Australia Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

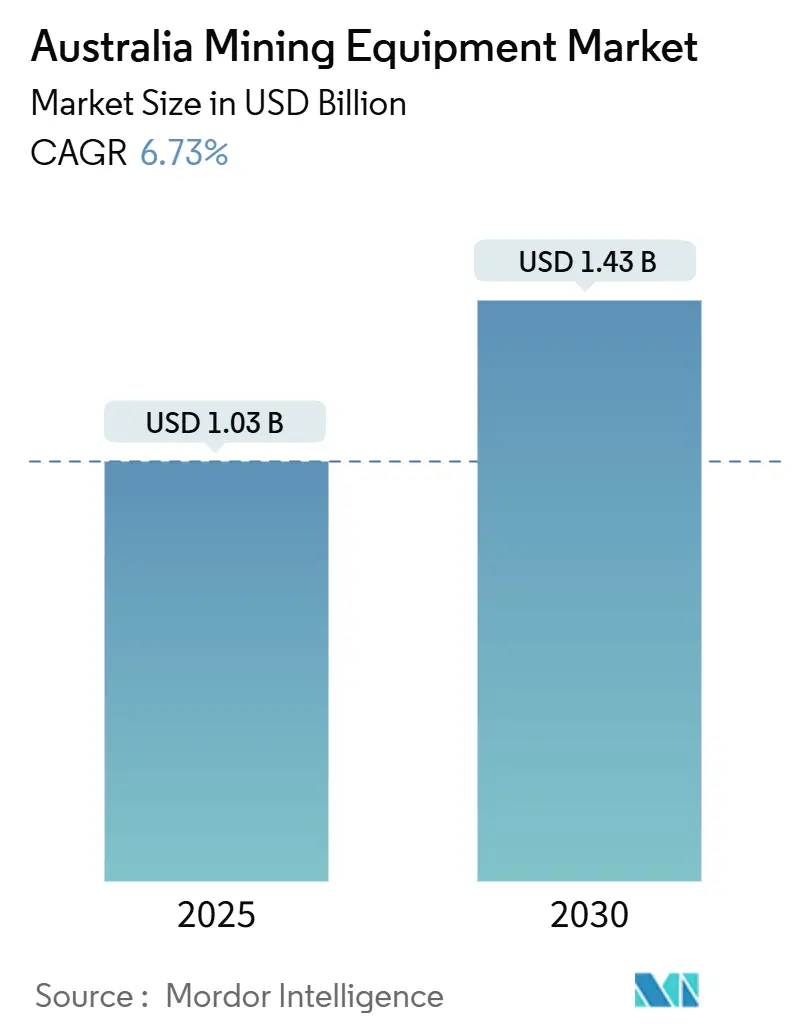

| Market Size (2025) | USD 1.03 Billion |

| Market Size (2030) | USD 1.43 Billion |

| Growth Rate (2025 - 2030) | 6.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Mining Equipment Market Analysis by Mordor Intelligence

The Australian Mining Equipment Market size is estimated at USD 1.03 billion in 2025, and is expected to reach USD 1.43 billion by 2030, at a CAGR of 6.73% during the forecast period (2025-2030). Sustained capital spending by major iron-ore, copper, and lithium producers, generous federal incentives for low-emission fleets, and the rapid shift toward autonomous haulage underpin the current upcycle in the Australian mining equipment market. Dump trucks dominate fleet purchases because long-haul open-pit operations still require large payload capacity. Yet, battery-electric loaders and drills are scaling fast as underground mines chase ventilation savings. Demand momentum is further supported by rental fleets that let contract miners reduce upfront outlays, while OEMs deepen local rebuild capabilities to counter prolonged component lead times. Near-term downside risk comes from commodity price swings and skilled-labour shortages, but operators continue to modernize fleets to maintain productivity, safety, and ESG compliance.

Key Report Takeaways

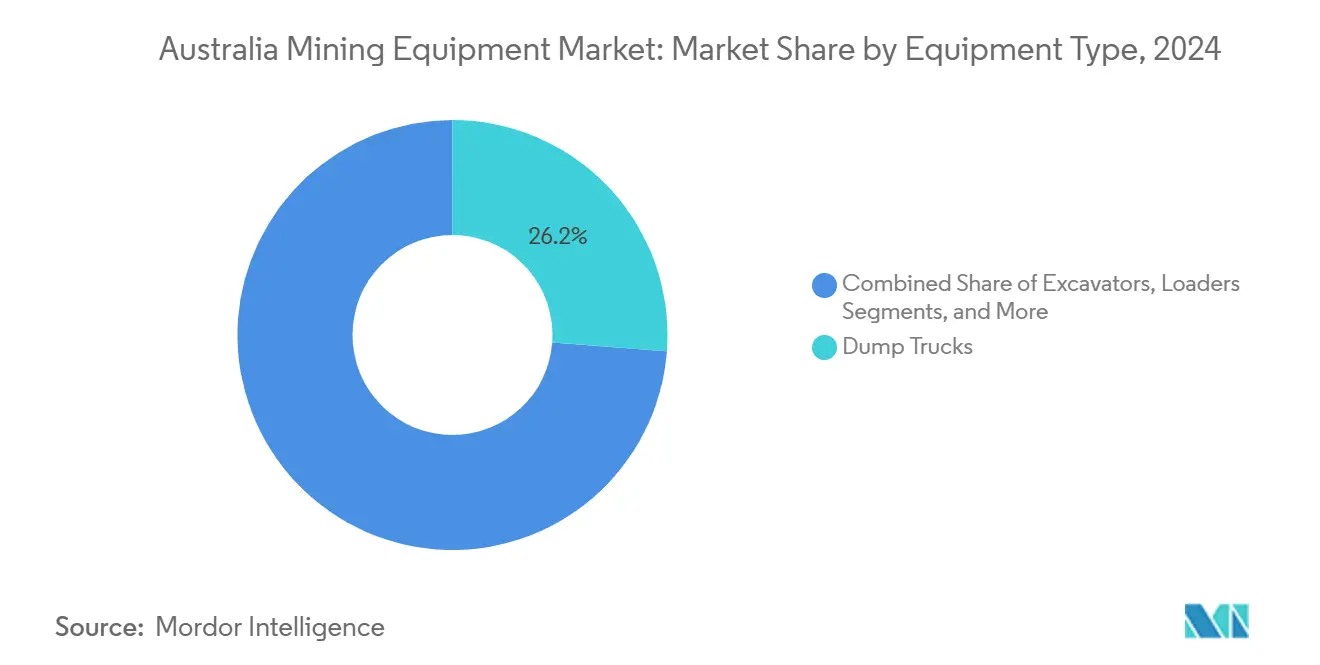

- By equipment type, dump trucks led with 26.23% of the Australian mining equipment market share in 2024, while battery-electric loaders are forecast to expand at a 6.84% CAGR to 2030.

- By equipment category, surface mining accounted for a 52.24% share of the Australian mining equipment market in 2024, and underground equipment is projected to grow at a 6.79% CAGR through 2030.

- By application, metal mining held a 45.01% share of the Australian mining equipment market size in 2024, with mineral mining advancing at a 6.81% CAGR to 2030.

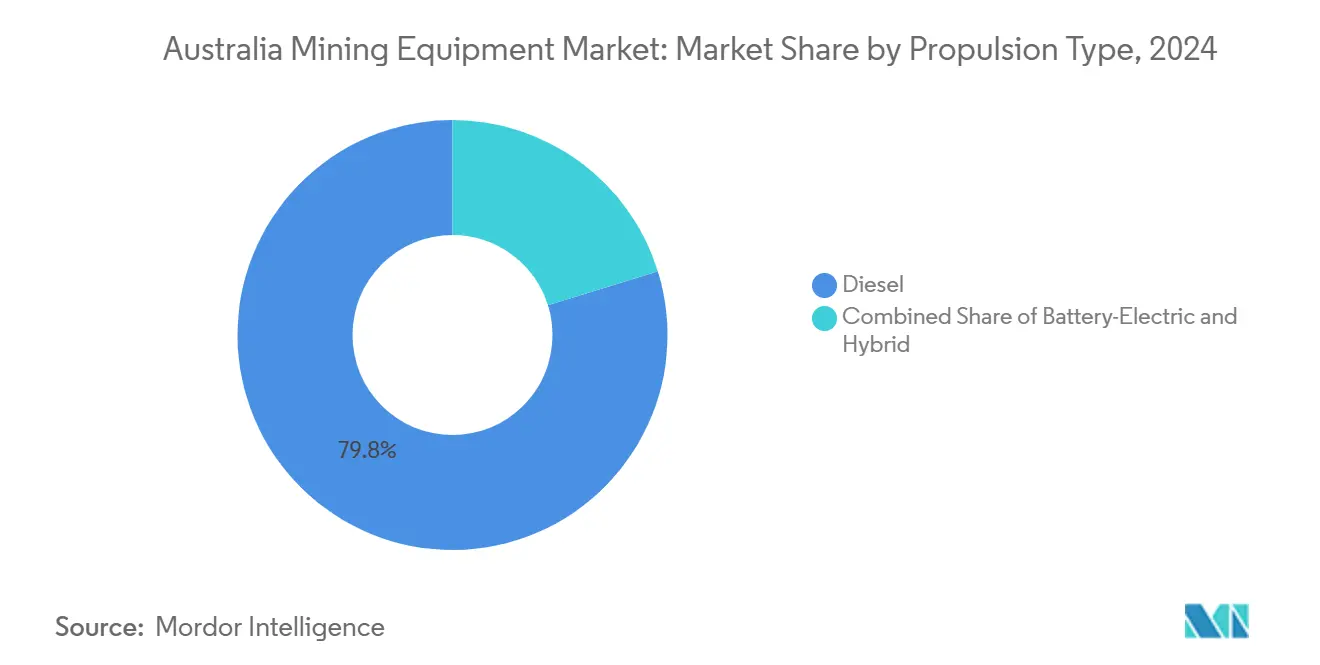

- By propulsion type, diesel systems comprised 79.81% of the Australian mining equipment market share in 2024; battery-electric units are set to rise at a 6.88% CAGR through 2030.

Australia Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in bulk-commodity CAPEX pipeline | +1.2% | National, concentrated in WA Pilbara and QLD mining regions | Medium term (2-4 years) |

| Autonomous-equipment adoption | +1.1% | National, led by WA iron ore operations | Long term (≥ 4 years) |

| Ageing-fleet replacement cycles | +0.9% | National, particularly in coal and gold mining regions | Medium term (2-4 years) |

| Government incentives | +0.8% | National, with early adoption in NSW and WA | Short term (≤ 2 years) |

| Contract-mining boom lifts rental | +0.7% | National, concentrated in remote mining locations | Short term (≤ 2 years) |

| Subscription-based predictive-maintenance models | +0.4% | National, early adoption in large-scale operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Bulk-Commodity CAPEX Pipeline

Record investment outlays by majors are swelling order books for haul trucks, excavators, and autonomous drills. Rio Tinto increased its 2025 capital guidance and BHP’s South Flank posted successive production records, signalling sustained tender flow for large-class surface equipment[1]“2025 Capital Markets Day,” Rio Tinto, riotinto.com . In 2023-24, the Federal Resources and Energy Quarterly allocated a significant portion of its investments in mining, primarily targeting iron-ore expansions and developing critical minerals. New pits and waste-stripping projects necessitate the timely delivery of fleets, benefiting equipment suppliers. The Australian mining equipment market enjoys multi-year visibility, bolstered by surging demand for lithium, copper, and rare-earth elements, all tied to the global energy transition. As producers weave next-generation safety and productivity systems into their project budgets, autonomous haulage retrofit packages emerge as a lucrative revenue stream.

Autonomous-Equipment Adoption

Australia's embrace of autonomous and tele-remote machinery has positioned it as a pivotal player in shaping global technology roadmaps. Autonomous Haulage System and Command platforms have demonstrated their effectiveness, increasing output by approximately 40% and reducing fuel consumption by 10%, as evidenced by their deployment. Key mining regions have robust communications infrastructure that enables near-real-time data transmission between pits and control centers. By integrating LiDAR, radar, and AI-driven obstacle detection as standard features, OEMs cut down on incremental costs and broaden the spectrum of potential sites. With a steadfast commitment to workforce decarbonisation and safety, the push for autonomous capabilities has become a non-negotiable criterion in new mine approvals, solidifying the trajectory for Australia's mining equipment market.

Ageing-Fleet Replacement Cycles

In New South Wales (NSW), authorities mandate the retrofitting or retirement of pre-Tier Two engines, a trend mirrored in various Australian regions. Some operators prioritize autonomous readiness and high-voltage battery platforms to replace aging units when seeking quotations. They've allocated a reasonable budget for equipment renewal programs, encompassing component rebuilds and factory remanufacturing contracts. Mid-life overhaul specialists are experiencing a consistent influx of spare parts and services, expanding the Australian mining equipment industry. These activities ensure a steady baseline demand, even amidst fluctuating commodity prices.

Government Incentives for Low-Emission Fleets

Federal resource funding and targeted tax offsets are now alleviating part of the incremental costs associated with battery-electric and Tier 4-final diesel equipment. These initiatives encompass Tier 4 standards for all new mobile plants, hastening replacement schedules, and promoting trials of cable-electric blasthole rigs and underground LHDs. A pilot by the Electric Mine Consortium demonstrated that fully electric underground loaders can reduce ventilation power needs by significant percentages, aligning their total cost of ownership with that of diesel units. Mid-tier miners, once hesitant to upgrade, are now tapping into concessional loans, leading to a noticeable rise in electric-ready orders with OEMs. Additionally, substantial infrastructure grants, particularly funneled into Queensland's nickel, cobalt, and graphite processing, are expanding the market for low-carbon equipment packages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-price volatility | -1.80% | National, with higher impact on marginal operations | Short term (≤ 2 years) |

| Skilled-labour shortages | -1.10% | National, acute in WA Pilbara and remote QLD operations | Long term (≥ 4 years) |

| Emission-compliance cost burden | -0.90% | National, concentrated in coal mining regions | Medium term (2-4 years) |

| Prolonged OEM component lead-times | -0.70% | National, affecting all equipment categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility

As lithium carbonate benchmarks plunged, spodumene producers postponed their sustaining-capital budgets. Board approvals now routinely involve scenario planning, leading some miners to break down fleet tenders into phased options tied to price triggers. These deferred orders send ripples through dealer pipelines, extending the payback horizons for new workshops. While the federal critical-minerals fund commits to enhancing value-added processing, procurement managers are treading carefully until demand stabilizes. This caution is expected to temper any immediate growth in the Australian mining equipment market.

Emission-Compliance Cost Burden

Large-class trucks see two-fifths of their purchase price consumed by Tier 4-final engines, diesel particulate filters, and selective catalytic reduction systems. Small operators grapple with the challenges of retrofitting legacy fleets, facing extended downtimes, craneage issues, and the hunt for specialist labor. Coal mines in NSW and QLD, operating older fleets, confront heightened compliance challenges. They also face the added financial burden of investing in fugitive methane abatement. Although grants alleviate some of this financial strain, many operators resort to short-term leasing instead of outright purchases, leading to a slowdown in unit sales volumes. While OEMs are rolling out flexible finance plans in response, the capital challenges pose a significant headwind for the Australian mining equipment market in the coming years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Dump Trucks Lead Despite Electric Loader Surge

In 2024, dump trucks commanded a dominant 26.23% share of the Australian mining equipment market, driven by the needs of long-haul iron-ore and coal pits requiring 200-400-tonne payloads. Enhancements like second-generation autonomous retrofit kits and advanced tyre monitoring systems boost truck uptime, solidifying their role in productivity gains.

While still a niche, battery-electric loaders are witnessing the swiftest growth at a 6.84% CAGR, as underground miners chase ventilation cost savings and adhere to regulatory emission limits. Komatsu’s WX04B battery-swap LHD, tailored for narrow-vein mines in hard rock operations, showcases the adaptability of high-energy-density batteries within existing tunnel profiles. Electric-ready excavators lead the charge, contributing to nearly 40% of fuel-efficiency gains, aligning seamlessly with operator carbon budgets. Though motor graders, dozers, and specialist drills operate in smaller volume pools, they reap benefits from technological advancements like AI-guided blade control and autonomous drilling.

By Equipment Category: Surface Mining Dominance Amid Underground Growth

In 2024, surface mining equipment commanded a 52.24% share of the Australian market, bolstered by robust iron-ore operations transporting vast tonnages annually. Key players in these open pits include autonomous haul trucks, 700-ton class excavators, and large-radius drills. Meanwhile, underground equipment is rising, boasting a 6.79% CAGR, driven by the transition of deeper copper, nickel, and gold deposits from feasibility studies to active extraction. Recent investments in fully electric autonomous drills underscore the growing demand for low-emission fleets in underground operations.

In the Australian mining equipment sector, there's a notable shift from reactive to predictive maintenance models for surface fleets. This transition reduces planned downtime and enhances output per operating hour. Underground operators are increasingly turning to battery-powered Load-Haul-Dump (LHD) vehicles. This shift is primarily to mitigate costs associated with diesel-particulate filtration and ventilation. The savings on ventilation fans justify the higher upfront cost of battery LHDs. Additionally, hybrid shotcrete units and tethered jumbo drills are being embraced for adaptability during the industry's electrification phase. Original Equipment Manufacturers (OEMs) are also capitalizing on this trend, offering training simulators to enhance operator skills in both surface and underground settings, thereby boosting their aftermarket revenue. As miners diversify their portfolios across multiple ores, there's a pressing need to optimize capital allocation between surface and underground fleets. This strategic balance is pivotal for fostering growth in the Australian mining equipment market's total addressable demand.

By Propulsion Type: Diesel Dominance Challenged by Electric Transition

In 2024, diesel technology commanded a 79.81% share of the Australian mining equipment market. This dominance is attributed to diesel's long refuelling intervals and the maturity of its powertrains, adeptly handling the extreme 50 °C conditions of the outback. Meanwhile, battery-electric units are surging ahead, boasting a 6.88% CAGR, outpacing all other propulsion formats. Hybrid solutions fill the technological void, offering incremental fuel savings without requiring extensive infrastructure overhauls. The MegaWatt Charger prototype makes waves, enabling sub-30-minute dumps for 240-kWh battery packs and addressing concerns over perceived utilisation penalties.

While diesel overhaul capacity remains a linchpin in the Australian mining equipment industry, workshops proactively install high-voltage isolation bays, gearing up for the impending electric-truck fleets. Mines are also integrating renewable energy micro-grids, ensuring a consistent supply of green power and aligning with their Scope 1 reduction targets. Looking ahead, the next decade promises a split in propulsion demand: large surface mines are poised to transition to hydrogen or battery trucks, contingent on advancements in charging and haul-road grades. In contrast, underground sectors lean towards complete battery solutions to curtail ventilation costs.

By Application: Metal Mining Leadership with Mineral Mining Acceleration

In 2024, metal mining dominated the Australian mining equipment market, claiming a 45.01% share, buoyed by robust iron-ore outputs exceeding 900 million tonnes annually. Australian Mines hubs, driven by productivity targets, maintain a steady demand for high-horsepower trucks and loaders. Meanwhile, mineral mining, focusing on lithium, graphite, and rare earths, is projected to grow at a 6.81% CAGR, bolstered by federal grants that mitigate project finance risks. This substantial investment highlights the government's dedication to enhancing downstream value chains. While coal remains a significant player, it's grappling with transition challenges. Yet, coking coal operations continue to invest in large dozers for strip removal, providing a buffer against decline.

In Australia's mining equipment sector, mineral miners gravitate towards modular, battery-ready fleets, aiming to draw in ESG-linked capital. Metal mines are channeling significant investments into autonomous rail systems, ensuring seamless integration with port logistics. Leading global players in autonomous operations are harnessing a standardized digital architecture across the iron ore and copper sectors, optimizing maintenance processes. As the market evolves, equipment suppliers recognize the need to customize their offerings based on diverse cash-flow profiles: while high-margin iron-ore operations lean towards outright purchases, budding mineral developers gravitate towards lease-to-own or revenue-sharing models. This nuanced segmentation not only deepens the market but also fortifies its resilience.

Geography Analysis

In 2024, Western Australia dominated the Australian mining equipment market, bolstered by iron-ore complexes utilizing 400-tonne trucks, 700-ton excavators, and autonomous trains stretching a kilometre. The region boasts over 350 autonomous haul trucks in operation, driving a steady demand for parts and services. State policies, including the Battery and Critical Minerals Strategy, aim to significantly boost economic contributions by the end of the decade, accelerating the shift towards electric and autonomous units in a bid for decarbonisation.

Queensland's mining equipment market is surging, fueled by expansions in metallurgical coal and critical minerals. A significant boost is expected from the multi-billion-dollar CopperString 2032 transmission line project [2]“Project Overview,” CopperString 2032 Pty Ltd, copperstring.com.au . NRW and CIMIC's crusher project contract fills the tender pipelines for surface equipment. Additionally, state safety regulations amplify the demand for Tier 4 engines and collision-avoidance systems. New South Wales, benefiting from Hunter Valley coal operations and proactive autonomous haul safety guidelines, is witnessing increased replacement expenditures.

While South Australia, Tasmania, and the Northern Territory play smaller yet growing roles, South Australia stands out with the OZ Minerals Carrapateena expansion and pilot plants for critical minerals. These developments necessitate specialized underground loaders and paste-fill systems. Meanwhile, the Northern Territory's Butcherbird manganese mine is experimenting with autonomous trucks, highlighting the spread of advanced haulage solutions. Challenges posed by remote locations boost the attractiveness of rental fleets and predictive-maintenance subscriptions, aiding suppliers in tapping into new areas of the Australian mining equipment market. Throughout the nation, factors like emissions caps, a shortage of skilled labor, and infrastructure deficiencies shape technology adoption trends, impacting regional order compositions and the intensity of aftermarkets.

Competitive Landscape

The Australian mining equipment market is moderately concentrated. Caterpillar, Komatsu, and Liebherr anchor top-tier positions through broad portfolios, large dealer footprints, and in-country component hubs established since the 1950s[3]“Caterpillar in Australia – Historical Milestones,” Caterpillar Inc., cat.com .

In today's landscape, technology leadership is a more decisive factor for success than sheer manufacturing scale. OEMs are now bundling predictive-maintenance software, mixed-reality training, and performance-based financing, creating a tighter customer bond.

As competition heats up, new players from China and South Korea are introducing battery-electric prototypes tailored for mid-tier mines. This move threatens established vendors, urging them to hasten their innovation efforts. Looking ahead, the depth of R&D investments, the extent of after-sales services, and the ability to expand into emerging markets will play pivotal roles in determining market standings and driving long-term growth.

Australia Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery

Liebherr Group

Epiroc AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BHP announced a strategic partnership with XCMG to co-design battery-ready mining fleets for Australian sites.

- April 2025: Epiroc secured an MAUD 350 (SEK 2.2 billion) order to deliver autonomous, cable-electric Pit Viper 271 E and battery-electric SmartROC D65 BE rigs to Fortescue’s Pilbara mines.

Australia Mining Equipment Market Report Scope

| Excavators |

| Loaders |

| Dozers |

| Motor Graders |

| Dump Trucks |

| Others |

| Underground Mining |

| Surface Mining |

| Crushing/Pulverising/Screening |

| Drills & Breakers |

| Others |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| Diesel |

| Battery-Electric |

| Hybrid |

| By Equipment Type | Excavators |

| Loaders | |

| Dozers | |

| Motor Graders | |

| Dump Trucks | |

| Others | |

| By Equipment Category | Underground Mining |

| Surface Mining | |

| Crushing/Pulverising/Screening | |

| Drills & Breakers | |

| Others | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Propulsion Type | Diesel |

| Battery-Electric | |

| Hybrid |

Key Questions Answered in the Report

What is the 2025 size of the Australian mining equipment space, and how fast will it expand?

Spending totals USD 1.03 billion in 2025 and is forecast to reach USD 1.43 billion by 2030 on a 6.73% CAGR, driven by CAPEX pipelines, low-emission incentives, and automation roll-outs.

Which equipment category commands the largest share of Australian purchases?

Dump trucks hold the lead with a 26.2% share thanks to long-haul iron-ore and coal operations that require 200-400-tonne payload capacity.

How quickly are battery-electric machines penetrating Australian fleets?

Battery-electric units post the fastest rise, growing at 6.88% CAGR through 2030 as emission rules and lower ventilation costs incentivise underground and surface deployments.

Why are rental and leasing options gaining traction among Australian mines?

Contract-mining expansion and capital-efficiency goals push operators toward rental fleets, a segment projected to grow at 6.92% CAGR while offering bundled maintenance and rapid technology access.

Which Australian states deliver the strongest equipment demand?

Western Australia remains the largest buyer due to Pilbara iron-ore hubs, whereas Queensland shows the fastest growth powered by metallurgical coal projects and CopperString 2032 infrastructure spending.

How concentrated is supplier competition in Australia’s mining equipment landscape?

The top five OEMs control roughly around three-fifths of sales, yielding a moderate concentration score of 6—large incumbents dominate high-volume segments, but niche and service specialists still secure a meaningful share.

Page last updated on: