South Africa Testing Inspection And Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

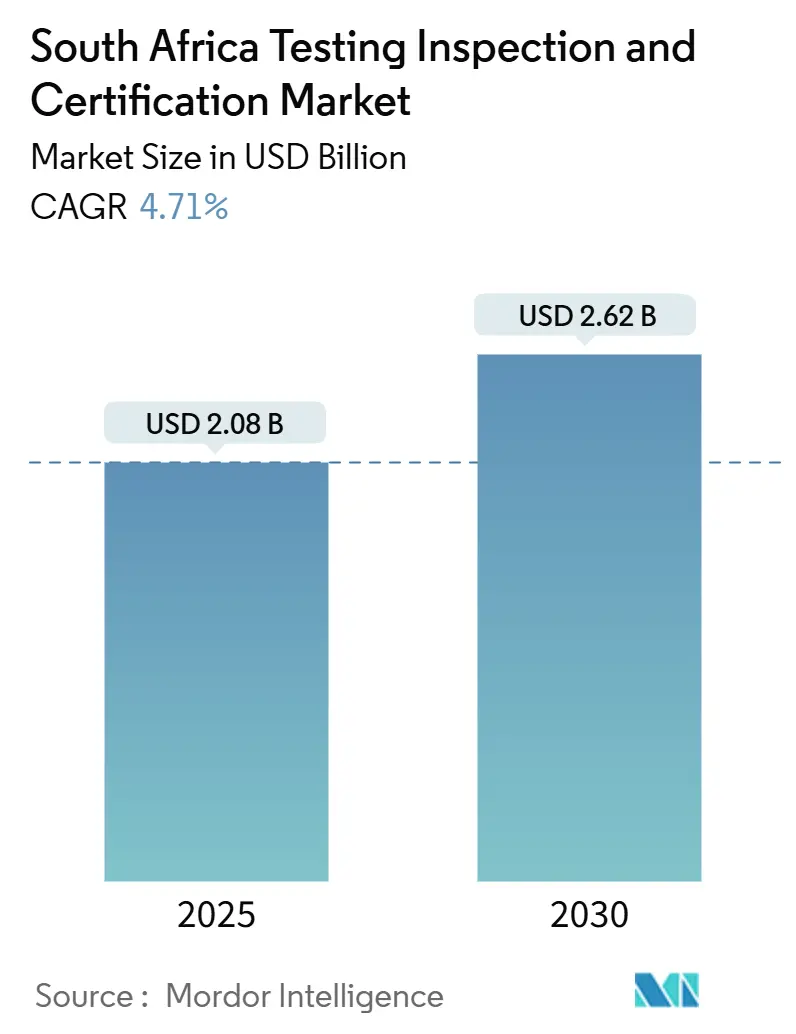

| Market Size (2025) | USD 2.08 Billion |

| Market Size (2030) | USD 2.62 Billion |

| Growth Rate (2025 - 2030) | 4.71% CAGR |

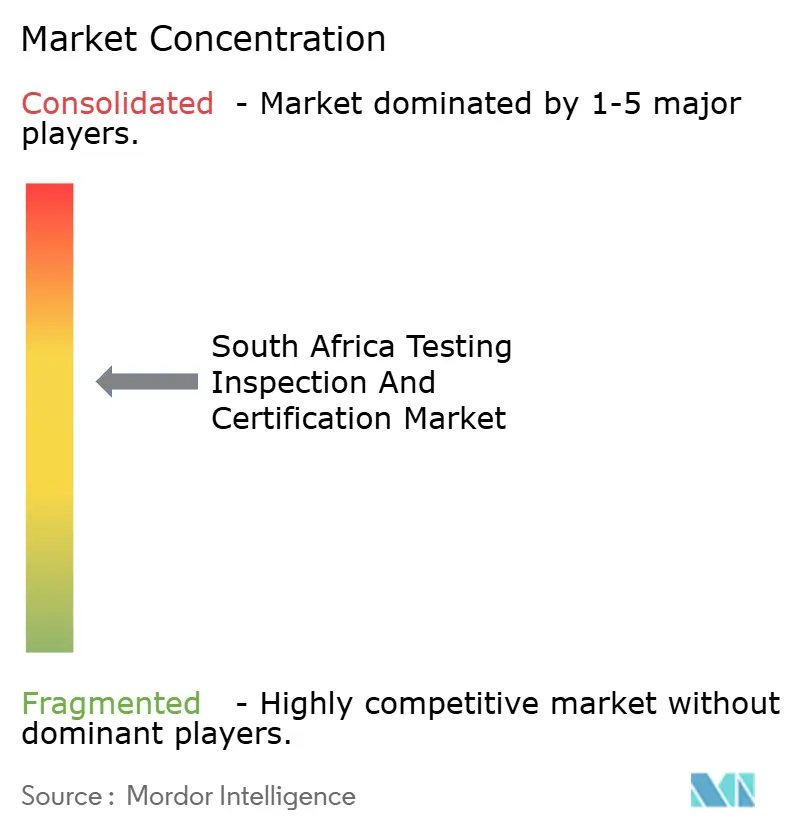

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Testing Inspection And Certification Market Analysis by Mordor Intelligence

The South Africa testing inspection and certification market size is estimated at USD 2.08 billion in 2025 and, supported by a 4.71% CAGR, is forecast to reach USD 2.62 billion by 2030. Expansion is fueled by stricter domestic regulations, rapid export growth in agri-food and minerals, and fast-rising demand for digital inspection services that offset chronic infrastructure constraints such as power shortages. Certification is advancing the quickest because SAHPRA made ISO 13485 mandatory for all medical-device establishments from April 2025, while testing remains the largest revenue contributor thanks to South Africa’s commodity-export orientation. Outsourcing continues to surge as firms abandon in-house laboratories after SABS lost accreditation in January 2025, and international TIC majors accelerate investments in AI-enabled platforms to boost efficiency. Renewable-energy localization rules, automotive export compliance, and ESG verification requirements provide further structural tailwinds for the South Africa testing inspection and certification market.

Key Report Takeaways

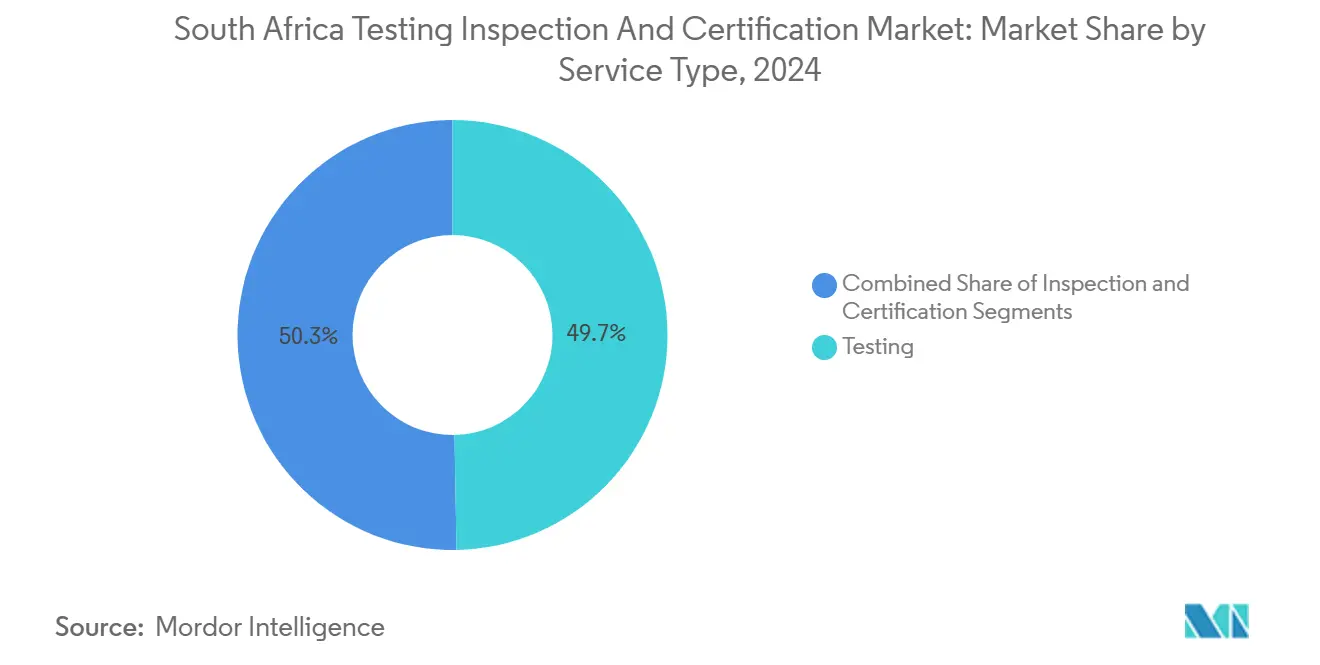

- By service type, testing led with 49.7% of South Africa testing inspection and certification market share in 2024, while certification is projected to post the fastest 5.3% CAGR to 2030.

- By sourcing type, outsourced services accounted for 59.7% of the South Africa testing inspection and certification market size in 2024 and are projected to expand at 5.1% CAGR through 2030.

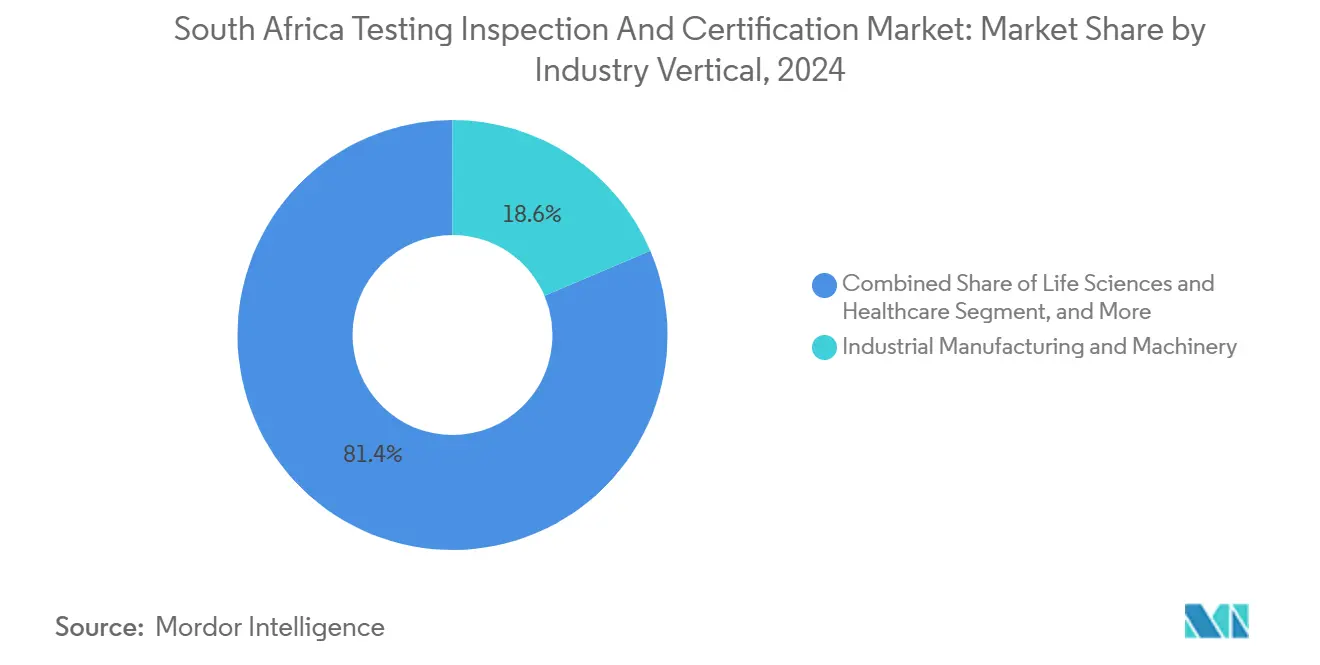

- By industry vertical, industrial manufacturing and machinery captured 18.6% revenue share in 2024; life sciences and healthcare is forecast to record the highest 5.6% CAGR over 2025-2030.

- By mode of service delivery, on-site services held 54.2% share of the South Africa tes ting inspection and certificationmarket in 2024, while remote and digital inspections are advancing at a 5.8% CAGR.

South Africa Testing Inspection And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter domestic product-safety regulations | +1.2% | Gauteng, Western Cape | Medium term (2-4 years) |

| Export-oriented agri-food and mineral growth | +0.9% | Western Cape, Northern Cape, Limpopo | Long term (≥ 4 years) |

| Digital and AI-enabled inspection uptake | +0.8% | Urban centers nationwide | Short term (≤ 2 years) |

| OEM localization mandates | +0.7% | Eastern Cape, Gauteng | Medium term (2-4 years) |

| Mandatory ISO 13485 for medical devices | +0.6% | Pharmaceutical hubs nationwide | Short term (≤ 2 years) |

| Rising ESG and carbon-verification demand | +0.5% | Mining regions and export corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Domestic Product-Safety Regulations Across Key Sectors

South Africa’s regulators have tightened product-safety rules in healthcare, automotive, and construction, pushing companies toward comprehensive compliance services. SAHPRA’s ISO 13485 mandate hits over 2,000 medical-device firms and creates a USD 150 million annual certification opportunity. Vehicle makers now face tougher NRCS homologation criteria to protect the nation’s status as Africa’s largest exporter. Construction contractors must conform to more rigorously enforced SANS building standards, driving structural-testing demand. Together these changes add 1.2 percentage points to the baseline CAGR and lock in recurring recertification revenue for the South Africa testing inspection and certification market.

Rapid Growth of Export-Oriented Agri-Food and Mineral Commodities

Agri-food exports rose 12% in 2024 as PPECB certified 3.2 million tons of fresh produce, spurring greater phytosanitary testing and cold-chain audits. Meanwhile, platinum group metals and rare-earth shipments need exacting quality and ESG proofs to satisfy global buyers. SGS boosted grain-testing capacity by adding mycotoxin and GMO laboratories in 2024. AfCFTA trade liberalization promises additional cross-border flows, keeping TIC demand high for years and contributing 0.9 percentage points to market CAGR.

Digital-First, Remote and AI-Enabled Inspection Solutions Seeing Fast Uptake

Persistent load-shedding forces companies to seek technology that cuts site visits and bolsters uptime. Bosch Rexroth Africa’s Smart Inspection platform allows offline data capture and real-time analysis through mobile apps. SGS rolled out its QiiQ system that trims on-site presence by 40% through remote monitoring. Mining groups employ AI-driven predictive maintenance integrated with TIC services, while the Digital Twin Consortium’s 2025 framework accelerates adoption of virtual asset models. These innovations add 0.8 percentage points to market growth in the near term.

OEM Localization Mandates for Renewable-Energy and Rail Projects

REIPPPP rules require 40%-45% local content in new solar and wind farms, compelling developers to verify supply chains rigorously. Transnet insists on 60% local inputs for rolling stock, monitored by independent inspectors. TÜV Rheinland responded by expanding asset-integrity programs focused on renewable energy and rail in 2025. These mandates add 0.7 percentage points to the forecast CAGR as localization audits become indispensable through mid-decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of SANAS-accredited staff | -0.8% | Nationwide, severe in niche technical domains | Long term (≥ 4 years) |

| Eskom load-shedding disrupting labs | -0.6% | Nationwide, regionally variable | Medium term (2-4 years) |

| Slow SABS/NRCS harmonization with global norms | -0.4% | Nationwide | Long term (≥ 4 years) |

| Dollar-denominated equipment vs weak Rand | -0.3% | Nationwide, equipment-intensive operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of SANAS-Accredited Technical Staff and Auditors

SABS’s accreditation loss in January 2025 laid bare South Africa’s chronic lack of certified professionals, lengthening project lead times by up to 40%. Specialized domains such as medical-device testing and renewable-energy certification feel the pinch most acutely because global rules demand highly qualified personnel. Emigration and under-funded training pipelines exacerbate the deficit, cutting 0.8 percentage points from the South Africa testing inspection and certification market’s CAGR and forcing firms to create local academies or import expertise.

Persistent Eskom Load-Shedding Disrupting Lab Operations

Although outages eased in 2024, power cuts still compromise equipment requiring stable voltage and precise environmental control. Labs restart sensitive tests after each interruption, stretching turnaround times and operating costs. Many TIC providers now invest in generators and UPS systems, yet these measures erode margins and scalability. The cumulative drag lowers market CAGR by 0.6 percentage points until private generation and grid reforms materially stabilize supply

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type – Testing Holds Sway While Certification Accelerates

Testing represented 49.7% of the South Africa testing inspection and certification market in 2024 thanks to rigorous export verification across agriculture, minerals, and manufactured goods. Automotive output of 633,332 units in 2023 continues to feed homologation and component validation requirements. Certification, however, registers the quickest 5.3% CAGR as firms pursue preventive compliance under ISO 13485 and other management-system regimes. SGS, TÜV Rheinland, and Bureau Veritas have broadened certification menus to address asset-integrity and process-safety needs, cementing the strategic pivot from reactive quality control to holistic risk governance. Testing remains vital, yet clients increasingly bundle it with certification and inspection for end-to-end assurance.

Certification’s upshift is rooted in regulatory enforcement and global buyer expectations. The South Africa testing inspection and certification market size for certification services is projected to widen materially as medical-device makers, renewable-energy suppliers, and exporters seek market access barriers lifted through recognized certificates. Linked digital-audit trails further speed adoption by reducing documentation cycles and supporting continuous recertification models.

By Sourcing Type – Outsourcing Dominates Amid In-House Constraints

Outsourced providers commanded 59.7% revenue in 2024 and are poised for 5.1% CAGR through 2030 as firms offload specialized testing to accredited experts. SABS’s accreditation lapse removed a public in-house alternative, accelerating migration to third-party laboratories. Maintaining equipment, accreditations, and staffing remains capital intensive, so hybrid models are emerging: businesses keep basic QA tools but rely on TIC majors for high-complexity testing. Digital dashboards such as SGS’s QiiQ reinforce outsourcing by offering transparent, real-time reporting that satisfies both regulators and clients without on-premise infrastructure. Consequently, the South Africa testing inspection and certification market continues to tilt toward service specialists with broad technical scope and geographic reach.

In-house facilities persist in large multinationals with global laboratory networks, yet even they increasingly collaborate with local TIC companies to navigate South African regulatory nuances. Smaller exporters and renewable-energy EPCs find outsourcing indispensable because accreditation costs dwarf in-house budgets. The trajectory indicates deeper integration between client ERP systems and TIC digital platforms, reinforcing the outsourcing value proposition.

By Industry Vertical – Industrial Manufacturing Leads, Healthcare Surges

Industrial manufacturing and machinery held 18.6% revenue in 2024, underpinned by domestic automotive production and extensive mining-equipment demands. The South Africa testing, inspection, and certification market size for industrial manufacturing benefits from continuous machinery exports and stringent safety checks on heavy equipment used in deep-level mining. Life sciences and healthcare are expanding at a 5.6% CAGR as SAHPRA’s ISO 13485 deadline compels device makers to engage certification bodies swiftly. Pharmaceutical exporters aiming at wider African markets also need GMP audits and batch testing, reinforcing vertical momentum.

Automotive and transportation still matter significantly, driven by NRCS homologation updates and new component manufacturing joint ventures. Oil, gas, and petrochemicals maintain robust demand for material verification and corrosion testing, evidenced by Bureau Veritas enlarging its petroleum labs in 2025.[1]Bureau Veritas South Africa, “Power and Utilities,” bureauveritas.co.za Food, agriculture, and beverages rely on phytosanitary and cold-chain certificates to maintain premium export prices. Renewable-energy expansion across wind and solar plants also elevates demand for grid-interconnection tests and turbine-component audits, integrating TIC services from construction through operation phases.

By Mode of Service Delivery – On-Site Prevails as Digital Rises

On-site inspections retained 54.2% share in 2024 because heavy industry, construction, and mining require physical presence for safety checks. Yet remote and digital delivery is outpacing with 5.8% CAGR as power constraints and distance logistics make virtual inspections attractive. Bosch Rexroth’s Smart Inspection and SGS’s QiiQ show how mobile apps, drones, and IoT sensors allow specialists to advise from centralized hubs, minimizing travel delays. The South Africa testing inspection and certification market share for digital services should widen steadily as clients gain confidence in regulator acceptance of remote evidence.

Off-site laboratories remain crucial for advanced analyses that demand controlled environments. However, laboratories increasingly integrate cloud-connected instruments that feed results directly into client dashboards, blending traditional and digital models. On-site work is not disappearing but evolving: field engineers now deploy portable analyzers and augmented-reality helmets to stream data to remote experts, shortening decision cycles and reducing rework costs.

Geography Analysis

Gauteng anchors the South Africa testing inspection and certification market thanks to its concentration of automotive assembly, mining-services headquarters, and financial institutions that set procurement standards. Western Cape follows, driven by agri-food exports funneled through Cape Town port and stringent cold-chain verification needs. Eastern Cape is fast becoming a renewable-energy manufacturing cluster with wind-turbine and battery-storage factories, stimulating localized testing requirements. Northern Cape’s solar corridors and mineral exploration increase demand for environmental and component certification.

Load-shedding unevenly affects regions, amplifying demand for mobile labs in remote mining territories where power restoration lags. SANAS-accredited facilities cluster in urban centers, so TIC providers deploy containerized labs and drone-based inspection to cover distant client sites quickly. Port cities form key gateways where PPECB and customs officers coordinate with TIC firms to validate shipments before export, ensuring compliance with foreign standards.

Digital inspection platforms help bridge geographic gaps by allowing centralized specialists in Johannesburg or Durban to supervise inspections in far-flung solar farms or rail upgrades. Nonetheless, physical audits remain mandatory for critical infrastructure, so providers invest in regional hubs and talent pipelines to ensure quick response times. As provincial governments roll out industrial parks and special economic zones, localized TIC capacity will continue expanding to support diversified export bases.

Competitive Landscape

International majors such as SGS, Bureau Veritas, and Intertek dominate the South Africa testing, inspection, and certification market, leveraging global best practices and broad accreditation portfolios. Market concentration is moderate but tightening as SGS executed 11 worldwide acquisitions worth CHF 200 million (USD 226 million) in 2024 to deepen cybersecurity, environmental testing, and customs capabilities.[2]SGS, “Annual Report 2024,” sgs.com Talks of a USD 33 billion SGS-Bureau Veritas merger could propel a single company to unprecedented scale, reshaping local competitive dynamics.

Digital differentiation now separates leaders from laggards. Bureau Veritas joined the Africa Solar Industry Association in 2024 to cement its renewable-energy position.[3]Africa Solar Industry Association, “Bureau Veritas Membership,” africa-solar.org TÜV Rheinland extended asset-integrity consulting to capture localization-driven demand in energy and rail. Local specialists carve out niches in mineral sample preparation, vis-à-vis Tabono Mining Solutions’ 2024 collaboration with Minprotech, while startups focus on drone inspection or data analytics.

White-space opportunities are emerging in ESG auditing, cybersecurity testing, and 5G infrastructure certification, where regulatory frameworks are nascent. TIC firms with AI-enabled platforms attract client loyalty by cutting inspection turnaround and ensuring audit-trail transparency, a decisive factor under tightening global trade rules. Partnerships with universities and technical colleges are increasing to alleviate talent shortages, creating feeder programs for SANAS-accredited professionals.

South Africa Testing Inspection And Certification Industry Leaders

SGS South Africa (Pty) Ltd

Bureau Veritas South Africa (Pty) Ltd

Intertek Testing Services South Africa (Pty) Ltd

TÜV Rheinland South Africa (Pty) Ltd

DEKRA Industrial (Pty) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bosch Rexroth Africa launched Smart Inspection, a SaaS platform for offline inspections and real-time asset monitoring via QR-enabled mobile apps.

- January 2025: SABS lost accreditation, triggering immediate migration to private TIC providers for testing and certification.

- January 2025: TÜV Rheinland South Africa expanded asset-integrity management consulting for renewable-energy and rail projects.

- December 2024: SGS completed 11 acquisitions totaling CHF 200 million (USD 226 million) to broaden service depth.

South Africa Testing Inspection And Certification Market Report Scope

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

What is the projected value of the South Africa testing inspection and certification market in 2030?

The market is forecast to reach USD 2.62 billion by 2030 on the back of a 4.71% CAGR.

Which service type is growing fastest within South Africa testing inspection and certification?

Certification services are expanding at a 5.3% CAGR because of new ISO 13485 and other compliance mandates.

Why are outsourced TIC services gaining share in South Africa?

Companies prefer accredited third-party providers after SABS lost accreditation and because outsourcing lowers capital and staffing costs.

How do power outages affect TIC operations?

Eskom load-shedding forces laboratories to invest in backup systems and adds delays, reducing overall market CAGR by 0.6 percentage points.

Which industry vertical shows the fastest TIC growth?

Life sciences and healthcare is growing at 5.6% CAGR due to mandatory medical-device certification and expanding pharmaceutical exports.

What technologies are reshaping testing inspection and certification services in South Africa?

AI-enabled remote inspection platforms, digital twins, and mobile data-capture apps are cutting on-site visits and speeding compliance reporting.

Page last updated on: