Saudi Arabia Testing Inspection and Certification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

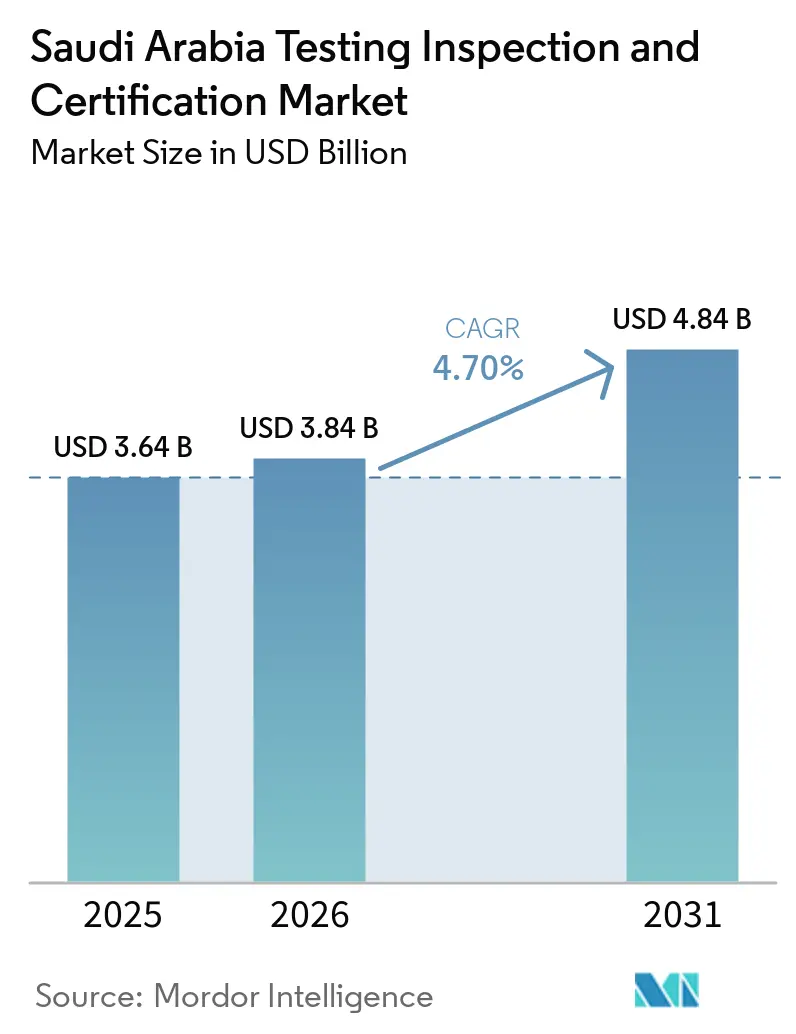

| Base Year Market Size (2025) | USD 3.64 Billion |

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 4.84 Billion |

| Growth Rate (2026 - 2031) | 4.70% CAGR |

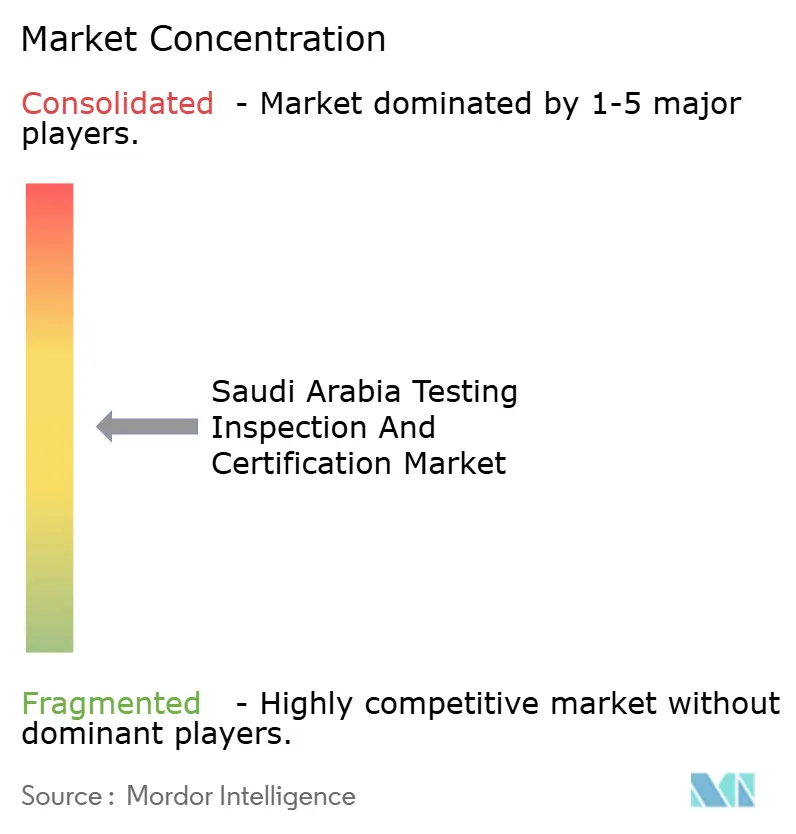

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Testing Inspection and Certification Market Analysis by Mordor Intelligence

The Saudi Arabia Testing Inspection And Certification Market size was valued at USD 3.64 billion in 2025 and is estimated to grow from USD 3.84 billion in 2026 to reach USD 4.84 billion by 2031, at a CAGR of 4.70% during the forecast period (2026-2031).

Vision 2030’s sweeping industrial policies, SASO’s tighter import rules, and an unprecedented pipeline of giga-projects are together pushing demand for comprehensive testing, inspection, and certification across factories, energy assets, and smart-city construction sites. Rising foreign investment, the rapid rollout of digital inspection tools, and increased adoption of international standards are further expanding addressable opportunities for providers that hold local accreditation and domain expertise. At the same time, supply constraints in accredited laboratories, overlapping approval pathways, and Saudization quotas weigh on service capacity and add cost pressures. Competitive advantage increasingly favors firms able to combine global technical depth with Saudi-based talent, automated testing equipment, and end-to-end conformity management platforms.

Key Report Takeaways

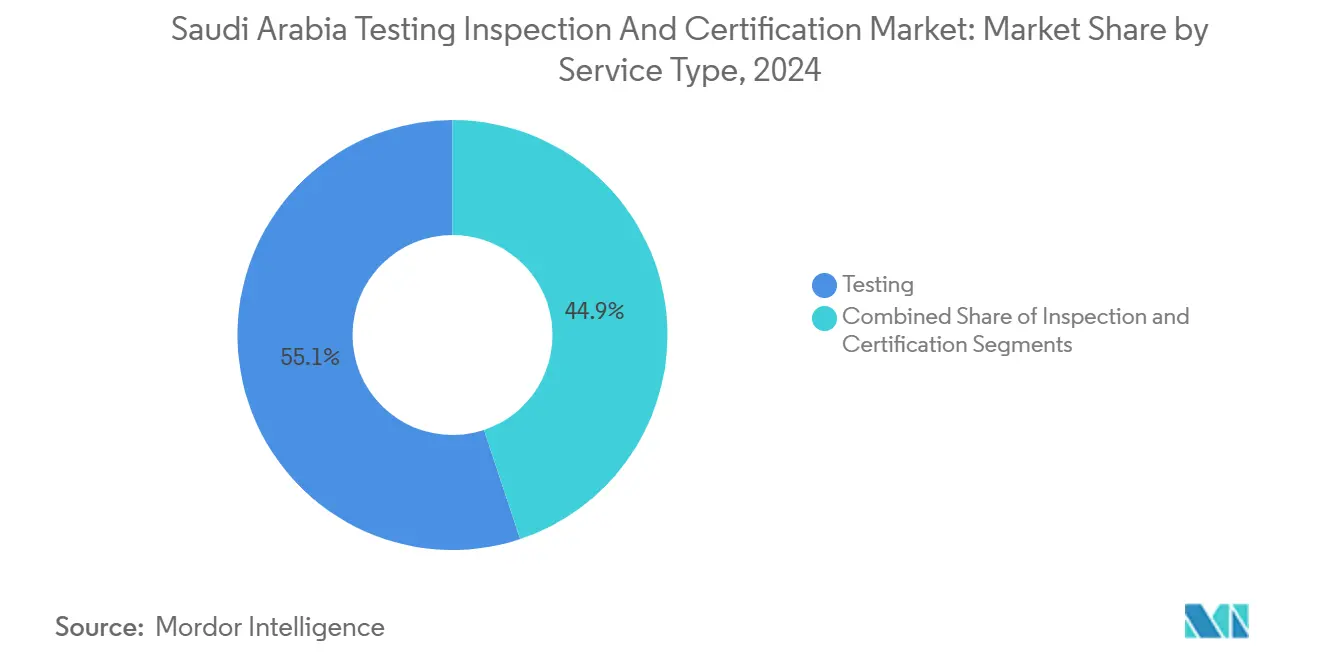

- By service type, testing captured 55.1% revenue share in 2024 while certification is advancing at a 5.5% CAGR through 2030.

- By sourcing type, outsourced services held 62.6% of the Saudi Arabia testing inspection and certification market share in 2024; the same segment is forecast to expand at a 5.1% CAGR.

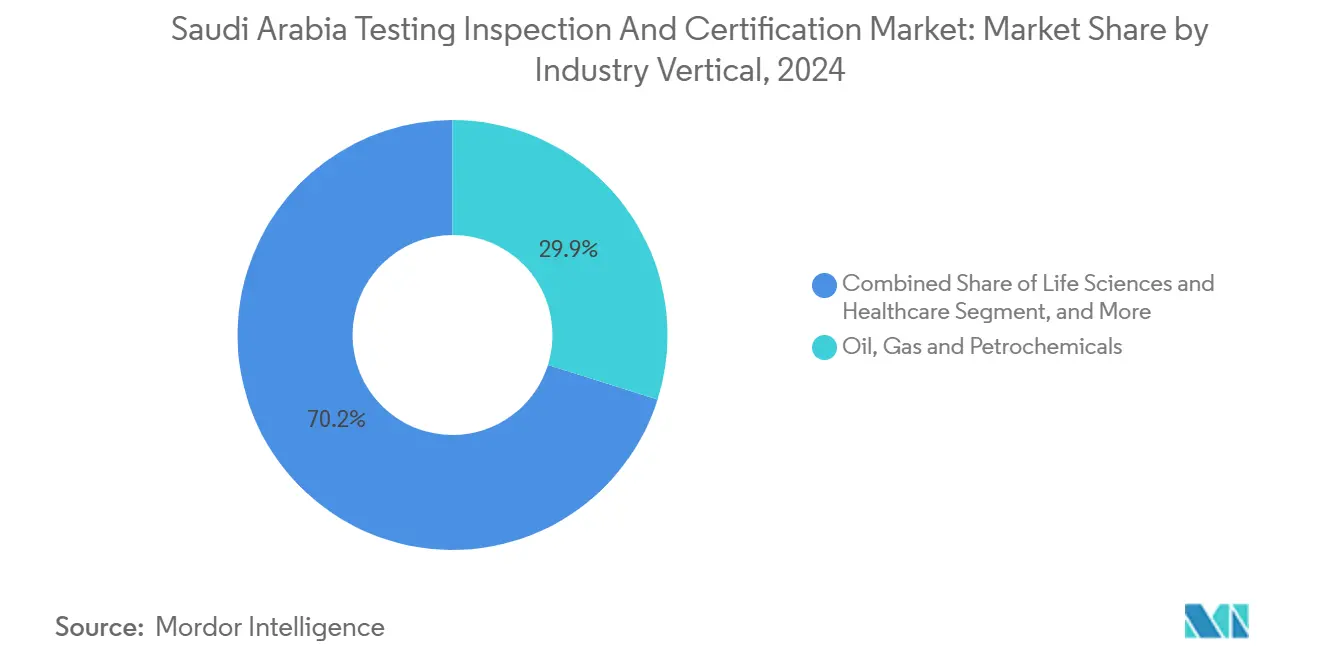

- By industry vertical, oil, gas, and petrochemicals led with 29.85% revenue share in 2024, whereas life sciences and healthcare is poised for the fastest 5.6% CAGR to 2030.

- By mode of service delivery, on-site solutions accounted for 51.2% of the Saudi Arabia testing inspection and certification market size in 2024, while remote and digital services register the highest 5.8% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Testing Inspection and Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrial diversification under Vision 2030 | +1.8% | Global | Medium term (2-4 years) |

| Stringent national product-safety regulations | +1.2% | Global | Short term (≤ 2 years) |

| Expanding FDI-backed manufacturing footprint | +0.9% | Riyadh, Eastern Province, Makkah | Medium term (2-4 years) |

| Oil and gas infrastructure modernisation cycle | +0.7% | Eastern Province, core spillover to other regions | Long term (≥ 4 years) |

| NEOM and giga-projects' digital inspection needs | +0.6% | NEOM, Red Sea, Qiddiya project sites | Long term (≥ 4 years) |

| Hydrogen pilot-plants requiring new certificates | +0.4% | NEOM Oxagon, industrial cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Industrial Diversification Under Vision 2030

Government programs such as the National Industrial Development and Logistics Program have issued 1,379 new factory licenses in 2023, representing SAR 81 billion (USD 21.6 billion) in committed investment.[1]Saudi Gazette, “Saudi factories post robust growth of 60% since launch of Vision 2030,” saudigazette.com.sa The policy goal of 36,000 factories by 2035 signals multi-year momentum for the Saudi Arabia testing inspection and certification market. New entrants in pharmaceuticals, advanced materials, and food processing must validate raw materials, manufacturing environments, and finished-goods performance before domestic sale or export. Large chemicals firms use initiatives like SABIC’s NUSANED to vet local suppliers, creating cascading demand for third-party audits at smaller workshops.[2]SABIC, “Toward Saudi Vision 2030: Driving Local Content,” sabic.com Export-oriented “Made in Saudi” labeling also requires accredited conformity certification to satisfy destination-market customs.

Stringent National Product-Safety Regulations

SASO’s dual-certificate mandate that took effect in January 2025 replaced Letters of Undertaking with compulsory Product and Shipment Certificates processed through the SABER platform. Parallel reforms at SFDA have aligned medical-device oversight with EU MDR, introducing risk-based classifications and heightened post-market surveillance.[3]Saudi Food and Drug Authority, “Overview – Medical Devices,” sfda.gov.sa Importers and domestic producers now face more extensive document reviews, factory audits, and technical testing, gaps that most small and mid-size firms cover by purchasing external testing inspection and certification services. Harmonization of SASO regulations with Gulf standards further pushes demand for multi-country accreditation capabilities.

Expanding FDI-Backed Manufacturing Footprint

Foreign direct investment into Saudi industry reached USD 738 million in Q2 2023, reflecting 23% year-over-year growth across 1,226 projects. International plants must prove local content contributions and worker-training commitments while still meeting global quality norms, which drives bundled inspection and certification contracts. Special Economic Zones offer tax incentives but enforce the same safety and environmental requirements, so newcomers continue to rely on third-party laboratories for commissioning tests. TIC workloads cluster around Riyadh, Jubail, and Jeddah, where most greenfield facilities break ground.

Oil and Gas Infrastructure Modernization Cycle

Saudi Aramco’s digital transformation program now deploys UAVs, subsea ROVs, laser-based methane detectors, and AI-enabled analytics to monitor pipelines and storage assets. Each new tool introduces sensors that must be validated for accuracy, cybersecurity, and hazardous-area compliance. Service demand extends to NDT of retrofitted wells, calibration of continuous emissions monitors, and certification of hydrogen-ready equipment at refinery upgrades. Longer-term projects within SABIC and smaller operators mirror these requirements, spreading advanced testing contracts across the broader hydrocarbon value chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory overlaps delaying approvals | -0.8% | Global | Short term (≤ 2 years) |

| Shortage of accredited local laboratories | -0.6% | National, with gaps in secondary cities | Medium term (2-4 years) |

| High price-sensitivity among SMEs | -0.5% | National, concentrated in emerging industrial areas | Short term (≤ 2 years) |

| Expat-inspector dependence vs Saudization quotas | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Overlaps Delaying Approvals

Projects often require separate permits from SASO, SFDA, and sector-specific ministries, leading to duplicated document reviews and sequential audits that extend lead times. SFDA’s 2023 guideline for designating conformity assessment bodies adds technical-staff and management-system criteria that overlap with SAAC accreditation, forcing laboratories through dual compliance cycles. Although Saudi authorities are expanding digital portals to streamline submissions, the absence of full inter-agency data sharing continues to slow accreditation renewals and market entries.

Shortage of Accredited Local Laboratories

SAAC’s registry shows most accredited facilities located in Riyadh, Dammam, and Jeddah, leaving emerging industrial zones such as Al-Qassim or Asir with limited coverage. Manufacturers in those regions either ship samples hundreds of kilometers or accept longer testing queues, raising cost and delaying product launches. Rules favoring Saudi ownership in private laboratories, combined with a 70% localization quota for medical labs, complicate foreign investment in new capacity. Limited talent inflow further constrains expansion despite rising demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Sustains Lead While Certification Accelerates

Testing contributed 55.1% of 2024 revenue, anchored by SASO’s expanding list of technical regulations and SFDA’s device-classification regime that require laboratory evidence for every safety and performance claim. The Saudi Arabia testing inspection and certification market size attributable to testing is projected to grow alongside new standards for smart appliances, industrial machinery, and hydrogen systems. Inspection services, which comprised roughly 30% of 2024 value, remain essential for infrastructure quality verification and asset-integrity programs, yet their growth trails that of standards-driven segments. Certification although the smallest contributor enjoys a 5.5% CAGR as local producers seek ISO, IEC, and GSO marks to unlock export channels. The convergence of digital twins with in-situ sensors requires integrated testing protocols for data integrity, further buttressing laboratory workloads. ISO 17025 accreditation, already a prerequisite for chemical and materials analysis, continues to raise capital barriers for new entrants, consolidating demand with fewer, larger providers.

The Saudi Arabia testing inspection and certification market expects a steady migration toward bundled service contracts where certification bodies partner with labs to deliver cradle-to-gate conformity solutions. Multinationals leverage global networks to import specialized assays or rare-gas calibrations that local facilities lack, while domestic laboratories fast-track capacity expansions in wireless EMC, battery safety, and additive-manufacturing powders. Service firms that integrate blockchain traceability and automated report generation differentiate on turnaround time and audit readiness, factors increasingly valued by auto, electronics, and consumer-goods manufacturers.

By Sourcing Type: Outsourcing Dominates as Compliance Grows More Complex

Organizations outsourced 62.6% of TIC spending in 2024, reflecting a preference for variable-cost engagements over the fixed expenses of internal labs. The Saudi Arabia testing inspection and certification market sees this model reinforced by SASO’s 2025 rule changes, which stretched the depth of documentation and scope of sample testing required for every shipment. SMEs lack trained compliance staff and sophisticated instruments, making third-party support almost mandatory. Even large oil majors increasingly externalize specialized NDT for corrosion mapping, phased-array UT, and drone-based flare inspections to firms that invest continually in new hardware and ISO 45001 safety systems.

In-house capabilities persist inside petrochemical majors and select giga-project contractors that maintain proprietary pilot plants and pilot test rigs. Nevertheless, hybrid models are proliferating: international testing inspection and certification leaders open local satellite labs to handle on-site sampling while routing complex analyses to global centers. Saudi firms meanwhile enter joint ventures with foreign laboratories to share accreditation lifecycles and knowledge transfer obligations, aligning with local-content policies. Outsourcing growth is set to remain above 5% as evolving cyber-physical regulations and sustainability metrics demand new test methods that cannot be justified on individual corporate balance sheets.

By Industry Vertical: Energy Supremacy Faces Fast-Moving Healthcare Upswing

Oil, gas, and petrochemicals accounted for 29.85% of 2024 revenue, powered by large-scale refinery turnarounds, pipeline-integrity surveys, and LNG tank certifications. The segment’s importance ensures recurring full-cycle inspection contracts, extensive materials characterization, and highly specialized destructive testing. Yet, life sciences and healthcare is charting the sharpest trajectory with a 5.6% CAGR. Intensified SFDA oversight of medical devices and pharmaceuticals mandates technical-file audits, biocompatibility assays, and GMP compliance inspections that few facilities can perform in-house. The Saudi Arabia testing inspection and certification market share associated with life sciences is therefore set to enlarge substantially, benefiting laboratories accredited to ISO 15189 and ISO 13485.

ICT and telecom represents roughly 15% of value, supported by network-equipment EMC testing and 5G radiation-pattern verification. Construction and infrastructure claim about 12%, stimulated by mega-projects that require soil, concrete, and environmental monitoring. Food, agriculture, and beverage maintain steady spending through import-surveillance programs and halal conformity reviews, whereas industrial manufacturing and machinery expand in lockstep with Vision 2030’s localization targets. Providers able to address multiple verticals under unified quality-management systems gain revenue synergies and cross-selling leverage.

By Mode of Service Delivery: Digital and Remote Methods Gain Momentum

On-site services delivered 51.2% of 2024 spend, underlining the need for physical access during weld inspections, pressure-vessel hydrotests, and structural steel surveys. Off-site laboratory analysis accounts for about 35%, focusing on chemistry, metallurgy, and microbiology. Remote and digital models, though still nascent, post the highest 5.8% CAGR through 2030. Saudi Aramco’s deployment of UAVs and ROVs showcases how high-resolution imagery, AI defect recognition, and real-time cloud reporting can reduce downtime and enhance safety. NEOM’s emphasis on digital construction workflows drives demand for virtual inspections, BIM data validation, and sensor network commissioning.

The Saudi Arabia testing inspection and certification market increasingly integrates mixed-reality headsets for third-party auditors, blockchain for immutable certificate storage, and edge devices for continuous emissions monitoring. Pandemic-era policy exceptions that allowed remote factory audits have matured into formal procedures within several sectoral regulations, further legitimizing hybrid delivery. Providers that combine ruggedized instrumentation with secure telemetry platforms and certified cyber-teams position themselves to capture next-generation conformity budgets.

Geography Analysis

Eastern Province generated roughly 35% of 2024 testing inspection and certification revenue, anchored by Jubail’s petrochemical cluster, Dammam’s service corridor, and port-linked import inspection activity. High asset density in pipelines, storage terminals, and specialty chemicals plants produces continuous NDT, calibration, and environmental-monitoring demand. Riyadh captured 30%, leveraging its 4,502 factories, government regulators, and corporate headquarters, all of which require routine quality audits and certification renewals. Makkah region secured 20% as Jeddah Port remains the primary entry point for consumer goods that must clear SABER-linked conformity checks.

Secondary provinces now register above-average growth. Al-Qassim’s 546 plants in agrifood processing need pesticide-residue tests, cold-chain audits, and halal verifier training. Madinah and Asir ride tourism-led construction booms that necessitate soils analysis, structural steel testing, and elevator safety certification. The Saudi Arabia testing inspection and certification market size attached to these emerging hubs is modest today but could triple by 2030 if laboratory investment keeps pace. Yet SAAC lists only a handful of accredited facilities outside the three main metros, compelling businesses in interior regions to ship samples long distances or accept mobile-lab surcharges .

Tabuk’s NEOM project is a special case. Element’s new laboratory in NEOM Community 2 provides dedicated concrete, aggregate, and environmental testing to meet advanced sustainability specs . Concentrated giga-project schedules create temporary demand spikes, sometimes exceeding available technician capacity and driving premiums for rapid-response teams. Government plans for Special Economic Zones near ports may redistribute future demand, especially if incentives succeed in attracting EV battery plants, hydrogen electrolyzer factories, or green-steel mills that each carry high testing intensity.

Competitive Landscape

The Saudi Arabia testing inspection and certification market shows moderate concentration. SGS, Intertek, and Bureau Veritas collectively command roughly 40% revenue, capitalizing on global technical libraries, multi-sector accreditations, and long-standing ties with SASO and SFDA. Bureau Veritas’s multi-year framework with NEOM’s engineering office underscores how incumbents secure mega-project slots requiring massive manpower and cross-disciplinary expertise. International leaders continually refresh fleets of drones, crawler robots, and mobile labs, ensuring rapid deployment for flare inspections or weld defect mapping.

Local players occupy strategic niches. Saudi K-KEM leads specialized ultrasonic and radiographic testing for onshore and offshore oil assets. Gulf Lab Services focuses on materials chemistry for cement and steel producers. Consolidation trends are visible: ACES International’s acquisition of Inspection Technology Company expands non-destructive testing coverage across Aramco sites. Public Investment Fund’s backing for Elm’s purchase of Thiqah consolidates national digital-platform capability, integrating e-certification services with labor-qualification checks.

Technology remains a key differentiator. Providers investing in AI-enabled crack detection, cloud-based certificate management, and blockchain authentication shorten turnaround times and win renewals. Firms slow to automate remain vulnerable to price pressure, especially in commoditized soil and concrete testing. Localization policies and Saudization quotas also shape competition; companies able to train and retain Saudi engineers gain regulatory goodwill and smoother license renewals, an intangible yet decisive edge in tender scoring.

Saudi Arabia Testing Inspection and Certification Industry Leaders

SGS Gulf Ltd.

Intertek Saudi Arabia Ltd.

Bureau Veritas Saudi Arabia Ltd.

TÜV Rheinland Arabia Co. Ltd.

TÜV SÜD Saudi Arabia LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: NEOM Green Hydrogen Company launched a virtual career fair to recruit O and M staff for the world’s largest green-hydrogen project targeting 2026 operations.

- January 2025: PIF and Elm agreed on Elm’s acquisition of Thiqah, consolidating national digital capabilities to support e-certification and conformity platforms.

- January 2025: SASO enforced mandatory Product and Shipment Certificates for all imports, removing Letter of Undertaking alternatives and raising compliance checkpoints

- January 2025: ACES International completed the purchase of Inspection Technology Company, adding Aramco-approved NDT services to its Saudi portfolio

Saudi Arabia Testing Inspection and Certification Market Report Scope

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

How large is the Saudi Arabia testing inspection and certification market in 2025?

The sector was valued at USD 3.64 billion in 2025 and is projected to reach USD 4.64 billion by 2030, implying a 4.97 CAGR.

Which service type contributes most to Saudi testing inspection and certification revenue?

Testing dominates with 55.1% of 2024 revenue owing to mandatory conformity assessments tied to SASO and SFDA regulations.

What vertical shows the fastest growth in Saudi testing inspection and certification demand?

Life sciences and healthcare posts the highest 5.6% CAGR as SFDA tightens medical-device oversight.

Why are outsourcing levels high in Saudi testing inspection and certification activities?

Outsourced services account for 62.6% of 2024 spending because evolving regulations and advanced test methods exceed most firms’ in-house capabilities.

Which region inside Saudi Arabia generates the greatest testing inspection and certification demand?

Eastern Province leads with about 35% of national revenue, driven by its dense oil, gas, and petrochemicals infrastructure.

How are giga-projects influencing TIC opportunities?

Projects like NEOM, the Red Sea development, and Qiddiya create spikes in on-site testing, environmental monitoring, and digital inspection demand as construction accelerates toward 2030.

Page last updated on: