Oman Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

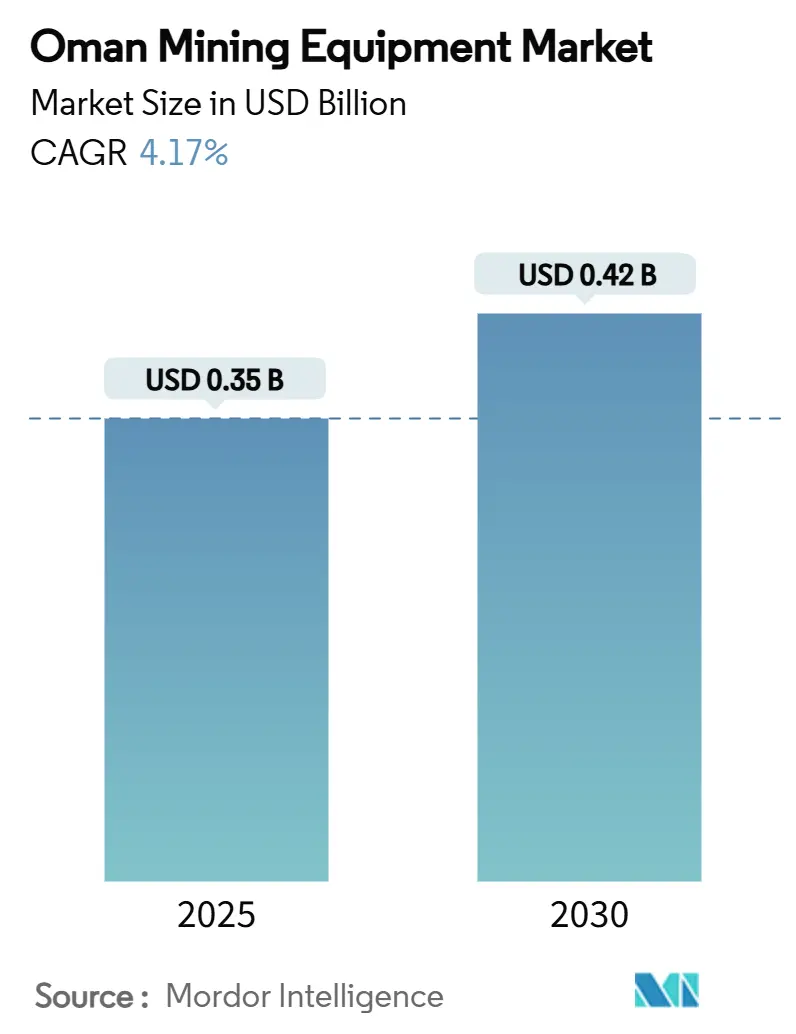

| Market Size (2025) | USD 0.35 Billion |

| Market Size (2030) | USD 0.42 Billion |

| Growth Rate (2025 - 2030) | 4.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Mining Equipment Market Analysis by Mordor Intelligence

The Oman Mining Equipment Market size is estimated at USD 0.35 billion in 2025, and is expected to reach USD 0.42 billion by 2030, at a CAGR of 4.17% during the forecast period (2025-2030). Vision 2040 moves the economy away from hydrocarbons, and the 2020 restructuring of the Ministry of Energy and Minerals has eased licensing, speeding up procurement cycles for modern fleets. Capital spending on new copper-gold projects in the Batinah and Dhofar belts and a mineral‐railway plan linking interior pits to Duqm Port sustains a steady pipeline for drills, loaders, and haulage units. Battery-electric models are gaining traction because 2025 diesel-emission caps tighten compliance windows, while In-Country Value (ICV) rules drive global vendors to set up joint workshops and training centres. Desalinated water costs and import‐heavy supply chains temper enthusiasm. Yet, Mining Development Oman’s massive funds and the Joint Supplier Registration System provide confidence that orders will continue despite these constraints.

Key Report Takeaways

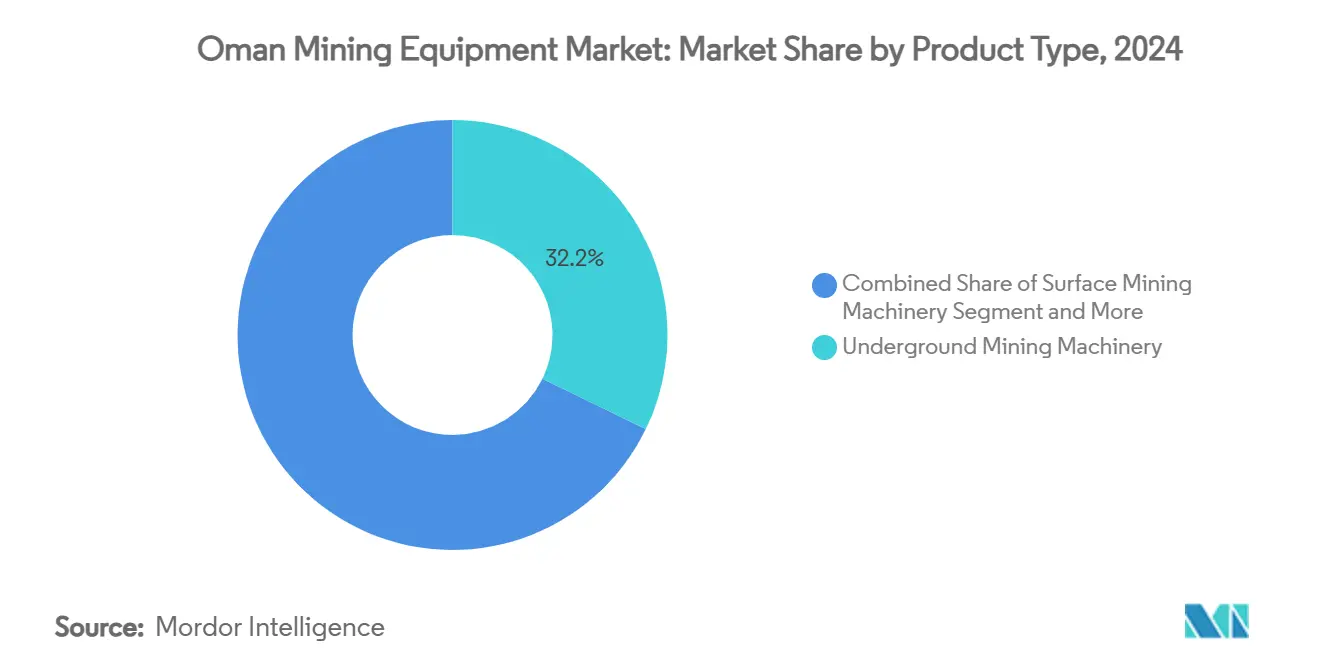

- By product type, underground mining machinery held 32.17% of the Oman mining equipment market share in 2024, and mineral processing machinery is projected to post the fastest 4.26% CAGR, raising its weight in the Oman mining equipment market size through 2030.

- By function type, transportation equipment accounted for 45.11% revenue in 2024 and is forecast to expand at a 4.19% CAGR by 2030.

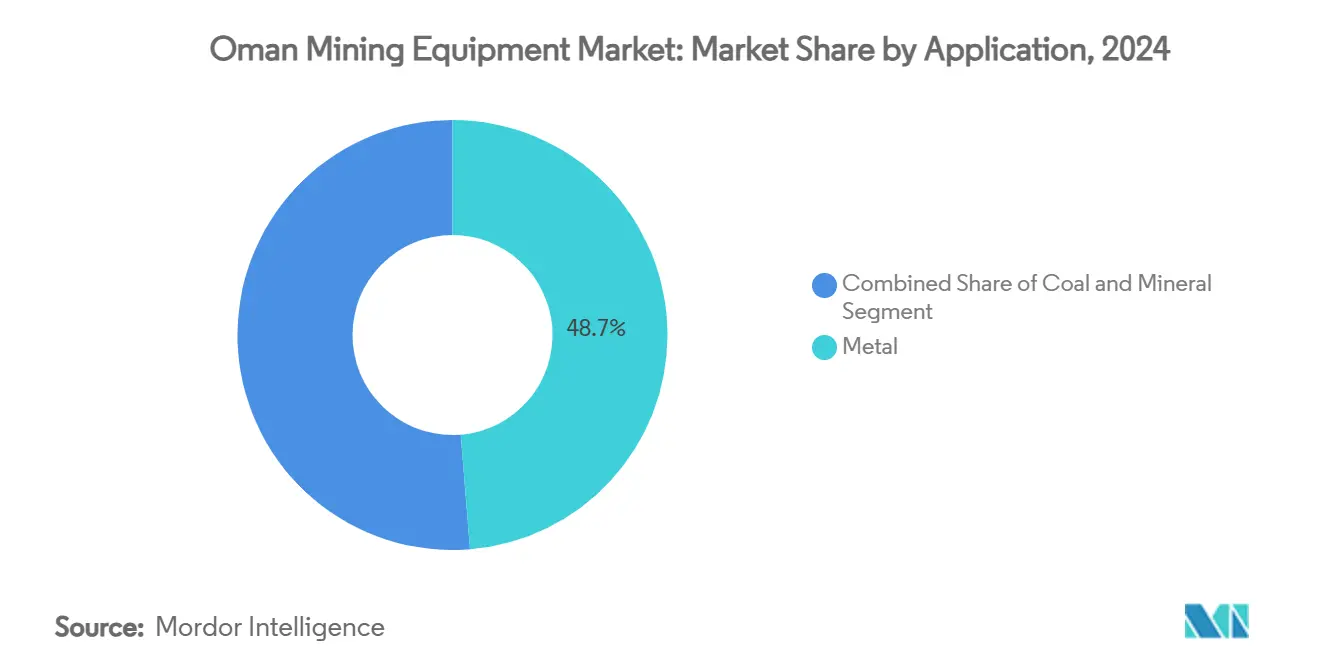

- By application, metal mining represented 48.73% of the Oman mining equipment market size in 2024 and should progress at a 4.31% CAGR to 2030.

- By propulsion type, diesel-powered equipment holds a dominant 71.26% share in 2024. However, battery-electric machines are projected to grow at a CAGR of 14.55%—outpacing the overall growth of the Oman mining equipment market.

Oman Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Government Expenditure | +0.8% | National, concentrated in Batinah and Dhofar | Medium term (2-4 years) |

| Accelerated Copper-gold Discoveries | +0.7% | Batinah and Dhofar regions, spillover to adjacent areas | Long term (≥ 4 years) |

| Mandatory "In-Country Value" Clauses | +0.6% | National, with emphasis on industrial zones | Medium term (2-4 years) |

| Fleet Renewal Prompted | +0.5% | National, priority in urban-adjacent mining sites | Short term (≤ 2 years) |

| Surge in Small-Scale Chromite Mine Leasing | +0.4% | Semail Ophiolite Belt, concentrated around Sohar | Medium term (2-4 years) |

| Pilot Adoption of Autonomous Hauling | +0.3% | Ghubrah region, potential expansion to other limestone sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Government Expenditure on Mining & Quarrying Projects

Mining Development Oman’s massive equity fund allows co-investment in high-grade deposits, translating directly into loader, drill, and plant orders. Large projects such as Yanqul Copper, where the state retains 41%, require entire fleets of underground rigs, hoisting systems, and smart ventilation. Budget allocations also cover the 386 km Mineral Line railway to Duqm, which triggers added demand for bulk-loading hoppers, track-maintenance machines, and on-site locomotives. Digitalization budgets include 3-D modeling, AI-assisted predictive maintenance, and drone surveying, so premium suppliers with integrated software platforms gain a volume edge.

Accelerated Copper-Gold Discoveries in the Batinah & Dhofar Belts

Savannah Resources confirmed high-grade zones at the Aarja prospect and updated geodata listed 79 fresh targets, 26 of which carry positive risk scores despite low copper prices[1]“Block 4 Drilling Update,” Savannah Resources Plc, savannahresources.com . Thick ophiolite sequences force miners underground, lifting demand for low-profile jumbos, battery-electric load–haul–dumpers, and high-capacity boosters. Concentrated discoveries let service crews pool spares, trimming inventory costs and fostering multi-site maintenance hubs. Al Hadeetha Resources is developing an ore system that could absorb dozens of 4 m³ loaders, smart bolters, and block-caving rigs. Streamlined license approvals shorten the lag from drill core to development, smoothing the Oman mining equipment market order book.

Mandatory In-Country Value Clauses Favouring Local Service Contracts

ICV rules set a floor of 10% local spend per award, expanding to two-fifths in flagship deals such as KCA Deutag’s rig contract, which opened multiple Omani jobs[2]“In-Country Value Report 2024,” Petroleum Development Oman, pdo.co.om . Suppliers now team with Sohar and Duqm fabricators to assemble buckets, truck trays, and compressor housings, trimming shipping lead times. Joint Supplier Registration System accreditation increases tender eligibility, so certified distributors enjoy an inside track. Workforce clauses compel OEMs to run operator-training labs, creating a domestic pool of skilled mechanics and data analysts. Local Community Contractor status grants priority in concession zones, nudging foreign brands to embed parts depots in rural mining towns, enlarging the Oman mining equipment market’s aftermarket revenues.

Fleet Renewal Prompted by 2025 Diesel-Emission Caps

New particulate ceilings in 2025 trigger an accelerated retirement of Tier 0 and Tier 1 engines. Sales of battery-electric loaders, trucks, and utility vehicles, already running at a 14.55% CAGR, receive a further lift as operators pre-buy to avoid penalties. Global precedents such as Sandvik’s SEK 750 million battery-electric order for South32 validate business cases that hinge on lower ventilation costs. Liebherr’s USD 2.8 billion zero-emission haul–truck deal with Fortescue shows why miners regard electrification as a long-term hedge against fuel volatility. Oman’s solar and wind build-out underpins low-carbon charging, reducing the total cost of ownership over diesel platforms. Early movers secure carbon-offset credits and social-license benefits that translate to easier financing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Desalinated Water | -0.3% | National, acute in inland mining areas | Long term (≥ 4 years) |

| Limited Local Component-Manufacturing Ecosystem | -0.2% | National, concentrated in industrial zones | Medium term (2-4 years) |

| Delays in Mining-law Secondary Regulations Issuance | -0.2% | National, affecting all mining concessions | Short term (≤ 2 years) |

| Fluctuating Export Prices | -0.1% | National, with emphasis on coastal mining operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Desalinated Water for Dust Suppression

Oman’s annual water gap forces mines to purchase desalinated output, a cost well above global drill-site norms. Every open-pit haul road demands thousands of cubic meters daily for dust control, raising opex and curbing capital budgets. Batinah groundwater salinization intensifies the squeeze, competing with agriculture. Although hybrid solar-RO plants are planned, relief is medium-term, so operators pivot to dry-fog nozzles, surfactant additives, and enclosed conveyor belts that lower spray requirements. OEMs selling water-efficient crushers and sizers gain a comparative advantage in the Oman mining equipment market.

Limited Local Component-Manufacturing Ecosystem

High-precision gears, sensor arrays, and alternators still arrive via Jebel Ali, adding freight, duty, and currency exposure. Sohar’s metalworks sector mainly fabricates structural steel, not Tier-1 machine parts. Repair turnarounds stretch while components clear customs, prolonging downtime and inflating the total cost of ownership. Government incentives for OEM‐backed machining centers exist, yet technology transfer lags because volumes remain modest. Suppliers that bankroll in-country CNC workshops or consignment hubs reduce machine idle time and win long‐term service contracts, partly offsetting this structural drag on the Oman mining equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Underground Machinery Leads Specialized Extraction

Underground units dominated 32.17% of the Oman mining equipment market share in 2024 as narrow high-grade veins underpin demand for drill-jumbos, bolting rigs, and battery LHDs. The Oman mining equipment market size tied to underground fleets will deepen as Al Hadeetha, Yanqul, and Block 4 projects ramp up, requiring multi-level declines, smart ventilation, and seismic monitoring. Komatsu’s WX04B battery LHD launched at MINExpo 2024, fits the 3.5 m-high Semail ophiolite stopes and shortens recharge with a swap battery—an appealing attribute for Batinah belts where ventilation energy is costly.

Mineral processing machinery, though only 14% of 2024 outlays, delivers the fastest 4.26% CAGR, reflecting Vision 2040’s insistence on value-added exports. New sulphide float plants for copper concentrate, a Sohar antimony refinery, and upgraded chromite spirals lift orders for mills, cyclones, and filter presses. FLSmidth’s 13.1% mining EBITA margin in 2024 shows global appetite for such kit. Meanwhile, surface-equipment demand holds steady, servicing limestone and gypsum quarries that feed domestic cement kilns and GCC drywall customers.

By Function Type: Transportation Dominates Dispersed Operations

Oman’s deposits scatter 900 km from Musandam to Dhofar, so haulage, conveyors, and rail stock captured 45.11% of 2024 turnover and are rising 4.19% annually. Long-distance ore-to-port corridors spur spending on 90-t trucks, high-lift loaders, and railcar dumping stations. The new Mineral Line railway triggers needs for ballast tampers, track welders, and EMD freight locomotives—Progress Rail inked a 27-unit deal in October 2024.

Processing equipment follows, lifted by domestic beneficiation directives. Excavation machinery purchases remain resilient because overburden stripping precedes metals and industrial minerals. Autonomy pilots at the Ghubrah limestone block use lidar-guided 100-t rigid trucks, and results show 15% fuel savings, pressing buyers toward sensor-rich fleets that can later shift to battery packs.

By Application: Metal Mining Drives Strategic Focus

Metallic ores delivered 48.73% of 2024 revenue and clocked a 4.31% CAGR, as copper-gold output chases EV demand and regional smelters. The Strategic and Precious Metals Processing Plant in Sohar adds antimony to the mix, encouraging the purchase of hydro-met reactors and vacuum furnaces. The Oman mining equipment market size tied to metals will swell once Block 5’s massive VMS lenses progress beyond PFS, compelling additional twin-boom jumbos and raise-borers.

Industrial minerals—gypsum, limestone, marble—still fill bulk tonnage, but their equipment intensity is lower. Chromite pits near Sohar need compact dozers and spiral separators, though groundwater restrictions cap expansion. Coal remains negligible, consistent with the sultanate’s gas-solar power path and net-zero pledge.

By Propulsion Type: Electric Transition Accelerates

Diesel platforms kept 71.26% of 2024 turnover, yet battery-electric grows 14.55% annually, double the headline Oman mining equipment market. Sandvik’s fleet management suite tracks battery cycles and charger utilization, proving payback under five years on a 10-level mine plan. Hybrid systems bridge the gap, mixing downsized engines with regen braking; Caterpillar’s trial with CRH in 2025 deploys such drivetrains in 70-t trucks at a limestone pit just outside Ibri.

The government plans to supply 40 million solar panels and 2,000 turbines with green electricity, smoothing the shift to electric fleets. Liebherr’s R 9600-E concept studies show 20% life-cycle opex savings when solar PPAs fix power at USD 0.028 per kWh.

Geography Analysis

Batinah’s ophiolite corridor remains the heart of the Oman mining equipment market. Easy access to Sohar Port lowers freight on heavy machines and a cluster of service depots along Route 1 trims downtime. Block 4 drilling hit 4 % copper over 12 m, motivating Savannah Resources to pre-order additional twin-boom jumbos. Equipment spending in Dhofar picks up as monazite beach-sand projects add dozer-tractors and gravity spirals, while Salalah’s free-zone incentives lure OEM parts warehouses.

Interior governorates such as Al-Dhahirah host the Ghubrah autonomous haul pilot and Yanqul Copper, demanding reliable road-rail links. Minerals Development Oman flew fixed-wing aeromagnetic surveys covering 21,480 km², spotlighting new nickel-cobalt anomalies that, if drilled, will widen the Oman mining equipment market footprint into remote wadis. The Duqm Special Economic Zone’s 150 km² renewables hub provides green power for a planned 1 Mtpy copper rod plant, tying port cranes, stacker-reclaimers, and high-tonnage loaders into broader logistics spend.

Musandam’s limestone quarries, though smaller, still import crawler drills and harbor conveyors via Khasab. Government balance-development mandates channel road upgrades into these northern enclaves, improving low-bed trailer access for oversized machines. Across all geographies, vendors with mobile service vans and tele-diagnostic centers gain loyalty because site dispersion complicates spare-parts logistics in the Oman mining equipment market.

Competitive Landscape

The Oman mining equipment market is moderately fragmented; the top five OEMs command around 35% combined share, leaving room for niche specialists. Caterpillar, Komatsu, and Sandvik leverage autonomous haulage and analytics packages, while Liebherr’s zero-emission line captures early movers seeking ESG differentiation. Market entry barriers rose in 2023 once Joint Supplier Registration became mandatory for public contracts; certified dealers Al Bahar and General Engineering Services thus enjoy a tendering edge.

ICV compliance forces multinationals to localize value; Komatsu partnered with Sohar-based Sharakah Workshops to assemble rock-breaker booms, and Sandvik opened a Dhofar parts warehouse staffed by Omani graduates. White-space competition emerges in software: Sensmore raised USD 7.3 million for Physical-AI that retrofits autonomy onto legacy fleets, challenging OEM embedded stacks[3]“Series A Funding Round Details,” Sensmore, sensmore.ai . Regional distributors Al Marwan Machinery and Abdul Latif Jameel Machinery differentiate via 24/7 remote-support platforms and consignment stock.

Price rivalry is tempered by lifecycle contracts that bundle analytics, spares, and operator training, shifting focus toward uptime guarantees. Vendors capable of 95% mechanical availability win multi-site framework deals, a decisive factor because Batinah and Dhofar operations operate far from Muscat workshops. As electrification accelerates, partnerships with IPP solar developers give OEMs a competitive hook, bundling mobile chargers and power-purchase agreements into equipment bids.

Oman Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd

Sandvik AB

Epiroc AB

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sandvik secured a SEK 750 million order for battery-electric underground units from South32’s Hermosa project, deliveries 2026-2030.

- October 2024: Progress Rail signed for 27 EMD locomotives to bolster freight links between Oman and the UAE.

- September 2024: Liebherr and Fortescue expanded their alliance with a USD 2.8 billion commitment for 475 zero-emission machines, including 360 autonomous T 264 trucks.

Oman Mining Equipment Market Report Scope

| Underground Mining Machinery |

| Open-Pit Mining Machinery |

| Surface Mining Machinery |

| Drills & Breakers |

| Crushing, Grinding, Filtering & Screening Equipment |

| Mineral Processing Machinery |

| Transportation |

| Processing |

| Excavation |

| Coal |

| Mineral (Industrial) |

| Metal (Base & Precious) |

| Diesel-Powered Equipment |

| Battery-Electric Equipment |

| Hybrid Equipment |

| By Product Type | Underground Mining Machinery |

| Open-Pit Mining Machinery | |

| Surface Mining Machinery | |

| Drills & Breakers | |

| Crushing, Grinding, Filtering & Screening Equipment | |

| Mineral Processing Machinery | |

| By Function Type | Transportation |

| Processing | |

| Excavation | |

| By Application | Coal |

| Mineral (Industrial) | |

| Metal (Base & Precious) | |

| By Propulsion Type | Diesel-Powered Equipment |

| Battery-Electric Equipment | |

| Hybrid Equipment |

Key Questions Answered in the Report

How large is the Oman mining equipment market in 2025?

The Oman mining equipment market size is USD 0.35 billion in 2025 and is projected to reach USD 0.42 billion by 2030.

Which equipment type sells the most units in Oman?

Transportation machines hold 45.11% of 2024 revenue, reflecting dispersed deposits that rely on haulage fleets.

What growth pace is expected for battery-electric machinery?

Battery-electric equipment shows a 14.55% CAGR, outpacing the overall 4.17% market rate as firms prepare for 2025 emission caps.

How do In-Country Value rules affect suppliers?

ICV mandates require 10% local expenditure, so OEMs that set up Omani assembly, training, and parts centers gain contract preference.

What geographic areas see the heaviest demand?

Batinah and Dhofar belts dominate due to copper-gold discoveries, while Duqm and interior governorates grow as new rail links unlock deposits.

Page last updated on: