Europe Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

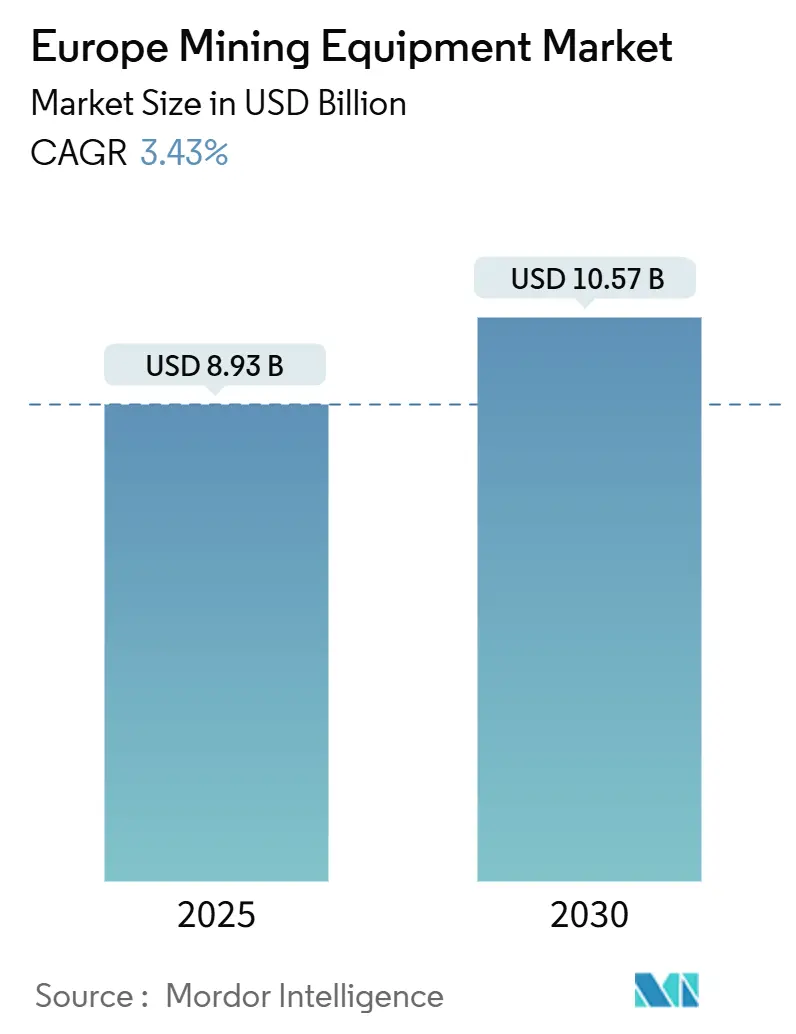

| Market Size (2025) | USD 8.93 Billion |

| Market Size (2030) | USD 10.57 Billion |

| Growth Rate (2025 - 2030) | 3.43% CAGR |

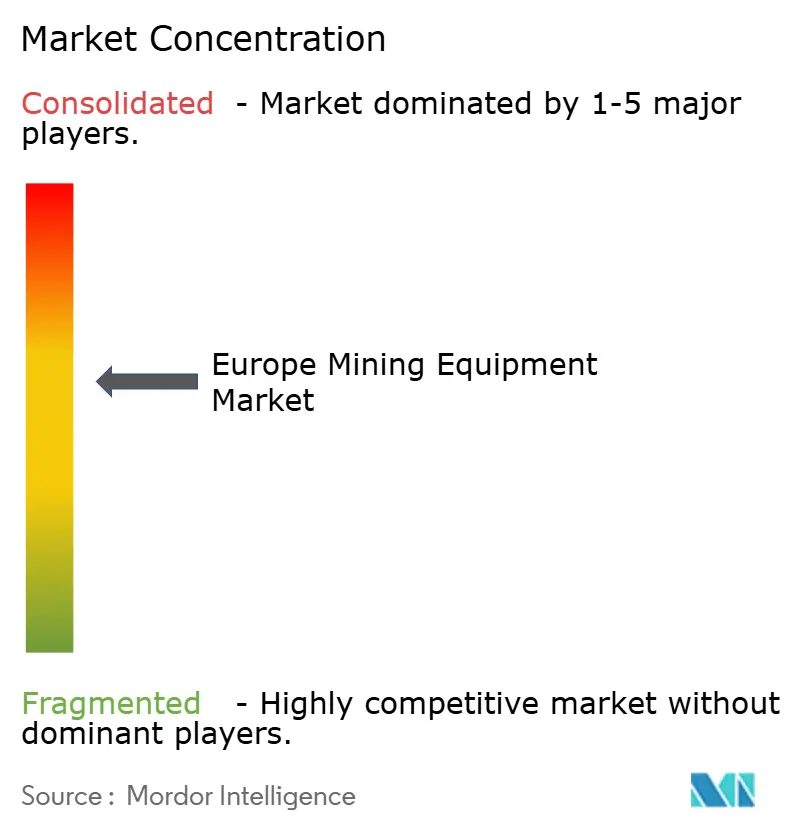

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Mining Equipment Market Analysis by Mordor Intelligence

The Europe Mining Equipment market reached USD 8.93 billion in 2025 and is expected to climb to USD 10.57 billion by 2030, translating into a steady 3.43% CAGR. The trajectory reflects the region’s push for raw-materials self-sufficiency under the Critical Raw Materials Act, the rapid shift toward battery-electric haulage, and sustained upgrades of mid-range surface fleets. Persistent labor shortages in Nordic mines, robust public-sector financing for green projects, and rising rental-as-a-service models underpin demand. At the same time, lengthier environmental approvals and grid constraints temper near-term momentum, keeping growth measured yet resilient.

Key Report Takeaways

- By equipment type, surface mining equipment led with 42.83% revenue share in 2024; Loaders and Haul Trucks are projected to advance at a 14.76% CAGR through 2030.

- By automation level, manual fleets held 68.27% of the Europe Mining Equipment Market share in 2024, while fully autonomous units posted the fastest growth at an 18.49% CAGR.

- By powertrain, internal-combustion vehicles controlled 64.12% of spending in 2024; battery-electric alternatives are forecast to expand at a 21.96% CAGR.

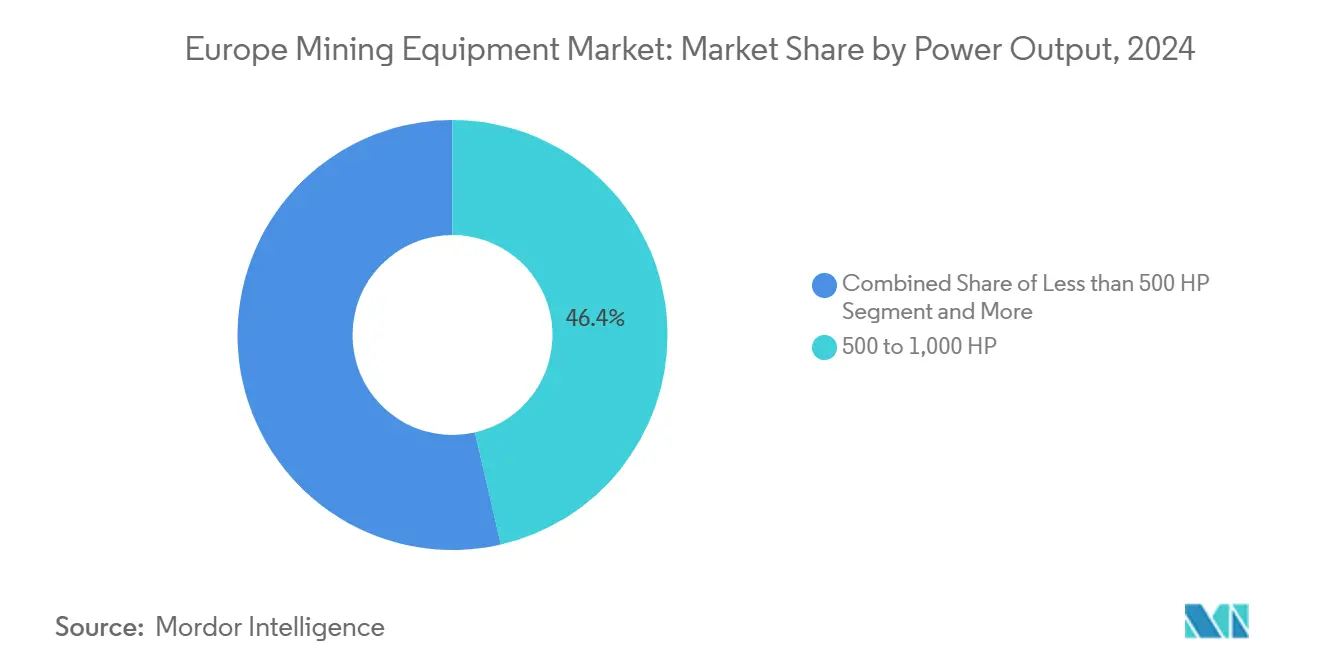

- By power output, the 500-1,000 HP band captured 46.38% of the Europe Mining Equipment market size in 2024; thanks to compact electric rigs, units below 500 HP are on track to grow at a 9.42% CAGR.

- By application, metal mining accounted for a 51.06% share of the Europe Mining Equipment Market size in 2024 and is advancing at an 8.73% CAGR through 2030.

- By country, Germany anchored demand with 25.14% market share in 2024, while France records the highest projected CAGR at 9.79% to 2030.

Europe Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Critical-Raw-Material Demand for EU Battery and Wind Supply Chains | +0.8 | EU-wide, Concentrated in Nordic and Central Europe | Medium Term (2–4 Years) |

| Rapid Adoption of Battery-Electric and Trolley-Assist Haulage | +0.6 | Nordic Countries, Germany, Expanding to Eastern Europe | Short Term (≤ 2 Years) |

| Automation to Offset Skilled-Labor Shortages in Nordic Mines | +0.5 | Finland, Sweden, Norway | Medium Term (2–4 Years) |

| EU Green Deal Grants and EIB Green-Asset Financing | +0.4 | EU-wide with Focus on Cohesion Regions | Long Term (≥ 4 Years) |

| Rental-as-a-Service Models Boosting SME Equipment Access | +0.3 | Western Europe, Expanding Eastward | Short Term (≤ 2 Years) |

| Mine-to-Mill Digital Twins Cutting Opex More Than 12% | +0.2 | Advanced Mining Regions, Nordic Leadership | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Surge in Critical-Raw-Material Demand for EU Battery and Wind Supply Chains

The European Union's strategic pivot toward critical raw materials self-sufficiency creates unprecedented equipment demand across lithium, cobalt, and rare-earth extraction operations. The Critical Raw Materials Act's approval of 47 Strategic Projects requiring EUR 22.5 billion in investment directly translates to substantial mining equipment procurement, particularly for extraction and processing facilities. Finland's Keliber lithium project, backed by EUR 150 million EIB financing, exemplifies this trend, establishing the EU's first integrated lithium hydroxide production facility[1]"Finland: EU and Sibanye-Stillwater, through its Keliber lithium project, join forces in €150 million deal to improve EU access to and resilience in battery materials," EIB, eib.org.. The Transport and Environment analysis indicates that if all planned projects proceed, 60% of EU lithium demand for electric vehicles could be met domestically by 2030, requiring massive infrastructure and equipment investments. Nordic countries possess particularly rich deposits of critical materials, including cobalt, graphite, and lithium, with Finland hosting Europe's largest known cobalt resources and the continent's only cobalt-producing mines. This geographic concentration intensifies equipment demand in regions with established mining expertise and favorable regulatory environments.

Rapid Adoption of Battery-Electric and Trolley-Assist Haulage

Battery-electric mining equipment adoption accelerates across European operations, driven by operational cost advantages and emission reduction mandates. Liebherr's partnership with Fortescue, valued at USD 2.8 billion, represents the largest equipment transaction in Liebherr's 75-year history, featuring 360 autonomous battery-electric T 264 trucks scheduled for validation by late 2025[2]"Liebherr and Fortescue announce significant expansion of zero emission equipment partnership at MINExpo 2024," liebherr.com. . Sweden's Boliden mine implements ABB's trolley infrastructure for electric mine trucks, targeting 70 million tons of annual rock transport while reducing greenhouse gas emissions from transportation by up to 80%.

Automation to Offset Skilled-Labor Shortages in Nordic Mines

European mining faces acute skilled labor shortages, with mining leaders indicating that talent scarcity hampers production and strategic goals, driving automation adoption as a strategic necessity. Mining engineering enrollments dropped in Australia since 2014, reflecting a global trend affecting European operations that increasingly rely on automated solutions to maintain productivity. Epiroc's Q1 2025 results demonstrate strong demand for automation and digitalization solutions, with order intake increasing 17% to MSEK 16,586, driven particularly by wireless connectivity solutions essential for mining automation. Nordic countries lead this transformation, leveraging their advanced technological infrastructure and regulatory support for autonomous operations. Finland's GTK Mintec facility utilizes digital twins and machine learning for mineral processing optimization, representing the digitalization solutions addressing operational challenges through reduced human intervention requirements. The COVID-19 pandemic accelerated automation adoption by highlighting the benefits of minimizing human interaction in mining operations, creating lasting demand for autonomous equipment solutions.

EU Green Deal Grants and EIB Green-Asset Financing

The European Investment Bank's expanded REPowerEU financing package, increased from EUR 30 billion to EUR 45 billion, directly supports mining equipment procurement for strategic net-zero technologies and critical raw materials extraction[3]"EIB to support Green Deal Industrial Plan with EUR 45 billion in additional financing," eib.org.. This initiative mobilizes investments by 2027, enhancing Europe's industrial competitiveness while supporting the mining equipment market expansion. EIT RawMaterials' funding increases per project, with up to EUR 2.5 million available for mining, processing, and recycling projects, addressing financing bottlenecks that historically constrained equipment investments. Germany's Lusatia region receives EUR 150 million EIB investment for transitioning from lignite mining to a climate-neutral economy, demonstrating how green financing reshapes regional mining equipment demand patterns. Sandvik's EUR 500 million EIB loan for R&D in advanced machining solutions, electrification, and automation exemplifies how green financing directly translates to mining equipment innovation and market expansion. The financing framework's emphasis on eligible sectors, including renewable energy technologies, battery storage, and critical raw materials, creates sustained demand for specialized mining equipment across multiple market segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy Environmental-Permit Lead-Times Post-2025 CRMA | -0.4 | EU-wide, Particularly Complex in Germany and France | Short Term (≤ 2 Years) |

| Power-Grid Constraints at Remote Mine Sites | -0.3 | Nordic Regions, Eastern European Mining Areas | Medium Term (2–4 Years) |

| CAPEX Premium (More Than 35%) for Next-Gen BEV Loaders and Trucks | -0.2 | Europe-Wide, Especially Challenging for Mid-Tier Miners | Medium Term (2–4 Years) |

| Volatile Nickel and Copper Prices Denting Investment Planning | -0.1 | Central and Southern Europe, Global Commodity Impact | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Lengthy Environmental-Permit Lead-Times Post-2025 CRMA

Environmental permitting complexities intensify following the Critical Raw Materials Act implementation, creating significant project delays despite streamlined processes for Strategic Projects. The CRMA establishes fast-tracked permitting requiring single points of contact and minimized environmental assessment timelines, yet practical implementation faces bureaucratic challenges across member states. Mining permitting issues account for nearly 40% of project delays globally, with average mine development timelines extending beyond 16 years primarily due to regulatory processes. EU safety regulations for chemicals create additional complications for critical minerals industry development, as top miners express concerns about regulatory impacts on extraction and processing operations. The OECD's analysis of ten EU regions' mining ecosystems identifies community opposition and permitting delays as primary challenges, despite geological endowments and innovation infrastructure advantages. These delays particularly affect equipment procurement timelines, as mining companies defer capital investments until regulatory certainty emerges, creating cyclical demand patterns that impact market growth trajectories.

Power-Grid Constraints at Remote Mine Sites

Remote European mining sites face significant power grid infrastructure limitations that constrain battery-electric equipment adoption despite abundant renewable energy resources in Nordic regions. Data center analysis reveals that electricity demand growth creates grid congestion, with connection delays extending up to 13 years in constrained markets, highlighting broader infrastructure challenges affecting energy-intensive mining operations. Nordic countries possess substantial sustainable energy potentials including hydropower, wind, and biomass resources, yet distribution infrastructure struggles to support increasing energy demand from mining and energy-intensive industries. The Arctic regions' energy-intensive industries growth, including battery cell manufacturing and fossil-free steel production through initiatives like HYBRIT, competes for limited grid capacity with mining electrification projects. Battery-electric mining equipment requires substantial charging infrastructure investments, with fast-charging solutions needed to support continuous operations, creating additional strain on already constrained power systems. These grid limitations force mining operators to maintain hybrid fleets or delay full electrification transitions, constraining the growth potential for battery-electric equipment segments despite favorable regulatory and environmental drivers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Operations Drive Market Leadership

Surface Mining Equipment maintains market dominance with 42.83% share in 2024, reflecting Europe's preference for open-pit operations that optimize resource extraction efficiency. The segment benefits from economies of scale and lower operational complexity than underground alternatives, particularly in Nordic iron ore and Eastern European coal operations. Underground Mining Equipment serves specialized applications in narrow-vein precious metal mines, while Mineral Processing Equipment supports the growing demand for ore beneficiation and waste reduction. Drills and Breakers represent essential infrastructure for surface and underground operations, with increasing automation integration driving replacement cycles.

Loaders and Haul Trucks emerge as the fastest-growing segment at 14.76% CAGR through 2030, propelled by the transition to autonomous and battery-electric haulage systems. Caterpillar's autonomous drilling milestone of 1 million meters drilled demonstrates the commercial viability of unmanned operations. Crushing, Pulverizing, and Screening equipment benefits from digital optimization technologies that enhance throughput and energy efficiency. The equipment type segmentation reflects Europe's strategic focus on maximizing extraction efficiency while minimizing environmental impact through advanced technology deployment.

By Automation Level: Manual Dominance Faces Autonomous Disruption

Manual Equipment commands 68.27% market share in 2024, representing the installed base of traditional mining operations across European facilities. This dominance reflects the substantial capital investments in existing equipment and the gradual nature of mining fleet replacement cycles. Semi-Autonomous Equipment serves as a transitional category, offering enhanced safety and efficiency while maintaining operator oversight and control. The segment provides a bridge between traditional manual operations and fully autonomous systems, allowing operators to gain experience with automated technologies.

Fully Autonomous Equipment accelerates at 18.49% CAGR, driven by labor shortage solutions and safety improvements in hazardous mining environments. Epiroc's mixed fleet automation solutions covering 3,100 vehicles demonstrate the scalability of autonomous technologies. The global autonomous mining vehicle fleet doubled from 500 to over 1,000 units, with BHP achieving 100% autonomy at its Spence copper mine for three months without safety incidents. This growth trajectory reflects the compelling economics of 24/7 operation capabilities and reduced labor costs in regions facing skilled worker shortages.

By Powertrain Type: Electric Transition Accelerates Despite ICE Dominance

Internal-Combustion Engine Vehicles retain 64.12% market share in 2024, reflecting the mature technology's reliability and established maintenance infrastructure across European mining operations. ICE powertrains offer proven performance in extreme operating conditions and benefit from extensive service networks and operator familiarity. Hybrid Vehicles provide intermediate solutions that combine combustion engines with electric assistance, offering improved fuel efficiency and reduced emissions while maintaining operational flexibility.

Battery-Electric Vehicles surge at 21.96% CAGR, representing the industry's most dynamic growth segment driven by environmental regulations and operational economics. Liebherr and Fortescue's USD 2.8 billion partnership to develop 475 zero-emission machines, including 360 autonomous battery-electric T 264 trucks, signals the scale of electrification commitments. Komatsu launched battery-electric versions of drilling and bolting rigs in May 2024, expanding the available electric equipment portfolio. The segment benefits from declining battery costs and improving energy density, making electric alternatives increasingly competitive with traditional powertrains on total cost of ownership metrics.

By Power Output: Mid-Range Dominance Reflects European Mine Characteristics

The 500 to 1,000 HP segment will capture 46.38% of the market share in 2024. It is optimized for European mining scales, which typically involve smaller operations compared to massive Australian or South American facilities. This power range provides an optimal balance between capability and efficiency for most European applications, from Nordic iron ore extraction to Eastern European coal mining. Above 1,000 HP equipment serves large-scale surface operations and specialized applications requiring maximum power output.

Less than 500 HP equipment grows at 9.42% CAGR, driven by the proliferation of compact, electric solutions suitable for narrow-vein underground operations and urban mining applications. Epiroc's Simba SM60 S drilling rig exemplifies this trend, featuring enhanced rod handling efficiency and reduced transport height of 2.8 meters for smaller drift mines. The segment benefits from electrification trends, as battery technology proves most viable in lower power applications where energy requirements remain manageable. Sandvik's introduction of the industry's most advanced narrow vein underground drill demonstrates the innovation focus on compact, high-efficiency equipment for specialized European mining conditions.

By Application: Metal Mining Leads Critical Materials Focus

Metal Mining dominates with 51.06% market share in 2024 and maintains 8.73% CAGR growth, reflecting Europe's strategic focus on critical raw materials extraction for battery and renewable energy supply chains. The segment encompasses copper, nickel, lithium, and rare earth element extraction that supports the EU's green transition objectives. Copper demand alone could create a 3.8 million ton deficit by 2035, driving sustained equipment demand for extraction and processing operations. Mineral mining serves industrial applications, including construction materials and specialty minerals, while coal mining faces declining demand due to renewable energy transitions and maintains equipment replacement needs for existing operations.

The application segmentation reflects Europe's transition from traditional fossil fuel extraction to critical materials enabling decarbonization technologies. Arctic Minerals' Hennes Bay project in Finland, with a JORC-compliant inferred Resource of 55.39 Mt at 1.0% Copper Equivalent, exemplifies the domestic resource development driving metal mining equipment demand. The EU's target to source 10% of strategic raw materials domestically by 2030 creates sustained demand for specialized extraction equipment capable of processing lower-grade ores and complex mineralogy characteristic of European deposits.

Geography Analysis

Germany’s scale, supplier depth, and pro-innovation policies keep it the largest buyer of advanced drills, articulated trucks, and digital monitoring systems. Strong trade-union engagement shapes procurement, emphasizing operator safety features and retraining packages bundled into major deals. France’s faster gear-up centers on lithium, cobalt, and manganese deposits critical to domestic cell plants. Low-interest public loans and a favorable permitting framework cut risk-adjusted payback periods, luring OEM demonstration units and joint development agreements with local universities.

The Nordic bloc showcases the highest technology penetration. Swedish and Finnish mines now run mixed fleets where battery-electric trucks share ramps with overhead-line trolley units, supplying real-world performance data that influences regional standards. Norway’s hydropower surplus underwrites aggressive electrification targets, while Iceland explores geothermal-powered crushing sites, illustrating how renewable abundance shapes specifications in the Europe mining equipment market.

Eastern European producers experience a dual agenda: decarbonize coal while unlocking copper and rare-earth assets. Poland pilots autonomous roof-bolters to improve underground safety, yet still procures diesel haul trucks for legacy lignite pits pending grid reinforcement. Cross-border collaboration programs funded by the EU Just Transition Mechanism equip local suppliers with retrofit expertise, slowly knitting fragmented demand into a more cohesive continental market.

Competitive Landscape

The Europe Mining Equipment market exhibits moderate fragmentation. Caterpillar, Komatsu, and Sandvik headline with diverse portfolios and continent-wide parts distribution, while Atlas Copco, Epiroc, and Liebherr leverage proximity to end-users for rapid customization cycles. Recent years have seen a strategy pivot from pure horsepower races to integrated software ecosystems. Sandvik’s record order for battery-electric underground rigs validated the margin potential of low-emission models, prompting rivals to fast-track similar launches.

Joint ventures dominate electrification: Liebherr’s USD 2.8 billion partnership with Fortescue will furnish 475 zero-emission units across multiple European mines, embedding service and energy-management contracts alongside hardware. Software overlays emerge as a new battleground—cloud-based fleet-management suites that tap real-time haul data to refine charge scheduling and route planning. Rental arms expand as OEMs seek recurring revenue, evidenced by Atlas Copco’s acquisition spree in specialty rental services targeting mid-tier operators.

Smaller specialists seize white space in narrow-vein drills, ore-sorting scanners, and modular battery packs, often licensing IP from academic spin-offs funded through Horizon Europe grants. The resulting ecosystem blends global scale with local agility, ensuring buyers can tailor mixed fleets without vendor lock-in, even as platform interoperability becomes a procurement criterion.

Europe Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Sandvik Group

-

Epiroc AB

-

Liebherr Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Liebherr showcased the future of construction and mining at Bauma 2025 with over 100 exhibits, including the battery-electric, autonomous T 264 mining truck and the electric R 9400 E mining excavator, both designed for zero emissions. The company emphasized digitalization with autonomous machines and intelligent assistance systems, collaborating with Fortescue to develop emissions-free mining machines for sustainable operations.

- March 2025: The European Commission selected 47 Strategic Projects under the Critical Raw Materials Act to enhance domestic raw material capacities, requiring EUR 22.5 billion total investment across 13 EU Member States. Projects include 25 extraction, 24 processing, 10 recycling, and 2 substitution activities focusing on lithium, nickel, cobalt, manganese, and graphite essential for EU battery raw material value chain.

- January 2025: Epiroc and ABB signed a Memorandum of Understanding to collaborate on underground trolley equipment, enhancing electrification solutions in the mining industry. The partnership focuses on increasing productivity and achieving decarbonization targets, building on previous successes in Swedish mines, with 76% of global mining companies seeing benefits in vehicle electrification.

Europe Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 to 1 000 HP |

| Above 1 000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| Germany |

| Italy |

| France |

| Netherlands |

| Spain |

| Poland |

| Rest of Europe |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 to 1 000 HP | |

| Above 1 000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Country | Germany |

| Italy | |

| France | |

| Netherlands | |

| Spain | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is demand for battery-electric mining trucks growing in Europe?

Orders for zero-emission haulage show strong momentum, highlighted by Fortescue’s USD 2.8 billion agreement for 360 autonomous battery-electric trucks, and are forecast to lift the related segment at a 15%-plus CAGR to 2030.

Which European sub-region leads automation adoption in mining?

The Nordic cluster of Finland, Sweden and Norway combines 5G connectivity, abundant renewable power and proactive regulators, making it the clear automation front-runner.

What share of equipment spending comes from contractors versus miners?

Contractors & Service Providers handle roughly one-quarter of purchases today but are the fastest-expanding buyer group at more than 11% CAGR.

How does the Critical Raw Materials Act influence equipment sales?

The Act fast-tracks 47 Strategic Projects that require EUR 22.5 billion in capex, directly translating into multi-year orders for drills, haul trucks, and processing lines.

What is the biggest supply-side bottleneck for electrified fleets?

Grid congestion at remote mine sites delays charging-infrastructure roll-outs, forcing interim hybrid or diesel backup solutions until transmission upgrades come online.

Which equipment category currently holds the largest market share?

Surface Drilling Equipment leads with 38.56% of total regional spending, driven by wide applicability across open-pit and underground projects.

Page last updated on: