Egypt Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

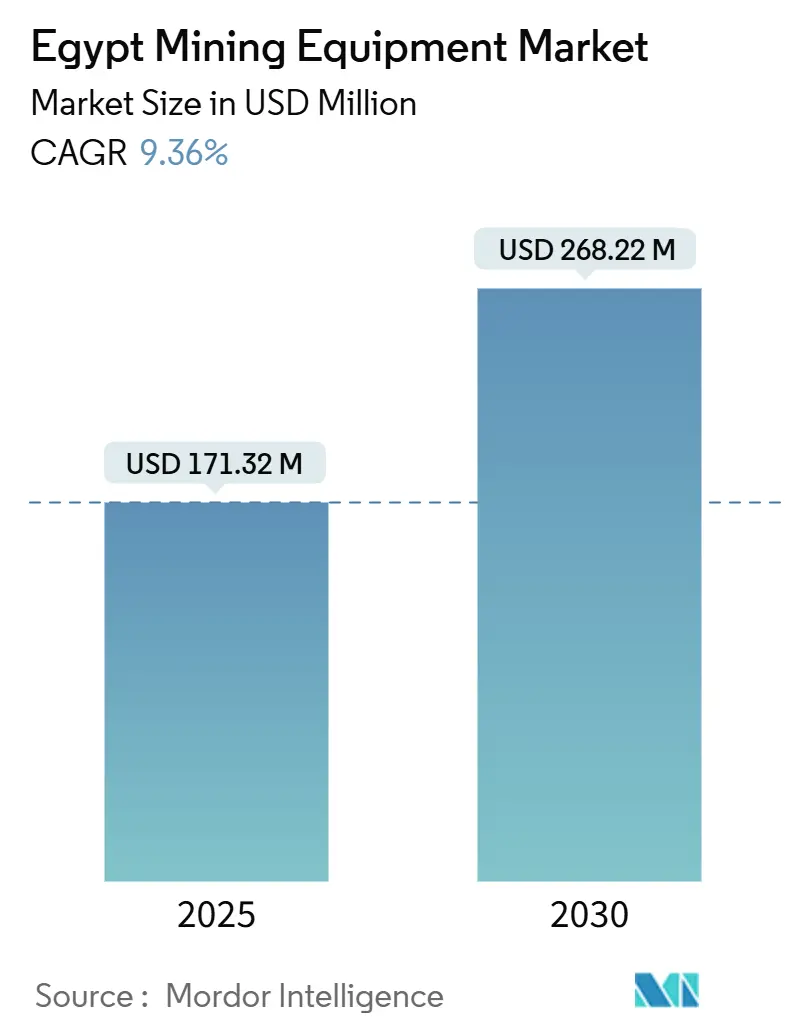

| Market Size (2025) | USD 171.32 Million |

| Market Size (2030) | USD 268.22 Million |

| Growth Rate (2025 - 2030) | 9.36% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Mining Equipment Market Analysis by Mordor Intelligence

The Egypt mining equipment market size stood at USD 171.32 million in 2025 and is forecast to expand to USD 268.22 million by 2030, registering a 9.36% CAGR. A sharp government pivot toward mining-driven diversification, investment pledges topping USD 375 million in the past two years, and the post-2019 Mining Law have combined to accelerate exploration licensing, spur fleet modernization, and draw global OEMs toward battery-electric and autonomous offerings. Rising surface extraction of gold and phosphate, aggressive replacement of aging haul-age vehicles, and project-linked demand for specialized mineral-processing lines underpin a sustained uptake of mid-range 500 to 1,000 HP equipment. Currency volatility, however, inflates imported unit costs, nudging operators toward rental, lease, and service-centric procurement while encouraging select local assembly.

Key Report Takeaways

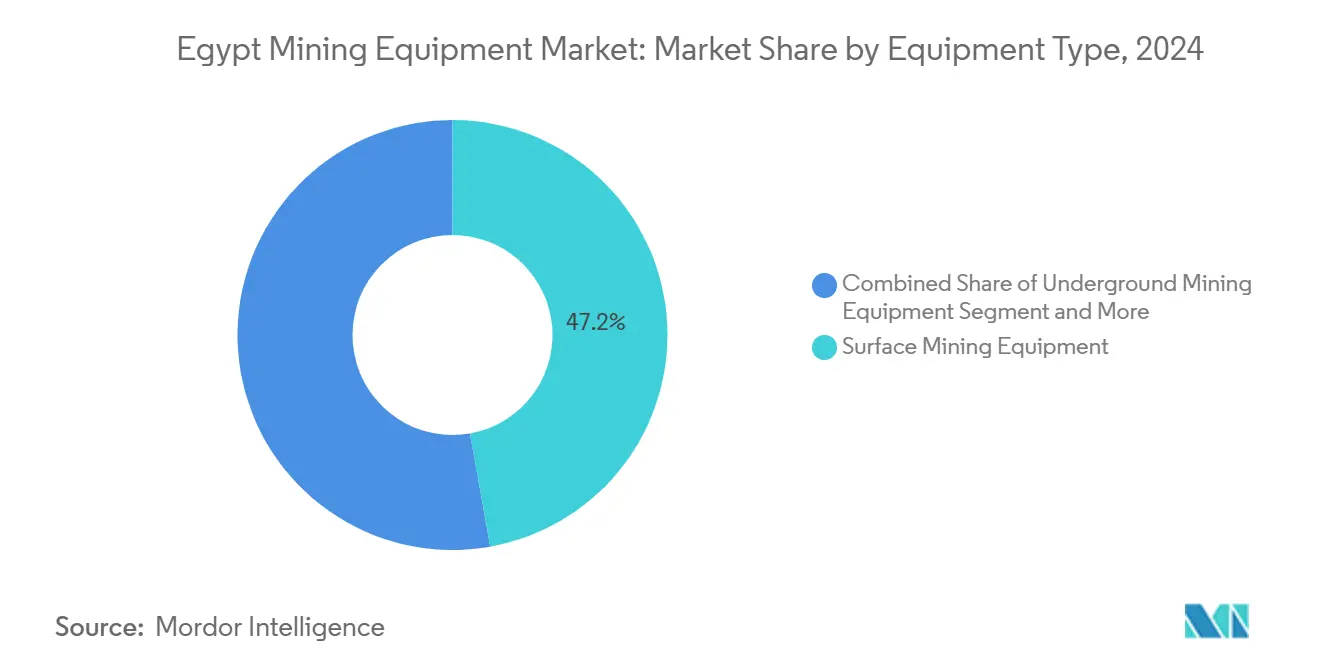

- By equipment type, surface mining systems commanded 47.21% of Egypt mining equipment market share in 2024, whereas battery-electric loaders are projected to post a 16.23% CAGR to 2030.

- By automation level, manual machines dominated with 71.08% share in 2024, while fully autonomous units are poised for an 18.47% CAGR through 2030.

- By powertrain, internal-combustion fleets held 82.14% of the Egypt mining equipment market size in 2024, but battery-electric vehicles are forecast to expand at an 18.96% CAGR to 2030.

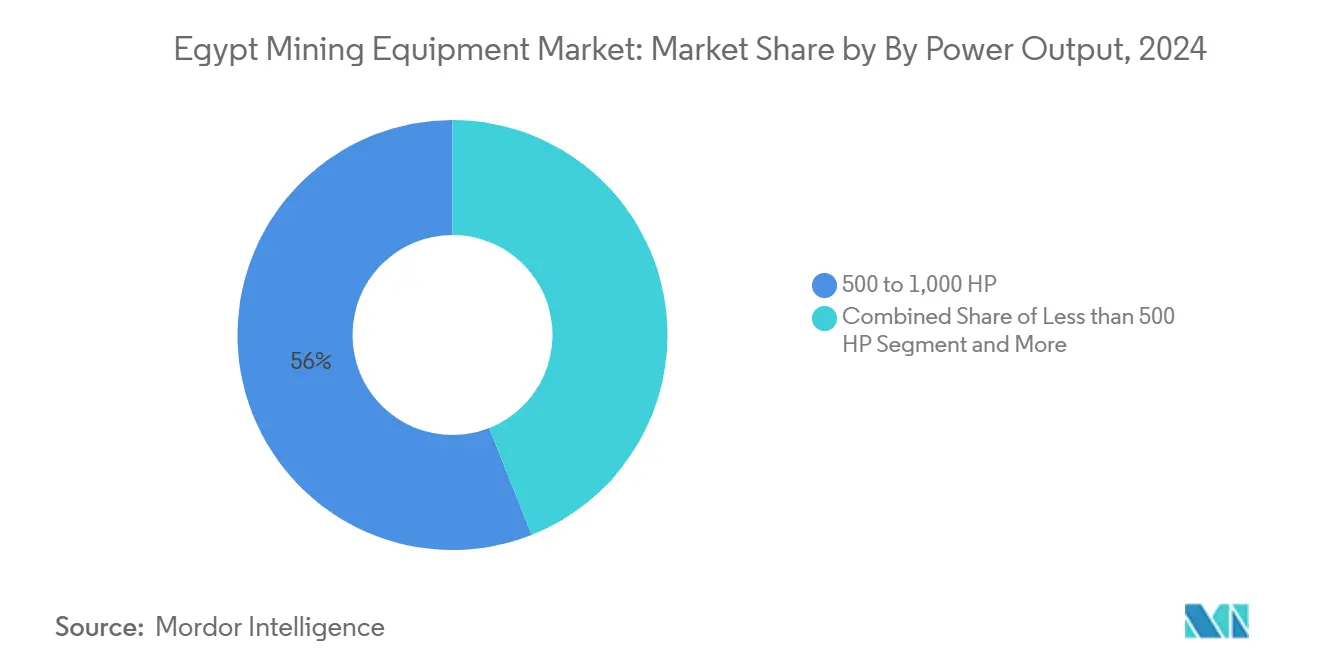

- By power output, 500 to 1,000 HP machines captured 56.04% of demand in 2024, whereas sub-500 HP models are set to rise at a 12.09% CAGR through 2030.

- By application, mineral mining led with a 49.06% share of the Egypt mining equipment market size in 2024; metal mining is projected to advance at a 10.31% CAGR between 2025 and 2030.

- By geography, Cairo and the Suez Canal led with a 61.32% share in 2024, while the Nile Delta region is projected to register the highest demand CAGR of 11.23% through 2030.

Egypt Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Push to Raise Mining to 5 to 6% of GDP by 2030 | 2.1% | National, with concentration in Eastern Desert and Golden Triangle | Long Term (≥ 4 Years) |

| Growing Gold and Phosphate Exploration Licenses Post-2019 Mining Law | 1.8% | Eastern Desert, Western Desert, Sinai Peninsula | Medium Term (2–4 Years) |

| High Replacement Demand for Aging Surface-Mine Fleets | 1.2% | National, particularly existing mining regions | Short Term (≤ 2 Years) |

| Rise of Rental/Leased Equipment to Defer Capex | 0.9% | Cairo and Suez Canal Zone, Alexandria Region | Medium Term (2–4 Years) |

| Upcoming Green-Hydrogen Projects Needing Iron-Ore and Phosphate Inputs | 0.8% | Suez Canal Economic Zone, Red Sea Coastal Areas | Long Term (≥ 4 Years) |

| On-Site Solar-Plus-Storage Driving Battery-Electric Haul Trucks | 0.6% | National, with early adoption in major mining operations | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Government Push to Raise Mining to 5-6% of GDP by 2030

Egypt's systematic mining elevation from a peripheral economic activity to a strategic growth pillar represents a fundamental shift that will reshape equipment demand patterns through the decade. The government's commitment to achieving 5-6% GDP contribution by 2030, compared to the sector's current contribution, requires an estimated USD 1 billion in total investments over the forecast period, with equipment procurement representing approximately 40-45% of this capital allocation[1]"Egypt discovers gold deposit of over 1 million ounces in Eastern Desert," ahram.org.eg.. This target necessitates incremental capacity additions and a complete modernization of extraction capabilities across gold, phosphate, iron ore, and emerging rare earth operations. The Ministry of Petroleum and Mineral Resources' establishment of dedicated mining complexes in the Eastern Desert (gold), Western Desert (phosphate), and Sinai (copper) creates concentrated demand nodes that favor standardized equipment procurement strategies. The government's parallel focus on value-added processing rather than raw material exports further amplifies equipment intensity, as downstream beneficiation requires sophisticated crushing, screening, and separation technologies. Most significantly, this GDP target embeds mining equipment demand into Egypt's broader economic planning framework, ensuring sustained policy support and budget allocation even during periods of fiscal constraint.

Growing Gold and Phosphate Exploration Licenses Post-2019 Mining Law

The 2019 Mining Law's transition from production-sharing agreements to a taxes-and-royalties framework has unleashed a wave of exploration activity that directly translates into drilling equipment demand and subsequent extraction infrastructure requirements. The award of 82 gold exploration blocks to 11 companies in 2024 represents the largest global tender for gold exploration, signaling a systematic approach to resource development that will require sustained equipment deployment over multiple phases[2]"11 International and Egyptian Companies Win 82 Gold Exploration Zones in Egypt in the Largest Global Bid," emra.gov.eg.. This regulatory shift eliminates the previous requirement for joint ventures with government entities, enabling international mining companies to deploy their preferred equipment specifications and maintenance protocols without bureaucratic constraints. The law's 5% royalty structure and corporate social responsibility fee create predictable cost structures that facilitate long-term equipment financing arrangements, particularly for capital-intensive surface mining operations. Phosphate exploration in the Abu Tartour region, with estimated reserves approaching 1 billion tons, positions Egypt as a potential global supplier, requiring large-scale extraction equipment capable of handling the projected 5 million tons per year production capacity[3]Doaa Ashraf, "The Rock Beneath the Rise: Phosphate Fuels Egypt’s Industrial Ambitions," egyptoil-gas.com.. The exploration-to-production timeline typically spans 3-5 years, suggesting that current exploration activities will drive equipment procurement cycles beginning in 2026-2027, creating a sustained demand pipeline that extends well beyond the immediate forecast period.

High Replacement Demand for Aging Surface-Mine Fleets

Egypt's surface mining operations, concentrated primarily in iron ore extraction at El Gedida and phosphate mining in the Red Sea region, operate equipment fleets with an average age approaching 12-15 years, well beyond the optimal economic replacement threshold of 8-10 years for harsh desert operating conditions. The economic replacement time model for mining equipment in similar geological conditions suggests that maintenance costs begin to escalate exponentially after 115 months of operation, creating compelling replacement economics for operators seeking to optimize total ownership costs. The harsh operating environment of Egypt's desert regions, characterized by extreme temperature variations, abrasive sand conditions, and limited maintenance infrastructure, accelerates equipment degradation compared to more temperate mining regions. Surface mining equipment replacement in Egypt typically involves upgrading to higher-capacity, more fuel-efficient units that can handle the increasing scale of operations as reserves are developed more intensively. The replacement cycle also coincides with operators' transition toward more automated and electrified equipment, as aging diesel-powered units are replaced with hybrid or battery-electric alternatives that offer superior operational economics in Egypt's high-solar-irradiation environment.

Rise of Rental/Leased Equipment to Defer Capex

The shift toward equipment rental and leasing arrangements in Egypt's mining sector reflects both capital preservation strategies amid currency volatility and the operational flexibility required for exploration-phase activities that may not justify full equipment ownership. Mining companies increasingly favor rental arrangements for specialized equipment such as drilling rigs, crushing units, and material handling systems during exploration and early-stage development phases, when production volumes and ore characteristics remain uncertain. The rental model proves particularly attractive for international mining companies entering the Egyptian market, as it eliminates the complexities of equipment importation, customs clearance, and local regulatory compliance while providing access to maintained equipment with local technical support. Currency hedging benefits also drive rental adoption, as rental agreements denominated in Egyptian pounds provide natural currency protection compared to outright equipment purchases that require hard currency outlays. The emergence of performance-based rental contracts, where equipment availability and productivity metrics determine rental rates, aligns operator and rental company incentives while transferring maintenance risks to specialized service providers with deeper technical expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Volatility Inflating Imported Equipment Cost | -1.4% | National, with acute impact on import-dependent operations | Short Term (≤ 2 Years) |

| Fragmented Small-Scale Mines Limiting Autonomous Uptake | -0.8% | National, particularly affecting smaller regional operations | Medium Term (2–4 Years) |

| Slow Rail-Logistics Upgrades for Bulk Minerals | -0.7% | National, especially Upper Egypt and remote mining corridors | Medium Term (2–4 Years) |

| Limited Local Component Manufacturing Base (Under-the-Radar) | -0.5% | National, with pronounced effects in maintenance-intensive sites | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Currency Volatility Inflating Imported Equipment Cost

Egypt's foreign currency crisis has created a structural impediment to mining equipment procurement, with the Egyptian pound's devaluation making imported machinery prohibitively expensive for many operators and creating payment difficulties that have strained relationships with international suppliers. The U.S. Department of Commerce reports that Egyptian buyers face significant challenges meeting financial obligations to American companies, with stringent banking requirements for import financing complicating the procurement of essential mining machinery and components. This currency instability has forced mining companies to defer equipment upgrades and rely on extended maintenance cycles for aging equipment, ultimately reducing operational efficiency and increasing safety risks. The impact extends beyond initial equipment purchases to spare parts availability, as distributors struggle to maintain adequate inventory levels when currency fluctuations can erode profit margins overnight. Mining companies have responded by seeking alternative financing arrangements, including supplier credit facilities and lease-to-own structures that denominate payments in local currency, though these arrangements typically carry premium pricing that reflects currency risk. The government's efforts to stabilize the exchange rate through IMF-supported reforms provide some optimism, but the mining equipment market remains vulnerable to currency shocks that can rapidly alter project economics and equipment procurement timelines.

Fragmented Small-Scale mines Limiting Autonomous Uptake

The prevalence of small-scale mining operations across Egypt's diverse geological landscape creates a market structure that inherently resists the adoption of advanced autonomous mining technologies, which require substantial scale and standardization to achieve economic viability. Unlike large-scale operations such as Centamin's Sukari mine, which can justify the capital investment and technical infrastructure required for autonomous systems, Egypt's numerous smaller gold, phosphate, and industrial mineral operations lack the production volumes and technical sophistication necessary to support advanced automation. The fragmented nature of these operations also limits the development of specialized technical service networks that autonomous equipment requires, as service providers cannot achieve sufficient density of installations to justify local technical support capabilities. Small-scale operators typically prioritize equipment simplicity and maintainability over productivity optimization, favoring conventional manual equipment that can be serviced by local technicians rather than sophisticated autonomous systems that require specialized training and diagnostic equipment. This market fragmentation also impedes the standardization of operating procedures and safety protocols that autonomous systems require to function effectively across multiple sites. The economic threshold for autonomous equipment adoption typically requires operations processing at least 10,000-15,000 tons per day, a scale that few Egyptian mining operations currently achieve outside of the major gold and phosphate projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Operations Drive Market Leadership

Surface mining equipment's 47.21% market share in 2024 reflects Egypt's geological endowment and the economic advantages of open-pit extraction across the country's significant mineral deposits. The Eastern Desert's gold operations, Western Desert's phosphate reserves, and Sinai's copper deposits predominantly favor surface extraction due to their geological characteristics and the cost-effectiveness of large-scale open-pit operations in Egypt's arid climate. Battery-electric loaders emerge as the fastest-growing segment within surface equipment at 16.23% CAGR through 2030, driven by Centamin's pioneering 30MW solar power integration at the Sukari Gold Operation and similar renewable energy initiatives across the sector.

Underground mining equipment captures a smaller but strategically important segment, primarily serving the deeper gold deposits in the Eastern Desert and specialized applications in rare earth extraction. Mineral processing equipment benefits from Egypt's strategic shift toward value-added production rather than raw material exports, with the USD 172 million silicon complex in New Alamein exemplifying this trend toward downstream processing. Drills and breakers experience steady demand growth driven by the 82 gold exploration blocks awarded in 2024, while crushing, pulverizing, and screening equipment align with the government's emphasis on beneficiation and value addition. The loaders and haul trucks segment reflects the capital-intensive nature of Egypt's surface mining expansion, with replacement cycles accelerating as operators upgrade aging fleets to meet higher production targets and environmental standards.

By Automation Level: Manual Dominance Faces Autonomous Disruption

Manual equipment's substantial 71.08% market share in 2024 underscores the current state of Egypt's mining sector, where operational simplicity and maintenance accessibility outweigh productivity optimization for most operators. However, fully autonomous equipment's aggressive 18.47% CAGR through 2030 signals a fundamental shift as larger operations seek to address skilled labor shortages and enhance operational safety in Egypt's challenging desert environment. Epiroc's expansion of automation solutions, including deploying 3,450 driverless machines globally, provides a technological foundation that Egyptian operators can leverage as they scale operations.

Semi-autonomous equipment is a transitional category, allowing operators to implement graduated automation strategies that balance productivity gains with operational familiarity. The automation adoption pattern in Egypt reflects the broader global mining trend, where autonomous vehicles have grown significantly, indicating a proven pathway for technology deployment. The economic justification for autonomous systems strengthens as Egyptian mining operations achieve greater scale, with the government's 5-6% GDP target necessitating productivity improvements that manual operations cannot deliver. The concentration of mining activities in remote desert locations also favors autonomous systems, which can operate continuously without the logistical challenges of maintaining large workforces in harsh environments.

By Powertrain Type: ICE Dominance Yields to Electric Innovation

Internal combustion engine vehicles maintain 82.14% market control in 2024, reflecting Egypt's current mining fleet's established infrastructure and operational familiarity. Yet battery-electric vehicles' remarkable 18.96% CAGR through 2030 represents the most significant technological transition in the market, driven by Egypt's exceptional solar resources and the operational cost advantages of electric powertrains in high-utilization mining applications. The global mining industry's forecast to retrofit 1 million diesel mining vehicles to electric by 2030 provides context for Egypt's electrification potential.

Hybrid vehicles occupy a strategic middle ground, allowing operators to capture fuel efficiency benefits while maintaining operational flexibility for applications where pure electric solutions may not be economically viable. Integrating on-site solar generation with battery-electric mining equipment creates compelling economics in Egypt's high-irradiation environment, where solar capacity factors exceed 25% and provide predictable energy costs that insulate operators from fuel price volatility. Caterpillar's introduction of fully electric mine truck prototypes and the broader industry shift toward zero-emission vehicles align with Egypt's renewable energy targets and provide a technology roadmap for Egyptian operators. The electrification trend also supports Egypt's green hydrogen ambitions, as mining operations can serve as anchor loads for renewable energy projects while providing the iron ore and phosphate inputs required for hydrogen production infrastructure.

By Power Output: Mid-Range Equipment Dominates Operational Sweet Spot

Equipment in the 500 to 1,000 HP range captured 56.04% of the market share in 2024, reflecting the operational requirements of Egypt's major surface mining operations, where this power class provides optimal productivity for the scale and geological conditions encountered across the country's mineral deposits. Less than 500 HP equipment's 12.09% CAGR through 2030 indicates growing demand for specialized applications, including exploration drilling, auxiliary operations, and the emerging rare earth extraction activities that require more precise, lower-intensity processing approaches.

Above 1,000 HP equipment serves the most significant operations, including primary phosphate extraction in the Western Desert and the most intensive gold mining operations in the Eastern Desert. The power output segmentation reflects Egypt's mining sector maturity, where established operations have optimized equipment sizing for their specific geological and operational requirements. The growth in smaller power classes aligns with the diversification of Egypt's mineral portfolio beyond traditional gold and phosphate extraction, including copper, rare earths, and industrial minerals that may require different operational approaches. Equipment manufacturers' focus on fuel efficiency and operator comfort, exemplified by Volvo's new A50 articulated hauler, addresses the total cost of ownership considerations that drive power class selection in Egypt's competitive mining environment.

By Application: Mineral Mining Leads Diversified Portfolio

Mineral mining's 49.06% market share in 2024 reflects Egypt's diversified geological endowment, encompassing phosphate operations in the Western Desert, industrial minerals extraction across multiple regions, and the emerging rare earth potential identified in the Abu Tartour area and Eastern Desert granites. Metal mining's 10.31% CAGR through 2030 signals the sector's strategic importance, driven by gold production expansion, copper development in Sinai, and the potential for iron ore intensification to support green hydrogen projects.

Coal mining represents a smaller segment, primarily concentrated in the northeast Sinai deposits, though its role may expand as Egypt seeks energy security and industrial feedstock diversification. The application segmentation underscores Egypt's strategic positioning as a diversified mineral producer rather than a single-commodity dependent economy. Metal mining's accelerated growth reflects both the high-value nature of gold and copper extraction and the government's focus on attracting international mining companies with advanced extraction capabilities. The discovery of over 1 million ounces of gold deposits in the Eastern Desert and the establishment of dedicated mining complexes for different commodities create application-specific equipment demand patterns that favor specialized rather than generic mining solutions.

Geography Analysis

Cairo and the Suez Canal Zone dominate import logistics, funnelling more than 60% of inbound units through Alexandria and Adabiya ports before rail or road dispatch to mining zones. Proximity to the USD 42 billion green-hydrogen corridor positions the district as a service hub combining warehousing, component remanufacturing, and training academies. The World Bank-financed Cairo–Alexandria rail bypass improves bulk mineral transit, trimming journey times and lowering equipment relocation costs.

The Eastern Desert is the nation’s mining epicenter, hosting Sukari Gold Mine and the newly identified 1-million-ounce deposit. Equipment demand here emphasizes high-capacity surface fleets, solar-integrated power-trains, and dust-resistant electrical enclosures suitable for abrasive conditions. AngloGold Ashanti’s post-acquisition modernization plan is set to create one of the region’s largest integrated fleets, setting technical benchmarks for Egypt mining equipment market participants.

Upper Egypt and the Western Desert pivot around Abu Tartour’s phosphate belt. Long-life 5 million t/y extraction supports sustained procuring draglines, in-pit crushers, and beneficiation trains designed for low-moisture ore. The relative remoteness drives reliance on dealer field-service trucks and predictive-maintenance telemetry to minimize unplanned stoppages.

Sinai and the Red Sea corridor offer copper, uranium, and heavy-mineral sand prospects but trail in infrastructure and security stability, tempering immediate equipment volumes. Nevertheless, targeted state support could unlock investments once transport links and power supply improve. The Nile Delta’s mineral-sands dredging potential introduces specialized dredgers and floating concentrators, adding a maritime dimension to Egypt's mining equipment market growth.

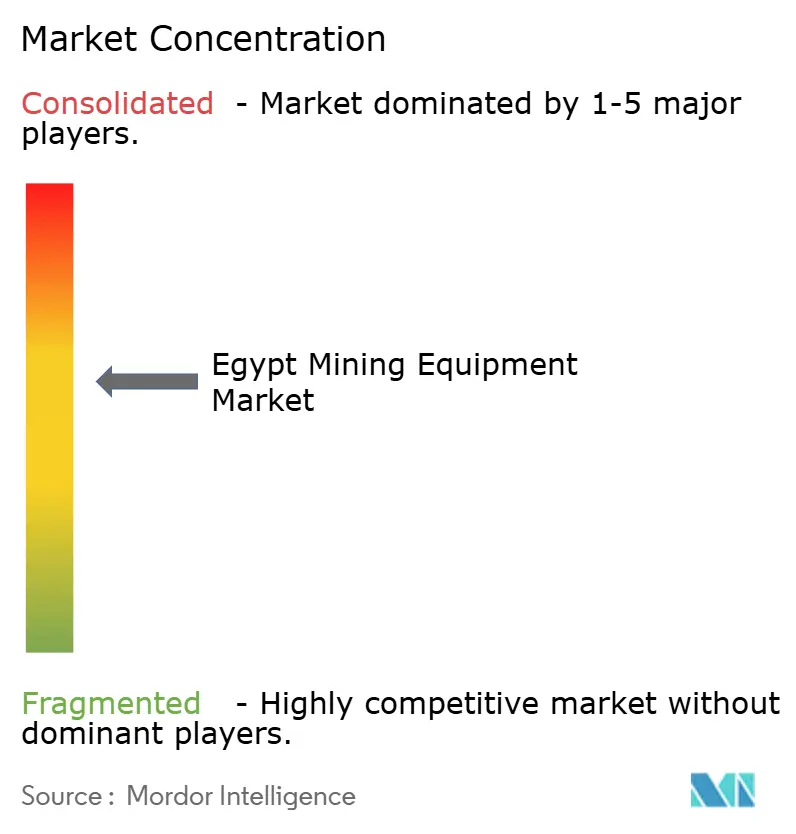

Competitive Landscape

The Egyptian mining equipment market remains moderately fragmented, as global OEMs such as Caterpillar, Komatsu, Sandvik, Liebherr, and Epiroc vie with emerging Chinese brands offering budget-oriented alternatives. Caterpillar benefits from its extensive Mantrac Egypt dealership, stocking full-line parts and 24-hour service. Komatsu leverages hybrid haul truck technology to court operators, balancing capex and fuel savings.

Technology capabilities define share battles. Epiroc’s portfolio of safety-rated automation modules secures pilot contracts for autonomous blast-hole drills, while Sandvik positions its battery-electric underground loaders for deep gold projects. Given import lead times and currency constraints, aftermarket support—including condition monitoring and component overhaul—becomes decisive. Local assembly discussions between OEMs and Egyptian partners could provide cost relief and local-content benefits, provided adequate volume commitments materialize.

White-space opportunities lie in electrification ecosystems: charging infrastructure, lithium-iron-phosphate battery supply chains, and solar micro-grids calibrated for high-load cycles. Service-wrapped equipment leases further differentiate suppliers, shifting investment risk from mine to OEM while ensuring steady component off-take.

Egypt Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Sandvik AB

-

Epiroc AB

-

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Sukari Gold Mine received government endorsement for growth prospects, indicating potential equipment expansion and modernization initiatives at Egypt's flagship mining operation.

- October 2024: AngloGold Ashanti's USD 2.5 billion takeover of Centamin received Egyptian government approval, creating the potential for significant equipment modernization and standardization across Egypt's largest gold mining operation while maintaining the government's 50% profit-sharing arrangement.

Egypt Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 to 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| Cairo and Suez Canal Zone |

| Alexandria and Northern Coast |

| Upper Egypt |

| Sinai and Red Sea |

| Nile Delta |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 to 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Geography | Cairo and Suez Canal Zone |

| Alexandria and Northern Coast | |

| Upper Egypt | |

| Sinai and Red Sea | |

| Nile Delta |

Key Questions Answered in the Report

What is the current value of Egypt mining equipment market?

The Egypt mining equipment market size is USD 171.32 million in 2025.

How fast is the market expected to grow through 2030?

The market is projected to register a 9.36% CAGR, reaching USD 268.22 million by 2030.

Which equipment type commands the largest share?

Surface mining machines lead with 47.21% of 2024 revenue.

Which powertrain segment is growing the fastest?

Battery-electric vehicles are forecast to expand at an 18.96% CAGR through 2030.

What regional zone generates the highest equipment demand?

The Eastern Desert holds the highest forward equipment demand growth, projected at 11.2% CAGR.

What is the main risk to equipment procurement in Egypt?

Currency volatility, which has increased imported equipment prices by up to 30% since 2024, is the leading risk.

Page last updated on: