France Testing, Inspection, And Certification (TIC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

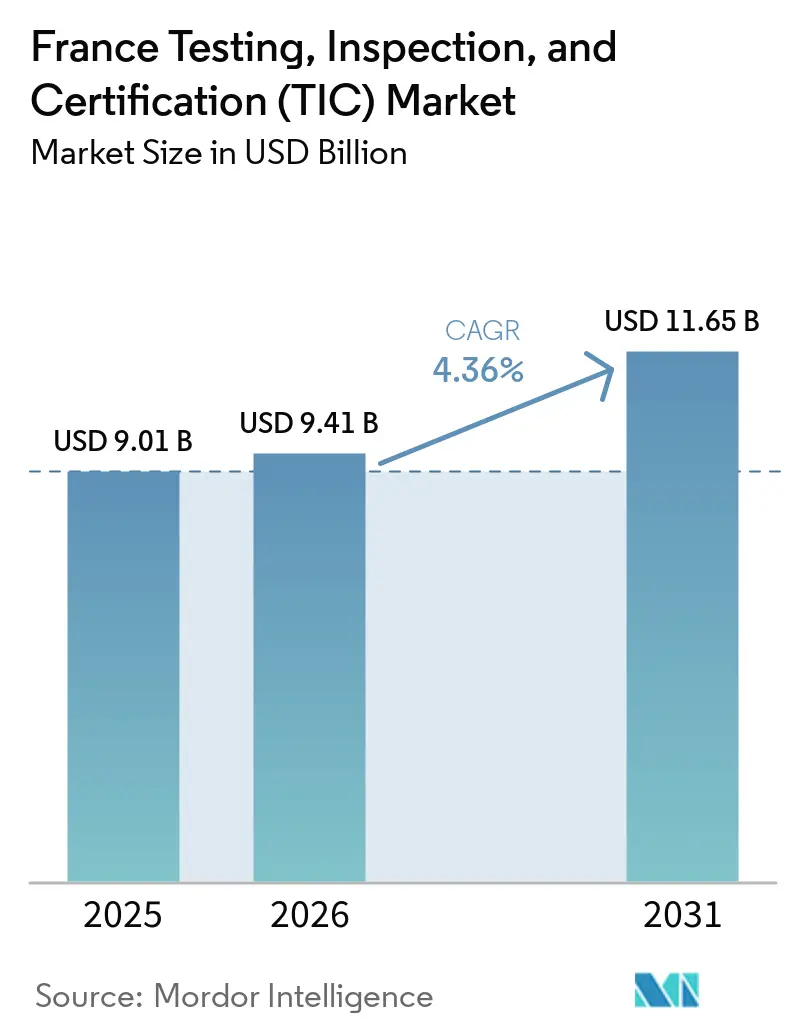

| Base Year Market Size (2025) | USD 9.01 Billion |

| Market Size (2026) | USD 9.41 Billion |

| Market Size (2031) | USD 11.65 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

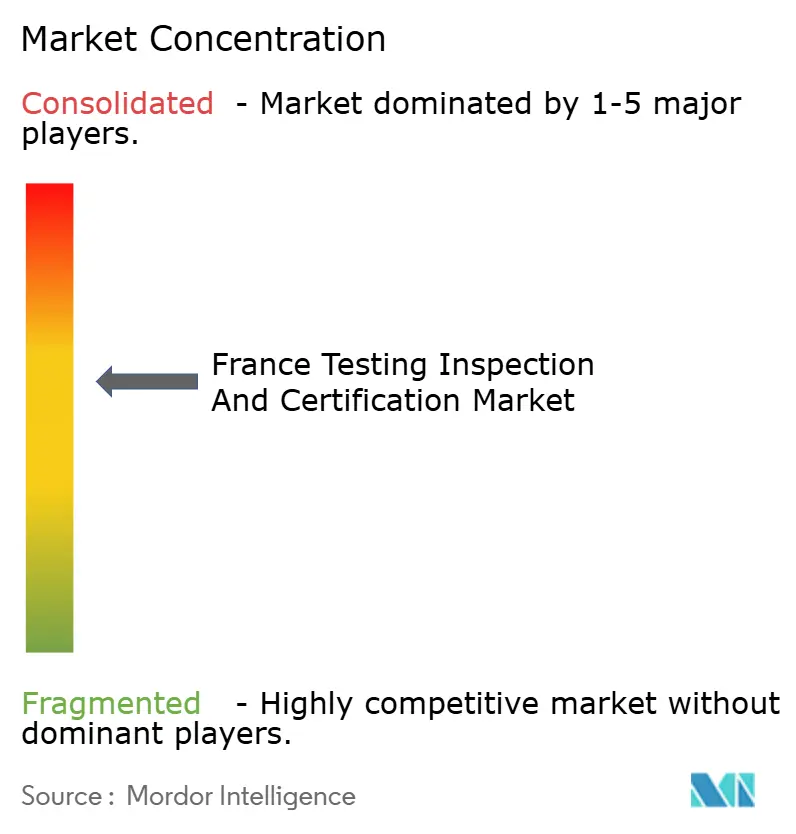

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Testing, Inspection, And Certification (TIC) Market Analysis by Mordor Intelligence

The France testing, inspection, and certification (TIC) market size is expected to increase from USD 9.01 billion in 2025 to USD 9.41 billion in 2026 and reach USD 11.65 billion by 2031, growing at a CAGR of 4.36% over 2026-2031. Solid demand stems from France’s role as the European Union’s second-largest economy, its leadership in nuclear energy and aerospace, and its fast-growing hydrogen and battery industries. Enterprises are consolidating compliance spending under multi-year frameworks that combine product safety, cybersecurity, and sustainability audits, which raises the average contract value and length. Digital inspection platforms delivered over private fifth-generation networks are compressing travel costs while preserving audit rigor, improving provider margins. Meanwhile, the European Commission’s March 2026 approval of a one-gigawatt hydrogen subsidy package underscores a pipeline of projects that will require continuous conformity assessment for at least the next decade.

Key Report Takeaways

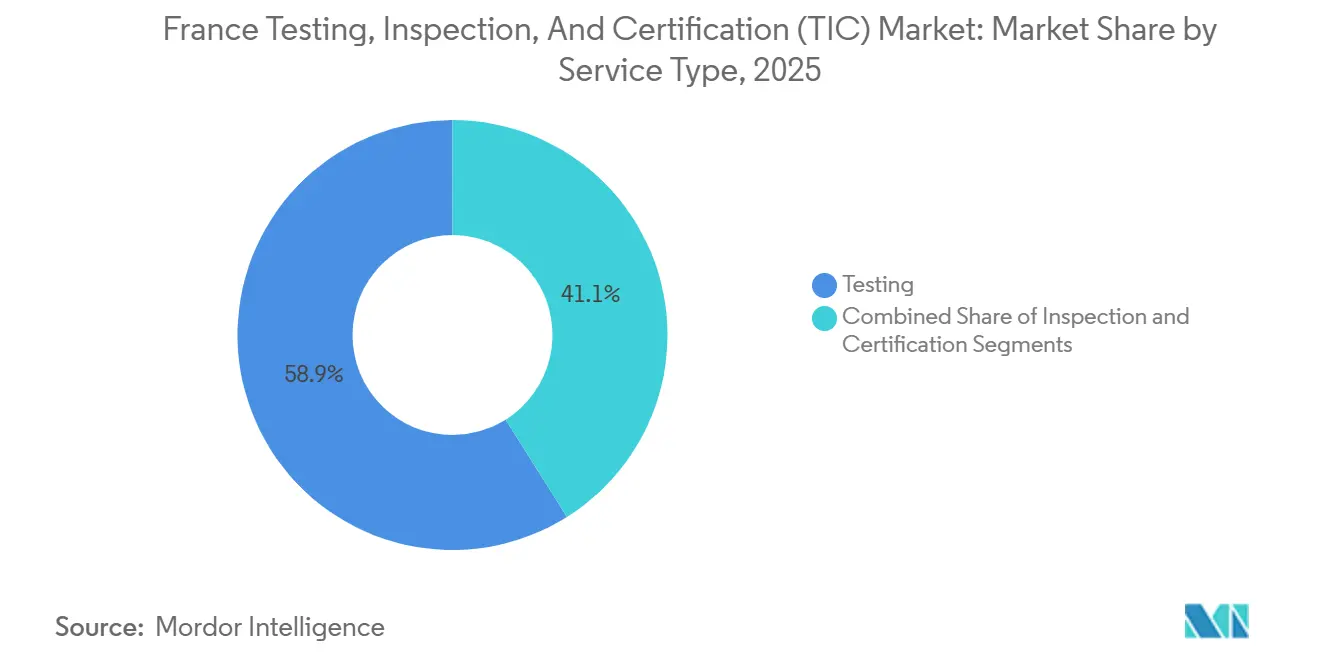

- By service type, testing led with 58.94% revenue share in 2025, whereas certification is projected to record the fastest 5.12% CAGR through 2031.

- By sourcing type, outsourced services held 64.31% of the France testing, inspection and, certification market share in 2025 and are forecast to expand at a 4.93% CAGR.

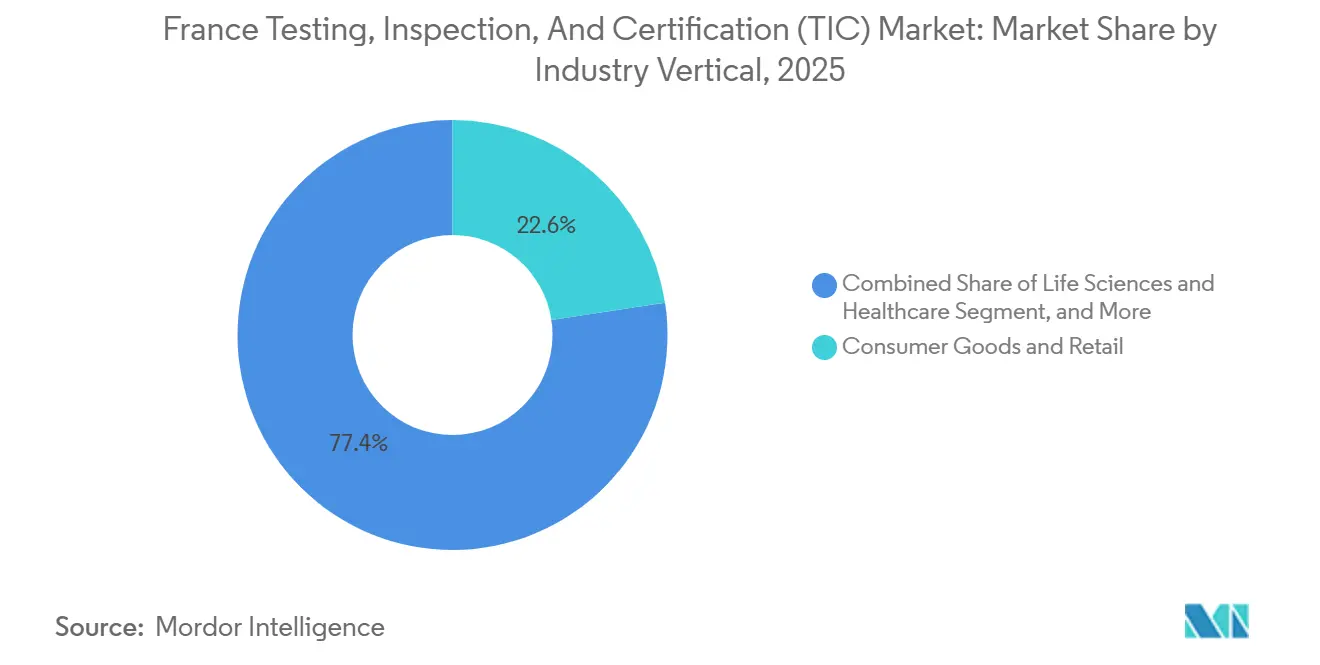

- By industry vertical, consumer goods and retail accounted for 22.60% of industry revenue in 2025, but life sciences and healthcare is set to grow fastest at a 5.44% CAGR.

- By delivery mode, on-site work represented 52.40% of 2025 revenue, yet remote and digital inspections are forecast to advance at a 5.94% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Testing, Inspection, And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory EU and French Regulatory Compliance Surge | +1.2% | National, concentrated in Île-de-France, Auvergne-Rhône-Alpes, Grand Est | Medium term (2-4 years) |

| Hydrogen and Battery Gigafactory Build-Out Needs | +0.9% | National, early focus in Hauts-de-France and Nouvelle-Aquitaine | Long term (≥ 4 years) |

| Sustainability and ESG Verification Demand | +0.8% | National, higher adoption in Paris, Lyon, Toulouse | Medium term (2-4 years) |

| Digital-Device Proliferation and Cybersecurity Testing | +0.7% | National, with EU cross-border e-commerce spillover | Short term (≤ 2 years) |

| Outsourcing of TIC Functions by Large Enterprises | +0.6% | National, led by automotive, aerospace, pharmaceuticals | Medium term (2-4 years) |

| 5G-Enabled Remote and Digital Inspections Adoption | +0.5% | National, pilots in rail, manufacturing, aerospace | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory EU And French Regulatory Compliance Surge

The Network and Information Security Directive 2, which took effect in October 2024, obliges more than 10,000 French organizations to commission periodic cybersecurity audits, with fines tied to global turnover for non-compliance. The Cyber Resilience Act extends third-party CE-mark assessments to connected products from September 2026, creating a two-year capacity-build window for laboratories. National alignment efforts, such as ANSSI’s ReCyF framework, have standardized audit checklists, accelerating accreditation of inspection bodies.[1]ANSSI, “ReCyF Framework 2024,” ssi.gouv.fr Parallel obligations under the Corporate Sustainability Reporting Directive require limited assurance for large firms by 2026 and reasonable assurance by 2028, driving integrated audit contracts that bundle product safety, cybersecurity, and ESG verification. Together, these rules sustain high recurring revenue for providers able to deliver multidisciplinary programs.

Hydrogen and Battery Gigafactory Build-Out Needs

Verkor’s EUR 1.5 billion (USD 1.73 billion) Dunkirk battery plant, inaugurated in December 2025, illustrates the recurring laboratory workload attached to electrode quality, electrolyte purity, and thermal-runaway testing. Lhyfe’s RFNBO certification in May 2025 shows how third-party attestations unlock multi-year production subsidies. The European Commission’s March 2026 green-hydrogen scheme foresees several 200 megawatt electrolyzers, each demanding ISO 17025-accredited analyses of hydrogen purity, pressure-vessel integrity, and grid-connection safety.[2]European Parliament, “Corporate Sustainability Reporting Directive,” europarl.europa.eu Both battery and hydrogen facilities require periodic re-certification as EU technical standards tighten, guaranteeing a durable pipeline for conformity services.

Sustainability and ESG Verification Demand

The Corporate Sustainability Reporting Directive, even after the Omnibus I threshold increase, still captures roughly 500 large French firms that must secure assurance on greenhouse-gas inventories and supply-chain risks. Many also fall under the older Duty of Vigilance Law, amplifying disclosure depth. Testing majors such as Bureau Veritas and SGS have launched dedicated practices combining ISO 14064 emissions checks, Science Based Targets validation, and TCFD alignment reviews, positioning these services as annual engagements. The 2028 shift from limited to reasonable assurance elevates the rigor to financial-audit level, compelling providers to hire chartered accountants and environmental scientists while investing in analytics platforms that can trace emissions far into tier-three supply chains.

Digital-Device Proliferation and Cybersecurity Testing

Connected equipment, from industrial PLCs to consumer smart-home devices, enters a new regulatory era once the Cyber Resilience Act mandates CE-mark conformity by December 2027. Manufacturers must submit products for penetration tests, firmware update validation, and cryptographic key audits. Factory deployments such as Schneider Electric’s fifth-generation network in Vaudreuil create thousands of industrial devices that will trigger repeat re-certification with every significant firmware patch. The act’s 24-hour incident-reporting rule further fuels demand for continuous monitoring services that blend testing with threat intelligence, a capability still scarce among French laboratories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Accredited Labs and Skilled Auditors | -0.4% | National, acute in cybersecurity, ESG, hydrogen | Medium term (2-4 years) |

| SME Price-Sensitivity to Premium TIC Fees | -0.3% | National, strong in food and beverage, textiles | Short term (≤ 2 years) |

| Patch-Work Local Environmental Rules | -0.2% | Paris, Lyon, Marseille, Toulouse, Bordeaux, Strasbourg | Short term (≤ 2 years) |

| Strategic Sector Protectionism Delaying Approvals | -0.1% | Defense, critical infrastructure, dual-use tech | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Accredited Labs and Skilled Auditors

COFRAC’s December 2024 LAB REF 08 revision lengthened accreditation cycles to as much as 24 months, coinciding with surging demand for hydrogen purity, battery safety, and cybersecurity penetration tests.[3]COFRAC, “LAB REF 08 Revision,” cofrac.fr Labor supply grows only 3% annually, versus 5-6% demand growth. Dekra’s plan to recruit 1,000 inspectors in France highlights the talent gap, while new programs such as the 2026 biobank accreditation stretch surveillance teams thinner. Universities have yet to scale curricula in ESG assurance or IoT security, forcing providers to poach staff or fund multi-year apprenticeships that delay capacity relief.

SME Price-Sensitivity to Premium TIC Fees

Mandatory certifications often cost EUR 10,000-25,000 (USD 11,600-29,000) per cycle, a heavy burden for the small businesses that make up 99% of French firms. While electric-vehicle purchase incentives help consumers, they do not offset the laboratory fees that component suppliers face for battery safety or electromagnetic compatibility tests. Fragmented low-emission-zone rules multiply audit costs for logistics operators who must certify fleets across 42 jurisdictions. Unable to match the economies of scale of global majors, some small labs charge higher prices, encouraging SMEs either to delay certification or resort to low-quality alternatives that raise enforcement risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Momentum Under Wide-Ranging Attestation Mandates

Testing dominated the France testing, inspection, and certification market with 58.94% revenue in 2025, anchored by laboratory-intensive fields such as pharmaceuticals and food safety. Certification, however, is poised for the strongest 5.12% CAGR because the Cyber Resilience Act, NIS2, and the Corporate Sustainability Reporting Directive all stipulate third-party attestations that in-house labs cannot deliver. The France TIC market size for certification is therefore set to expand steadily through 2031. Providers able to combine pre-market tests with post-market surveillance inside a single audit package are winning multi-year contracts, evidencing how regulation converts certification from a cost center into a revenue enabler.

Testing remains indispensable where high-frequency sampling or destructive assays are mandatory, yet its growth is steadier. Inspection services fill the middle ground by supporting asset-integrity programs in energy, elevators and construction. The emerging France TIC market share for hybrid solutions that blend all three services underpins the sector’s long-run stability.

By Sourcing Type: Outsourcing Rises as Firms Shed Non-Core Compliance Work

Outsourced contracts held 64.31% share in 2025 and are forecast to climb at a 4.93% CAGR, the fastest in this segmentation. Tightened COFRAC scope-management rules have raised the fixed cost of maintaining in-house ISO 17025 accreditation, prompting even large manufacturers to shift routine audits outside. The France testing, inspection, and certification (TIC) market size captured by external providers therefore widens each year as accredited majors spread compliance overhead across hundreds of clients.

In-house teams persist only for proprietary or classified work, such as aerospace failure analysis or pharmaceutical formulation studies. Yet even these actors outsource periodic legal audits to reduce payroll costs. Private five-generation networks enable remote verification, shrinking the advantage once held by resident inspectors. Over the forecast horizon, the France TIC market share of in-house services is expected to erode incrementally.

By Industry Vertical: Life Sciences Sets the Pace Under Faster Trial Timelines

Consumer goods and retail generated 22.60% of 2025 revenue, but life sciences and healthcare are on track for the quickest 5.44% CAGR thanks to the French medicines agency’s 14-day fast-track clinical-trial authorization. The France testing, inspection, and certification market size attached to investigational medicinal products will therefore grow faster than any other vertical. Automotive demand is shifting from internal-combustion testing toward battery thermal-abuse, electromagnetic-compatibility, and low-emission-zone certifications, creating a mixed outlook.

Aerospace and defense remain steady buyers because Airbus and the defense procurement agency insist on domestic laboratories for dual-use technologies. Energy and utilities add new volume from offshore wind and hydrogen projects, while construction sees rising traction for SOCOTEC’s BIM-based certifications that underpin public-works tenders. Overall, diversified industrial demand underpins resilience even when individual sectors cycle.

By Mode Of Service Delivery: Remote and Digital Methods Accelerate on A 5G Backbone

On-site work still commanded 52.40% of 2025 revenue, yet remote and digital inspections are forecast to log the top 5.94% CAGR. Fifth-generation networks, augmented-reality headsets, and drone imaging allow specialists to evaluate assets without the travel time, supporting France's testing, inspection and certification market share gains for digital models. Railway, aerospace, and manufacturing pilots show that hybrid models can satisfy regulators while lowering carbon footprints.

While laboratories continue to conduct destructive chemical and mechanical tests, digital portals now enable clients to monitor sample progress in real time. As time progresses, data-rich digital twins will facilitate predictive analyses, transitioning inspections from a calendar-based to a condition-based schedule, thereby altering the revenue mix. Additionally, the integration of these technologies is likely to drive innovation in testing methodologies.

Geography Analysis

Île-de-France, Auvergne-Rhône-Alpes, and Grand Est form the core compliance corridors because they concentrate pharmaceuticals, chemicals, automotive assembly, and logistics hubs. Low-emission zones across 42 cities, including Paris and Lyon, triggered a wave of vehicle retrofit and emissions certifications once 41% of the national fleet fell under road restrictions in 2025. Paris alone fines non-compliant light vehicles EUR 68 (USD 79) per breach, spurring immediate certification demand.

Hauts-de-France is emerging as a battery and hydrogen testing center after Verkor’s 16 gigawatt-hour Dunkirk gigafactory launch. Nouvelle-Aquitaine hosts France’s first RFNBO-certified hydrogen plant and is expected to attract more electrolysis projects. Occitanie benefits from Airbus and Safran supply chains that require non-destructive tests and supplier audits, while Provence-Alpes-Côte d’Azur leverages cosmetics clusters demanding GMP certifications.

Remote inspection technology is flattening historical geographic advantages. A Lyon laboratory can now guide an augmented-reality drone over a Brittany wind farm, narrowing location premiums. Nevertheless, proximity still matters for sampling that cannot be shipped, such as hazardous-materials testing, so regional specialization endures.

Competitive Landscape

The market shows moderate concentration: the top five providers, Bureau Veritas, SGS, Apave, SOCOTEC, and Eurofins, capture roughly 45-50% of revenue. Bureau Veritas deepened its domestic lead by absorbing Apave’s EUR 1.3 billion (USD 1.37 billion) portfolio and 11,000 staff in early 2025. Clients value a one-stop partner that can handle vehicle inspections, building controls, and nuclear audits under a unified contract.

Specialists such as SOCOTEC and Kiwa France compete by digitizing workflows. SOCOTEC’s three-year BIM Model in Use certification helps construction firms win ESG-weighted public bids. Intertek France extended ISO 17025 coverage in March 2026 to textile durability tests that let fashion brands cut eco-modulation fees. Bureau Veritas completed the Horizon Europe DiGiChecks project in May 2025, adding predictive maintenance algorithms that link sensor data to audit schedules.

White-space opportunities lie in hydrogen-purity analysis and cybersecurity penetration testing, where current capacity covers only a fraction of the demand implied by the Cyber Resilience Act’s 2027 deadline. COFRAC’s 2026 biobank accreditation program additionally opens a medical testing niche, although its stringent traceability rules set a high entry bar.

France Testing, Inspection, And Certification (TIC) Industry Leaders

Bureau Veritas SA

SGS France SAS

Apave SA

Dekra SE France

Eurofins Scientific SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Intertek France gained COFRAC accreditation for Refashion eco-modulation textile durability tests, helping brands meet circular-economy rules.

- March 2026: The European Commission cleared France’s EUR 797 million (USD 922.2 million) green-hydrogen scheme, guaranteeing 15-year production subsidies that hinge on RFNBO certification.

- March 2026: ANSM launched a 14-day fast-track clinical-trial authorization, slashing the previous 31-day window.

- December 2025: Verkor inaugurated a EUR 1.5 billion (USD 1.73 billion) Dunkirk battery gigafactory with 16 gigawatt-hours annual capacity.

France Testing, Inspection, And Certification (TIC) Market Report Scope

The France Testing, Inspection, and Certification (TIC) Market refers to the global industry that provides services ensuring products, systems, and processes meet regulatory standards, quality benchmarks, and safety requirements across diverse sectors such as manufacturing, healthcare, automotive, energy, consumer goods, and construction.

The France Testing, Inspection, and Certification (TIC) Market Report is Segmented by Service Type (Testing, Inspection, Certification), Sourcing Type (In-house, Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Automotive and Transportation, Aerospace and Defense, Oil Gas and Petrochemicals, Energy and Utilities, Industrial Manufacturing and Machinery, Chemicals and Materials, Construction and Infrastructure, Life Sciences and Healthcare, Food Agriculture and Beverage, Others), and Mode of Service Delivery (On-site, Off-site Laboratory, Remote Digital). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others Industry Verticals |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others Industry Verticals | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

What is the current France testing, inspection, and certification (TIC) market size and its expected growth?

The market stands at USD 9.41 billion in 2026 and is projected to reach USD 11.65 billion by 2031, reflecting a 4.36% CAGR over 2026-2031.

Which service type is growing fastest in France?

Certification services are forecast to post the strongest 5.12% CAGR through 2031 because European regulations increasingly require third-party attestations.

Why are life sciences audits expanding rapidly?

A new 14-day fast-track clinical-trial authorization introduced by ANSM in 2026 accelerates product development, lifting demand for laboratory tests and Good Clinical Practice inspections.

How is remote inspection affecting service delivery models?

Fifth-generation networks, drones and augmented-reality headsets allow inspectors to verify assets without traveling, pushing remote and digital methods toward a 5.94% CAGR.

Which regions inside France generate the most compliance demand?

Île-de-France, Auvergne-Rhône-Alpes and Grand Est dominate due to dense pharmaceutical, chemical and automotive clusters, while Hauts-de-France is rising on battery and hydrogen projects.

Who are the leading companies in the French TIC space?

Bureau Veritas, SGS, SOCOTEC, Eurofins and Apave together capture roughly half of the market, with digital capabilities emerging as the next differentiation lever.

Page last updated on: