Morocco Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

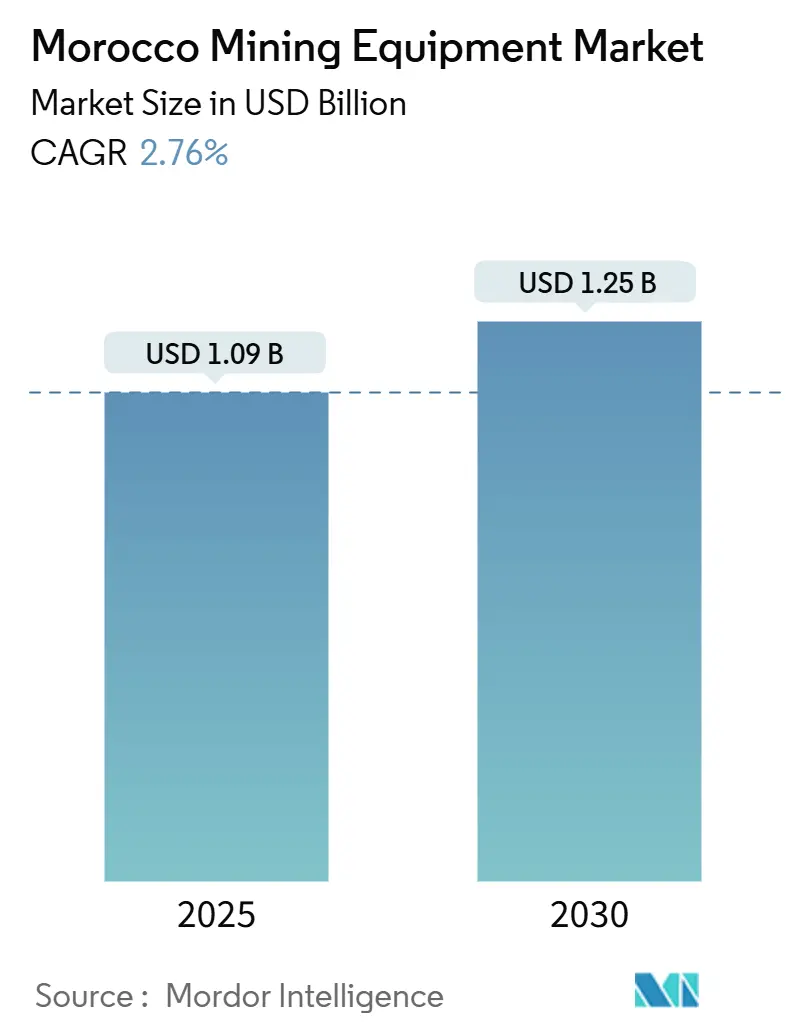

| Market Size (2025) | USD 1.09 Billion |

| Market Size (2030) | USD 1.25 Billion |

| Growth Rate (2025 - 2030) | 2.76% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Morocco Mining Equipment Market Analysis by Mordor Intelligence

The Morocco mining equipment market size stood at USD 1.09 billion in 2025 and is forecast to reach USD 1.25 billion by 2030, expanding at a 2.76% CAGR. This trajectory signals a maturing phase in which replacement cycles, technology upgrades, and stricter environmental standards steer demand. The phosphate sector continues to set the procurement tone, yet electrification, automation, and diversification into critical minerals now shape the Morocco mining equipment market more than greenfield expansion. Strategic investments led by OCP Group, government incentives under Plan Maroc Mines 2021-30, and rising interest in copper and cobalt improve long-term visibility for suppliers, while water scarcity compliance and commodity volatility temper near-term spending plans.

Key Report Takeaways

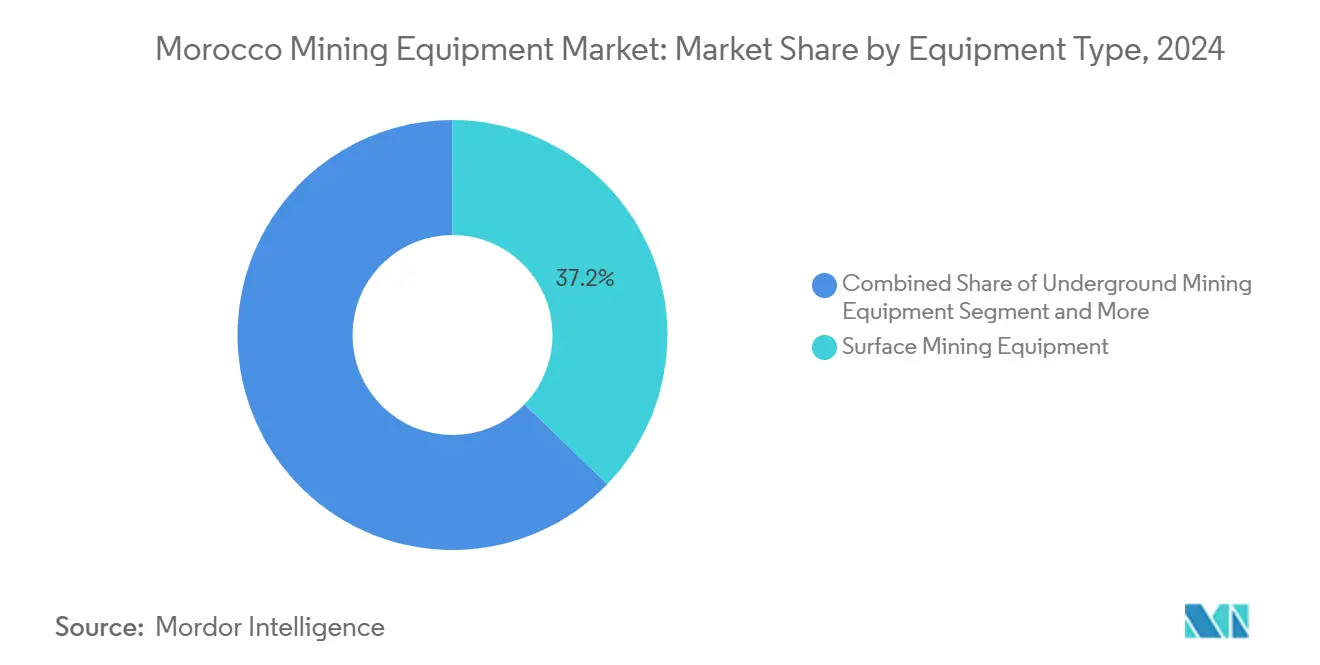

- By equipment type, surface mining led with 37.24% revenue share in 2024; battery-electric load-haul-dump equipment is projected to advance at a 15.26% CAGR through 2030.

- By automation level, manual equipment held 64.83% of the Morocco mining equipment market share in 2024, while fully autonomous equipment shows the highest projected CAGR at 18.17% through 2030.

- By powertrain type, ICE vehicles captured an 87.92% share of the Morocco mining equipment market in 2024, and battery-electric vehicles are growing at a 17.43% CAGR over the forecast period.

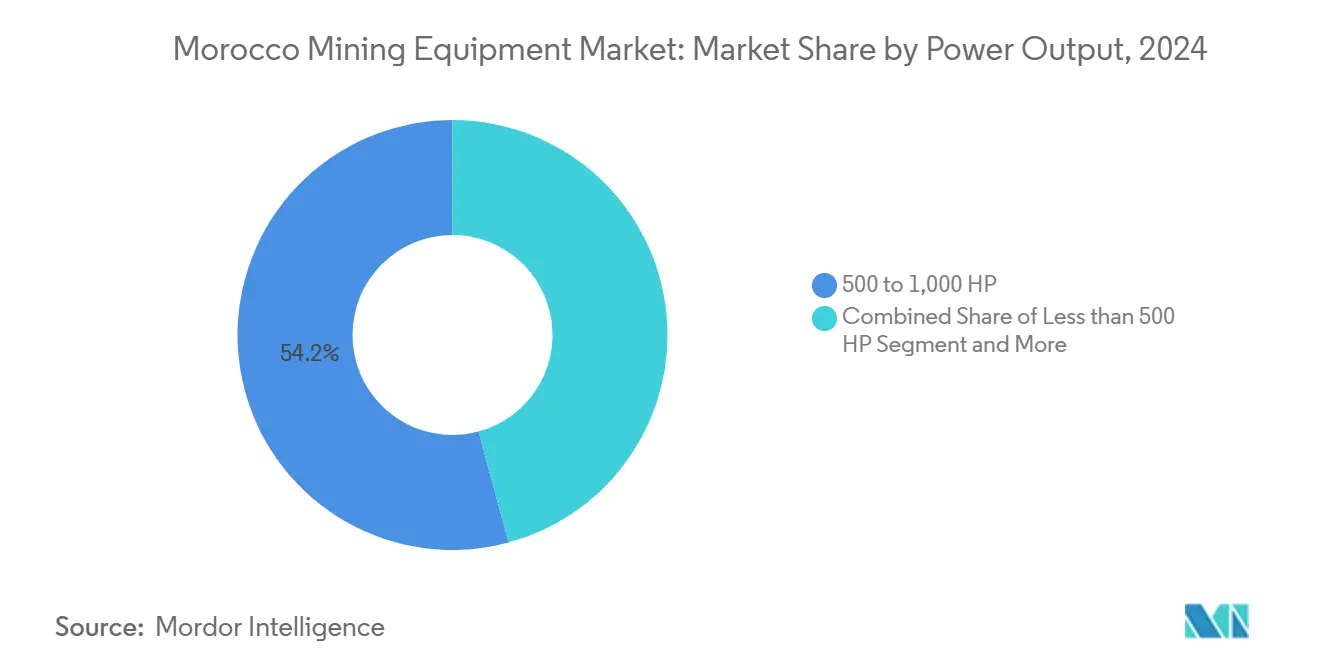

- By power output, the 500–1,000 HP class accounted for a 54.16% share in 2024, and equipment below 500 HP is forecast to grow at a 14.07% CAGR to 2030.

- By application, metal mining represented 46.38% of the market in 2024 and is set to register a 12.48% CAGR through 2030.

Morocco Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phosphate-Sector CAPEX Boom by OCP Group | +0.8% | National, concentrated in Khouribga, Benguerir, Youssoufia | Medium term (2–4 years) |

| Government "Plan Maroc Mines 2021–30" Incentives | +0.4% | National, with focus on emerging mining regions | Long term (≥ 4 years) |

| Uptake of Mine-Site Automation and Digital Twins | +0.6% | National, early adoption in major OCP sites | Medium term (2–4 years) |

| EV-Linked Demand for Cobalt and Copper | +0.3% | Regional, Anti-Atlas and emerging deposits | Long term (≥ 4 years) |

| Offshore Polymetallic-Nodule Exploration Prospects | +0.2% | Coastal regions, Atlantic seaboard | Long term (≥ 4 years) |

| Green-Hydrogen Powered Mine-Fleets Initiatives | +0.3% | National, integrated with renewable energy zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Phosphate-sector CAPEX Boom by OCP Group

OCP Group's unprecedented USD 13 billion investment program through 2027 represents the largest single driver reshaping Morocco's mining equipment landscape. The program encompasses doubling mining capacity and tripling processing capacity, with a specific focus on the Meskala mine opening and Mzinda fertilizer complex expansion. This investment cycle differs from traditional CAPEX booms by integrating sustainability mandates from inception, requiring equipment suppliers to demonstrate carbon footprint reduction capabilities alongside productivity gains. The Benguerir site's planned production tripling exemplifies this approach, where Weir Group's GBP 25 million contract for separation solutions specifically targets energy-efficient technologies with a projected mine life exceeding 100 years[1]"Weir awarded £25m contract for separation solutions at two greenfield projects in Morocco," PNG Business News, pngbusinessnews.com.. OCP's transition to 100% renewable energy by 2028 creates cascading equipment requirements, as traditional diesel-powered machinery becomes incompatible with the company's operational mandate. The strategic shift toward green ammonia production, targeting 1 million tons annually by 2027, necessitates specialized equipment for hydrogen-powered mining fleets, positioning Morocco as a testing ground for next-generation mining technologies.

Government "Plan Maroc Mines 2021-30" Incentives

Morocco's National Mining Sector Development Strategy creates systematic incentives that extend beyond traditional tax breaks to encompass technology transfer requirements and local content mandates. The strategy's emphasis on tripling mining revenue and doubling employment by 2025 drives demand for productivity-enhancing equipment while simultaneously creating workforce development pressures. The new mining code under development prioritizes digitization of mining title management and extends exploration permits, creating regulatory certainty that encourages long-term equipment investments. Morocco's ranking as Africa's most attractive mining destination by the Fraser Institute in 2022 and 2023 reflects the policy framework's effectiveness in attracting international equipment suppliers and technology partners. The government's focus on critical minerals development, particularly the 7 of 24 critical minerals Morocco possesses, creates niche equipment opportunities for rare earth extraction and processing technologies. Local content requirements embedded within the strategy favor equipment suppliers who establish manufacturing or assembly operations within Morocco, creating competitive advantages for companies willing to invest in domestic capabilities.

Uptake of Mine-site Automation and Digital Twins

Morocco's mining automation adoption accelerates through strategic partnerships that bypass traditional implementation barriers. OCP's collaboration with Teal Technology Services for digital transformation and QuWireless-Nexaglobe partnership for 4G/LTE connectivity in harsh mining environments demonstrates the infrastructure foundation necessary for autonomous operations. The implementation of Distributed Control Systems (DCS) in phosphoric acid and fertilizer units since 1997 provides Morocco with advanced process automation experience that translates into mining equipment sophistication. Mantrac Group's deployment of AI-powered Driver Safety Systems, engaging 90 operators with fatigue detection technology, showcases the practical application of automation in improving safety metrics while reducing operational downtime. The development of autonomous Load-Haul-Dump systems, achieving 90% bucket fill factors in underground operations, indicates Morocco's readiness to adopt sophisticated automation technologies that enhance productivity in challenging mining environments. Digital twin technology integration allows real-time monitoring and predictive maintenance, reducing equipment downtime and extending asset lifecycles in Morocco's water-scarce operating environment.

EV-linked Demand for Cobalt and Copper

Morocco's strategic positioning in the electric vehicle supply chain creates sustained demand for specialized extraction equipment targeting cobalt and copper deposits. The establishment of China's BTR New Material Group battery plant, involving MAD 3 billion investment and 2,500 jobs, demonstrates the downstream integration driving upstream mining equipment requirements[2]Latifa babas, "Morocco signs deal for electric vehicle battery plant with China's BTR New Material Group," en.yabiladi.com. . Managem's expansion into cobalt and copper mining across 8 African countries, with market capitalization increasing from USD 2 billion to USD 6.1 billion, reflects the sector's growth trajectory and equipment investment capacity. The Tizert copper mine development in Morocco and acquisition of the Karita gold project in Guinea indicate geographic diversification that requires adaptable equipment platforms capable of operating across different geological conditions. Morocco's role as an unexpected beneficiary of China's strategy to circumvent the U.S. Inflation Reduction Act creates additional equipment demand through joint ventures like Canada's SRG Mining partnership with China's Carbon One for graphite-based anode production[3]"Morocco, an Unexpected Winner of China’s Strategy to Circumvent the U.S. Inflation Reduction Act," Center for Strategic & International Studies, csis.org.. The projected tripling of critical mineral demand by 2040, with market value reaching USD 400 billion by 2050, positions Morocco's mining equipment market for sustained growth driven by energy transition requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-Price Cyclicality | -0.7% | Global, with regional amplification in Morocco | Short term (≤ 2 years) |

| High CAPEX of Advanced Equipment | -0.5% | National, affecting smaller operators disproportionately | Medium term (2–4 years) |

| Water-Scarcity Compliance Costs | -0.4% | National, concentrated in inland mining regions | Long term (≥ 4 years) |

| Scarcity of Autonomous-Mining Skill Sets | -0.3% | National, with regional variations in technical education | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commodity-price Cyclicality

Phosphate price volatility fundamentally impacts Morocco's mining equipment procurement cycles, with OCP's revenue fluctuations directly translating into CAPEX adjustments that affect the entire supply chain. The commodity's sensitivity to agricultural demand cycles creates equipment investment uncertainty, as demonstrated by historical patterns where price downturns delay major equipment purchases by 12-18 months. Morocco's heavy dependence on phosphate exports, accounting for 26% of national exports, amplifies price cycle impacts compared to more diversified mining economies. The challenge intensifies for smaller operators who lack OCP's financial resilience, forcing equipment suppliers to develop flexible financing models that accommodate cyclical cash flows. Mining companies increasingly adopt scenario-based planning methodologies that adjust equipment procurement based on commodity price forecasts, creating demand volatility that equipment manufacturers must navigate through inventory management and production flexibility. The integration of renewable energy costs into mining operations adds complexity to commodity price calculations, as energy-intensive equipment becomes more attractive during high energy price periods but faces scrutiny during commodity downturns.

High CAPEX of Advanced Equipment

The capital intensity of next-generation mining equipment creates adoption barriers that segment Morocco's market between technology leaders and cost-conscious operators. Battery-electric Load-Haul-Dump machines command premium pricing that can exceed traditional diesel equivalents by 40-60%, creating financing challenges for smaller mining operations despite lower operational costs over equipment lifecycles. Autonomous mining systems require substantial upfront investments in infrastructure, training, and integration that many operators cannot justify without guaranteed productivity improvements and safety benefits. The challenge compounds in Morocco's developing mining regions where supporting infrastructure for advanced equipment may be inadequate, requiring additional CAPEX for power systems, connectivity, and maintenance facilities. Equipment suppliers respond by developing modular upgrade paths that allow operators to incrementally adopt advanced features rather than requiring complete fleet replacement. Leasing and equipment-as-a-service models gain traction as methods to reduce upfront CAPEX while providing access to cutting-edge technology, though these arrangements shift financial risk to equipment suppliers who must accurately predict utilization rates and maintenance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Dominance Meets Electrification Pivot

Surface mining machinery generated 37.24% of 2024 sales in the Morocco mining equipment market, driven by Khouribga, Benguerir, and Youssoufia’s open-pit phosphate pits. The sub-segment stays resilient because overburden haulage remains unavoidable, yet its growth rate lags the 15.26% CAGR assigned to battery-electric LHDs that now handle haulage within pit rims. Demand for mineral-processing gear rises in parallel with OCP’s downstream fertilizer expansion as the group aims to triple processing capacity by 2027.

Underground equipment gains relevance as Managem intensifies copper and gold exploration, prompting orders for narrow-vein drills and low-profile trucks. The Morocco mining equipment market size tied to drills and breakers accelerates because harder lithologies prevail in Anti-Atlas ore bodies, requiring high-impact hammers and rotary blasthole rigs. Suppliers widen parts inventories for carbide bits and hydraulic seals to cut lead times from 10 weeks. Electric crusher lines see early adoption where grid access is stable, and vendors bundle dust-suppression packages because inland pit humidity hovers below 30%, elevating silica-particle breach risks.

By Automation Level: Manual Supremacy Under Systematic Erosion

Manual equipment still controls 64.83% of installed units across the Morocco mining equipment market, reflecting legacy fleets and operator familiarity. However, fully autonomous platforms expand at 18.17% CAGR, pushed by documented safety wins and overtime cost avoidance. Semi-autonomous kits serve as bridging technology, enabling stepwise migration without wholesale fleet turnover.

Course curricula at Moroccan technical institutes now incorporate autonomous haul-road design and LiDAR calibration, trimming the skills gap that restrains uptake. Vendors integrate remote-operation stations to let one driver supervise up to four trucks, yielding productivity lifts validated in pilot studies at Benguerir. Payback periods hover near four years when diesel savings, tire life extension, and reduced incident downtime are tallied, helping financiers green-light higher ticket prices. As connectivity deepens, the Morocco mining equipment industry gains a data layer that underpins predictive maintenance subscription models.

By Powertrain Type: ICE Majority Feels Battery Pressure

ICE vehicles commanded 87.92% of 2024 shipments, yet their share erodes as battery-electric alternatives clock 17.43% CAGR. OCP’s plan to cover 100% of power needs with renewables by 2028 reshapes total cost calculations, moving battery units into parity on a life-cycle basis. Hybrid powertrains fill operational gray zones where charging infrastructure only operates part-time; their share inches upward in underground headings where ventilation savings matter most.

OEMs pilot hydrogen-ready engines in over-1,000 HP haulers, leveraging Morocco’s green-ammonia rollout announced with Fortescue in 2024. Thermal-management modules advance in tandem because desert pit temperatures surpass 45 °C during late summer, risking battery degradation. Financiers now insist on carbon-intensity disclosures within loan covenants, further nudging buyers toward electrified choices.

By Power Output: Mid-range Core, Small-scale Upswing

Units rated 500 to 1,000 HP hold a 54.16% share as they balance payload with maneuverability inside Morocco’s mid-strip phosphate pits. In contrast, sub-500 HP machinery grows fastest at 14.07% CAGR as selective mining gains ground in cobalt and gold veins. Modular, smaller engines pair well with autonomous traction control that reduces wheel slip on steep grades common in the Anti-Atlas.

Morocco mining equipment market size tied to more than 1,000 HP units remains important for long-distance haul between pit and rail spur, yet new rail alignments slated under the USD 37 billion national program will shrink average haul lengths, loosening the hold of mega-trucks. Suppliers recalibrate inventories to avoid over-stocking ultra-class tires as fleet compositions rebalance toward lighter trucks and in-pit crushing systems.

By Application: Metal Mining Broadens Demand Base

Metal mining produced 46.38% of the 2024 turnover in the Morocco mining equipment market and will outpace phosphate growth at 12.48% CAGR by 2030. Copper, cobalt, and silver dominate procurement lists, each requiring distinct processing flowsheets that drive orders for regrind mills, gravity concentrators, and pressure oxidation autoclaves. The Morocco mining equipment industry benefits because Managem exports its expertise to eight African countries, often purchasing from Moroccan dealers who bundle regional service contracts.

Mineral mining, led by phosphate, underpins steady baseline demand; however, value migrates downstream, so OCP’s fertilizer complexes now draw in higher-spec pumps, valves, and granulation drums. Coal equipment demand remains negligible because Morocco targets 52% renewable electricity by 2030, aligning national energy policy with decarbonization imperatives. Suppliers that formerly focused on coal adapt by repositioning product lines toward biomass blending and waste-heat recovery inside fertilizer plants, keeping revenue taps open despite coal’s decline.

Geography Analysis

Khouribga-Settat concentrates roughly 70% of OCP ore pick-up and remains the largest spending pocket in the Morocco mining equipment market. Continuous strip mining requires belt rebuilds every three years and fleet replacements on eight-year cycles. The adjacent Jorf Lasfar industrial platform magnifies parts demand because it processes ore into phosphoric acid, requiring 24-hour maintenance coverage. Gantour’s Benguerir and Youssoufia pits form the second-largest equipment cluster; production there is slated to triple once the Louta project comes online, calling for an extra 240-ton trucks, in-pit mobile crushers, and process water pumps running on reclaimed wastewater.

Boucraa in Western Sahara contributes about 8% of OCP output and operates in an arid desert that pushes OEMs to supply sealed-bearing idlers, dust-proof cabins, and saline-resistant hydraulics. Suppliers that maintain mobile service caravans win contracts because local workshop capacity is thin. Meanwhile, Anti-Atlas copper and cobalt prospects trigger demand for narrow-vein jumbos and battery-electric scoops able to negotiate sub-2.5-meter headings. Exploration companies prefer rental packages due to uncertain resource sizes, creating opportunities for dealers to build utilization-based revenue streams.

Due to port access and free-zone customs, Casablanca and Rabat function as equipment logistics hubs. Firms like AMESP warehouse critical spares there to cut lead times to 24 hours for Khouribga clients. Planned north–south high-speed rail corridors will slash heavy-haul trucking costs, encouraging centralized stocking instead of scattered depots. Regional diversification broadens the Morocco mining equipment market, compelling suppliers to layer national dispatch centers over localized field workshops.

Competitive Landscape

Global OEMs hold sway, yet their combined domestic share points to moderate concentration, keeping price competition alive. Caterpillar leverages a 31% global mining share and a dense parts pipeline; its remanufacturing hub in Tangier Free Zone reduces turnaround time for engine blocks from eight to five days. Komatsu pivots on a 65% aftermarket revenue model that aligns well with Morocco’s maintenance-heavy phosphate cycle, and its Autonomous Haulage System trials at Benguerir seek to establish reference sites.

Sandvik and Epiroc carve out premium niches via electrification depth. Sandvik’s record global order for BEV trucks in 2025 resonates locally as OCP explores diesel-free haulage inside indoor stockpiles. Epiroc, with 68% of revenue from services, packages battery rigs with three-year maintenance wraps, insulating clients against skills gaps. Chinese challengers SANY and XCMG undercut on price and sometimes bundle financing, targeting mid-tier copper start-ups in the Anti-Atlas.

Local specialists fill service white spaces. Mantrac integrates fatigue sensors, telematics, and lease financing into single-invoice offers that resonate with operators lacking internal engineering depth. AMESP focuses on fast-moving wear parts and articulates a 12-hour delivery promise within a 300-kilometer radius of Casablanca. This mesh of international technology and local service capabilities explains why no single player tops 50% share, preserving supply diversity in the Morocco mining equipment market.

Morocco Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Sandvik AB

-

Epiroc AB

-

Hitachi Construction Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Xtract Resources acquired a 50% shareholding in Wildstone SARL for USD 500,000, gaining access to 15 exploration licenses for copper, silver, and antimony in Morocco.

- May 2025: OCP Group and AFD Group formalized a EUR 350 million financing agreement to support OCP's USD 13 billion green investment program (2023-2027). The program aims to achieve 100% clean energy and carbon neutrality by 2040 while increasing decarbonized fertilizer production.

Morocco Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 to 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 to 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

What is the current value forecast for the Morocco mining equipment market by 2030?

The market is projected to reach USD 1.25 billion by 2030, climbing from USD 1.09 billion in 2025 at a 2.76% CAGR.

Which equipment category grows fastest in Morocco through 2030?

Battery-electric load-haul-dump machines lead with a 15.26% CAGR on rising electrification mandates.

How dominant are ICE vehicles in Morocco’s mining fleets today?

ICE units still hold 87.92% of shipments, though their share is shrinking as battery platforms post 17.43% CAGR growth.

Why does metal mining outpace phosphate in growth terms?

Rising demand for copper and cobalt tied to electric-vehicle supply chains drives metal mining’s 12.48% CAGR.

What regional hubs are critical for service and logistics?

Casablanca and Rabat anchor spare-parts warehousing and dispatch, while Khouribga and Benguerir remain equipment-usage hotspots.

How is water scarcity influencing equipment design?

Clients now prioritize closed-loop pumps and dust-resistant hydraulics that cut consumption and comply with desalination-sourced water limits.

Page last updated on: