Consumer Goods And Retail Testing, Inspection, And Certification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

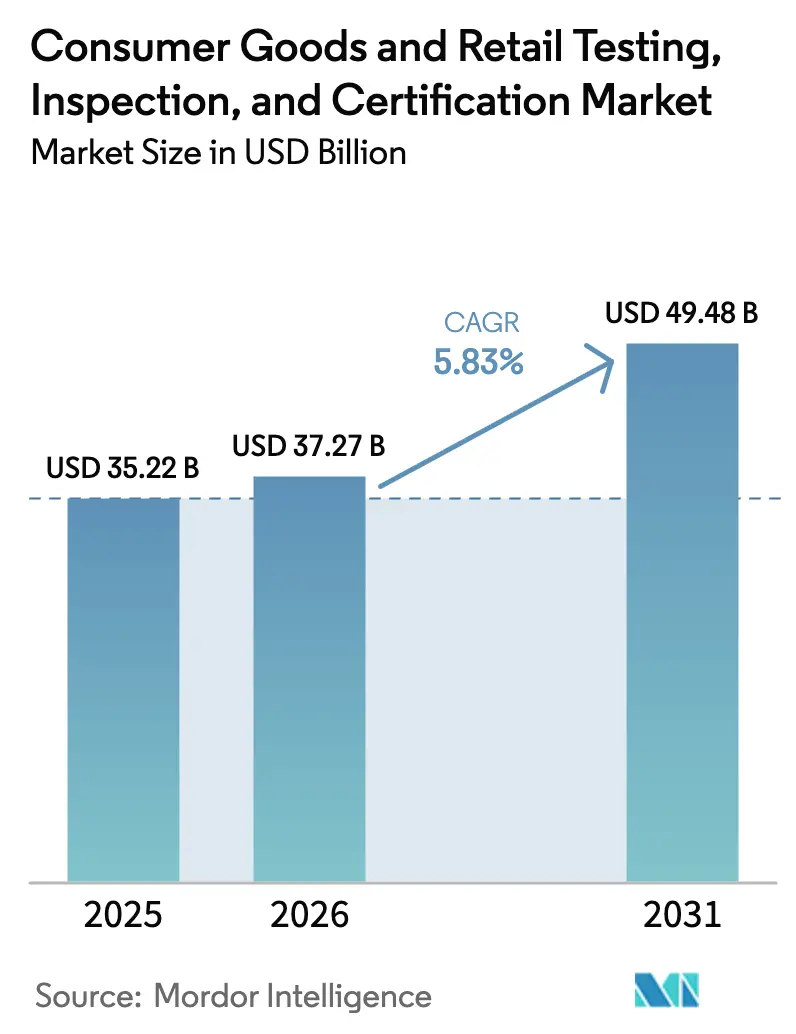

| Market Size (2026) | USD 37.27 Billion |

| Market Size (2031) | USD 49.48 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

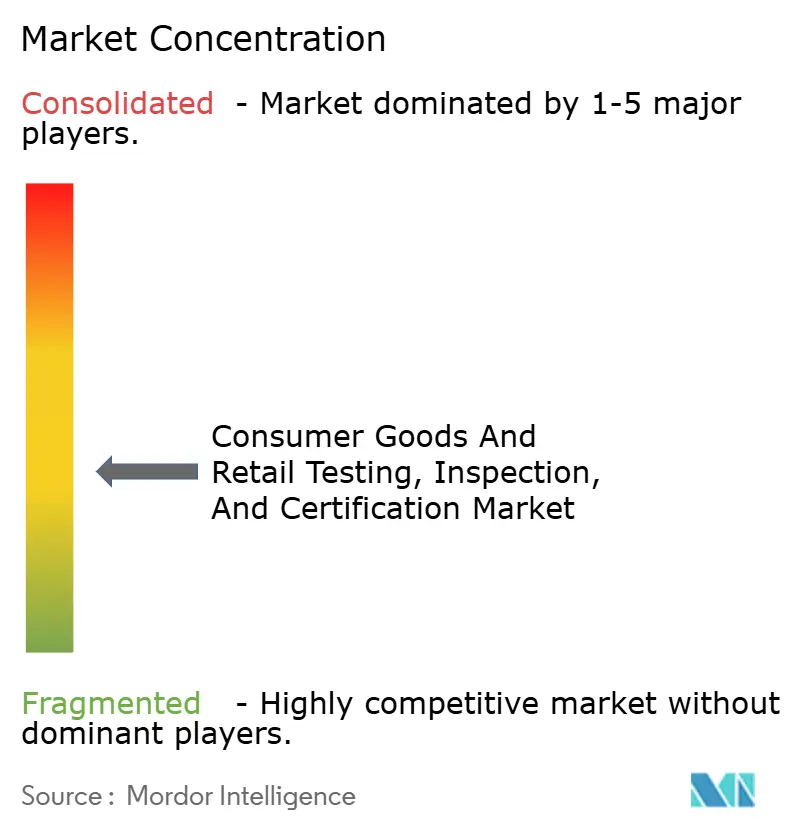

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Goods And Retail Testing, Inspection, And Certification Market Analysis by Mordor Intelligence

The consumer goods and retail testing, inspection, and certification market size is expected to grow from USD 35.22 billion in 2025 to USD 37.27 billion in 2026 and is forecast to reach USD 49.48 billion by 2031 at 5.83% CAGR over 2026-2031. Rising global trade, mandatory product-safety rules, and expanding ESG verification mandates sustain non-discretionary demand, while cross-border e-commerce and novel foods regulation introduce fresh revenue pools for established players. Asia-Pacific’s manufacturing dominance and tightening regional frameworks accelerate service uptake, whereas North America and Europe rely increasingly on digital inspection and sustainability validation to re-ignite growth. Outsourcing persists as the preferred sourcing model because it frees capital and grants rapid access to specialized laboratories. Despite steady consolidation attempts, the sector stays fragmented, encouraging bolt-on M and A that lets global brands fill portfolio gaps in cybersecurity, AI-enabled inspection, and sustainability assurance.

Key Report Takeaways

- By service type, testing services led with a 54.07% revenue share in 2025, while certification services are forecast to expand at a 6.28% CAGR through 2031.

- By sourcing type, the outsourced model commanded 63.52% of the consumer goods and retail testing, inspection, and certification market share in 2025, and is advancing at a 6.01% CAGR to 2031.

- By geography, Asia-Pacific captured 41.72% of 2025 revenue and is projected to post the fastest 6.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Consumer Goods And Retail Testing, Inspection, And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent sustainability and traceability mandates | +1.2% | Global, with the EU and North America leading | Medium term (2-4 years) |

| Rise of direct-to-consumer (D2C) private-label brands | +0.8% | Global, concentrated in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Integration of AI-enabled automated visual inspection | +0.6% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Growth in cross-border e-commerce product flows | +0.9% | Global, with Asia-Pacific export hubs and Western import markets | Short term (≤ 2 years) |

| Expansion of food safety regulations on novel foods | +0.5% | EU, North America, Singapore, China | Medium term (2-4 years) |

| Demand for ESG-verified consumer goods funding access | +0.7% | Global, with emphasis on the EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Sustainability and Traceability Mandates

Third-party verification has become pivotal as the EU Corporate Sustainability Due Diligence Directive, the Corporate Sustainability Reporting Directive, and the U.S. Uyghur Forced Labor Prevention Act push companies to document environmental and social integrity throughout supply chains. Supply chains account for nearly 80% of consumer-goods emissions, so upstream audits and lifecycle assessments have shifted from optional to obligatory service lines. TIC providers offering material tracing, forced-labor screening, and biodiversity impact attestations now command long-term annuity-like contracts. These mandates also drive demand for digital chain-of-custody platforms that embed audit data directly into ESG reports, strengthening switching costs for accredited labs. As regulators widen the scope to circular-economy metrics, certification revenues diversify beyond classic safety testing.[1]Oritain, “How ESG Is Driving Investment and the Future of Supply Chain Due Diligence,” oritain.com

Rise of Direct-to-Consumer Private-Label Brands

Thousands of D2C merchants now lean on marketplace dashboards such as Amazon’s Manage Your Compliance, which, since April 2024, requires third-party certification for dietary supplements before listings go live. Lean teams with tight launch calendars favor turnkey bundles that combine specification checks, label reviews, and customs clearance in a single workflow. Platforms like Factored Quality cut typical onboarding by three months and slash compliance costs by USD 10,000 per stock-keeping unit, rewarding TIC firms that provide API-driven documentation feeds. The surge of micro-brands, therefore, transforms the consumer goods and retail testing, inspection, and certification market into a volume business with rapid-response labs.

Growth in Cross-Border E-Commerce Product Flows

Cross-border sellers must juggle U.S. FCC electromagnetic-compatibility reports, EU CE marking, United Kingdom UKCA labels, and packaging producer-responsibility filings, often for a single shipment. Sellers lacking in-house regulatory teams turn to global TIC networks that promise harmonized protocols across 1,000+ accreditations. SGS, operating the world’s broadest authorization portfolio, leverages this edge to secure multi-year contracts with platforms like TEMU that route millions of parcels daily. The complexity of e-commerce rules, therefore, converts fragmented one-off testing orders into recurring engagements, lifting average revenue per client across the testing, inspection, and certification market.

Integration of AI-Enabled Automated Visual Inspection

Machine-learning algorithms embedded in cameras now pinpoint micron-level defects and measure tolerances at line speed, often surpassing human inspectors. TIC companies validate these systems, calibrate sensors, and issue algorithm-performance certificates demanded by regulators worried about opaque AI models. While automation mitigates labor shortages, the constant connectivity of vision systems exposes production lines to cyber risk, spurring new service demand for vulnerability assessments under the EU Cyber Resilience Act. The intertwining of AI accuracy testing and cybersecurity assurance unlocks dual-revenue streams and cements technology governance as a growth pillar.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory regimes across emerging markets | -0.4% | Africa, Latin America, Southeast Asia | Long term (≥ 4 years) |

| Shortage of qualified TIC talent in specialised verticals | -0.6% | Global, acute in North America and Europe | Medium term (2-4 years) |

| High cost of real-time testing instrumentation | -0.3% | Global, particularly affecting smaller TIC providers | Short term (≤ 2 years) |

| Cybersecurity risks in connected inspection devices | -0.2% | Global, concentrated in IoT-heavy manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified TIC Talent in Specialized Verticals

Food-safety auditors, sustainability verifiers, and cybersecurity testers require multi-year training in HACCP, FSMA, novel foods, ISO 27001, and secure-code review. Surveys show vacancy rates topping 20% in North American food labs, forcing providers to defer projects and lengthen turnaround times.[2]Food Safety Magazine, “Addressing the Food Safety Workforce Shortage,” food-safety.comThe talent gap widens as ESG and AI validation standards multiply faster than training pipelines. Firms react by acquiring boutique specialists and partnering with universities, yet these measures deliver capacity only after long lead times, capping near-term revenue capture in the testing, inspection, and certification market.

Fragmented Regulatory Regimes Across Emerging Markets

TIC firms entering Africa or Latin America face country-specific standards that duplicate testing and erode scale economies. Nigeria and Kenya require local lab accreditation, while Brazil’s medical-device rule changes obligate fresh audits even for previously cleared products. Duplicate protocols inflate client costs, leading some exporters to bypass smaller markets altogether. Although regional harmonization initiatives are underway, progress remains slow, deferring the efficiencies global players enjoy in more unified jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type – Testing Services Hold Scale as Certification Accelerates

Testing services represented 54.07% of 2025 revenue in the testing, inspection, and certification market, underscoring the enduring priority of verifying electrical safety, chemical composition, and mechanical resilience before goods ship to retailers. Mandatory protocols such as IEC 62368-1 and ISO 10993 compel manufacturers of electronics and medical devices to submit samples, often at multiple production stages. Multinational laboratories capitalize on high fixed-asset utilization, while regional specialists thrive by focusing on fast-turnaround consumer-goods batches. Certification services, however, deliver the fastest 6.28% CAGR, fueled by investors and regulators who now require independent validation of climate claims, ethical sourcing, and circular-design credentials. The pivot toward certification also raises margin profiles: documentation review and factory audits command premium pricing despite lighter capital requirements, widening EBIT spreads for providers that re-train staff into auditors.

Growing anti-greenwashing rules across Europe and California’s Truth in Labeling for Recyclable Materials Act propel demand for cradle-to-gate carbon-footprint stamps, while financial institutions embed third-party ESG ratings into lending covenants. These shifts elevate certification from a compliance afterthought to a gatekeeper for brand access to capital. The consumer goods and retail testing, inspection, and certification market size linked to sustainability credentials could therefore double relative to legacy safety scopes by 2030. Players that combine laboratory test data with auditor insights gain a one-stop advantage, further differentiating themselves from firms confined to physical test reports.

By Sourcing Type – Outsourcing Dominates as Hybrid Models Emerge

Outsourcing accounted for 63.52% of the consumer goods and retail testing, inspection, and certification market size in 2025, confirming that even high-volume manufacturers favor variable cost structures over owning lab assets. Outsourced demand accelerated during pandemic-era supply disruptions, when flexible capacity let brands reroute production without building new clean rooms or EMC chambers. Small and mid-size D2C labels essentially begin life with an outsourced-only mindset, embedding testing fees into cost-of-goods instead of capex budgets. Hybrid models nonetheless gain traction among automotive and semiconductor giants: they maintain pilot-line labs for R and D confidentiality but dispatch full-run samples to accredited partners for formal compliance certificates.

ISO 17025 accreditation and traceability to national measurement institutes remain decisive in vendor selection, because any non-conformance can trigger customs holds. Large TIC providers extend differentiation by integrating lab information management systems (LIMS) that feed real-time dashboards to brand portals, reducing administrative friction. Start-ups focused on AI-driven test data analytics complement the model by offering predictive failure insights based on pooled results, which creates a secondary advisory revenue line inside the testing, inspection, and certification industry.

Geography Analysis

Asia-Pacific anchored 41.72% of global revenue in 2025 and will expand at a 6.41% CAGR through 2031 thanks to manufacturing depth and rising domestic quality expectations. China’s National Health Commission tightened novel-foods safety dossiers in 2024, obliging importers and local innovators to submit toxicology, allergenicity, and nutritional-equivalence data before market entry, driving laboratory backlogs. India’s electronics and textile exporters must now navigate BIS marks plus parallel FCC and CE approvals, boosting demand for multi-jurisdiction bundling. Southeast Asia benefits from supply-chain diversification as brands pivot from single-country sourcing, requiring audits across Vietnam, Indonesia, and Thailand to ensure standard consistency.

Europe and North America exhibit lower absolute growth, yet sustainability and cyber-resilience statutes invigorate specialized services. The EU Corporate Sustainability Reporting Directive obliges roughly 50,000 companies to file third-party-verified ESG statements starting FY 2025. Simultaneously, the forthcoming Cyber Resilience Act sets baseline security thresholds for connected products, creating incremental testing volume for firmware, penetration, and vulnerability assessments. In North America, federal incentives for renewable-energy projects under the Inflation Reduction Act create a pipeline of wind-turbine and solar-module certifications, while the National Institute of Standards and Technology refreshes its cybersecurity framework, raising demand for IoT assurance audits.

The Middle East and Africa present nascent opportunities, with Saudi Arabia’s Vision 2030 industrial clusters mandating pre-shipment inspections and factory audits. Nonetheless, fragmented local standards in Africa raise transaction costs as TIC firms must duplicate tests. Regional economic communities consider harmonization, yet implementation timelines remain long-term. Latin America’s story is mixed: Mexico’s automotive hub sustains steady EMC and component-fatigue testing, whereas inconsistent rule changes in smaller economies deter broad laboratory investments.

Competitive Landscape

The top four providers – SGS, Eurofins, Bureau Veritas, and Intertek – jointly control a majority of global revenue, underlining the fragmented nature of the testing, inspection, and certification market. SGS posted USD 7.9 billion in 2024 revenue, leveraging more than 1,000 government accreditations to win multi-site contracts that smaller firms struggle to replicate. Eurofins matches SGS in turnover but concentrates on bioanalytical and food domains, while Bureau Veritas and Intertek diversify across industrial, consumer, and infrastructure verticals. The collapsed USD 30 billion SGS-Bureau Veritas merger in January 2025 illustrated both appetite and practical limits for mega-deals, particularly due to overlapping client bases and antitrust scrutiny.[4]Blue News, “SGS and Bureau Veritas Will Not Merge,” bluewin.ch

M and A strategies therefore tilt toward bolt-on deals: Bureau Veritas bought South Korea’s ONETECH, KOSTEC, and India’s Hi Physix Laboratory in March 2024, enlarging its electronics testing footprint for a combined EUR 20 million (USD 21.6 million). SGS closed 92 small acquisitions since 2019, most recently adding India’s Accutest Laboratories in January 2025 to solidify pharmaceutical and environmental testing capacity. Intertek’s April 2025 purchase of Automation Technology Inc. targets functional-safety and cybersecurity validation for Industry 4.0 control systems. Technology spend focuses on AI-vision platforms, digital client portals, and blockchain traceability tools, with providers racing to automate manual steps and cut chronic talent bottlenecks.

White-space opportunities cluster around sustainability assurance, IoT security, and novel-foods toxicology. Demand outstrips supply, creating pricing power for labs with specialized chemists or ethical-audit teams. However, the capital intensity of advanced instrumentation and the difficulty of hiring subject-matter experts temper expansion speed, suggesting continued fragmentation and ongoing acquisition activity throughout the forecast window.

Consumer Goods And Retail Testing, Inspection, And Certification Industry Leaders

Intertek Group PLC

SGS SA

Bureau Veritas SA

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Intertek purchased Automation Technology Inc. to bolster industrial automation, cybersecurity, and functional-safety services.

- January 2025: SGS and Bureau Veritas terminated merger talks valued at above USD 30 billion to pursue standalone growth plans.

- January 2025: SGS acquired Accutest Laboratories to deepen its Indian testing presence, enhancing multi-jurisdiction compliance support.

- September 2024: Bureau Veritas bought ArcVera Renewables, adding wind and solar project-assessment expertise for the North American market.

Global Consumer Goods And Retail Testing, Inspection, And Certification Market Report Scope

The testing, inspection, and certification market consists of conformity assessment bodies in the consumer goods and retail industry that offer services ranging from auditing and inspection to testing, verification, quality assurance, and certification.

The Testing, Inspection, and Certification Market in the Consumer Goods and Retail Industry is Segmented by Service Type (Testing and Inspection Service, Certification Service), by Sourcing Type (Outsourced, In-house), and Geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the testing, inspection, and certification market in consumer goods and retail industry?

The market is valued at USD 37.27 billion in 2026 and is set to climb to USD 49.48 billion by 2031.

Which region contributes the largest revenue?

Asia-Pacific accounts for 41.72% of 2025 revenue and is also the fastest-growing region with a 6.41% CAGR.

Which service category is growing the fastest?

Certification services, driven by ESG and sustainability verification, are projected to post a 6.28% CAGR through 2031.

Why are companies outsourcing testing functions?

Outsourcing offers capital efficiency, quicker scale-up, and access to accredited expertise across multiple jurisdictions.

How are sustainability rules shaping demand?

EU and U.S. mandates now require third-party verification of environmental and social claims, creating long-term recurring work for TIC providers.

What major challenge could limit market growth?

A shortage of specialized auditors and testers, particularly in food safety and cybersecurity, hampers providers’ ability to meet rising demand.

Page last updated on: