Turkey Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

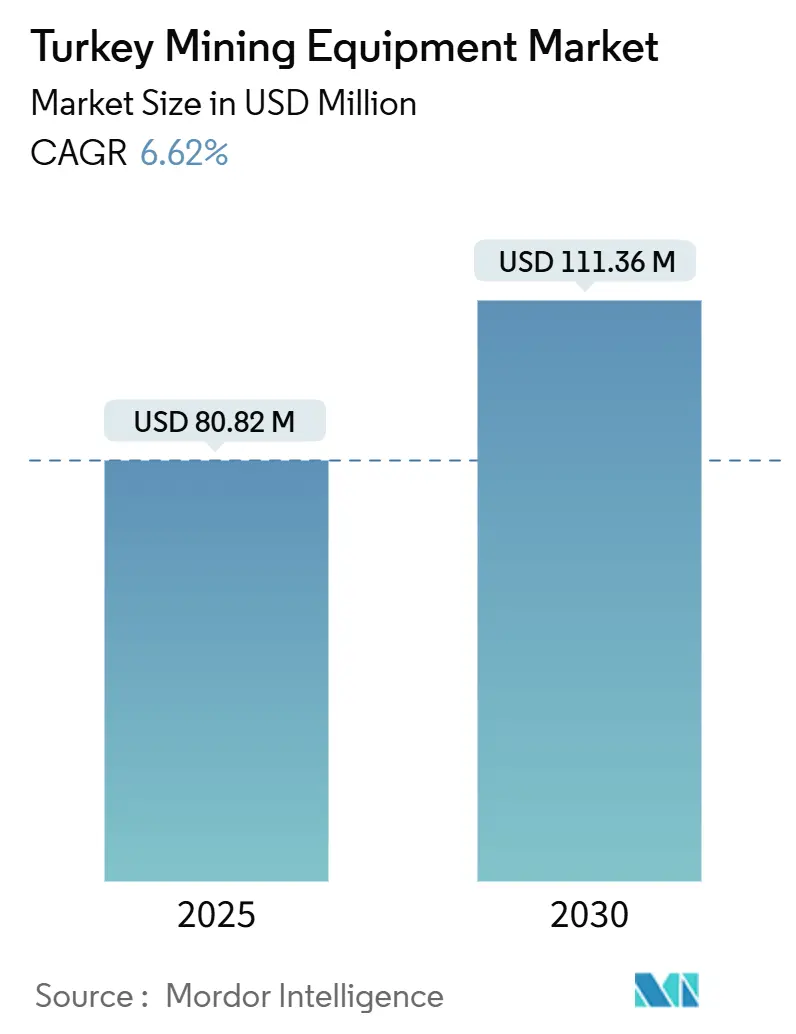

| Market Size (2025) | USD 80.82 Million |

| Market Size (2030) | USD 111.36 Million |

| Growth Rate (2025 - 2030) | 6.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Mining Equipment Market Analysis by Mordor Intelligence

The Turkey mining equipment market size is USD 80.82 million in 2025 and is forecast to reach USD 111.36 million by 2030 at a 6.62% CAGR. Robust mineral diversity, the country’s position as Europe’s largest gold producer, and its most global boron reserves underpin sustained demand for new machinery. Growing rare-earth exploration, government safety incentives, and rising construction activity amplify equipment orders. Global OEMs leverage local partnerships to shorten delivery times and tailor after-sales services, while domestic engineering know-how supports component manufacture. Investment in battery production and autonomous technology trials signals a gradual pivot away from diesel fleets toward electric and digitally enabled solutions.

Key Report Takeaways

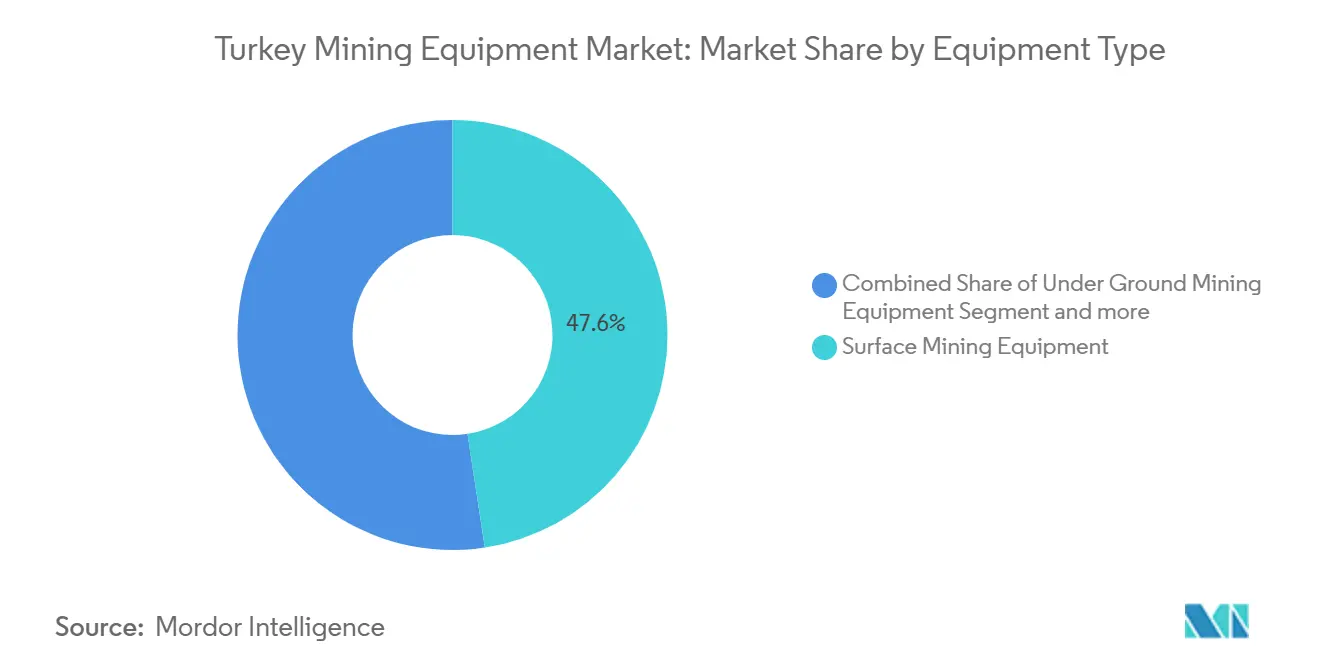

- By equipment type, Surface Mining Equipment captured 47.61% of the Turkey mining equipment market share in 2024, whereas Underground Mining Equipment is projected to expand at an 8.61% CAGR through 2030.

- By automation level, Manual Equipment led with 69.67% revenue share in 2024, while Fully-Automated systems record the highest anticipated CAGR of 10.34% to 2030.

- By powertrain, internal Combustion Engine units held a 76.27% share of the Turkey mining equipment market in 2024; Battery-Electric Vehicles are forecast to grow at an 11.82% CAGR over 2025-2030.

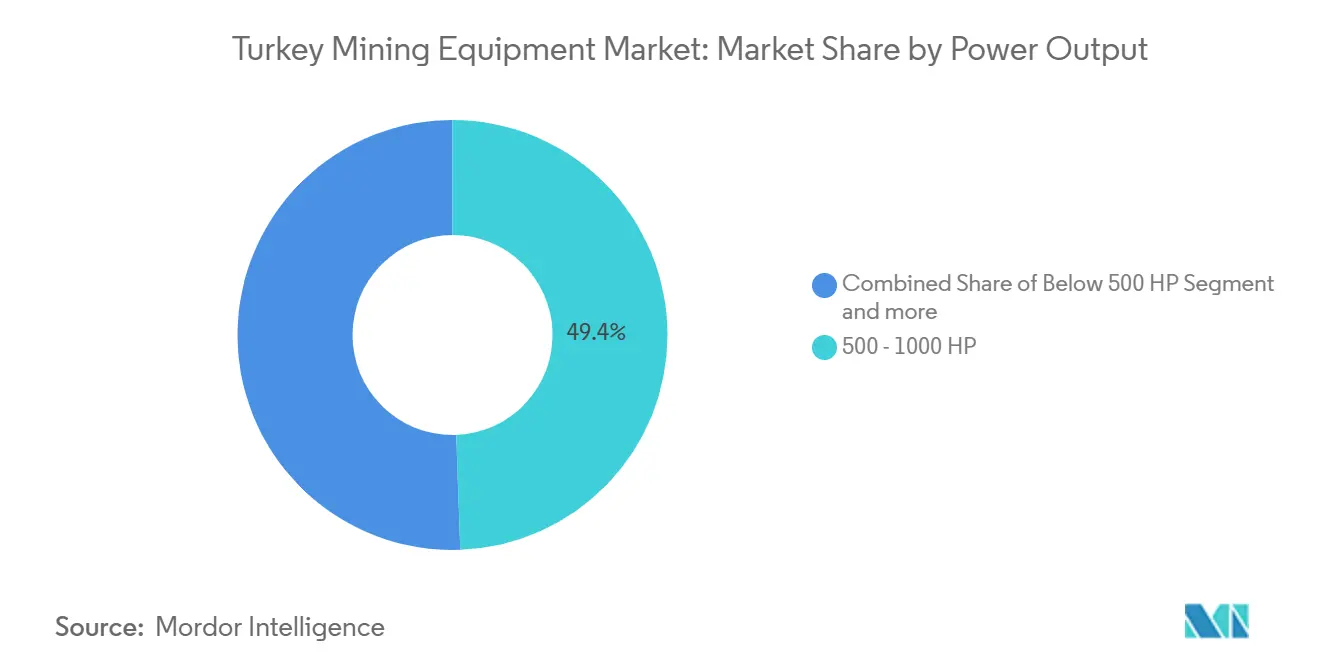

- By power output, the 500-1000 HP segment accounted for 49.42% of the Turkey mining equipment market size in 2024, and equipment below 500 HP is advancing at a 7.37% CAGR in the same period.

- By application, Metal Mining dominated with a 47.53% share of the Turkey mining equipment market size in 2024; Mineral Mining is poised for the fastest gain at a 9.39% CAGR up to 2030.

Turkey Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open-pit projects | +1.5% | Western and Central Anatolia | Long term (≥ 4 years) |

| Construction demand | +1.2% | Marmara and Central Anatolia | Medium term (2-4 years) |

| EU rare-earth financing | +1.1% | Eskişehir & nationwide | Long term (≥ 4 years) |

| Safety incentives | +0.9% | Coal-focused provinces | Short term (≤ 2 years) |

| Battery-electric shift | +0.8% | Major mining centers | Medium term (2-4 years) |

| Rental boom | +0.7% | Industrial hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Demand from Construction and Manufacturing

Turkey’s infrastructure upgrades and export-oriented manufacturing expansion keep aggregate and industrial mineral extraction at buoyant levels. Machinery exports climbed 11% in 2023, reflecting strong local fabrication capacity that feeds quarry expansion[1]“Machinery Export Performance 2023,” Turkish Statistical Institute, tuik.gov.tr. Urban transformation projects and new transport corridors require high-throughput crushers, loaders, and screening lines. The strategic crossroads between Europe and Asia channel regional construction supply chains through Turkish quarries, widening the customer base for equipment dealers. Firms prioritize fuel-efficient loaders and hybrid drills to defend margins amid volatile input costs.

EU-Backed Rare-Earth Exploration Financing

EU raw-materials policy channels concessional loans toward Eskişehir’s rare-earth complex, covering ore sorting plants and solvent-extraction lines. The pilot plant has been operational since 2023, validating process chemistry and demonstrating Turkey’s capability to supply neodymium and praseodymium to European magnet producers. Guaranteed offtake stimulates orders for specialty crushers, flotation cells, and multi-stage dryers that differ from mainstream copper or gold circuits, broadening equipment mix and aftermarket potential.

Government Incentives for Modernization and Safety

Post-Soma safety reforms accelerate fleet replacement programs. Lower royalties apply to mines meeting advanced safety thresholds, while the e-Maden licensing portal requires digital monitoring tools in every permit application. These rules push operators to adopt semi-autonomous haul trucks and real-time gas detection systems. Immediate uptake is most visible in underground coal districts where inspection frequency increased after 2024. Local OEM workshops supply compliant retrofits, shortening lead times for mandatory upgrades and creating a steady pipeline of demand for monitoring hardware.

Growth of Local Rental and Leasing Ecosystem

Smaller license holders opt for leasing rather than purchasing to navigate commodity cycles. Rental companies scale fleets that include battery-electric LHDs and autonomous drills, allowing miners to trial emerging technologies with limited upfront risk. OEMs partner with rent-to-own providers for maintenance contracts, ensuring factory-level servicing standards across dispersed regions. Flexible financing aligns equipment costs with production cash flow, smoothing procurement peaks and troughs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility | -1.8% | Metal-rich provinces | Short term (≤ 2 years) |

| Permit uncertainty | -1.4% | Sensitive areas | Medium term (2-4 years) |

| Battery supply gap | -0.9% | Nationwide | Medium term (2-4 years) |

| Autonomy skill gap | -0.7% | Advanced regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility

Daily price swings for copper and gold influence project cash flows. Mine's delays capital purchases during downturns and pivots to short-term rentals. Turkey’s mining index analysis shows strong short-run feedback loops with global metal prices, making procurement cycles highly cyclical. The pattern is acute in metal-intensive western belts, where operators hedge through modular fleets that can be redeployed quickly.

Shortage of Autonomous-Equipment Skillsets

Turkey hosts 19,609 registered mining engineers, yet advanced automation curricula remain scarce. Mines struggle to recruit lidar specialists and remote-operations supervisors, slowing the migration from semi-autonomous to fully driverless fleets. OEMs establish training centers, but skill gaps persist, delaying widespread adoption and tempering the driverless segment’s upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Mining Dominates Amid Automation Push

Surface Mining Equipment controlled 47.61% of the Turkey mining equipment market share in 2024, reflecting the prevalence of open-pit copper, gold, and industrial mineral operations across Western and Central Anatolia. Productivity gains stem from high-capacity electric shovels, 90-tonne haul trucks, and mobile crushers that match the scale of porphyry ore bodies. Underground Mining Equipment is expected to post an 8.61% CAGR through 2030 as deeper deposits come online and safety mandates drive mechanization. Demand centers on low-profile loaders, battery drill jumbos, and roadway support systems optimized for Turkey’s variable rock conditions.

Turkey mining equipment market size for drills and breakers is poised to expand with ongoing exploration of rare-earth and boron seams that demand high-precision coring rigs. Crushing, pulverizing, and screening lines benefit from the marble and natural stone trade, where Turkey holds a major share of global non-fuel mineral export value. Loaders and haul trucks see recurring orders as mid-tier mines refresh fleets to cut maintenance costs and comply with new exhaust standards.

By Automation Level: Manual Fleets Yield to Autonomy

Manual systems represented 69.67% of sector revenue in 2024, yet full autonomy exhibits a 10.34% CAGR to 2030. Early adopters retrofit existing drills with telemetry and collision-avoidance modules, lowering entry barriers. Semi-autonomous machines serve as a transitional class, combining remote cameras with on-board operators for complex maneuvers. Mines invest in secure data links and cloud analytics to maximize utilization and schedule predictive maintenance.

Turkey mining equipment market size for autonomous drills grows as operators validate productivity lifts of up to 15% in pilot pits. Market share is shifting as OEMs bundle software subscriptions, mapping support, and operator training into multi-year contracts. Collaboration with local universities aims to bolster remote-operations curricula and reduce the identified skills deficit.

By Powertrain Type: ICE Still Rules but Electric Accelerates

Internal-combustion engines held 76.27% of revenue in 2024 due to mature diesel infrastructure. Fuel efficiency packages such as dynamic idle control and advanced injection systems help mines curb operating costs without large capital outlays. Battery-electric powertrains, forecast at an 11.82% CAGR, gain traction in underground niches where fresh-air requirements push ventilation expenses higher than charger installation costs. Turkey mining equipment market share for electric loaders improves as mines leverage government subsidies tied to the 2053 net-zero pledge.

Hybrid powertrains bridge the transition, mixing downsized diesel engines with regenerative braking to cut fuel use. The gradual rollout of charging hubs across Marmara and Central Anatolia allows mines to test electric trucks on short, level haul roads before scaling up.

By Power Output: Mid-Range Units Provide Versatility

Equipment rated 500-1000 HP commanded 49.42% of Turkey's mining equipment market share in 2024. This horsepower window suits mid-tier gold pits, boron quarries, and limestone operations. Below 500 HP units are growing at a 7.37% CAGR as exploration teams and contract miners favor smaller, transportable gear.

Ultra-class machines over 1,000 HP remain essential for Çöpler-scale operations processing multimillion-ton ore bodies and are typically sourced via long-term supply agreements. Turkey's mining equipment market size for high-horsepower dozers and excavators is steady due to these capital-intensive projects.

By Application: Metals Lead, Minerals Rise

Metal mining absorbed 47.53% of equipment spending in 2024, anchored by gold output and nearly 3.7 million tons of copper reserves[2]“Metallic Minerals Export Data 2024,” Republic of Turkey Ministry of Trade, trade.gov.tr. Turkey mining equipment market size for mineral mining is projected to grow at a 9.39% CAGR, reflecting momentum in industrial minerals and rare-earth extraction.

In 2023, coal holds a significant share as it supplies approximately 26.2% of domestic energy, sustaining demand for continuous miners and shuttle cars while the emissions policy evolves. Application diversity drives OEMs to tailor fleets ranging from high-precision rare-earth separators to heavy-duty lignite excavators.

Geography Analysis

Marmara hosts the largest cluster of dealerships and parts depots, capitalizing on its proximity to Istanbul’s ports and manufacturing base. The region's high equipment turnover aligns with its infrastructure density and quarry activity.

Central Anatolia advances quickly on the back of Eskişehir’s rare-earth complex and vast boron seams, stimulating orders for specialized processing lines. Western Anatolia’s alignment with the Tethyan Belt fuels demand for large surface fleets at copper and gold sites. The Black Sea’s Zonguldak coal basin maintains steady purchases of continuous miners and roof supports essential for deep coal seams.

Eastern provinces such as Erzurum emerge as exploration frontiers, with light drilling rigs dispatched to new licenses. Southern Mediterranean districts diversify into industrial minerals, requiring compact excavators and belt feeders to navigate mountainous terrain.

Competitive Landscape

Global majors remain dominant. Caterpillar’s Resource Industries segment booked USD 13.6 billion in 2023 sales, leveraging Borusan Cat for domestic distribution. Komatsu strengthened its underground credentials through its 2024 takeover of GHH Group, expanding its product breadth for Turkish hard-rock operations.

Epiroc’s automation-heavy portfolio secured 17% order growth in Q1 2025, including remote drilling contracts in Western Anatolia. Sandvik landed a SEK 750 million battery-electric order for South32’s Hermosa project, demonstrating customer confidence in electric fleets. Local firms such as Hidromek pilot indigenous electric excavators, positioning for supply-chain resilience and import-duty advantages.

OEMs co-develop rental programs with Turkish lessors to capture small-mine customers. Consolidation, technology bundling, and aftermarket services define competition as fleet modernization cycles shorten.

Turkey Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Epiroc AB

Sandvik AB

Hitachi Construction Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Turkey and China signed an MoU on rare-earth collaboration, while Ankara joined the Minerals Security Partnership with the US and EU.

- July 2024: Komatsu completed the acquisition of GHH Group, boosting underground offerings for Turkish customers.

Turkey Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills & Breakers |

| Crushing, Pulverizing & Screening |

| Loaders & Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Below 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills & Breakers | |

| Crushing, Pulverizing & Screening | |

| Loaders & Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Below 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

What is the projected value of the Turkey mining equipment market in 2030?

The market is forecast to reach USD 111.36 million by 2030.

Which segment will grow fastest by 2030?

Battery-Electric Vehicles are expected to post the highest CAGR at 11.82% over 2025-2030.

How large is Surface Mining Equipment’s share?

Surface Mining Equipment captured 47.61% of total sales in 2024.

Why are battery-electric machines gaining traction underground?

They cut ventilation costs and align with Turkey’s 2053 net-zero target while matching diesel productivity.

Which region is emerging for rare-earth equipment demand?

Central Anatolia, led by the Eskisehir project, is becoming the hub for rare-earth processing machinery.

Page last updated on: