Oman Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

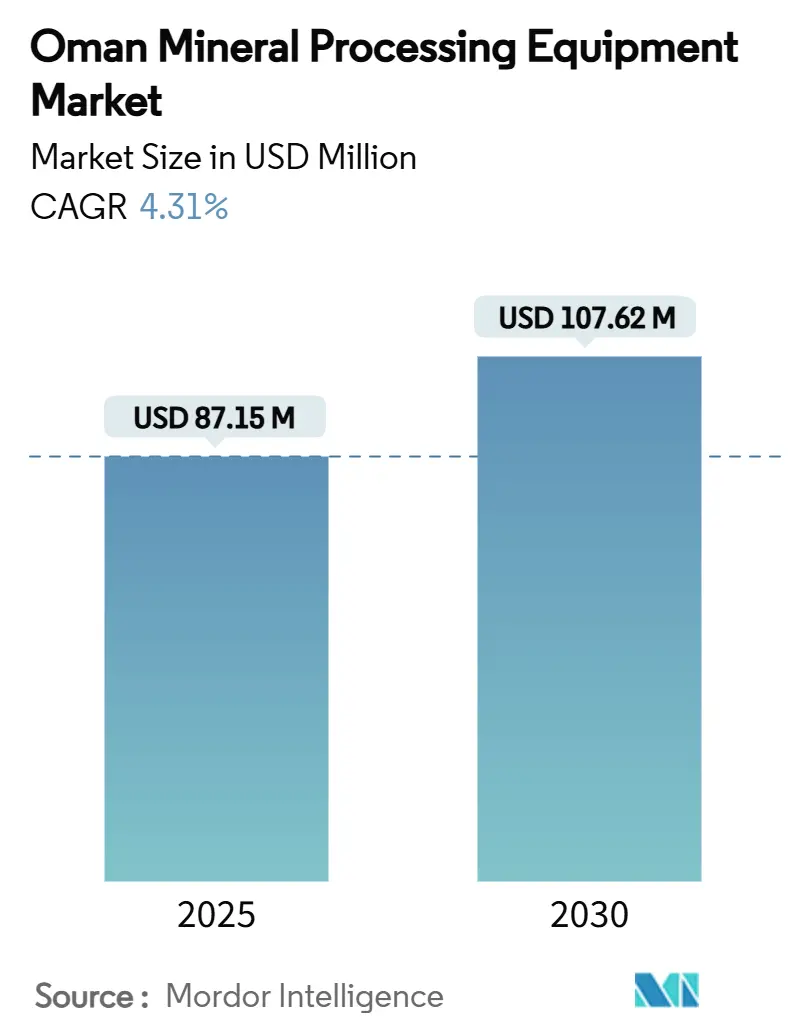

| Market Size (2025) | USD 87.15 Million |

| Market Size (2030) | USD 107.62 Million |

| Growth Rate (2025 - 2030) | 4.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Oman Mineral Processing Equipment Market size is estimated at USD 87.15 million in 2025, and is expected to reach USD 107.62 million by 2030, at a CAGR of 4.31% during the forecast period (2025-2030). This steady trajectory mirrors the sultanate’s bid to diversify its economy under Vision 2040, with mining promoted as a central pillar for reducing hydrocarbon dependence. Robust capital inflows from Future Fund Oman’s USD 5.2 billion allocation and Minerals Development Oman’s long-term investment program continue to underpin demand for high-capacity crushing, grinding, and material-handling systems. Accelerated copper and chromite field developments, plus early-stage lithium exploration, have widened the customer base for sophisticated separation and flotation technologies. Parallel advances in renewable-powered processing, automation, and predictive maintenance platforms are reshaping procurement criteria as operators look to cut energy costs, resolve skilled-labor gaps, and tighten environmental compliance. Free-zone incentives such as import duties and multi-decade tax holidays accentuate the market’s appeal for global original-equipment manufacturers (OEMs) with localized service networks.

Key Report Takeaways

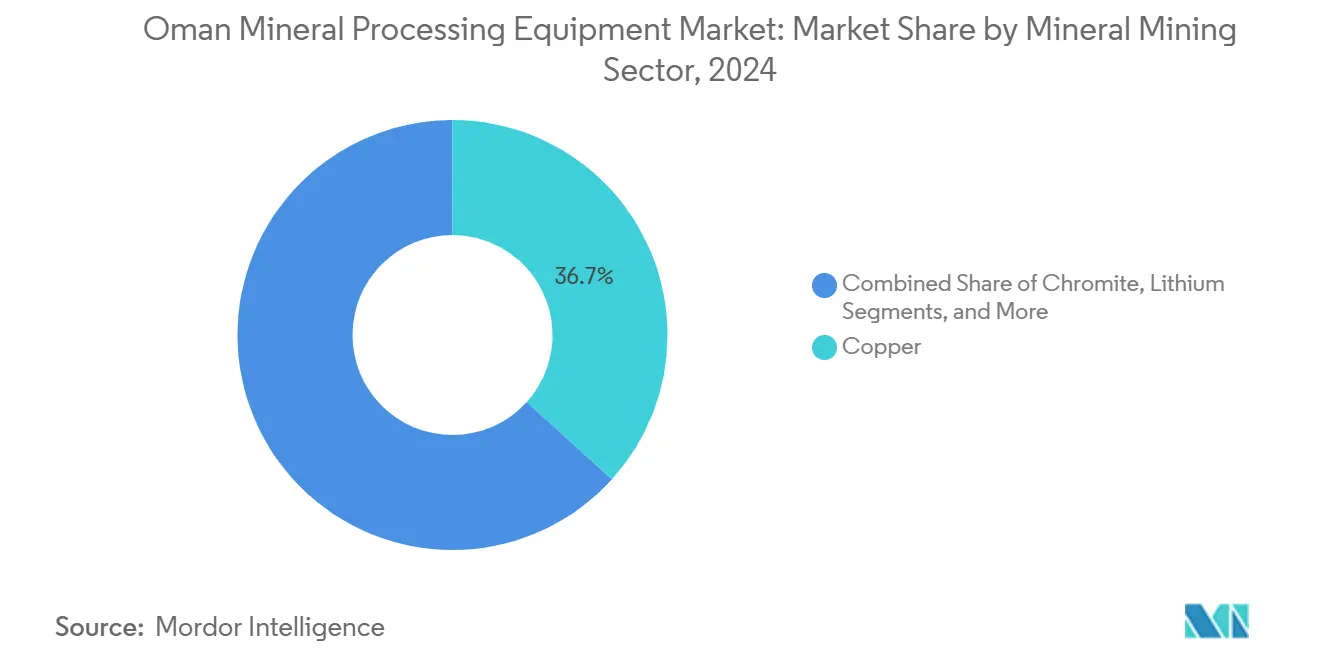

- By mineral mining sector, the copper segment held 36.71% of the Oman mineral processing equipment market share in 2024, while lithium processing is projected to grow at a 4.46% CAGR through 2030.

- By equipment type, crushers accounted for 28.14% of the Oman mineral processing equipment market size in 2024, whereas feeders and conveyors are poised for a 4.51% CAGR up to 2030.

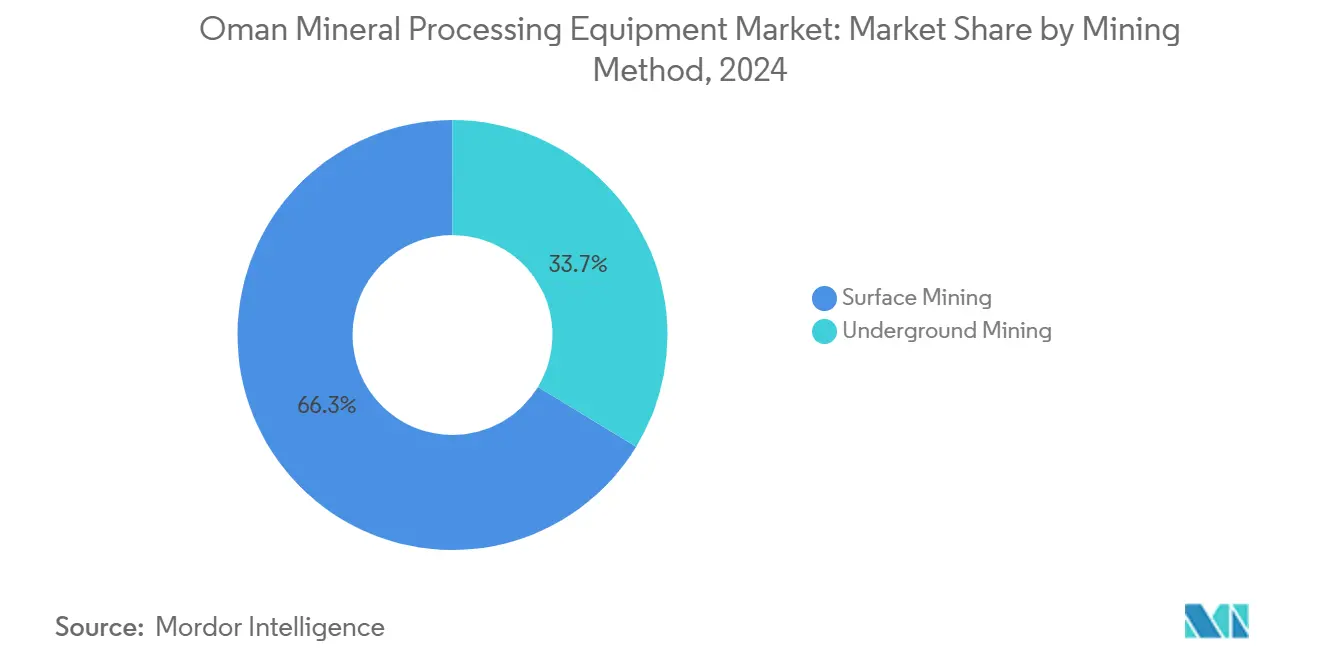

- By mining method, surface operations commanded 66.34% of the Oman mineral processing equipment market size in 2024; underground equipment is advancing at a 4.55% CAGR to 2030.

- By automation level, manual installations represented 45.13% of the Oman mineral processing equipment market size in 2024, yet fully-automated systems are set to rise at a 4.82% CAGR through 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with Oman being one of the contributors. Our global mineral processing equipment market size represents that cumulative total.

Oman Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Copper and Chromite Expansion Projects | +1.2% | National, concentrated in Al Dhahira and North Batinah | Medium term (2-4 years) |

| State-Backed Funding Via Minerals Development Oman | +0.8% | National, with priority on interior mining clusters | Long term (≥ 4 years) |

| Falling Renewable-Power Tariffs | +0.6% | National, particularly Duqm and Sohar industrial zones | Short term (≤ 2 years) |

| In-Country-Value (ICV) Rules | +0.5% | National, affecting all government procurement | Long term (≥ 4 years) |

| Exploration-Licensing Reforms | +0.4% | National, with early gains in Al Dhahira, North Batinah | Medium term (2-4 years) |

| Free-Trade Industrial Zones Waiving Import Duties | +0.3% | Sohar, Duqm, Salalah free zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Copper & Chromite Expansion Projects Under Vision 2040

Large-scale developments such as Al Hadeetha’s copper venture and the Yanqul Copper Project illustrate how Vision 2040 has revived dormant resources and attracted external capital[1]“Project Overview,” Al Hadeetha Resources, alhadeetha.com. Copper’s strategic role in global electrification and a forecast more than three-fifths demand jump by 2030 keep investors focused on high-throughput crushers, SAG mills, and bulk-flotation lines capable of treating low-grade ores profitably. Chromite producers follow suit, commissioning magnetic separators tailored to Omani ophiolite mineralogy to supply metallurgical-grade feed to regional steel and alloy makers. Procurement volumes rise further as operators integrate dust-suppressed conveyors and enclosed screening stations to meet stricter emissions rules.

State-Backed Funding via Minerals Development Oman (MDO)

MDO’s pivot from project-specific equity to end-to-end infrastructure finance secures multiyear order pipelines for conveyor-linked crushers, automated stacker-reclaimers, and rail-mounted loading stations engineered for desert climates. The planned Mineral Line connecting interior deposits to Duqm Port locks in future demand for wear-resistant feeders and IoT-enabled condition-monitoring modules. Technology-transfer clauses baked into MDO’s joint ventures oblige international OEMs to embed remote diagnostics and advanced process-control software, accelerating digital adoption across the Oman mineral processing equipment market.

Falling Renewable-Power Tariffs Boosting Energy-Intensive Grinding

Average levelized costs from wind and solar projects have dropped almost four-fifths since 2019, making around two-fifths of electricity-intensive grinding circuits financially attractive[2]“Renewable Energy Tender Results,” Oman Power & Water Procurement Company, opwp.om. Operators are retrofitting mill drives with high-efficiency variable-speed motors and evaluating HPGR installations that pair lower kWh/t with finer liberation. Metso’s recently launched electrically driven crusher and screen range demonstrates OEM efforts to capture sustainability-linked procurement budgets. Mines promoting renewable-powered processing gain faster environmental approvals and strengthen price negotiations with climate-conscious downstream buyers.

Exploration-Licensing Reforms Accelerating Mine Start-Ups

The 2019 Mineral Wealth Law trimmed permit cycles from 18 months to six and instituted flexible royalties indexed to profitability[3]“Mineral Wealth Law No. 19/2019,” Ministry of Energy and Minerals, meca.gov.om . Predictable timelines embolden juniors to commit to complete, modular equipment packages covering drilling to tailings paste backfill. International groups such as Knights Bay and several Canadian explorers have entered Oman, driving a surge in scoping studies that translate into multi-million-dollar gear orders once resource statements are confirmed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Water Scarcity Constraining Wet Processing | -0.9% | Interior regions, Al Dhahira and North Batinah | Long term (≥ 4 years) |

| Stringent Dust and Emissions Regulations | -0.7% | National, particularly affecting surface operations | Medium term (2-4 years) |

| Logistics Gaps Delayed Rail Link | -0.6% | Interior regions, connecting Al Dhahira to Duqm Port | Medium term (2-4 years) |

| Limited Skilled Mechatronics Workforce | -0.5% | National, with acute shortages in remote mining areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Water Scarcity Constraining Wet Processing

Processing 1 ton of copper ore can consume up to 4 m³ of water, an unsustainable demand on the sultanate’s stressed aquifers. Mines are shifting to dry screening, ore-sorting, and thickened-tailings solutions that reduce make-up water by up to four-fifths. OEMs that integrate column flotation with closed-loop recycling gain an edge, though lower recoveries can lengthen payback. Remote desalination plants in Dhofar raise opex and intensify the search for low-water leaching chemistries.

Stringent Dust & Emissions Regulations

Ministerial Decree 48/2017 compels mines to install continuous emissions monitors, enclosed transfer points, and water-fog cannons, which add around a quarter of initial capex. Extra filtration and real-time air-quality systems raise maintenance complexity, favoring suppliers with robust aftermarket parts coverage. Small leaseholders find compliance costs onerous and are increasingly pooling procurement or engaging contract operators equipped with dust-tight mobile crushing units.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Copper Dominance Drives Equipment Demand

Copper operations generated 36.71% of the Oman mineral processing equipment market share in 2024, the highest of any commodity segment. The Oman mineral processing equipment market size for lithium installations is projected to log a 4.46% CAGR to 2030, driven by battery-chain investors scouting pegmatite veins in the North Mountains.

New copper capacity is also spurring auxiliary demand for tailings thickeners, paste pumps, and geomembrane-lined storage, ensuring sustained aftermarket revenues for OEMs. Chromite players, while steadier, continue upgrading magnetic-separator lines to handle 30 million t of proven reserves. Explorers studying nickel laterite and rare-earth streams hint at additional demand for atmospheric-pressure leach reactors and multi-stage solvent-extraction circuits once feasibility milestones are reached.

By Equipment Type: Crushing Infrastructure Leads Market

Crushers dominated 28.14% of the 2024 billings as mines prioritized primary size-reduction solutions capable of handling highly abrasive ophiolite host rocks. The Oman mineral processing equipment market size attached to feeders and conveyors is expected to compound at 4.51% annually to 2030, propelled by the forthcoming Mineral Line railway and larger stockpile footprints at Sohar logistics hubs.

OEM bids increasingly specify automated liner-change arms, hydraulic toggle reliefs, and AI-guided choke-feed controls to curb downtime. High-pressure grinding rolls and stirred-media mills are gaining share as operators chase 10-15% energy savings and finer liberation in one pass. Vacuum-assisted drum filters, meanwhile, are replacing older thickeners where water quotas are tight, illustrating how sustainability criteria now shape purchasing patterns across the Oman mineral processing equipment market.

By Mining Method: Surface Operations Dominate Despite Underground Growth

Surface mining accounted for 66.34% of Oman mineral processing equipment market in 2024, underscoring the economic logic of bulk earthmoving for low-grade orebodies. Large hydraulic shovels, 220-t haul trucks, and 1,500 mm gyratory crushers headline procurement lists, complemented by in-pit crush-and-convey networks designed to slash diesel burn.

The Oman mineral processing equipment market share attached to underground fleets is climbing as producers tap deeper sulphide horizons. It is forecast to have a 4.55% CAGR through 2030. Orders focus on battery-electric LHDs, remote-controlled jumbos, and refuge-chamber packages that satisfy modern safety codes. Enhanced ventilation on demand and fibre-optic communications also boost capital intensity, giving technology-rich OEMs scope to upsell long-term service contracts.

By Automation Level: Manual Operations Transition to Full Automation

Manual installations accounted 45.13% of Oman mineral processing equipment market in 2024, reflecting legacy dependence on expatriate labor and basic mobile plant. Rising wages, import-permit limits, and safety directives have quickened the shift to operator-assist systems that automate drilling patterns, load dispatch, and crusher choke settings.

Fully automated installations are tracking a 4.82% CAGR to 2030, led by Epiroc SmartROC autonomous rigs and Sandvik AutoMine haulage clusters that deliver double-shift productivity without fatigue-related stoppages. Integrated mine-to-mill dashboards tie fleet health, ore-blend quality, and energy consumption into one decision loop, illustrating how digital backbones underpin the next growth wave in the Oman mineral processing equipment market.

Geography Analysis

Northern governorates remain the epicenter for demand for new equipment and aftermarket services. Al Dhahira and North Batinah host most copper and chromite concentrators, each within 200 km of Sohar Port, enabling efficient inbound logistics for oversized modules and containerized spare parts. The Oman mineral processing equipment market tied to these two regions is expected to retain a dominant double-digit share through 2030.

Interior governorates like South Batinah and Ad Dakhiliyah are emergent hotspots following streamlined licensing and ongoing rail and road expansions under Vision 2040. Early-stage explorers favor skid-mounted crushers, modular grinding lines, and containerized labs that can be relocated as drilling advances. OEMs with field-assembly teams able to mobilize within 48 hours enjoy a competitive edge as reliable after-sales support remains scarce inland.

Musandam and Dhofar present niche growth. Dhofar’s coastal setting suits desalination-dependent wet processing, while Musandam’s rugged terrain nudges operators toward underground methods requiring compact jumbos and narrow-vein ore sorters. SEZAD at Duqm is emerging as a re-export and maintenance hub for the wider GCC, driving orders for portside bulk-handling systems and workshop machinery. Several active projects provide OEMs with opportunities to site regional rebuild centers that shorten turnaround times for critical wear parts.

Coverage of the mineral processing equipment market by Mordor Intelligence spans a wide geographic footprint, with detailed country-level intelligence for Morocco, South Africa, Italy, Brazil, Saudi Arabia, Australia, China, Canada, and Germany, each shaped by local operating conditions.

Competitive Landscape

FLSmidth leads integrated plant solutions, leveraging almost half a jump in service orders to lock in lifecycle contracts across copper and chromite concentrators [4]. Metso Outotec contests the crushing and screening space with an electrified Lokotrack line that dovetails with Oman’s renewable energy drive, while maintaining a robust installed base of HPGRs. Epiroc’s digital drill-automation suite and Sandvik’s mine-planning cloud tools heighten competitive stakes around productivity guarantees and predictive maintenance.

Local content rules require Omani investment in public-sector mining contracts, prompting global OEMs to partner with domestic firms for assembly and component warehousing. Al-Bahar distributes Caterpillar underground fleets, supporting turnkey ventilation and power-solution packages that reduce project interface risk for operators.

Niche suppliers specializing in dust suppression, closed-loop water recycling, and real-time emissions monitoring capture share as environmental compliance costs rise. Price competition remains contained because the total cost of ownership, reliability in extreme heat, and rapid service response outweigh headline capex.

Oman Mineral Processing Equipment Industry Leaders

Metso Outotec

Sandvik AB

FLSmidth A/S

Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Pathfinder Minerals secured a USD 896 million U.S. EXIM Bank letter of intent to develop copper mines, representing the sector's most extensive single equipment finance package.

- April 2025: Weir Group finalized its USD 840 million purchase of Micromine, adding advanced geological modelling tools to its offering for Omani customers requiring integrated digital twin solutions.

- March 2025: Metso introduced a sustainable leaching process for low-grade copper concentrates that uses less process water and achieves higher recovery, which is timely for Omani projects facing water-use curbs.

Oman Mineral Processing Equipment Market Report Scope

| Copper |

| Chromite |

| Lithium |

| Iron Ore |

| Others |

| Crushers |

| Grinding Mills |

| Feeders & Conveyors |

| Drills & Breakers |

| Screens & Separators |

| Pumps & Thickeners |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully-Automated |

| By Mineral Mining Sector | Copper |

| Chromite | |

| Lithium | |

| Iron Ore | |

| Others | |

| By Equipment Type | Crushers |

| Grinding Mills | |

| Feeders & Conveyors | |

| Drills & Breakers | |

| Screens & Separators | |

| Pumps & Thickeners | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully-Automated |

Key Questions Answered in the Report

What is the current value of the Oman mineral processing equipment market?

The market is valued at USD 87.15 million in 2025 and is projected to reach USD 107.62 million by 2030.

Which commodity segment drives most equipment purchases in Oman?

Copper accounts for 36.71% of spending owing to large-scale projects such as Al Hadeetha and Yanqul.

How fast is fully automatic equipment adoption growing?

Installations incorporating full automation are forecast to rise at a 4.82% CAGR through 2030 as operators confront labor shortages.

What role do free-trade zones play in equipment imports?

Sohar, Duqm, and Salalah zones waive import duties and offer extended tax holidays, making them primary channels for high-value machinery.

Why are water-efficient technologies gaining traction?

Acute freshwater scarcity and tighter environmental rules compel mines to favor dry processing, thickened tailings, and closed-loop recycling.

Which OEMs lead the market?

FLSmidth, Metso Outotec, Epiroc, and Sandvik dominate through local partnerships, digital solutions, and strong aftermarket support.

Page last updated on: