Saudi Arabia Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

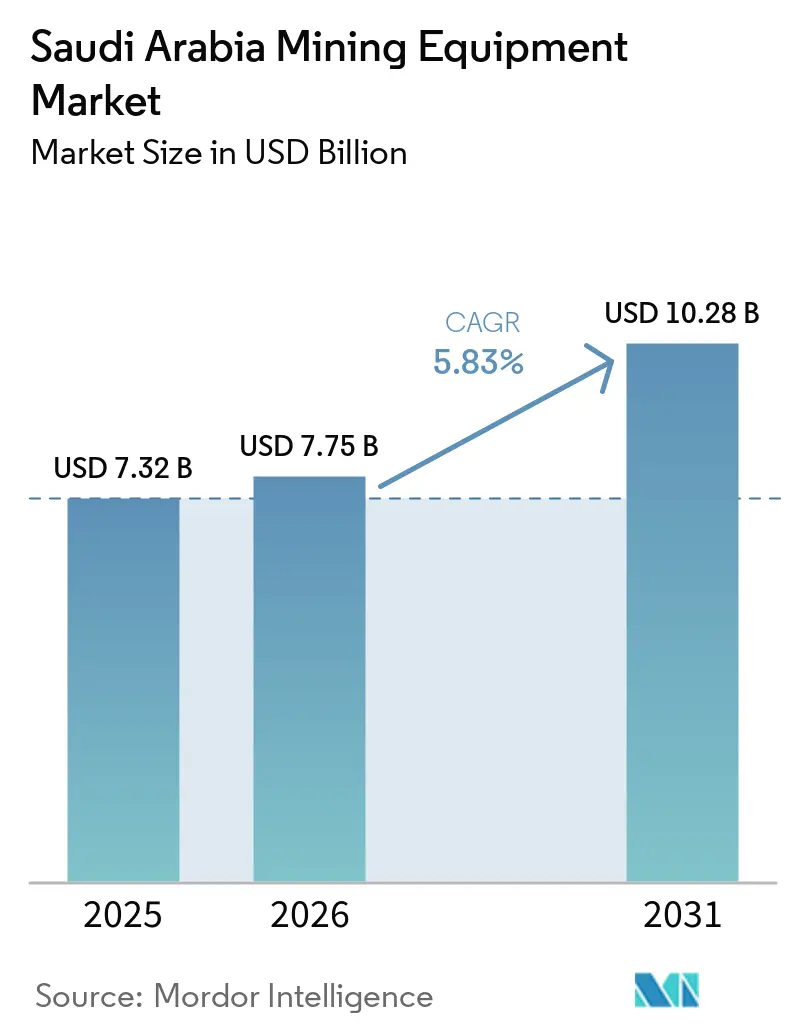

| Base Year Market Size (2025) | USD 7.32 Billion |

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 10.28 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Mining Equipment Market Analysis by Mordor Intelligence

The Saudi Arabia mining equipment market size was valued at USD 7.32 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 10.28 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031). Vision 2030 aims to significantly increase mining's contribution to GDP. This ambition is supported by Ma’aden's extensive capital plan, which invests heavily in excavation, hauling, and downstream processing. Exploration licenses have seen substantial growth, with a recent round releasing a large area of hard-rock terrain for private bidding, creating opportunities for drills, trenchers, and mobile crushers. With rising diesel prices, there is increased focus on fuel costs, driving trials of battery-electric haulage and trolley-assist systems. Local-content quotas for larger contracts have shifted purchasing preferences. This change benefits OEMs with assembly hubs, service centers, or technical academies in Saudi Arabia, offering protection for incumbent suppliers against low-cost imports.

Key Report Takeaways

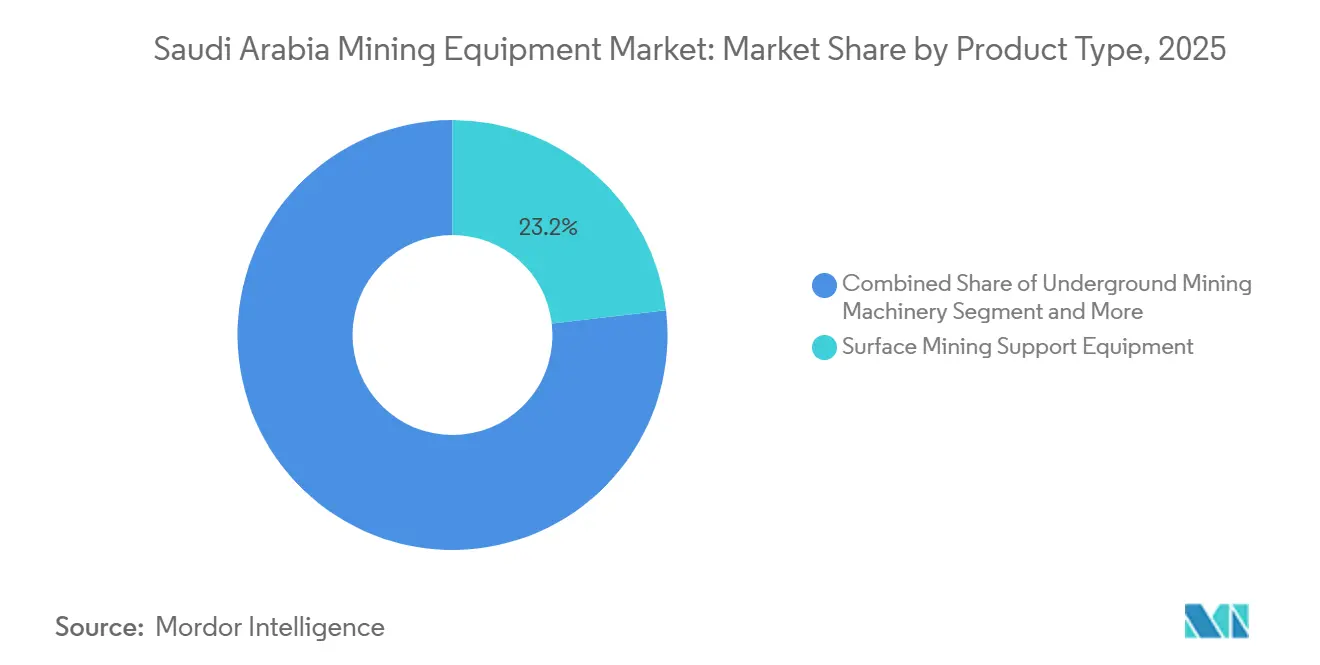

- By product type, Surface Mining Support Equipment led with 23.16% of the Saudi Arabian mining equipment market share in 2025. Drills & Breakers is projected to advance at a 6.17% CAGR through 2031, the fastest among all product groups.

- By function, Excavation accounted for 41.16% of the Saudi Arabian mining equipment market in 2025. Processing is set to expand at a 6.22% CAGR between 2026 and 2031, outpacing hauling and other support functions.

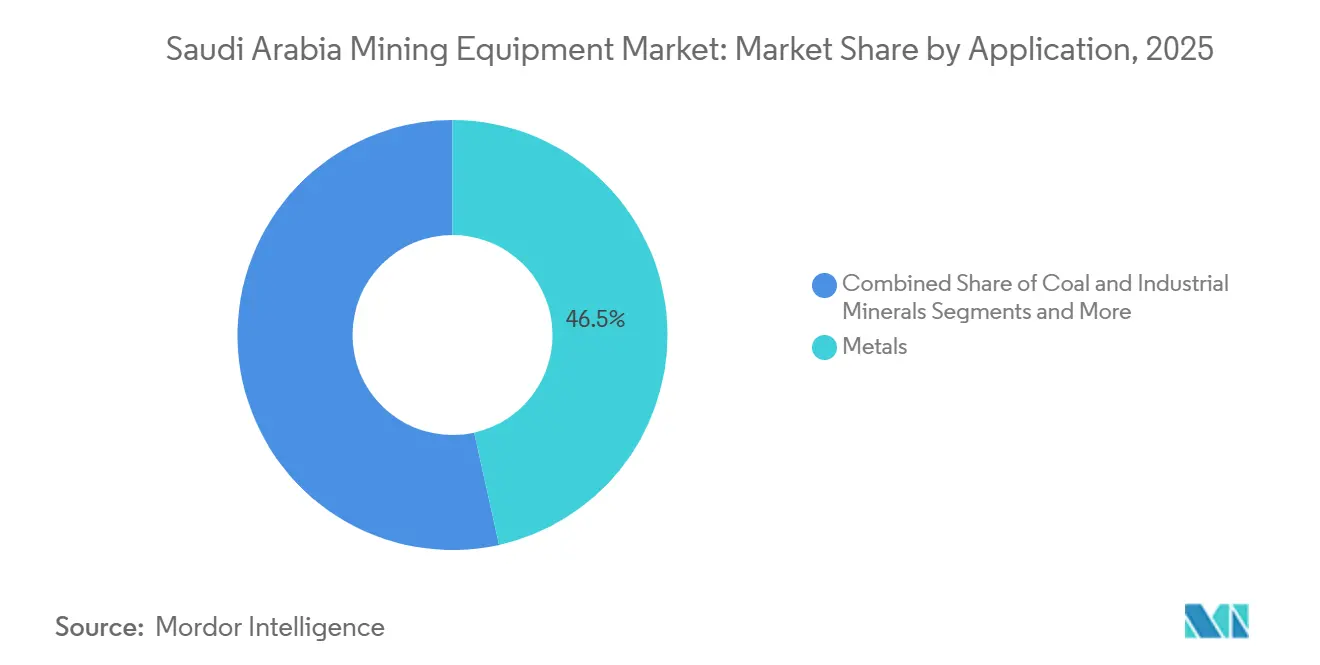

- By application, Metals commanded 46.53% share in 2025 and is expected to grow at 5.95% CAGR to 2031, benefiting from gold and battery-metal projects.

- By power source, Battery-Electric equipment is forecast to post a 9.31% CAGR over 2026-2031 versus diesel’s flat trajectory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Mine Privatizations | +1.2% | National, with concentration in Riyadh and Eastern Province | Medium term (2-4 years) |

| Hard-Rock Exploration Surge | +1.0% | Arabian Shield region, Northern and Western provinces | Short term (≤ 2 years) |

| Battery-Metal Refinery Expansion | +0.9% | Eastern Province and NEOM corridor | Medium term (2-4 years) |

| Local-Content Quotas | +0.8% | National, with manufacturing hubs in Ras Al Khair and Jubail | Long term (≥ 4 years) |

| Mine Automation & 5G Corridors | +0.7% | NEOM, Riyadh, and major mining sites | Medium term (2-4 years) |

| Diesel-to-Electric Conversion Incentives | +0.6% | National, with early adoption in mega-projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030-Linked Mine Privatizations

The issuance of 61 exploration licenses in 2025 illustrates the most aggressive release of mineral acreage since sector liberalization[1] “Annual Statistics 2025,”, Ministry of Industry and Mineral Resources, misa.gov.sa. Spending on early-stage drilling has significantly increased over time. However, a several-month lag exists between licensing and fleet procurement, resulting in a multi-year order book for blasthole drills and mobile crushers. Anchoring baseline demand is Ma’aden’s extensive program. In contrast, smaller players like Hancock Prospecting are leaning towards rental fleets and equipment-as-a-service models. Local-content regulations mandate OEMs to establish parts warehouses or assembly cells. A case in point is Tesmec, which plans to localize trenching-machine assembly in the near future, underscoring this trend. While these measures expand employment opportunities, they also elevate short-term capital expenditures as vendors set up duplicate facilities domestically.

Surge in Hard-Rock Exploration Licences

Across the Arabian Shield, gold, copper, and zinc prospects are increasingly turning to high-penetration rotary drills and wear-resistant hammers, diverting investments from gentler phosphate rigs. Epiroc, in collaboration with Binshehab, has begun stocking face and production drill rigs in Dammam, aiming to reduce lead times. Only a small percentage of the Shield’s known occurrences comply with JORC or NI 43-101 standards, creating a backlog for core-drilling contractors. Mansourah & Massarah recently achieved their first doré and are progressing toward full production capacity. Meanwhile, Ar Rjum is preparing for an EPCM award with specifications for Sandvik DI650i and DP1100 rigs. Due to arid conditions, numerous projects are now implementing dry-drilling loops. While this increases capital expenditures, it can significantly reduce consumable costs over time.

Rapid Build-Out of Battery-Metal Refineries

EV Metals Group is investing in a lithium hydroxide plant, while Northern Graphite is allocating funds for an anode facility. Both facilities require sub-micron feedstock, pushing legacy phosphate lines to their limits. Metso has secured a significant award for the Ar Rjum gold plant, and FLSmidth has received a major order for Phosphate 3. These turnkey packages now surpass the threshold for large-scale throughput. Capchem's new electrolyte complex is driving a parallel demand for high-purity inputs, even as the Kingdom continues to import the majority of its lithium carbonate and graphite. Due to extended grid queues at Yanbu and Ras Al Khair, projects are being forced to install captive power. This move is inflating capital expenditures per module but also advancing Vision 2030's renewable energy objectives once interconnection issues are resolved.

Mandatory Local-Content Quotas in Equipment Purchasing

The “mandatory list” now includes over 1,000 industrial products, including excavators, haul trucks, and crushers. It also provides a bid uplift for packages sourcing a significant portion of their value domestically. Distributors like Zahid Tractor (representing Caterpillar) and Abdul Latif Jameel Summit (representing Komatsu) enhance their scores by utilizing technician academies. Metso has partnered with Saudi Mining Polytechnic to certify hundreds of technicians annually. Meanwhile, Epiroc operates a large parts hub in Dammam, achieving high same-day fill rates. Chinese OEMs offer lower prices compared to Western competitors. However, their lower scores on local-content metrics restrict their participation to smaller, non-Ma’aden projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Operator Shortage | -1.1% | National, with acute shortages in remote mining areas | Medium term (2-4 years) |

| High Import Tariffs | -0.9% | National, affecting all equipment imports | Short term (≤ 2 years) |

| Water Use Restrictions | -0.7% | Arid regions, particularly Northern and Central provinces | Long term (≥ 4 years) |

| Volatile Phosphate & Bauxite Prices | -0.5% | Phosphate belt regions and Northern mining areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Skilled Heavy-Equipment Operators

Saudi Arabia’s skill-based work permit scheme, launched in July 2025, categorizes operators into three tiers. Still, supply lags behind demand for autonomous-haul truck supervisors and high-pressure grinding roll technicians. Wage inflation encourages miners to adopt remote-operation platforms that require fewer on-site staff; however, the transition imposes training overheads and delays procurement until competence frameworks mature. Utilization dips when machines queue for licensed drivers, undercutting productivity assumptions baked into purchase business cases and tempering expansion in the Saudi Arabia mining equipment market.

High Import Tariffs on Non-GCC Equipment

A decent number of customs duties applied since January 2025 elevates landed costs for specialist shovels, crushers, and sensor suites sourced outside the GCC common-tariff zone. The customs services fee adds to the total price, prompting miners to prolong replacement cycles or refurbish aging fleets. More minor concessions, lacking scale leverage, struggle to absorb higher capex, and defer orders that would otherwise grow the Saudi Arabia mining equipment market. OEMs counter by inflating stock levels in Dammam bonded warehouses and boosting regional content to reclassify units under the zero-tariff GCC origin rules [2]“Customs Tariff Schedule 2025,”, General Authority of Customs, gazt.gov.sa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Support Equipment Leads Diversification

Surface Mining Support Equipment accounted for 23.16% of Saudi Arabia's mining equipment market share in 2025, mirroring the dominance of open-pit phosphate and bauxite mines in the Eastern Province and Northern Borders. These deposits consume haul-road graders, dewatering pumps, and LED lighting that together absorb roughly one-fifth of annual equipment spend. Drills & Breakers, forecast at a 6.17% CAGR through 2031, will benefit most as hard-rock licenses climb and gold majors standardize rotary-blasthole fleets capable of deeper, faster penetration. The Saudi Arabian mining equipment market continues to favor open-pit machinery such as Caterpillar 777 trucks and Komatsu PC1250 shovels. Still, demand for DTH hammers and hydropower breakers is rising with the expansion of shield-area projects.

While open-pit mining continues to dominate in terms of value, underground operations are gaining momentum, especially with the Mansourah & Massarah mines reaching significant depths. Sales of processing equipment are on the rise, paralleling the introduction of new circuits for lithium-hydroxide, graphite-anode, and gold-flotation. Metso's award for the Ar Rjum project and FLSmidth's contract for Phosphate 3 highlight a trend: single-site packages are now achieving substantial value. Refineries, aiming for finer feed sizes, are increasingly ordering cone crushers, vertical roller mills, and ultrafine screens, in addition to the traditional SAG mills. Furthermore, continuous, high-throughput sizers are becoming more popular as operators shift their focus from brute-force crushing to energy efficiency.

By Function Type: Processing Gains Momentum

Excavation dominated the Saudi Arabia mining equipment market with a 41.16% share in 2025, thanks to high-capacity shovels such as the CAT 6030 (34 m³ bucket) and Komatsu PC5500 (29 m³). Processing, though smaller in absolute terms, is projected to grow fastest at 6.22% CAGR to 2031 as battery-metal and gold-processing plants proliferate. Ma’aden’s Phosphate 3 and Ar Rjum contracts illustrate that crushers, mills, paste thickeners, and flotation columns can equal or exceed haulage capex on a like-for-like tonnage basis.

Transportation and hauling remain a significant area of expenditure but face challenges from in-pit crushing and conveying (IPCC). Tesmec's collaboration with Ma'aden led to improved ore recovery and a substantial reduction in diesel consumption. This success has led Tesmec to plan for localized assembly in the near future. Fluctuations in diesel prices are encouraging miners to adopt trolley-assist haul trucks. When combined with downhill regenerative charging, ABB's retrofit kits can significantly reduce lifetime costs. However, the Ministry of Energy's mandate for a zero-emission zone is primarily focused on underground operations for the time being, allowing diesel to retain its dominance in large phosphate pits.

By Application: Metals Dominate Strategic Focus

Metals captured 46.53% of Saudi Arabia's mining equipment market share in 2025 and is forecast to expand at a 5.95% CAGR through 2031, propelled by gold and emerging battery-metal feedstocks. Mansourah & Massarah aims for 250 koz/y output, while Ar Rjum’s 8 Mt/y circuit under Bechtel will start filling purchase orders for loaders, drills, and reclaim feeders from 2026 onward. Hancock Prospecting’s five new licenses in the Ad-Duwayhi belt signal fresh capex cycles for mobile crushers and blasthole rigs.

Industrial minerals—chiefly phosphate and bauxite—rank second but are slowing now that Phosphate 3 is the final phase of Wa’ad Al Shamal. Coal remains immaterial, accounting for less than 1% of spend, as the Kingdom imports small thermal volumes for cement kilns. Battery-metal refining, despite relying on imported concentrates, continues to buy fine-grinding mills, air-classification circuits, and ultrafine screens well ahead of any domestic spodumene or graphite mine, locking in equipment demand on the processing side even before upstream ore emerges.

By Power Source: Electric Transition Accelerates

Diesel machines held 75.16% share in 2025, but battery-electric units are projected to expand at 9.31% CAGR, the fastest among power options. Diesel inflation has risen sharply, and with the Ministry of Energy mandating zero emissions for new underground mines in the near future, fleet strategies are undergoing a major transformation. Epiroc's battery-ready Scooptram ST14 S and ST1030 loaders are already achieving substantial savings in shaft ventilation costs. While the Saudi Industrial Development Fund offers a green-equipment window at a favorable interest rate, effectively reducing payback periods, challenges remain. The high battery replacement costs and delays in grid connections are tempering the pace of roll-out.

Hybrid-electric drives, positioned in a transitional phase, provide notable fuel savings through regenerative braking. However, they have a higher capital cost than traditional diesel. ABB's trolley-assist kits have enabled the complete elimination of diesel use on downhill grades, resulting in significant fuel savings across specific phosphate haul profiles. Despite these advancements, the Saudi Arabian mining equipment market anticipates that diesel will continue to dominate large open-pit sites for the foreseeable future, thanks to fuel subsidies keeping pump prices low.

Geography Analysis

In Saudi Arabia's mining equipment landscape, the Eastern Province stands out, particularly for Ma’aden’s Al Jalamid and Al Khabra phosphate pits, which together annually extract significant amounts of ore. These sites utilize high-tonnage trucks, large-capacity shovels, and comprehensive dewatering systems. Recently, Volvo’s rigid dump trucks replaced older models, enhancing payload consistency[3]"Saudi Arabia’s surface contract miners", International Mining, im-mining.com. Given the region's minimal annual rainfall, water scarcity is a pressing issue. This has led to the adoption of zero-liquid-discharge plants and reverse-osmosis systems, which have substantially reduced water consumption.

Tabuk and the Northern Borders are emerging as new hubs, attracting the attention of EPCM majors due to their hard-rock licenses. The Ar Rjum, Mansourah & Massarah sites require underground loaders, battery-compatible drills, and retrofit crushing trains with significant annual capacity. Metso secured a major deal for cone crushers, screens, and paste thickeners, while Sandvik drills made their entry through Jac Rijk Al-Rushaid’s mining contract. However, exploration firms are grappling with a shortage of drill crews, leading to prolonged core campaigns and sustained high day rates for rigs.

Yanbu Industrial City and Ras Al Khair are the primary locations for battery-metal and downstream chemical facilities. The trio of EV Metals Group, Northern Graphite, and Capchem has collectively announced substantial capital expenditures. Each has placed orders for fine-grinding, classification, and purification lines, anticipating a domestic resource supply. Projects are facing grid bottlenecks, prompting a shift towards captive solar or gas turbines. This pivot has escalated equipment budgets, particularly for gensets, switchgear, and heat-recovery boilers. With expectations of grid upgrades and renewables achieving a significant share of generation in the near future, energy-intensive refineries are eyeing substantial reductions in scope-3 carbon emissions.

Competitive Landscape

In Saudi Arabia's mining equipment market, Caterpillar, Komatsu, Sandvik, and Metso Corporation, through their long-established dealers and service networks, command a significant share, indicating a moderate concentration. Zahid Tractor, celebrating its long-standing partnership with Caterpillar, boasts impressive same-day parts availability exceeding a high percentage. Meanwhile, the Abdul Latif Jameel Summit adopts a similar approach for Komatsu. Although XCMG and SANY offer Western list prices at a notable discount, local-content scoring and bid uplifts for bids with a substantial Saudi value present challenges to their market penetration. Weir Group recently formed a joint venture with Olayan Saudi Holding, establishing a domestic base for WARMAN pumps and Cavex hydrocyclones, coinciding with the ramp-up of a major phosphate project.

Today's technological advancements prioritize total cost of ownership over sticker price alone. For instance, ABB's e-haul retrofits promise significant savings over the equipment's lifetime, while Epiroc's battery loader conversions achieve a substantial reduction in cost per ton-kilometer. Tesmec's in-pit trencher, which boosts ore recovery by a notable percentage, is undergoing localization to significantly shorten its import lead time. Both Caterpillar and Komatsu are piloting autonomous haulage systems, projecting a potential reduction in labor needs. This is particularly significant given the current operator-to-vacancy ratio in Jubail and Yanbu. However, regulatory approval for these driverless fleets remains pending, with full operational capability not anticipated for several years.

Emerging opportunities lie in offering equipment-as-a-service tailored for cash-light explorers, implementing IPCC in diesel-heavy pits, and developing specialized ultrafine circuits for lithium and graphite refineries. Additionally, funding boosts, such as the SIDF's green-equipment initiative, provide momentum. Yet, smaller miners, especially those not affiliated with Ma’aden, grapple with diminishing margins due to tariffs on imported chassis and drivelines.

Saudi Arabia Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Metso Corporation

-

Sandvik AB

-

Liebherr Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ma’aden signed a four-year exploration contract with Fleet Space Technologies and Tahreez JV worth over USD 50 million to survey 12,012.6 km² of the Arabian Shield using ExoSphere imaging.

- April 2025: Ma’aden announced plans to secure a foreign partner for rare-earth processing operations, underscoring the Kingdom’s ambition to create a regional critical-minerals hub.

- January 2025: Aramco and Ma’aden unveiled a joint venture to commence lithium production by 2027 after successful pilot extraction from produced water streams.

Saudi Arabia Mining Equipment Market Report Scope

The Saudi Arabia mining equipment market report is segmented by product type (underground mining machinery, open-pit mining machinery, surface mining support equipment, drills & breakers, crushing, grinding, screening & filtering, and mineral processing machinery), function type (excavation, transportation & hauling, and processing), application (coal, industrial minerals, and metals), and power source (diesel, hybrid-electric, and battery-electric). The market forecasts are provided in terms of value (USD) and volume (units).

| Underground Mining Machinery |

| Open-Pit Mining Machinery |

| Surface Mining Support Equipment |

| Drills & Breakers |

| Crushing, Grinding, Screening & Filtering |

| Mineral Processing Machinery |

| Excavation |

| Transportation & Hauling |

| Processing |

| Coal |

| Industrial Minerals |

| Metals |

| Diesel |

| Hybrid-Electric |

| Battery-Electric |

| By Product Type | Underground Mining Machinery |

| Open-Pit Mining Machinery | |

| Surface Mining Support Equipment | |

| Drills & Breakers | |

| Crushing, Grinding, Screening & Filtering | |

| Mineral Processing Machinery | |

| By Function Type | Excavation |

| Transportation & Hauling | |

| Processing | |

| By Application | Coal |

| Industrial Minerals | |

| Metals | |

| By Power Source | Diesel |

| Hybrid-Electric | |

| Battery-Electric |

Key Questions Answered in the Report

How fast is equipment spending on Saudi battery-metal refineries growing?

Processing machinery tied to lithium and graphite plants is advancing at a 6.22% CAGR between 2026-2031, faster than any other function.

Which segment is the largest contributor to equipment revenue?

Excavation commanded 41.16% of total spend in 2025, underpinned by large phosphate and bauxite shovels and trucks.

How significant is battery-electric equipment adoption in Saudi mines?

Battery-electric machines are expected to log a 9.31% CAGR through 2031 as miners tap diesel-to-electric incentives and renewable charging corridors.

Which application area commands the largest share of equipment demand?

Metals mining leads with 46.53% share and remains the fastest-growing segment through 2031.

What are the main restraints on growth in Saudi Arabia’s mining equipment space?

Elevated import tariffs on non-GCC machinery and a shortage of skilled heavy-equipment operators currently temper complete market expansion.

Page last updated on: