UAE Testing Inspection And Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

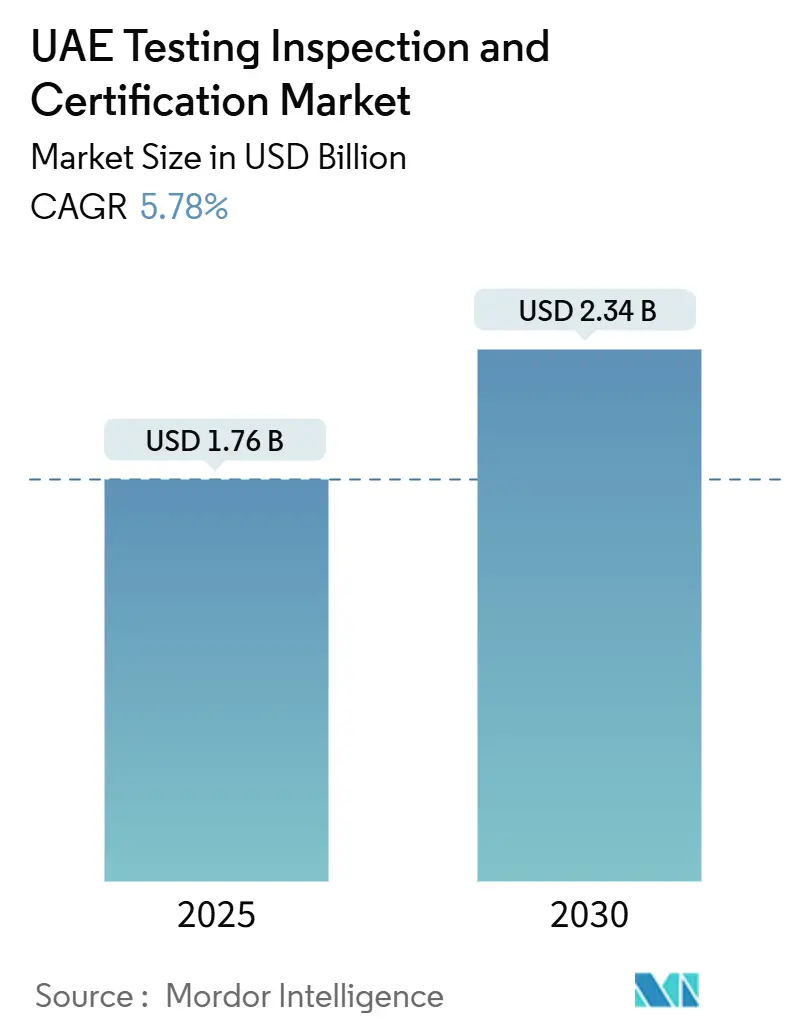

| Market Size (2025) | USD 1.76 Billion |

| Market Size (2030) | USD 2.34 Billion |

| Growth Rate (2025 - 2030) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Testing Inspection And Certification Market Analysis by Mordor Intelligence

The UAE testing, inspection, and certification market size stood at USD 1.76 billion in 2025 and is forecast to reach USD 2.34 billion by 2030, translating into a steady 5.78% CAGR over the period. The robust trajectory is underpinned by tightening federal conformity regimes, the government’s industrial-diversification drive, and accelerating digitalization initiatives that demand new test protocols and cyber-assurance programs. Surging merchandise trade total exports hit USD 570.25 billion, while imports reached USD 470.54 billion in 2023, creating a constant flow of consignments that must clear Emirates Conformity Assessment Scheme (ECAS) checks, keeping laboratory utilization rates elevated. The UAE Vision 2030 blueprint calls for expanded hydrogen, pharmaceutical, and advanced-manufacturing capacity, each of which depends on accredited laboratories and inspection bodies to secure permits and project financing.[1]UAE Ministry of Energy and Infrastructure, “National Hydrogen Strategy,” moei.gov.ae Multinational corporations gravitate toward local testing, inspection, and certification providers to shorten turnaround times, reinforcing the country’s role as a regional hub while boosting margins for outsourced specialists.

Key Report Takeaways

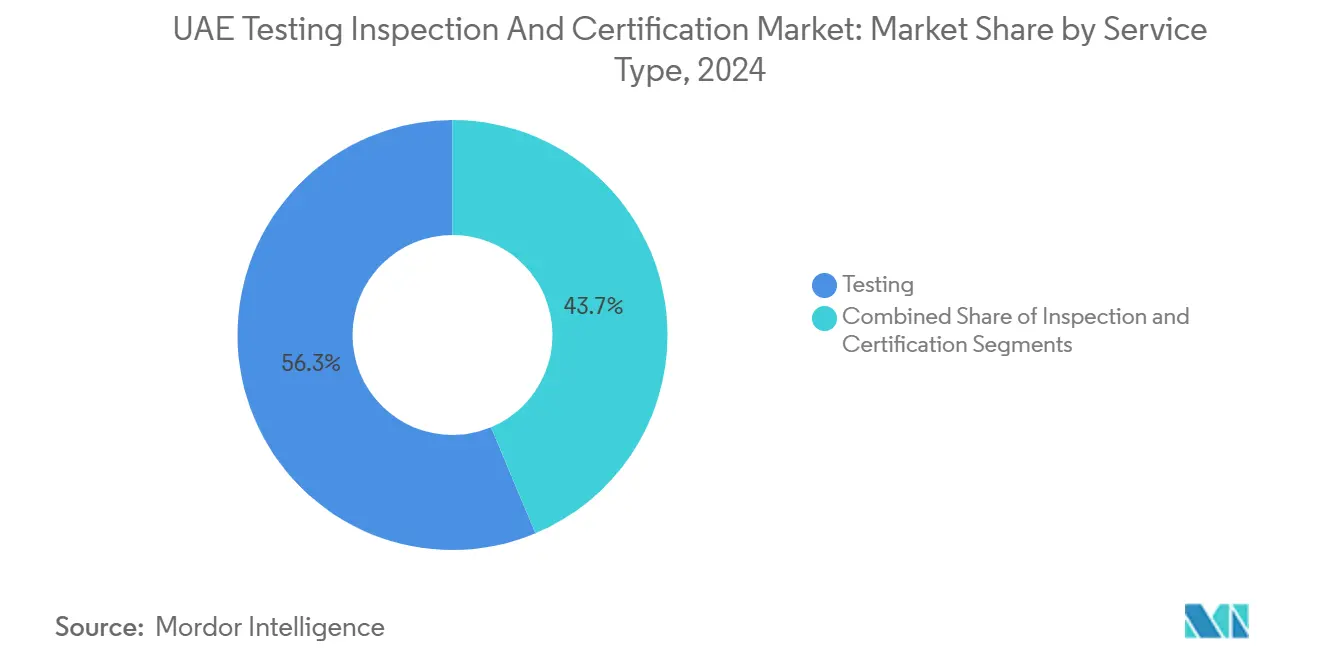

- By service type, testing captured 56.3% of the UAE testing, inspection, and certification market share in 2024, whereas certification is projected to register the fastest 6.2% CAGR to 2030.

- By sourcing model, outsourced services held 64.5% of the UAE testing, inspection, and certification market size in 2024 and are advancing at a 5.9% CAGR through 2030.

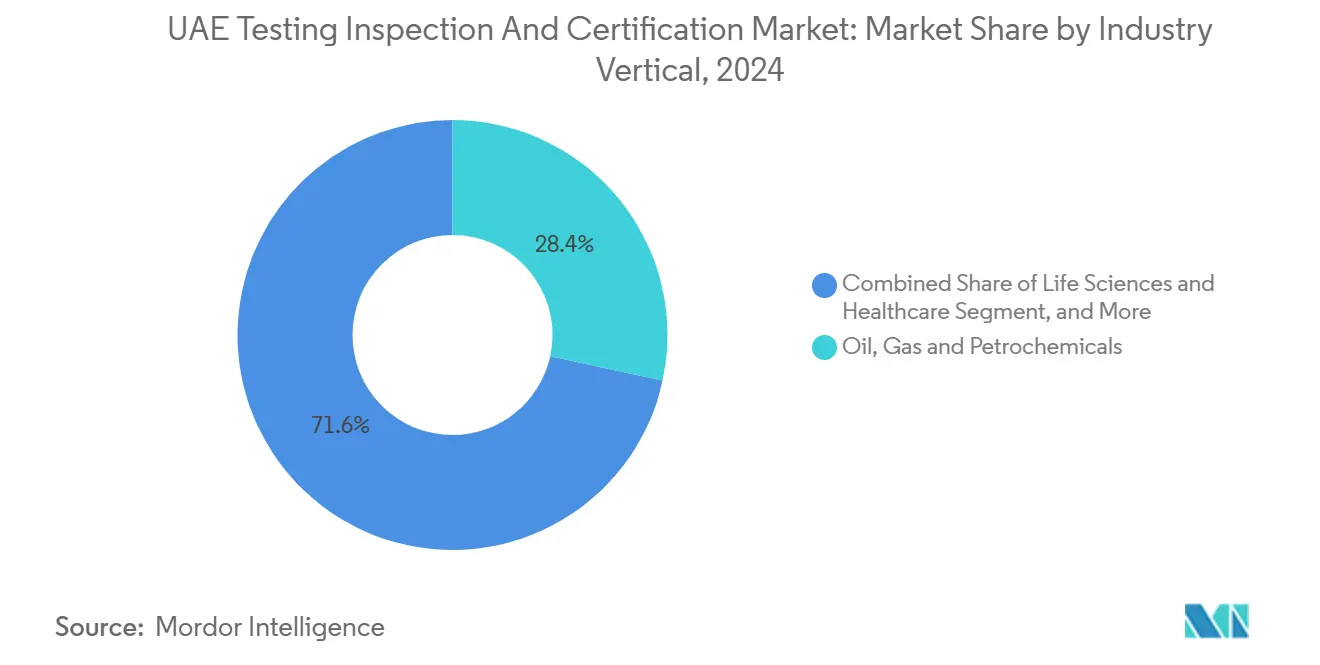

- By industry vertical, oil, gas, and petrochemicals led with 28.4% revenue share in 2024; life sciences and healthcare are forecast to expand at a 6.5% CAGR through 2030.

- By mode of service delivery, on-site services accounted for 41.4% of the UAE testing, inspection, and certification market size in 2024, while remote/digital services are set to grow at a 6.6% CAGR over the same horizon.

UAE Testing Inspection And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations for product quality and safety compliance | +1.8% | Dubai and Abu Dhabi core, nation-wide reach | Long term (≥ 4 years) |

| Industrial diversification under UAE Vision 2030 | +1.5% | Abu Dhabi, Dubai, Sharjah first movers | Medium term (2-4 years) |

| Rising trade volumes driving conformity assessment demand | +1.2% | All Emirates, GCC spill-over | Short term (≤ 2 years) |

| Digital transformation and Industry 4.0 adoption | +1.0% | UAE, wider Middle East and Africa | Medium term (2-4 years) |

| Emergence of hydrogen economy requiring new test protocols | +0.8% | Abu Dhabi and Dubai clusters | Long term (≥ 4 years) |

| Mandatory ESG disclosure spurring assurance services | +0.6% | UAE financial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations for Product Quality and Safety Compliance

Multiple federal statutes converge to make pre-market testing non-negotiable for regulated goods. ECAS obliges every importer to register products and obtain a Certificate of Conformity, a process that mandates laboratory analysis ranging from electromagnetic compatibility to heavy-metal screening.[2]WWBridge, “Fast certification procedures in the UAE,” wwbridge-cert.com The Emirates National Accreditation System (ENAS) lists more than 200 accredited labs, inspection entities, and medical laboratories, giving manufacturers viable local options to prevent costly shipment holds at seaports. Budget implications are material: trade-license fees alone vary from AED 17,000 (USD 4,624) to AED 100,000 (USD 27,200) per product line, encouraging firms to engage one-stop testing, inspection, and certification providers to minimize re-testing cycles. In 2024, Dubai Civil Defence endorsed the Emirates Safety Laboratory and Dubai Acoustic Research Laboratory alliance to deliver joint fire-safety and acoustic-proofing tests, illustrating how regulators welcome integrated compliance hubs that shorten project approvals. Such frameworks effectively lock in a baseline growth floor for the UAE testing, inspection, and certification market because every new product category triggers fresh conformity layers.

Industrial Diversification Under UAE Vision 2030

Operation 300bn and the National Hydrogen Strategy have set ambitious capacity targets that can only be realized with robust testing, inspection, and certification support. The government aims for USD 300 billion in local industrial output by 2031 and intends to produce 1.4 million tpa of hydrogen, milestones that necessitate new protocols for gas purity, electrolyzer safety, and composite-tank durability. Masdar and ADNOC have disclosed green- and blue-hydrogen pilot plants requiring bespoke materials-compatibility studies to mitigate hydrogen embrittlement risks. Beyond energy, Borouge’s intended ethane-cracker expansion is estimated to generate USD 165-200 million in annual EBITDA and demands extensive process-hazard analysis and pressure-vessel certification at every project phase. Each investment unlocks serial testing contracts, elevating the UAE testing, inspection, and certification market position as a strategic enabler of national diversification.

Rising Trade Volumes Driving Conformity Assessment Demand

The Emirate’s free-zone logistics ecosystem, anchored by Jebel Ali Port and Khalifa Port, moves millions of containers annually. Every incoming regulated item, from small appliances to automotive spares, undergoes ECAS review, making laboratory throughput correlate almost linearly with trade volumes. The USD 3 billion Abu Dhabi-Fujairah crude pipeline has elevated Fujairah’s role as an energy-trading hub, further multiplying the variety of goods requiring customs-clearance testing. Multinationals' warehousing in Dubai distributes to the wider GCC, compelling them to commission batch stability trials and shelf-life studies that meet not just UAE but also Saudi and Omani standards. As the UAE continues to leverage bilateral trade agreements, conformity-assessment bookings tend to spike immediately after every tariff-liberalization round, reaffirming a structural growth driver for the UAE testing, inspection, and certification market.

Digital Transformation and Industry 4.0 Adoption

The UAE’s technology spending accelerates demand for both validating new digital assets and embedding AI inside testing, inspection, and certification workflows. Microsoft’s USD 1.5 billion stake in G42 came with commitments to build two AI centers in Abu Dhabi, installations that require electrical-load testing, cooling-system thermal validation, and cybersecurity audits before handover. The USD 100 billion MGX fund earmarks large-scale data-center clusters that will rely on electromagnetic-interference testing to safeguard high-performance compute racks. Artificial-intelligence-driven inspection approaches are gaining ground: Gecko Robotics secured a USD 30 million ceiling contract with ADNOC Gas, enabling 99.6% coverage through wall-climbing robots and predictive analytics dashboards. Such case studies propel wider adoption of remote sensing, drone imagery, and digital twins, all of which reinforce demand for calibration labs, software-algorithm validation, and third-party penetration testing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex for advanced labs and skilled talent | −0.8% | Dubai and Abu Dhabi | Medium term (2-4 years) |

| Regulatory overlaps across Emirates | −0.5% | Entire UAE | Short term (≤ 2 years) |

| Limited local accreditation for AI/IoT standards | −0.4% | Tech hubs | Long term (≥ 4 years) |

| Emiratization policy tightening talent pipeline | −0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cap-ex for Advanced Labs and Skilled Talent

Building ISO/IEC 17025-accredited facilities for next-generation materials and hydrogen testing entails multimillion-dollar spectrometry, micro-CT, and high-pressure-hydrogen chambers. Compliance also demands periodic proficiency testing, pushing ongoing opex higher. On the human-capital side, Emiratization mandates require firms with more than 50 employees to raise their Emirati headcount by 2% annually, or face fines ranging from AED 6,000 (USD 1,632) to AED 108,000 (USD 29,376) per annum. The salary premium for local engineers further inflates project budgets, while global shortages of PhD-level metallurgists and cybersecurity auditors lengthen hiring cycles. Farnek’s 2024 facility-management experience managing over 9,000 workers highlights the scale of workforce requirements once large industrial complexes come online. Together, these factors place a ceiling on how quickly smaller testing, inspection, and certification players can scale.

Regulatory Overlaps Across Emirates

Although ESMA governs national standards, individual emirates operate parallel systems that can duplicate compliance routines. Dubai’s Trakhees authority, for example, issues its own marine-project safety certificates in Jebel Ali Free Zone, even for assets already cleared under federal rules. Free-zone entities like DIFC and ADGM administer separate legal frameworks, creating multiple audit tracks for testing, inspection, and certification providers that serve clients with multi-emirate footprints. The federal Competition Law’s new AED 300 million (USD 81.6 million) turnover threshold for merger filings adds another procedural layer for acquisitions, complicating scale-up strategies designed to ease fragmentation. The administrative burden diverts resources away from technology upgrades and delays service launches, presenting a moderate but persistent headwind for the UAE testing, inspection, and certification market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Dominance Drives Market Foundation

Testing services held a commanding 56.3% of the UAE testing, inspection, and certification market share in 2024 as mandatory ECAS protocols obligate laboratory analysis before any regulated product can reach retail shelves. The segment’s revenue base is enlarged by high-volume consumer-electronics imports that now undergo expanded electrical-safety regimes after SGS inaugurated new Dubai test bays in January 2025. Certification, while smaller today, is forecast to rise at a 6.2% CAGR as ESG-linked listing requirements and hydrogen-economy guidelines emerge; in value terms, certification is on track to add nearly USD 80 million by 2030, lifting its contribution to the overall UAE testing, inspection, and certification market size. Inspection remains essential in oil-and-gas integrity programs, with recent ADNOC turnaround campaigns triggering multi-site non-destructive-testing bursts that keep technician utilization near capacity.

Historical trajectories reveal that certification revenue has doubled since 2019, signaling corporates’ growing appetite for externally verified sustainability and cyber-discipline claims. TÜV Rheinland’s multi-year corrosion-inspection deal across Abu Dhabi pump stations showcases steady inspection demand amid asset-life-extension drives. Meanwhile, data analytics and automation push testing labs toward higher throughput; Gecko Robotics’ AI model reduced per-unit inspection windows by 93%, enabling higher daily sample loads. As digital twins integrate with lab information systems, hybrid models are forming, where continuous sensor data feeds selective destructive testing, enhancing both accuracy and cost efficiency for the UAE testing, inspection, and certification market.

By Sourcing Type: Outsourcing Accelerates Specialization Trends

Outsourced contracts captured 64.5% of the UAE testing, inspection, and certification market size in 2024, driven by corporates that prefer variable-cost models over capital-heavy in-house labs. Margin pressures in refining and manufacturing have made external providers attractive because they amortize equipment costs across multiple clients while retaining specialist staff. The 5.9% forecast CAGR for outsourcing eclipses in-house expansion, reflecting how swiftly regulatory complexity and technology cycles outpace internal capability refresh rates. Borrowing talent on demand also aligns with Emiratization quotas, enabling principal employers to meet nationality targets without bloating payroll lists.

In-house operations persist among asset-heavy majors: ADNOC maintains independent metallurgy centers for routine coupon analysis, while Emirates Steel runs its own spectrometry rigs for heat-number verification. However, even these giants now subcontract advanced hydrogen-embrittlement or AI-model-validation tests to boutique houses that possess unique accreditations. AIMMS Group’s Trakhees-approved marine-survey arm illustrates how niche authorization status can clinch high-value assignments. Over 2025-2030, hybrid models are likely, where core QA/QC stays internal but peak-load and frontier technology projects swing to specialist vendors, solidifying the primacy of external networks in the UAE testing, inspection, and certification market.

By Industry Vertical: Energy Sector Leadership Faces Healthcare Disruption

Oil, gas, and petrochemicals accounted for 28.4% of the UAE testing, inspection, and certification market share in 2024, bolstered by ADNOC’s USD 45 billion Ruwais expansion that mandates materials-traceability checks and pressure-boundary inspections at every EPC milestone. The segment benefits from deep-water rig refurbishments and hydrogen co-firing pilots that layer on additional safety audits. Yet life sciences and healthcare clock the fastest 6.5% CAGR through 2030 as the Emirates courts pharmaceutical investments with fast-track GMP certification pipelines. M42’s advanced diagnostics labs, coupled with Cleveland Clinic Abu Dhabi’s medical-device trials, require an expanding portfolio of sterility, biocompatibility, and data-integrity tests, creating fresh revenue pools for testing, inspection, and certification operators proficient in ISO 13485 standards.

Telecom and ICT sustain mid-single-digit growth on continued 5G rollout and data-center clustering, each new base-station and server hall calling for electromagnetic-field audits and structured-cabling conformance checks. Construction testing remains resilient amid the USD 17.97 billion infrastructure project slate approved for Abu Dhabi in 2024, including super-span bridges and smart-city districts that must meet stringent fire-retardance and acoustic-attenuation codes. Consumer-goods testing stays vibrant because Dubai’s re-export engine funnels products to neighboring markets. All combined, these cross-currents keep the UAE testing, inspection, and certification market diversified, reducing dependence on any single vertical and cushioning cyclical dips.

By Mode of Service Delivery: Digital Transformation Reshapes Traditional Models

On-site execution dominated with 41.4% of the UAE testing, inspection, and certification market size in 2024, as refinery turnarounds, pipeline pigging, and civil-structure audits necessitated technicians’ physical presence. High-risk environments often require rope-access non-destructive examinations that cannot yet be fully automated. Yet remote/digital channels will clock a 6.6% CAGR, underwritten by drone surveys of flare stacks, real-time corrosion mapping, and AI-enabled image analytics. The Gecko-ADNOC use case proves that one remote crew covering multiple assets via robotic crawlers can replace several field teams during shutdown windows, with inspection depth hitting 99.6%.

Off-site laboratories continue to capture roughly 35% revenue because controlled conditions remain indispensable for instrument calibration and destructive metallographic tests. SGS’s enlarged Dubai facility now hosts climate chambers and anechoic rooms, allowing simultaneous testing of connected appliances for ECAS electromagnetic compliance and environmental durability. Looking forward, expect blended models, where live sensor feeds trigger remote alarms and only anomalous data points convert into on-site call-outs or lab pulls. This convergence not only lifts asset uptime but also underpins next-decade growth for the UAE testing, inspection, and certification market.

Geography Analysis

Abu Dhabi and Dubai jointly commanded nearly 70% of revenue in 2024, mirroring their status as energy and commercial nerve centers. ADNOC’s mega-projects and Masdar’s hydrogen initiatives keep Abu Dhabi’s laboratory network humming, while Dubai’s logistics platforms drive consumer-goods and electronics testing demand. Both emirates possess mature accreditation ecosystems, shortening client approval cycles and reinforcing their gravitational pull within the UAE testing, inspection, and certification market.

The Northern Emirates, Sharjah, Ras Al Khaimah, Fujairah, Ajman, and Umm Al Quwain make up the remaining 30% but are outpacing the leaders with 6.2-6.8% CAGR projections. Ras Al Khaimah’s RAK Ports renovation and RACS-DNV ECAS delivery pact illustrate how localized industrial clusters spawn TIC demand off the traditional axis.[3]DNV, “DNV and RACS sign collaboration agreement,” dnv.com Fujairah’s strategic crude-storage parks require cathodic-protection and leak-detection audits, while Sharjah’s manufacturing estates need boiler inspections and clean-room validations for emerging life-science tenants.

Geographic rebalancing also rides on lower land-lease rates and Emirate-specific incentives that attract medium-sized factories seeking cost shields. Free-zone rules enable full foreign ownership, prompting multinational lab networks to set up satellite units closer to client plants, reducing sample transit times. Collectively, these shifts are widening the geographical footprint of the UAE testing, inspection, and certification market and democratizing access to accredited services across the federation.

Competitive Landscape

The UAE testing, inspection, and certification market features a moderate concentration of global heavyweights SGS, Bureau Veritas, Intertek, and the combined TÜV group, controlling core industrial accreditations and deep brand equity. Merger discussions between SGS and Bureau Veritas, valued at USD 33 billion, if finalized, could raise the top-two combined share above 45%, triggering compulsory antitrust reviews under the new AED 300 million notification thresholds. Size apart, differentiation is tilting toward digital capability. SGS’s Dubai lab now integrates IoT-enabled chambers that stream real-time data to client dashboards, while Intertek pilots blockchain-secured certificate repositories to prevent document tampering.

Niche specialists defend turf by carving out high-barrier segments. AIMMS Group, freshly Trakhees-approved, tackles maritime and offshore inspections inside Jebel Ali Free-Zone, a requirement international chains seldom meet without local partners.[4]AIMMS Group, “Trakhees approved Third-Party Inspection,” aimmsgroup.com Gecko Robotics’ AI inspection service has set new benchmarks in coverage and speed, compelling traditional firms to fast-track robotics partnerships or risk share erosion. DNV’s link-up with RACS leverages mutual strengths: international brand trust and local regulatory familiarity, respectively.

Price competition remains rational because entry barriers are high capital intensity, accreditation lead times, and skilled talent shortages prevent race-to-bottom dynamics. Yet client expectations are climbing; hydrogen-pilot owners, for example, insist on labs capable of 0.1-ppm gas chromatograph accuracy, narrowing the viable provider list. Overall, digital prowess and sector-specific credentials will dictate rank shifts more than sheer scale, keeping the UAE testing, inspection, and certification market both dynamic and innovation-led.

UAE Testing Inspection And Certification Industry Leaders

SGS Gulf Ltd

Bureau Veritas UAE LLC

Intertek Middle East LLC

TÜV SÜD Middle East LLC

TÜV Rheinland Middle East

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DEKRA acquired Chilworth Global to deepen process-safety offerings, broadening its UAE service menu..

- May 2025: AIMMS Group received Trakhees approval for third-party inspection and maintenance services across Dubai Maritime City and Jebel Ali Port.

- April 2025: Borouge awarded Linde Engineering and Target Engineering contracts for cracker and polyethylene-unit upgrades expected to add USD 165-200 million in annual EBITDA once operational in 2027.

- March 2025: UAE Cabinet instituted AED 300 million turnover thresholds for merger-control notifications, influencing TIC consolidation plays.

UAE Testing Inspection And Certification Market Report Scope

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

How large is the UAE testing inspection and certification market in 2025?

The UAE TIC market size is USD 1.76 billion in 2025 and is projected to grow to USD 2.34 billion by 2030 at a 5.78% CAGR.

Which service category leads revenue?

Testing services hold 56.3% of the UAE TIC market share in 2024, driven by mandatory ECAS laboratory requirements.

What segment grows fastest through 2030?

Certification services record the highest 6.2% CAGR thanks to upcoming ESG and hydrogen-economy protocols.

Why are outsourced TIC services gaining ground?

Outsourcing commands a 64.5% share because external providers spread capital costs and help firms meet Emiratization quotas while accessing niche expertise.

Which emirates offer the strongest growth outlook?

Khaimah, and Fujairah together advance at more than 6% CAGR as industrial projects and new free-zone incentives spread TIC demand beyond Abu Dhabi and Dubai.

How will AI affect inspection services?

AI-enabled robotics, such as Gecko Robotics’ crawlers, achieve asset-coverage rates above 99% and cut inspection time by over 90%, accelerating the adoption of digital inspections across the UAE.

Page last updated on: