Saudi Arabia Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

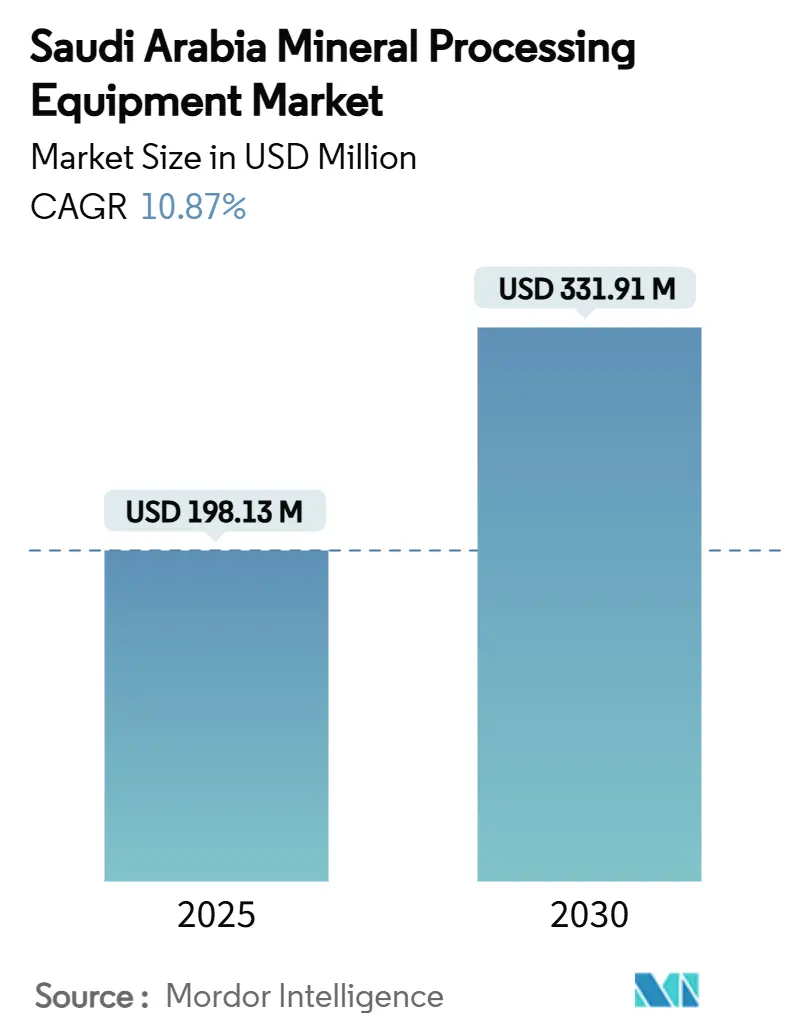

| Market Size (2025) | USD 198.13 Million |

| Market Size (2030) | USD 331.91 Million |

| Growth Rate (2025 - 2030) | 10.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Saudi Arabia mineral processing equipment market size is valued at USD 198.13 million in 2025, and it is forecast to expand to USD 331.91 million by 2030, reflecting a 10.87% CAGR to 2030. Substantial government investment, Vision 2030 localization incentives, and rising demand for battery-grade minerals underpin the near-double-digit growth pace. Ma’aden’s multi-commodity expansions, a USD 100 billion national mining investment pledge, and accelerating EPC contract awards at NEOM are consolidating capital flows toward new beneficiation plants and digitalized processing lines. Equipment suppliers align portfolios with electric-drive, AI-enabled, and low-water-consumption designs to meet energy-cost and sustainability mandates. International OEMs are partnering with Saudi conglomerates to satisfy stringent in-country-value thresholds while mitigating import-related lead-time risks. Fragmented exploration licenses across the Arabian Shield create a pipeline of greenfield projects requiring crushing, milling, and classification systems over the next five years.

Key Report Takeaways

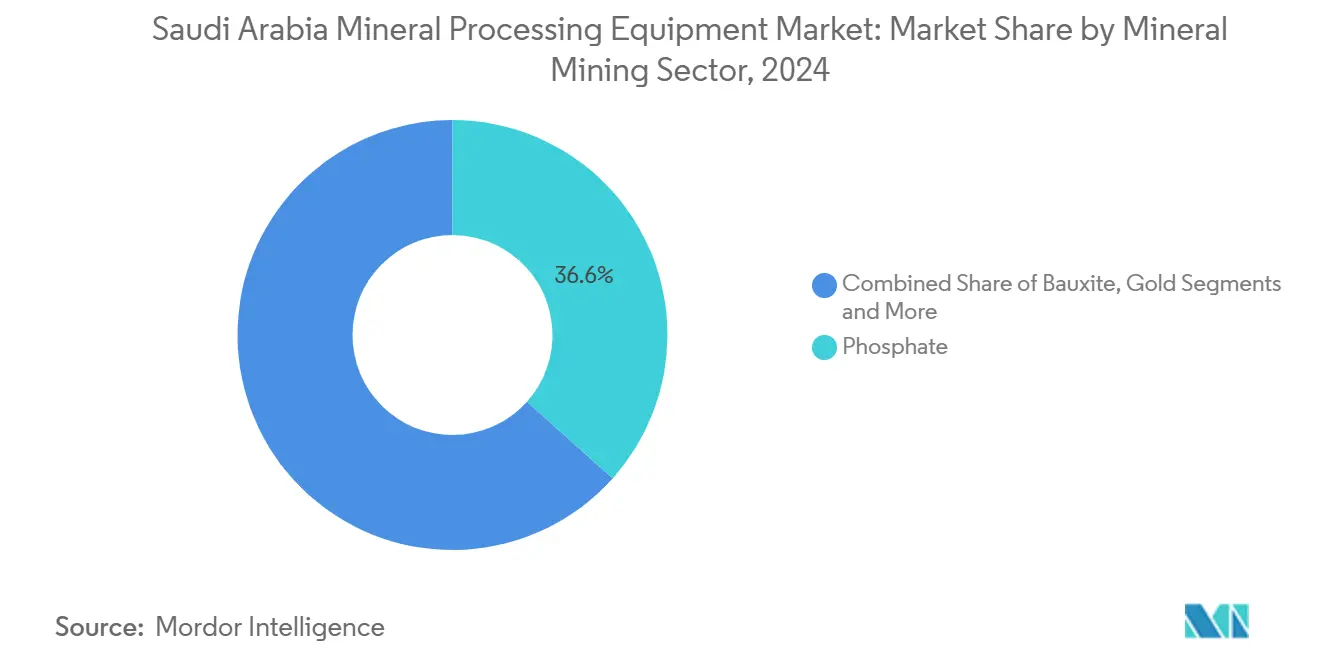

- In the mineral mining sector, phosphate processing led with 36.62% revenue share in 2024, while lithium recorded the fastest CAGR at 10.26% through 2030.

- By equipment type, crushers and mills accounted for 35.38% of the Saudi Arabia mineral processing equipment market share in 2024; pumps and cyclones are projected to post the highest 10.93% CAGR to 2030.

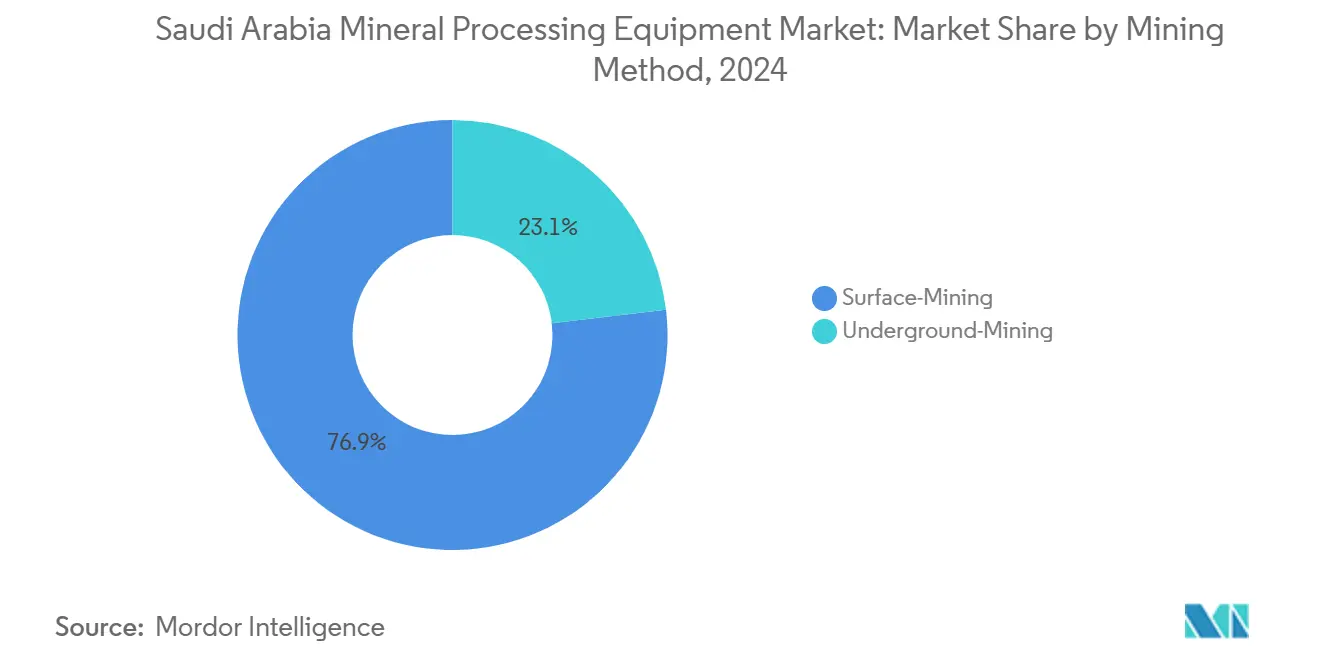

- By mining method, surface extraction controlled 76.87% share of the Saudi Arabia mineral processing equipment market size in 2024, whereas underground techniques are advancing at an 11.28% CAGR to 2030.

- By automation level, semi-automated systems held a 53.28% share in 2024, yet fully automated solutions are expanding at a 13.83% CAGR through 2030.

- By province, Eastern Province captured 41.19% revenue in 2024, and Tabuk is forecast to grow at 12.84% CAGR between 2025 and 2030.

Figures recorded within Saudi arabia feed into a worldwide estimate while studying the global industry. Mordor Intelligence's mineral processing equipment market size captures this aggregation.

Saudi Arabia Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phosphate and bauxite project surge | +2.8% | Eastern Province, Al-Madinah | Medium term (2-4 years) |

| Vision 2030 localization push | +2.1% | National, with early gains in Eastern Province, Riyadh | Long term (≥ 4 years) |

| NEOM EPC contracts | +1.9% | Tabuk, spill-over to Northern regions | Medium term (2-4 years) |

| Electrified crushing and grinding | +1.6% | National, concentrated in major mining hubs | Short term (≤ 2 years) |

| AI predictive-maintenance uptake | +1.4% | Eastern Province, Riyadh, expanding nationally | Short term (≤ 2 years) |

| Ma’aden and JV exploration surge | +1.0% | National, focused on Arabian Shield regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Phosphate and Bauxite Extraction Projects

Ma’aden processes 11.6 million t/y of phosphate ore at Al Jalamid and Ras Al Khair and is adding capacity to reach 16 million t/y under the Wa’ad Al-Shamal expansion[1]“Ma’aden Expands Phosphate Output to 16 Mtpa,”, Al Arabiya English, alarabiya.net. The growing demand for bauxite also drives demand for crushing, grinding, and alumina calcination systems. Revised national resource estimates of USD 2.5 trillion have triggered 73 new exploration licences, intensifying equipment tenders across Eastern Province, where rail and port links minimize logistics cost for oversized machinery. The Saudi Arabia mineral processing equipment market is therefore receiving sustained orders for high-capacity beneficiation lines capable of handling abrasive phosphate and bauxite ores without productivity losses

Vision 2030 Downstream-Mining Localization Incentives

The National Industrial Development and Logistics Program targets local content in supply chains by 2030, creating preferential procurement for OEMs that establish domestic assembly or transfer technology to Saudi partners[2]“Mining Localization Initiatives,”, NIDLP, nidlp.gov.sa. A USD 182 million Exploration Enablement Program launched in 2024 grants fee waivers for companies meeting localization milestones, prompting Metso, Sandvik, and Weir to announce joint facilities with the Olayan and Rasi groups. Local content criteria now extend to spare-parts casting, pump refurbishment, and mill liner production, ensuring long-term aftermarket revenue stays within the Kingdom. Such policy certainty bolsters the Saudi Arabia mineral processing equipment market because international suppliers can justify capex for local service workshops that shorten downtime for Ras Al Khair and Wa’ad Al-Shamal users.

AI-Enabled Predictive-Maintenance Adoption

Ma’aden and Hexagon are building the region’s first digital mine, layering AI algorithms over sensors that track real-time vibration, temperature, and cyclone feed density [3]“Hexagon and Ma’aden Launch Middle East’s First Digital Mine,”, Mining.com, mining.com. Early deployments cut unscheduled downtime by 40% and optimize reagent dosing, widening recovery margins. Because Saudi Arabia faces a shortage of certified automation engineers, self-learning platforms are critical to scaling operations without a proportional rise in specialist headcount. OEMs now bundle machine-learning dashboards with new pumps, mills, and screens, embedding the Saudi Arabia mineral processing equipment market with software revenues that compound hardware sales.

Upsurge in Ma’aden and JV Exploration Spending

Ma’aden’s 2025 exploration budget ranks among the top 10 global miners, focusing on the mineral-rich Arabian Shield and joint ventures that de-risk early resource delineation. More than SAR 685 million in grant funding supports geophysics, drilling, and core testing, creating continuous demand for core cutting, sample prep, and pilot flotation units supplied under rental or sale. These programs feed the project pipeline expected to require full-scale processing plants within the forecast window, underpinning steady growth in the Saudi Arabia mineral processing equipment marke

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy permit process | -1.8% | National, particularly remote mining areas | Medium term (2-4 years) |

| High remote-power tariffs | -1.2% | Remote areas in Tabuk, Al-Madinah, Northern regions | Short term (≤ 2 years) |

| Automation-engineer shortage | -1.0% | National, concentrated in Eastern Province, Riyadh | Long term (≥ 4 years) |

| Import wear-part delays | -0.8% | National, affecting all mining operations | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Lengthy Environmental-Permit Lead-Times

Comprehensive impact assessments now stretch mine-development timelines by 18-24 months as multiple agencies require hydrology, biodiversity, and community-risk studies before construction can begin[4]“Jabal Sahabiyah Permitting Update,”, Royal Road Minerals Limited, royalroadminerals.com. Processing-plant orders, particularly for cyanidation and flotation circuits, cannot be released until permits are secure, delaying cash-flow and straining OEM forecasting. Lithium projects chasing electric-vehicle supply deals are most sensitive to these lags, exposing the Saudi Arabia mineral processing equipment market to deferred revenues unless fast-track assessment protocols materialize.

Lead-Time Delays from Import-Dependent Wear Parts

Saudi foundry capacity for high-chrome grinding media and rubber pump liners remains limited. Extended global shipping cycles can stretch mill liner replacement to 14 weeks, forcing operators to hold excess inventory or accept output losses. Local casting expansions under Vision 2030 are underway but will not relieve bottlenecks before 2027, constraining the Saudi Arabia mineral processing equipment market’s aftermarket potential in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Lithium Rises as Battery Ambitions Scale

Saudi Arabia's mineral processing equipment market for phosphate retained the largest 36.62% share in 2024, anchored by Ma’aden’s beneficiation plants, which process 5 million t/y of concentrate with 213 million t of reserves. Continuous flotation upgrades, high-capacity thickeners, and acid-grade filter presses protect phosphate leadership.

Lithium, however, is forecast to post the strongest 10.26% CAGR, reflecting the Kingdom’s goal of assembling 500,000 electric vehicles per year by 2030 and BMW-qualified lithium hydroxide output via the Obeikan–Critical Metals plant. Pilot solvent-extraction circuits, vertical pressure filters, and crystallizers dominate recent tender lists, and EPC contractors are bundling them with renewable-powered kilns to comply with net-zero targets. Bauxite, gold, copper, and emerging iron-ore projects diversify the Saudi Arabia mineral processing equipment market, yet none match lithium’s proportional uplift in new orders through 2030.

By Equipment Type: Pumps, Cyclones, and Smart Crushing Lead Technology Shifts

Crushers and mills captured 35.38% of the Saudi Arabia mineral processing equipment market share in 2024 thanks to Ma’aden’s Ras Al Khair debottlenecking that required larger SAG mills and cone crushers. Growth now tilts toward pumps and cyclones, expected to climb at 10.93% CAGR, because fine grind and regrind circuits rely on precise particle-size control as ore grades decline.

Electrified track-mounted crushers, regenerative conveyors, and variable-speed mills reflect a pivot to energy-optimized flowsheets. Remote-monitoring sensors embedded in slurry pumps feed AI dashboards that predict liner wear, lowering life-cycle cost for operators facing high import duties on replacement parts. Drills and breakers advance moderately under the USD 182 million Exploration Enablement Program, while “other” categories—autonomous sample stations, cloud-ready PLCs, and spectroscopic ore sorters—gain traction as technology suppliers leverage Saudi Arabia mineral processing equipment industry pilots to secure long-term contracts.

By Mining Method: Underground Equipment Demand Grows from Greenfield Discoveries

Surface mines still dominated 76.87% of sector revenue in 2024, supported by low strip ratios at Al Jalamid’s open pits where semi-mobile crushers feed overland conveyors to the plant gate. This capital-efficient model will persist for bulk phosphate and bauxite.

Underground methods are projected to expand at an 11.28% CAGR as deeper copper-zinc and gold lenses across the Arabian Shield require jumbo drills, LHDs, and battery-electric loaders. Battery propulsion delivers ventilation savings and smaller tunnel profiles, advantages that OEMs highlight to justify higher upfront investment. Pilot declines at the Mahd Ad Dahab and Al-Amar deposits validate interiors with grades that offset higher mining cost, bolstering orders for narrow-vein crushers, paste backfill pumps, and rapid-extraction hoists inside the Saudi Arabia mineral processing equipment market.

By Automation Level: Digital Mines Shift from Supervised to Autonomous

Semi-automated workflows held 53.28% share in 2024, leveraging centralized control rooms where human operators adjust density, pH, and grind size through HMI screens while field crews still perform shovel inspections. The model balances productivity with available skill sets.

Fully automated solutions are gathering momentum with 13.83% CAGR, as predictive-maintenance algorithms trained on vibration and slurry samples enable lights-out secondary crushing, automated reagent dosing, and robotic mill relining. Hexagon’s digital-mine alliance demonstrates 10% throughput gains at pilot scale, and FLSmidth’s ECS/ControlCenter installations prepare Saudi teams for remote support. Manual processes now represent a declining niche, retained only where geological judgement and complex maintenance tasks still justify human oversight.

Geography Analysis

Eastern Province leads the Saudi Arabia mineral processing equipment market, with a 41.19% stake in 2024. Ras Al Khair’s multi-commodity zone funnels demand for flotation cells, acid reactors, and alumina calciners. Deepwater port access optimizes exports, while integration with the North-South Railway lowers inbound heavy-machinery logistics costs.

Tabuk’s 12.84% CAGR outlook is anchored by NEOM’s construction materials pipeline and newly approved quarry licences covering 49 applications across sand and gravel complexes. The province’s renewable-energy build-out aligns with OEM offerings in electric crushers and beltless slurry pumps designed for low-carbon footprints.

Riyadh, Makkah, and Al-Madinah are driven by headquarters spending, tourism-related infrastructure, and drilling programs financed under the SAR 685 million Exploration Enablement Program. Completing 50% of the Arabian Shield survey by 2025 is likely to open new gold-copper corridors, trigger additional plant orders for gravity separation, cyanidation, and smelting equipment, and distribute the Saudi Arabia mineral processing equipment market benefits nationwide.

Mordor Intelligence evaluates the mineral processing equipment market with deeper country-level insights covering France, Spain, China, Canada, Germany, South Korea, Argentina, Turkey, and Japan.

Competitive Landscape

The Saudi Arabia mineral processing equipment market shows moderate concentration, with top multinational OEMs holding sizeable order pipelines but facing rising local-content hurdles.

Joint ventures deepen localization: Weir–Olayan focuses on pump refurbishments and mill-liner casting; Epiroc-Rasi targets autonomous drilling; MDS teamed with Abdul Latif Jameel Machinery to distribute heavy-duty screening lines for giga-projects. These alliances satisfy Vision 2030 content thresholds while delivering field-service reach that global OEMs alone could not match.

Technology differentiators are reshaping competition. Hexagon’s digital mine platform positions data analytics as a service revenue stream. Metso’s stirred-media-detritor and Swiss Tower Mills acquisition extends fine-grind capability for lithium and copper concentrates. White space persists in lithium hydroxide refining equipment, where chemical-process specialists outside the traditional mining sphere could enter and compete on crystallizer and solvent-extraction plant design. Overall, suppliers able to integrate low-carbon flowsheets, AI monitoring, and local manufacturing stand to capture the fastest-growing orders.

Saudi Arabia Mineral Processing Equipment Industry Leaders

Metso Outotec

FLSmidth A/S

Weir Group PLC

Sandvik AB

Thyssenkrupp Industrial Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saudi Ministry shortlisted 30 firms for 22 quarry licences in Eastern Province and Tabuk.

- January 2025: Weir Group and Olayan formed a service-center joint venture to localize pump and crusher maintenance.

- January 2025: Six mining firms qualified for the SAR 685 million Exploration Enablement Program, covering 4,000 sq km of leases. The Kingdom has handpicked Royal Road, Ajlan and Bros Holding, and EV Metals Group for the initial phase of qualification. Joining them are industry stalwarts Ma’aden, Gold and Minerals Co., and Al-Masane Al-Kobra Mining Co., commonly referred to as AMAK.

Saudi Arabia Mineral Processing Equipment Market Report Scope

| Phosphate |

| Bauxite |

| Gold |

| Iron Ore |

| Copper |

| Lithium |

| Others |

| Crushers & Mills |

| Screens & Feeders |

| Conveyors |

| Pumps & Cyclones |

| Drills & Breakers |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| Eastern Province |

| Makkah |

| Riyadh |

| Tabuk |

| Al-Madinah & Others |

| By Mineral Mining Sector | Phosphate |

| Bauxite | |

| Gold | |

| Iron Ore | |

| Copper | |

| Lithium | |

| Others | |

| By Equipment Type | Crushers & Mills |

| Screens & Feeders | |

| Conveyors | |

| Pumps & Cyclones | |

| Drills & Breakers | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated | |

| By Province | Eastern Province |

| Makkah | |

| Riyadh | |

| Tabuk | |

| Al-Madinah & Others |

Key Questions Answered in the Report

What is the current value of the Saudi Arabia mineral processing equipment market in 2025?

It stands at USD 198.13 million and is projected to climb to USD 331.91 million by 2030.

Which mineral segment is expanding the fastest in Saudi Arabia?

Lithium processing leads with a forecast 10.26% CAGR to 2030, driven by the Kingdom’s electric-vehicle ambitions.

Why is Eastern Province the largest regional buyer of processing equipment?

Ras Al Khair’s multi-commodity hub, integrated ports, and rail access anchor 41.19% of national demand.

How are localization policies affecting equipment suppliers?

Vision 2030 incentives reward OEMs that establish Saudi manufacturing or JV service hubs, influencing contract awards.

What is driving adoption of fully automated mineral processing plants?

Shortage of automation engineers and proven 40% downtime reductions from AI-enabled maintenance systems accelerate the shift.

Page last updated on: