Brazil Testing Inspection and Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

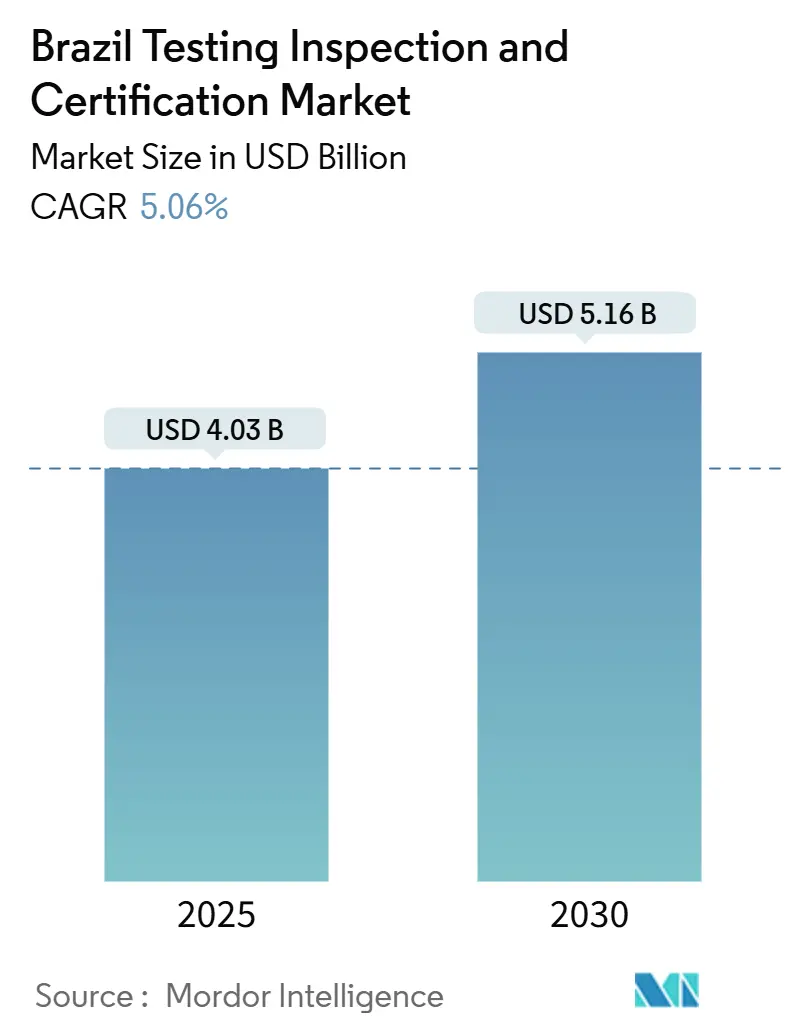

| Market Size (2025) | USD 4.03 Billion |

| Market Size (2030) | USD 5.16 Billion |

| Growth Rate (2025 - 2030) | 5.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Testing Inspection and Certification Market Analysis by Mordor Intelligence

The Brazil testing, inspection, and certification market size reached USD 4.03 billion in 2025 and is forecast to climb to USD 5.16 billion by 2030, expanding at a 5.06% CAGR. The Brazil testing, inspection, and certification market benefits from non-deferrable compliance mandates issued by ANVISA, INMETRO, and MAPA, which anchor spending even in cyclical downturns. Mandatory testing for offshore energy equipment, rising ESG disclosure needs, and expanding export certification programs collectively underpin the Brazil testing, inspection, and certification market’s resilience. Leading multinationals are accelerating digital inspection roll-outs, further stimulating high-value remote monitoring contracts. Simultaneously, INMETRO’s ongoing deregulation plan will simplify conformity assessments, supporting faster accreditation cycles and reducing service bottlenecks across the Brazil testing, inspection, and certification market.

Key Report Takeaways

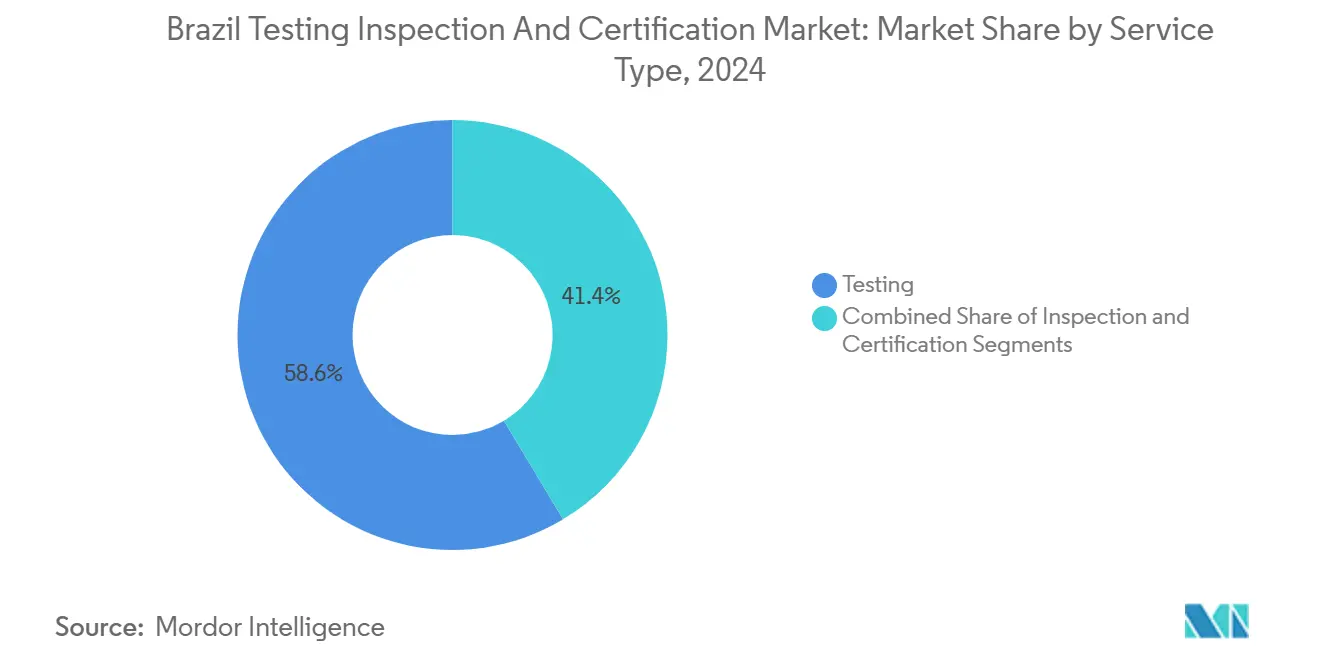

- By service type, Testing commanded 58.6% of the Brazil testing, inspection, and certification market share in 2024; Certification is projected to rise at a 5.8% CAGR through 2030.

- By sourcing type, outsourced activities captured 63.2% of the Brazil testing, inspection, and certification market size in 2024, while both outsourced and in-house solutions are forecast to expand uniformly at a 5.5% CAGR to 2030.

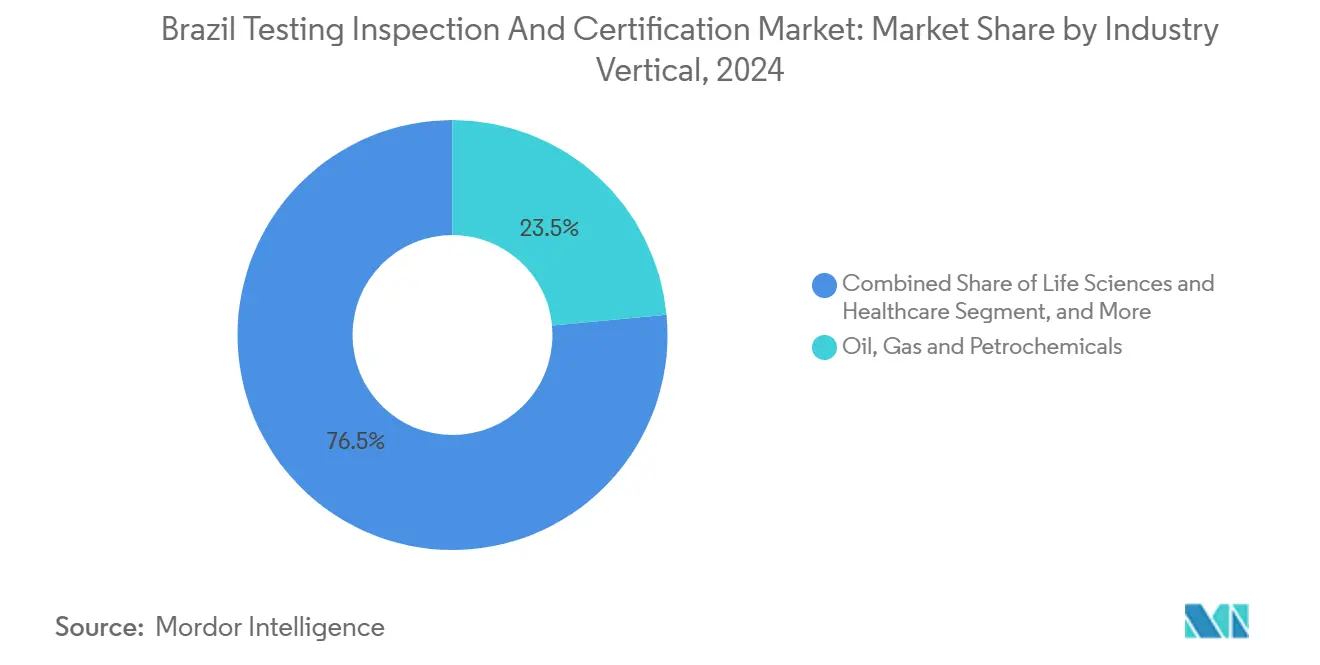

- By industry vertical, Oil, Gas, and Petrochemicals led with a 23.5% revenue share of the Brazil testing, inspection, and certification market in 2024; Life Sciences and Healthcare are advancing at a 6.2% CAGR through 2030.

- By mode of delivery, On-site services accounted for 47.1% of the Brazil testing, inspection, and certification market size in 2024, whereas Remote and Digital offerings are registering the fastest 6.4% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Testing Inspection and Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent enforcement of ANVISA, INMETRO and MAPA quality regulations | +1.2% | National, São Paulo and Rio de Janeiro industrial centers | Medium term (2-4 years) |

| Booming agrifood exports driving certification demand | +0.9% | Mato Grosso, Rio Grande do Sul, Paraná | Long term (≥ 4 years) |

| Accelerated industrial digitalisation and Industry 4.0 roll-outs | +0.8% | São Paulo, Santa Catarina, Rio Grande do Sul | Medium term (2-4 years) |

| ESG-linked financing mandating third-party audits | +0.7% | National, early adoption in multinational subsidiaries | Short term (≤ 2 years) |

| Remote inspection for Amazon-basin assets via drones and digital twins | +0.4% | Amazon region, offshore platforms | Long term (≥ 4 years) |

| EU anti-deforestation regulation boosting traceability tests on soy and beef | +0.6% | Cerrado and Amazon agricultural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Enforcement of ANVISA, INMETRO and MAPA Quality Regulations

Brazilian regulators have stepped up on-site audits, import checks and post-market surveillance, sharply increasing demand for accredited laboratories and inspection bodies. ANVISA broadened oversight of medical device shipments, while INMETRO is digitalising 72 normative acts to reduce paperwork and speed conformity approvals. MAPA now requires comprehensive pesticide residue and microbiological testing for agrifood exports, further expanding workload across the Brazil testing inspection and certification market. The combined effect is a predictable pipeline of verification projects that shields service providers from macroeconomic volatility. Strict adoption of IFRS S1 and S2 is also translating into new revenue streams for environmental assurance and greenhouse-gas inventory validation.

Booming Agrifood Exports Driving Certification Demand

Record soy and beef shipments have triggered an unprecedented volume of Halal, organic and traceability certifications. SGS invested in a 1,200 m² grain and food testing hub in São Bernardo do Campo that guarantees three-day turnaround to alleviate bottlenecks at Santos port. Buyers in Europe and Asia now insist on multi-parameter test reports covering pesticide residues, GMO status and nutritional profiles, raising the testing intensity per export container. Laboratories offering integrated chem-microbiology workflows win larger contracts as exporters consolidate supplier lists to meet ship-schedule constraints.

Accelerated Industrial Digitalisation and Industry 4.0 Roll-outs

Government-backed MetaIndústria centers in São Caetano do Sul and São Leopoldo advise manufacturers on sensor networks, robotics and digital twins, all of which introduce new conformity checkpoints. Safety assessments for interconnected machinery, functional safety audits, and cybersecurity certifications are now baseline requirements in automotive and aerospace tenders. Demand is rising for validation of twin-simulation fidelity and data-integrity testing, giving niche cyber-physical labs a growth runway inside the Brazil testing inspection and certification market.

ESG-linked Financing Mandating Third-party Audits

Banks and investors increasingly attach interest-rate step-ups or covenants to greenhouse-gas reduction targets, compelling companies to seek independent assurance for scope 1-3 emissions. The new IFRS mandate has fast-tracked a surge in verification orders, particularly from mining, agriculture and energy clients exposed to climate-related scrutiny. As Brazil’s voluntary carbon-credit framework matures, accredited verifiers stand to secure recurring revenue through baseline measurement, offset validation and periodic monitoring engagements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on federal accreditation lead-times | -0.8% | National, CGCRE-accredited labs | Medium term (2-4 years) |

| Shortage of qualified lab technicians in tier-2 cities | -0.6% | Interior cities outside São Paulo-Rio corridor | Long term (≥ 4 years) |

| Exchange-rate volatility squeezing price competitiveness | -0.4% | National | Short term (≤ 2 years) |

| Limited local battery-testing capacity delaying EV programmes | -0.3% | Automotive manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on Federal Accreditation Lead-times

A new laboratory scope can wait up to 18 months for CGCRE approval, tying up capital and keeping idle equipment on the books. Slow approvals weigh especially on emerging fields such as battery safety or PFAS analysis, where foreign standards evolve quickly. INMETRO’s digital reforms promise relief, yet the timeline for full rollout is still unclear.

Shortage of Qualified Lab Technicians in Tier-2 Cities

Interior hubs that host booming agrifood and mining activity face acute staff shortages, forcing samples to travel hundreds of kilometers to São Paulo or Rio laboratories.[1]Revista Fator MT, “Economia – Revista Fator MT,” fatormt.com.br Longer logistics chains inflate costs and extend lead times, pressuring exporters working beneath tight shipping windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type – Testing Maintains Volume Leadership While Certification Accelerates

Testing activities generated 58.6% of 2024 revenue in the Brazil testing inspection and certification market, reflecting mandatory analysis for oil platforms, consumer goods and construction materials. Inspection followed, bolstered by infrastructure modernization projects. Certification, albeit smaller, grew 5.8% CAGR and is poised for stronger traction as ESG auditing and ISO credentials become compulsory for supply chain entry. The Brazil testing inspection and certification market size for Certification is projected to rise in tandem with capital-market disclosure rules and international buyer standards. Global majors are reinforcing competencies through targeted takeovers; SGS’s 2024 purchase of cybersecurity firm CertX highlights the pivot toward high-value assurance niches.

Despite Testing’s scale, rising automation may taper its growth, whereas Certification’s advisory nature shields it from commoditization. Integrated providers that can bundle material analysis with management-system sign-offs are gaining share among exporters needing a one-stop solution. Over the forecast, hybrid contracts that combine real-time sensor data analysis with periodic certificate renewals are expected to redefine service packages across the Brazil testing inspection and certification market.

By Sourcing Type – Outsourcing Captures Cost-Sensitive Demand

External providers delivered 63.2% of 2024 turnover, underscoring companies’ preference to avoid capex-dense labs and accreditation overheads. The Brazil testing inspection and certification market sees outsourcing as a hedge against technical obsolescence, where rapid standard updates can render in-house instruments outdated. Yet large oil majors and aerospace OEMs retain core metallurgical and destructive testing bays for proprietary components, limiting full outsourcing penetration. Both outsourced and in-house revenue pools are forecast to climb 5.5% CAGR, indicating demand stems from higher test frequency rather than vendor churn.

Contractors are diversifying into managed data services, offering dashboards that transform raw results into compliance narratives, a value proposition resonating with mid-market exporters. Conversely, small chemical labs leverage niche in-house protocols to preserve intellectual-property secrecy. This balance suggests the Brazil testing inspection and certification market has approached a mature sourcing equilibrium built on technical specialization rather than blanket make-or-buy mandates.

By Industry Vertical – Energy Leads, Healthcare Surges

Oil, Gas and Petrochemicals held a 23.5% slice of 2024 sales in the Brazil testing inspection and certification market, driven by Petrobras’s subsea integrity checks. Inspection frequencies remain high due to stringent environmental stipulations around pre-salt assets. The Brazil testing inspection and certification market size for Life Sciences and Healthcare, however, is set to expand fastest as hospitals and device importers modernize labs post-pandemic. ANVISA’s tighter surveillance on implantable devices and pharma-grade APIs underpins this trajectory.

Agrifood, consumer goods and ICT segments also inject momentum through traceability testing, EMC measurements and cybersecurity audits. Meanwhile, battery certification is emerging within automotive verticals, and metals and minerals analysis is poised for uplift as EV supply-chain localization gains pace. Providers who master sector-specific protocols stand to secure recurring engagements that anchor regional revenue bases in the Brazil testing inspection and certification market.

By Mode of Service Delivery – Digital Adoption Gains Speed

On-site inspections accounted for 47.1% of 2024 revenue because regulatory statutes require physical presence during pressure-vessel or pipeline examinations. Off-site labs continue to thrive for high-precision assays using spectrometry and chromatography. The Brazil testing inspection and certification market shows the Remote and Digital segment advancing at a 6.4% CAGR, fueled by drone imagery, satellite feeds and digital twin dashboards that track asset health in real time.

Remote technologies reduce safety risks and logistics costs in the Amazon basin where river transport is seasonal. However, certifiers must still validate sensor calibration through periodic field cross-checks, ensuring on-site teams remain integral. As artificial-intelligence algorithms sharpen anomaly detection, remote offerings will capture incremental spend, but multi-modality packages combining lab, field and cloud analytics will dominate contract structures across the Brazil testing inspection and certification market.

Geography Analysis

The Sao Paulo-Rio de Janeiro corridor generated roughly 60% of the Brazil testing, inspection, and certification market’s value in 2024, capitalizing on dense industrial clusters, port infrastructure, and concentrated technical talent. São Paulo’s automotive, pharmaceutical, and electronics hubs rely heavily on metallurgical and EMC testing, maintaining a steady cadence of verification projects. Rio de Janeiro’s role as energy capital sustains demand for corrosion monitoring and subsea equipment certification tied to Petrobras’s platform upkeep.[2]SGS, “Acquisitions,” sgs.com

Southern states Rio Grande do Sul, Santa Catarina, and Paraná form the fastest-growing belt, recording about 6.8% CAGR as agro-processing expands to meet EU traceability mandates. Embrapa’s lab modernization in Rio Grande do Sul exemplifies public investment unlocking regional capability; new UHPLC systems and automated extraction lines support pesticide and antibiotic residue testing critical for premium beef exports. Local providers capturing agrifood volumes are embedding rapid microbiology platforms to shorten ship-ready cycles at Paranaguá port, thereby enlarging the Brazil testing, inspection, and certification market footprint outside the Southeast.

Competitive Landscape

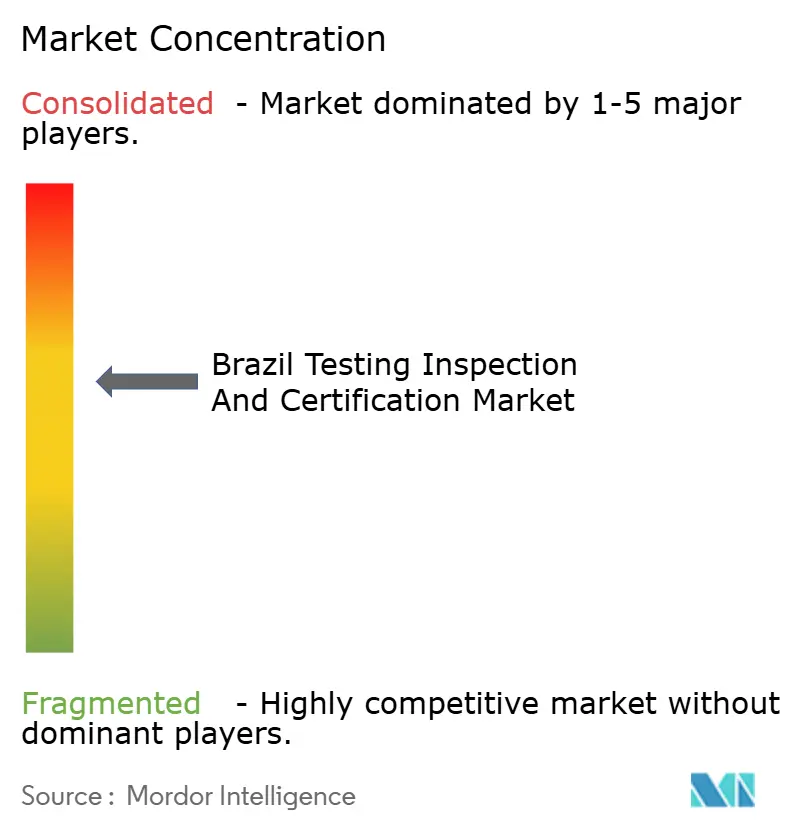

The Brazil testing, inspection, and certification market is moderately concentrated. Bureau Veritas, SGS, Intertek, and TÜV Rheinland jointly command a significant share of national revenue, while more than 200 licensed entities divide the remainder. A proposed USD 33 billion merger between Bureau Veritas and SGS could create a dominant 15-20% share player, subject to CADE scrutiny. Technology capabilities form the new competitive high ground: SGS’s acquisitions of RTI Laboratories for PFAS analytics and Aster Global for greenhouse-gas validation illustrate moves to pre-empt emerging compliance needs.[3]SGS, “Acquisitions,” sgs.com

Local independents defend positions via deep regulatory familiarity and quick-turn services. ASR Laboratory, for instance, specializes in soybean DNA testing with sample-to-result times under 24 hours, catering to exporters who must meet EU anti-deforestation rules. Foreign entrants usually partner with regional labs for accreditation coverage, illustrating that a trusted local presence remains pivotal in the Brazil testing, inspection, and certification market.

Digitalization reshapes rivalry; players embedding IoT sensor arrays and blockchain traceability into service bundles differentiate themselves on data transparency and audit readiness. Providers that integrate asset-health dashboards with predictive analytics not only lock in multi-year support contracts but also sidestep price-centric competition. As battery testing and cybersecurity certification mature, expect niche labs to become acquisition targets, accelerating consolidation and possibly nudging the Brazil testing, inspection, and certification market toward higher concentration ratios by decade-end.

Brazil Testing Inspection and Certification Industry Leaders

Bureau Veritas S.A.

SGS S.A.

Intertek Group plc

TÜV SÜD AG

DNV AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Embrapa Pecuária Sul secured Novo PAC funds to upgrade UHPLC and spectrophotometry assets, boosting agrifood testing throughput

- March 2025: Bureau Veritas purchased GeoAssay, broadening metals analytics capacity and signaling intent to expand into Brazilian mining basins.

- February 2025: SGS acquired RTI Laboratories and Aster Global, adding PFAS and carbon-credit validation skills to its Brazilian portfolio

- January 2025: Bureau Veritas and SGS confirmed merger talks aimed at a USD 33 billion combine, potentially reshaping the global and Brazil TIC market.

Brazil Testing Inspection and Certification Market Report Scope

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| Service Type | Testing |

| Inspection | |

| Certification | |

| Sourcing Type | In-house |

| Outsourced | |

| Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

How large is the Brazil testing inspection and certification market in 2025?

The Brazil testing inspection and certification market size stands at USD 4.03 billion in 2025 and is on track to reach USD 5.16 billion by 2030.

What is the expected growth rate for Brazil’s testing, inspection and certification providers?

Aggregate revenue is projected to climb at a 5.06% CAGR through 2030, supported by regulatory enforcement and export demand.

Which segment is expanding fastest inside Brazil’s conformity-assessment space?

Certification services, especially ESG-linked audits, are forecast to advance at a 5.8% CAGR, outpacing Testing and Inspection.

Why are outsourced TIC services popular among Brazilian manufacturers?

Outsourcing lets firms avoid capital-intensive labs and accreditation overheads while accessing specialized expertise for evolving standards.

Which region shows the quickest growth in TIC demand outside São Paulo?

Southern states such as Rio Grande do Sul are growing at roughly 6.8% CAGR, driven by agrifood traceability requirements and lab upgrades.

Page last updated on: