UAE Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

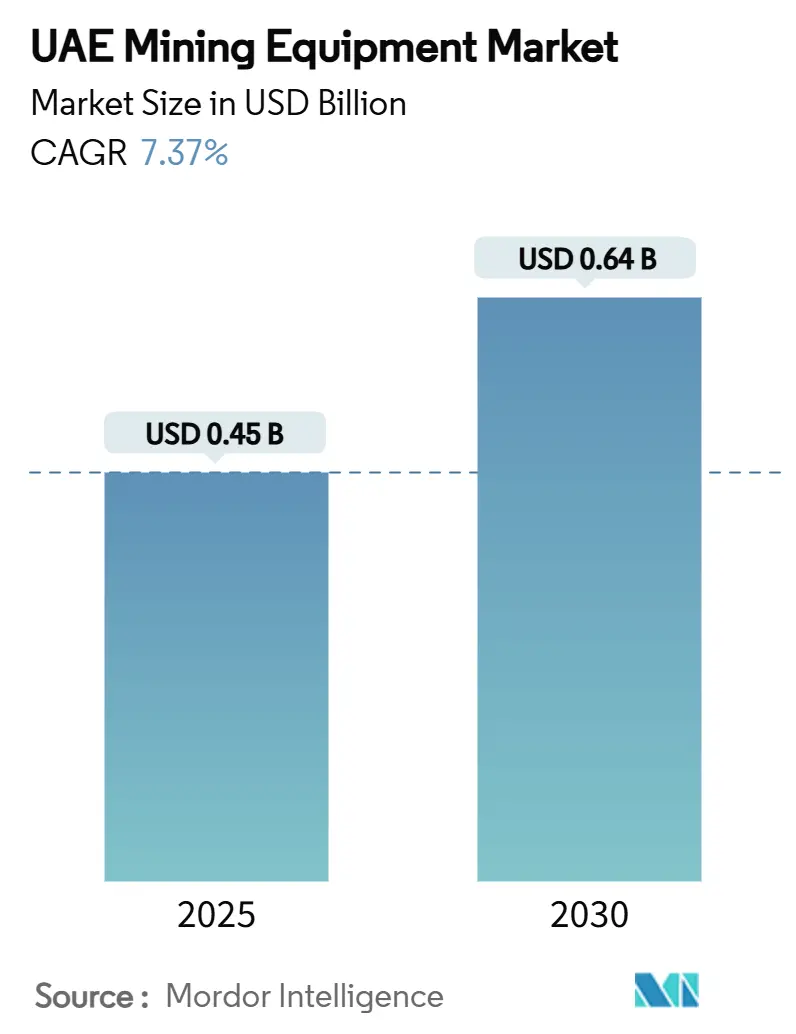

| Market Size (2025) | USD 0.45 Billion |

| Market Size (2030) | USD 0.64 Billion |

| Growth Rate (2025 - 2030) | 7.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Mining Equipment Market Analysis by Mordor Intelligence

The UAE Mining Equipment Market size is estimated at USD 0.45 billion in 2025, and is expected to reach USD 0.64 billion by 2030, at a CAGR of 7.37% during the forecast period (2025-2030). The expansion reflects the country’s broader industrial diversification agenda, especially Operation 300bn, and its ambition to become a global critical‐minerals hub. Government‐backed capital, a USD 2.5 billion Brazil partnership for strategic mineral exploration, and a USD 1.4 trillion pledge to the United States—a decent amount is earmarked for mining—are expanding procurement budgets for high-specification machinery. Surface equipment dominates because aggregate extraction underpins mega-projects from NEOM City to Dubai’s continuing urban build-out. At the same time, tighter energy-efficiency rules and the Barakah nuclear plant’s 25% share of national power are accelerating interest in battery-electric fleets. Moderate market fragmentation lets global OEMs leverage local partners for maintenance and distribution leverage while still facing price competition when commodity prices soften.

Key Report Takeaways

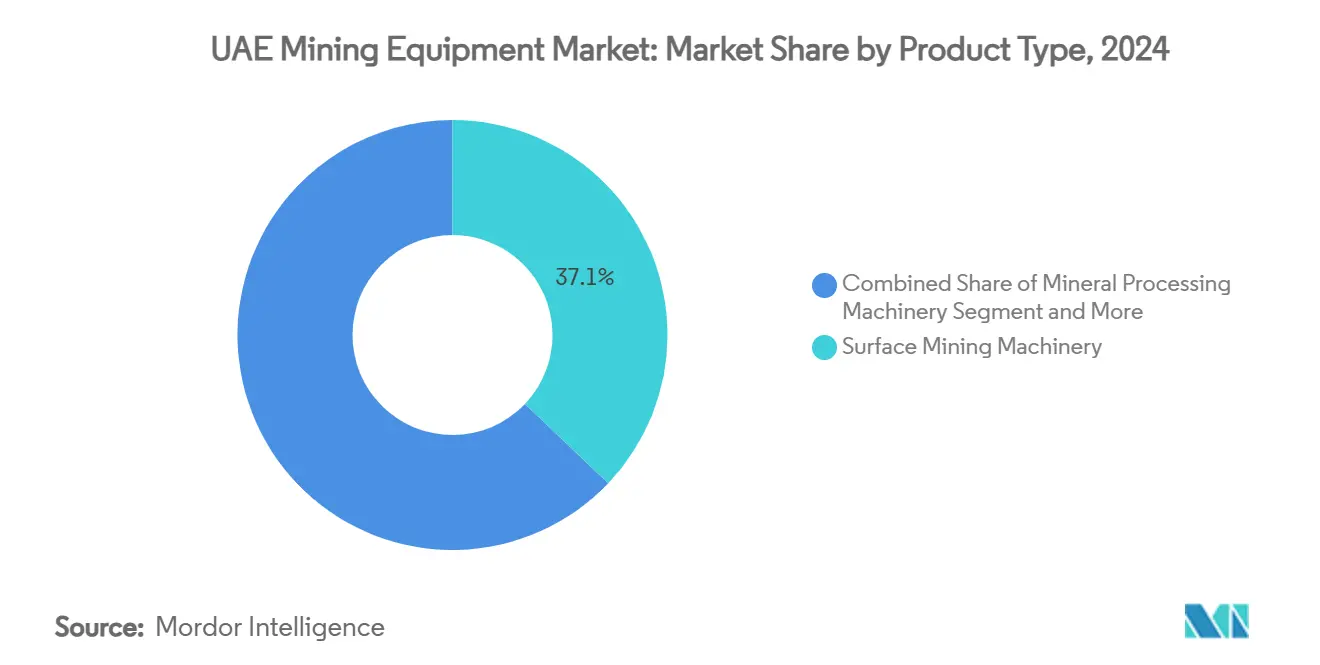

- By product type, Surface Mining Machinery held 37.13% revenue share in 2024; Mineral Processing Machinery is projected to expand at 7.41% CAGR through 2030.

- By function type, the transportation segment captured 43.18% of the UAE mining equipment market share in 2024, whereas processing equipment is set to record the fastest 7.56% CAGR to 2030.

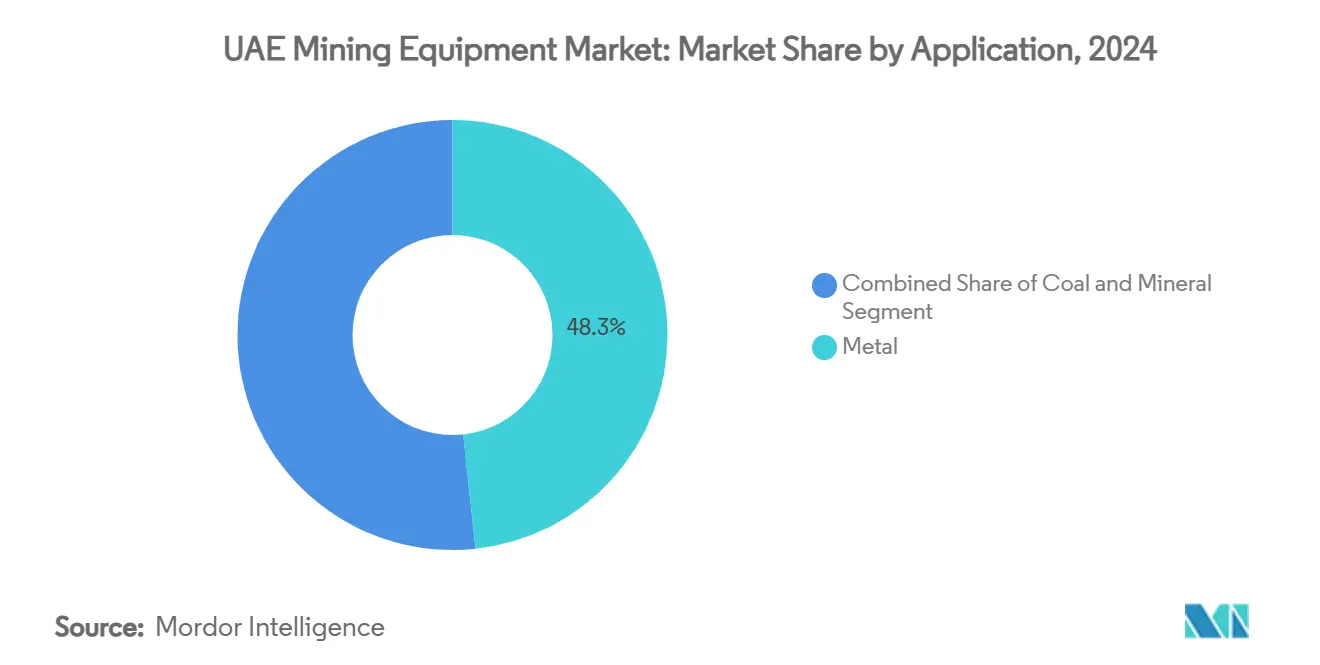

- By application, metal mining accounted for a 48.32% share of the UAE mining equipment market in 2024, and industrial minerals are advancing at a 7.39% CAGR through 2030.

- By power source, diesel-powered units commanded 76.17% share of the UAE mining equipment market size in 2024, while fully electric or battery-electric models are expected to post a 17.58% CAGR to 2030.

UAE Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Aggregates | +1.5% | National, with early gains in Dubai, Abu Dhabi, NEOM cross-border projects | Short term (≤ 2 years) |

| Government Investment | +1.2% | National, with concentration in Abu Dhabi and Dubai industrial zones | Medium term (2-4 years) |

| Expansion of Bauxite & Copper Exploration Projects | +0.9% | Global operations with UAE-based equipment procurement | Long term (≥ 4 years) |

| Adoption of Automation & Telematics | +0.8% | National deployment with technology transfer from global operations | Medium term (2-4 years) |

| Energy-Subsidy Reforms Driving Efficiency Upgrades | +0.7% | National, with higher impact in energy-intensive operations | Short term (≤ 2 years) |

| Growth of Mineral-Recycling Hubs | +0.6% | Concentrated in KEZAD, Jebel Ali, and Fujairah free zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Aggregates from Mega-Projects

An active national infrastructure pipeline drives peak aggregate output, benefitting excavators, articulated trucks, and mobile crushers. KEZAD alone added AED 126.5 billion in GDP during 2024, absorbing fleet additions for quarry and port projects. Etihad Rail is cutting haulage times and raising the utilisation of high-capacity rail-car loaders. Doosan’s 75 excavator shipment to the NEOM build demonstrates the UAE’s re-export advantage as a regional logistics hub. Aggregate intensity is expected to climax during 2025–2027, propelling short-cycle orders for surface equipment and on-site crushing spreads.

Government Investment via UAE Industrial & Logistics Strategy

Operation 300bn allocates a massive amount through the Emirates Development Bank to accelerate local manufacturing, including equipment assembly and rebuild centres within KEZAD’s 550 km² footprint[1]“Investor Presentation 2024,” KEZAD Group, kezadgroup.com . Industrial sector value added exponentially in 2023, a decent uptick, signalling healthy replacement cycles. Mashreq Bank’s AED 1 billion in 2024 credit lines, which boosts demand for smart mining assets. A new industrial licence under Make it in the Emirates delivers customs exemptions on components, lowering landed costs for diesel and electric machines. The policy blend pushes OEMs such as Caterpillar and Sandvik to deepen localisation strategies for quicker aftermarket support.

Expansion of Bauxite & Copper Exploration Projects

International Resources Holding spent a huge amount to secure more than half of Mopani Copper Mines, binding future fleet purchases to UAE-based distributors. Emirates Global Aluminium’s huge investment in bauxite chain in Guinea heightens volumes of crushers, conveyors, and 240-ton haul trucks[2]“Sustainability Report 2024,” Emirates Global Aluminium, ega.ae . The memorandum between EPointZero and IRH establishes renewable power solutions for Zambian operations, tilting specifications toward battery-electric drills and hydrogen haulage. Therefore, copper and bauxite self-sufficiency ambitions extend the UAE mining equipment market beyond domestic reserves and anchor forward demand visibility through 2030.

Adoption of Automation & Telematics in Mining Fleet

Hexagon’s fleet management roll-outs are reducing idle times by double-digit percentages at sites in Abu Dhabi, with safety performance gains attracting insurer incentives[3]“Mining Division Case Study 2024,” Hexagon AB, hexagon.com. Caterpillar’s MineStar installations, referenced by Rio Tinto, now appear in limestone quarries west of Dubai. Apadana Kavosh’s IoT-based tracking across 1,000 pieces confirms payback periods below 24 months. Epiroc’s LinkOA platform, unlocked by its ASI Mining acquisition, meshes drills and trucks for coordinated autonomous cycles. As subsidy reforms lift diesel costs, integrated autonomy provides a parallel route to double-digit productivity gains, reinforcing investment cases for fleet renewal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Commodity Prices | -1.1% | Global impact affecting UAE-based mining investments | Short term (≤ 2 years) |

| Limited Domestic Ore Reserves | -0.8% | National, with higher impact on local mining operations | Long term (≥ 4 years) |

| Water-Scarcity Driven Permitting Delays | -0.6% | National, with acute impact in inland mining operations | Medium term (2-4 years) |

| New Stage V Diesel-Emission Standards | -0.4% | National implementation with compliance costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Ore Reserves

UAE geology is weighted to gypsum, limestone, and sand, so high-value metal deposits are scarce. Fujairah produced massive amount of industrial minerals as recently as 2024, yet 80% went to domestic construction, limiting scale for large-capex underground machinery. Federal Law 24 of 1999 enforces rehabilitation duties, keeping stripping ratios conservative. The forthcoming federal mining law may streamline licences, but equipment volumes will still depend more on overseas concessions than local pits.

Water-Scarcity Driven Permitting Delays for Wet Plants

The Water Security Strategy 2036 targets more than two-fifths of demand reduction, so permits for slurry circuits and wet screens face long approval cycles. ADNOC Onshore trials closed-loop recycling for drilling mud to cut freshwater usage. The 150 million-gallon-per-day Umm Al Quwain desalination project partially offsets constraints but raises opex for water-intensive beneficiation. OEMs are responding with dry high-frequency screens and ore-sorters that enable low-water flowsheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surface Mining Dominates Equipment Demand

Surface Mining Machinery captured 37.13% of the UAE mining equipment market share in 2024 as quarries supplying cement plants and infrastructure jobs remain the backbone of domestic output. Equipment salesalign with shallow deposits and favourable stripping ratios around Ras Al Khaimah. Mineral Processing Machinery is forecast to log a 7.41% CAGR, reflecting free-zone incentives for in-country beneficiation. Open-pit rigs and 120-ton rigid trucks feed crushing lines integrated into new KEZAD recycling hubs. Underground units are niche, reserved for metro extensions in Dubai and stormwater tunnels under Abu Dhabi Corniche. Epiroc’s battery-electric SmartROC D65 BE is a regional test case for carbon-neutral drilling. Mobile crushers see higher utilisation as contractors pivot to on-site recycling, easing aggregate logistics for tower projects on the Palm Jebel Ali. Imports dominate high-tonnage shovels, yet local assembly of wear parts is growing in Sharjah industrial areas.

Second-round replacement cycles for primary crushers mirror 2018–2019 procurement waves. Life-extension rebuilds on 2007-vintage loaders are standard, but CAPEX shifts favour new telematics-enabled models because warranty bundles cover predictive maintenance. Cross-border rental pools positioned in Dubai World Central allow fleet managers to redeploy idle surface assets quickly onto Saudi contracts, smoothing utilisation across economic cycles. Consequently, the UAE mining equipment market hinges on surface fleet turnover, although processing lines now set the growth tempo.

By Function Type: Transportation Equipment Leads Market Share

Transportation equipment controlled 43.18% of the UAE mining equipment market share in 2024, thanks to long haul distances between quarries and coastal cement kilns. Higher-capacity road trains and 200-ton rigid trucks dominate procurement budgets. Processing machinery, however, is forecast to expand at a 7.56% CAGR, reflecting the policy to export higher-value mineral products. Conveyor system retrofits support Etihad Rail load-out terminals that link Fujairah quarries to Ruwais industrial complexes. Excavators retain consistent demand as brownfield pits widen benches to meet aggregate volume spikes during 2025–2027.

Fleet managers are ordering hybrid or full-electric 60-ton dump trucks to secure compliance ahead of stricter fuel benchmarks. Liebherr’s 360 T 264 battery-electric haul truck programme, co-developed with Fortescue, is viewed locally as proof of concept for zero-emission haulage. However, fast-charge infrastructure remains limited outside KEZAD and Jebel Ali. Processing firms in free zones invest in optical sorters that deliver lower grade losses than legacy wet techniques, trimming water drawdown. As subsidy reform narrows the diesel price advantage, life-cycle economics tilt further toward high-efficiency conveyor haulage and autonomous truck platooning.

By Application: Metal Mining Drives Equipment Procurement

Metal mining held 48.32% revenue in 2024 and continues to anchor the UAE mining equipment market demand. Emirates Global Aluminium’s 2.57 million-ton aluminium output needs bauxite crushers, alumina calciners, and residue handling systems. International Resources Holding’s copper projects funnel orders for 240-ton haul trucks and SAG mills through UAE trading subsidiaries. Industrial minerals are projected to grow at a 7.39% CAGR, supported by state infrastructure spend that absorbs gypsum, limestone, and dolomite.

Coal applications are negligible, so OEM sales teams prioritise quarry attachments and alloy-steel screens tuned to local rock abrasivity. DMCC’s status as the world’s second-ranked commodity trade hub simplifies import-export paperwork, shortening lead times for replacement parts. As EGA explores capacity upgrades, market entrants see upside in supplying modular smelter auxiliaries. Equipment builders also target design-build contracts for new alumina refineries in Guinea tied to UAE equity interests, thereby extending the commercial footprint of the UAE mining equipment market well beyond the federation’s borders.

By Power Source: Electric Equipment Gains Momentum

Diesel units continue to command a 76.17% share of the UAE mining equipment market, underpinned by well-established maintenance ecosystems and a still-favourable fuel tax regime. Yet battery-electric and hybrid machines will post the quickest 17.58% CAGR because Net Zero 2050 plans incentivize carbon budgeting, and the Barakah nuclear plant now supplies one-quarter of grid power. Caterpillar’s strategic sales agreement with CRH for battery-electric off-highway trucks has signalled mainstream acceptance of high-tonnage electrification.

Stage V emissions rules, starting 2027, will raise capex on new diesel units by adding SCR aftertreatment, narrowing total-cost gaps versus battery platforms. Hybrid loaders that reclaim braking energy provide transitional savings, particularly in quarries where high cycles per hour offer short payback. Charging infrastructure obstacles are receding as KEZAD pilots megawatt-scale fast-charge pads that are compatible with incoming fleets. OEM finance arms are rolling out lease packages indexed to verified CO₂ savings, giving procurement teams fresh pathways to meet ESG KPIs without expending upfront capital. Over the horizon, hydrogen fuel cell haulage, explored by Komatsu and General Motors, may join the technology mix if electrolysis costs keep falling.

Geography Analysis

Abu Dhabi and Dubai together comprise the core of UAE mining equipment demand, stimulated by heavy industrial footprints and efficient logistics. Abu Dhabi’s dominance traces to Emirates Global Aluminium at Al Taweelah and ADNOC’s Ruwais industrial zone, both requiring steady inflows of crushers, stackers, and port reclaimers. Dubai provides an international gateway through Jebel Ali Port and the DMCC free zone, enabling rapid import of high-value components and regional re-exports to Oman and Saudi Arabia.

Fujairah ranks third due to its multiple quarries clustered along the Hajar range. The emirate’s direct access to Gulf of Oman ports simplifies aggregate shipment to Qatar and India, pushing up orders for conveyor ship-loaders and coastal hopper loaders. Northern Emirates—Sharjah, Ras Al Khaimah, Umm Al Quwain—focus on ready-mix plants and cement kilns that source limestone locally. Due to cost sensitivity, many operators here upgrade 1990s-era wheeled loaders to Tier 3 rebuilds rather than new Tier 4-final models.

The 900 km Etihad Rail stage 2 alignment now links Fujairah to Ruwais, cutting three-hour truck runs to 90-minute rail hauls. This intermodal backbone raises the business case for in-pit crushers and rail-loop stacker reclaimers. Cross-border activity is expanding as contractors divert fleets to NEOM, The Line, and Red Sea projects, highlighting the UAE’s logistics role in regional fleet optimisation. Free zones across all emirates allow 100% foreign ownership, insulating operators from the 49% mainland cap and enabling OEMs to stock high-value spares duty-free, improving service levels and machine availability.

Competitive Landscape

The UAE mining equipment market sits in the mid-range on consolidation metrics. Caterpillar, Komatsu, Sandvik, Epiroc, and Liebherr collectively hold an estimated top-five share of nearly 60%, placing concentration below oligopolistic thresholds yet above highly fragmented construction machinery segments. Each OEM maintains local distributors—Al Bahar for Caterpillar, Galadari for Komatsu, and United Al Saqer for Liebherr—ensuring parts availability and factory-trained technicians. Barriers to entry arise from capital intensity, ISO 45001 safety accreditation needs, and the Emirates’ preference for globally recognised brands, which collectively protect incumbent positions.

Strategic moves centre on technology and sustainability. Komatsu’s July 2024 acquisition of GHH Group broadens underground capability for metro tunnel boring and boosts tele-remote loader offerings. Epiroc’s completion of ASI Mining’s takeover accelerates autonomous haulage integration, valuable for UAE quarries grappling with labour cost inflation. Caterpillar launched its Dynamic Energy Transition (DET) modular battery system that pairs with 190-ton trucks, a decisive step for operators targeting Scope 1 GHG cuts.

Local firms seize white-space opportunities in parts remanufacture, water-efficient dry processing, and nuclear-powered microgrid integration at remote concessions. KEZAD’s heavy-industry cluster hosts component machining shops, reducing lead times on bucket teeth and crusher liners. Financing solutions gain importance as fluctuating commodity prices push miners toward leasing and pay-per-hour structures over outright purchase. The competitive tempo is likely to accelerate as Stage V rules tighten in 2027, a phase expected to catalyse replacement demand while increasing technical barriers to grey-market imports.

UAE Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Sandvik AB

Epiroc AB

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: EPointZero and International Resources Holding signed an MoU to decarbonise Mopani Copper Mines in Zambia, prioritising renewable powered equipment rollouts.

- April 2025: Epiroc secured an MAUD 350 (SEK 2.2 billion) contract with Fortescue for fully autonomous and electric surface equipment, its largest order to date.

- March 2025: The UAE announced a USD 1.4 trillion investment plan into the United States, including USD 1.2 billion targeted at mining collaborations to lock in critical mineral supplies.

- January 2025: Brazil and the UAE established a USD 2.5 billion strategic partnership for mineral exploration, enhancing the procurement prospects for UAE-based equipment suppliers.

UAE Mining Equipment Market Report Scope

| Underground Mining Machinery |

| Open-Pit Mining Machinery |

| Surface Mining Machinery |

| Drills & Breakers |

| Crushing, Grinding, Filtering & Screening Equipment |

| Mineral Processing Machinery |

| Transportation |

| Processing |

| Excavation |

| Coal |

| Mineral (Industrial Minerals) |

| Metal (Ferrous & Non-ferrous) |

| Diesel-Powered Equipment |

| Hybrid (Diesel-Electric) Equipment |

| Fully Electric / Battery-Electric Equipment |

| By Product Type | Underground Mining Machinery |

| Open-Pit Mining Machinery | |

| Surface Mining Machinery | |

| Drills & Breakers | |

| Crushing, Grinding, Filtering & Screening Equipment | |

| Mineral Processing Machinery | |

| By Function Type | Transportation |

| Processing | |

| Excavation | |

| By Application | Coal |

| Mineral (Industrial Minerals) | |

| Metal (Ferrous & Non-ferrous) | |

| By Power Source | Diesel-Powered Equipment |

| Hybrid (Diesel-Electric) Equipment | |

| Fully Electric / Battery-Electric Equipment |

Key Questions Answered in the Report

What is the value of the UAE mining equipment market in 2025 and its growth outlook to 2030?

The market is valued at USD 0.45 billion in 2025 and is projected to reach USD 0.64 billion by 2030 at a 7.37% CAGR.

Which product category leads unit demand?

Surface Mining Machinery leads with 37.13% share because aggregate extraction underpins national infrastructure expansion.

Which application segment is growing the fastest?

Industrial minerals is forecast to grow at 7.39% CAGR due to sustained demand for construction aggregates through 2030.

How are UAE sustainability goals shaping purchasing decisions?

Net Zero 2050 targets and Stage V emission standards are accelerating adoption of battery-electric and hybrid equipment, especially in haulage and drilling.

What role do free zones play in equipment distribution?

Free zones such as KEZAD and Jebel Ali permit 100% foreign ownership, duty-free spare parts stocking, and fast customs clearance, making them pivotal distribution hubs.

Who are the key suppliers in the UAE?

Caterpillar, Komatsu, Sandvik, Epiroc, and Liebherr collectively hold the largest shares, supported by strong local dealer networks for parts and service.

Page last updated on: