polyethylene volumes that drive packaging, stacking, and export handling needs at coastal hubs. Oman is the fastest-growing geography, with energy and storage investments at Duqm that create new hydrocarbon and low-carbon flows alongside large tank farms and refinery operations. The country’s coastal positioning and emerging storage terminals are attracting projects that extend into green ammonia and hydrogen logistics, which will require cryogenic or refrigerated storage and specialized safety systems over time. Kuwait and Bahrain maintain specialized roles that link refinery output and feeder flows to regional distribution networks. Egypt’s Suez Canal Economic Zone is also advancing petrochemical ambitions that will rely on export-linked warehousing within bonded areas.

Operational risks heightened during 2026 with diversions and congestion in Gulf corridors that affected containerized and bulk sequences, which raised the importance of port pair diversification and buffer capacity in nearby hubs. Events in Oman earlier in 2026 underscored the value of redundancy for power and storage as operators managed disruptions and re-routed cargo through alternate terminals. These episodes encouraged shippers and 3PLs to strengthen contingency plans with multi-port options and pre-positioned inventory in compliant sites to avoid service breaks. In Saudi Arabia, new automated terminal features and temperature-controlled storage at emerging nodes are expected to support higher reliability as volumes scale. The Middle East chemical warehousing market continues to mature as industrial cities, free zones, and ports invest in digital systems and safety upgrades that help cushion volatility.

Analysis of the chemical warehousing market by Mordor Intelligence spans multiple other regional evaluations across North America, Europe, and Africa, supported by country-level insights for Germany, Canada, France, United Kingdom, Italy, and South Korea, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The competitive field blends national energy company affiliates, specialist third party logistics providers, and port operators that manage tankage, resin handling, and packaged chemicals. Integrated producers and their logistics arms are executing long term agreements that synchronize plant outputs with port moves and feeder capacity, which anchors steady utilization for compliant warehouse space. In new industrial cities, automated terminals and cold chain features are entering service to support dangerous goods and temperature controlled cargo, which raises the service bar for regional competitors. This environment is encouraging private operators to invest in foam based suppression, vapor control, and monitoring systems that meet evolving safety codes for HAZMAT storage.

Strategic moves in Qatar and Saudi Arabia show how large polymer and derivative projects translate into port adjacent warehousing footprints and drummed liquid capacity. Joint ventures in Saudi Arabia are adding mixed feed cracking and downstream units that require integrated tank farms and warehouse blocks for resin bagging and storage before export. In Oman, the expansion of refinery and storage capacity in Duqm is opening space for logistics firms to co locate HAZMAT warehouses and liquid terminals under shared safety and security envelopes. These moves position the Middle East chemical warehousing market to capture more value from integrated production and trade flows.

Global freight integrators securing footprints in regional free zones indicate rising expectations for service reliability and regulatory alignment. Partnerships with national platforms in Saudi Arabia and anchor tenants in Qatar’s free zones point to a broader logistics ecosystem that supports chemicals, polymers, and life sciences cargo with bonded handling and screening options. Across the Middle East chemical warehousing market, leading operators differentiate with safety performance, automation readiness, and the ability to manage both bulk and packaged dangerous goods under unified digital control. As volumes scale, customers favor providers that can maintain audit readiness, integrate with port operating systems, and assure continuity through climate and geopolitical shocks. This trajectory supports ongoing consolidation around high capability nodes and long term operating contracts in the Middle East chemical warehousing market.

Middle East Chemical Warehousing Industry Leaders

RSA TALKE

Tristar Group

Gulf Warehousing Company (GWC)

Rinchem Company

Aramex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Port operations in Oman were disrupted after a drone strike hit fuel storage, causing temporary suspensions and rerouting.

- December 2025: WuXi Biologics signed a memorandum of understanding with Qatar Free Zones to advance biologics manufacturing and R&D.

- June 2025: A long term logistics partnership was signed covering port operations, container handling, and feeder services for a leading polymer producer in the UAE.

Middle East Chemical Warehousing Market Report Scope

The Middle East Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, and Others), by End-user Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints, Coatings & Adhesives, Food & Feed Additives, Oil & Gas / Petrochemicals, and Others), and by Geography (Saudi Arabia, United Arab Emirates, Qatar, Oman, Kuwait, Bahrain, and Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| Rest of Middle East |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the projected size and growth of the Middle East chemical warehousing market by 2031?

The Middle East chemical warehousing market size is forecast to reach USD 6.17 billion by 2031, registering a 6.45% CAGR over 2026 2031.

Which warehouse type is expected to expand the fastest by 2031?

Temperature controlled facilities are projected to record a 7.14% CAGR through 2031 as life sciences and specialty inputs grow.

Which chemical categories are shaping storage design and safety in the region?

Flammable liquids lead volumes, while toxic substances grow fastest, driving investments in vapor control, containment, and monitoring systems.

Which end user groups are driving the most storage demand today?

Oil and gas and petrochemicals lead 2025 demand at 36.14%, while pharmaceuticals and life sciences show the fastest growth at 7.26% CAGR.

How are new port and free zone investments influencing warehouse operations?

Automated terminals, bonded zones, and integrated supply chain platforms are improving handling times and traceability, lifting service levels across nodes in Saudi Arabia, the UAE, Oman, and Qatar.

What operational risks are top of mind for operators in 2026?

Climate extremes and periodic shipping disruptions are key concerns, driving resilience investments in cooling, fire suppression, and multi port contingency planning.

Page last updated on: