Kuwait Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

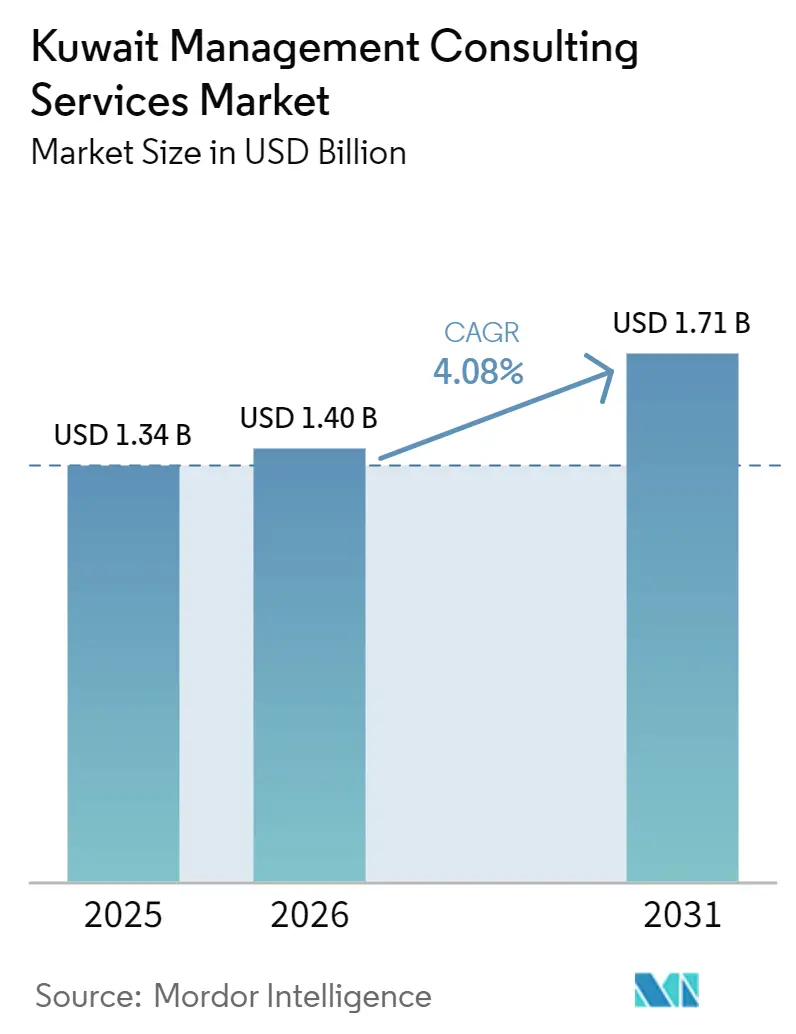

| Base Year Market Size (2025) | USD 1.34 Billion |

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

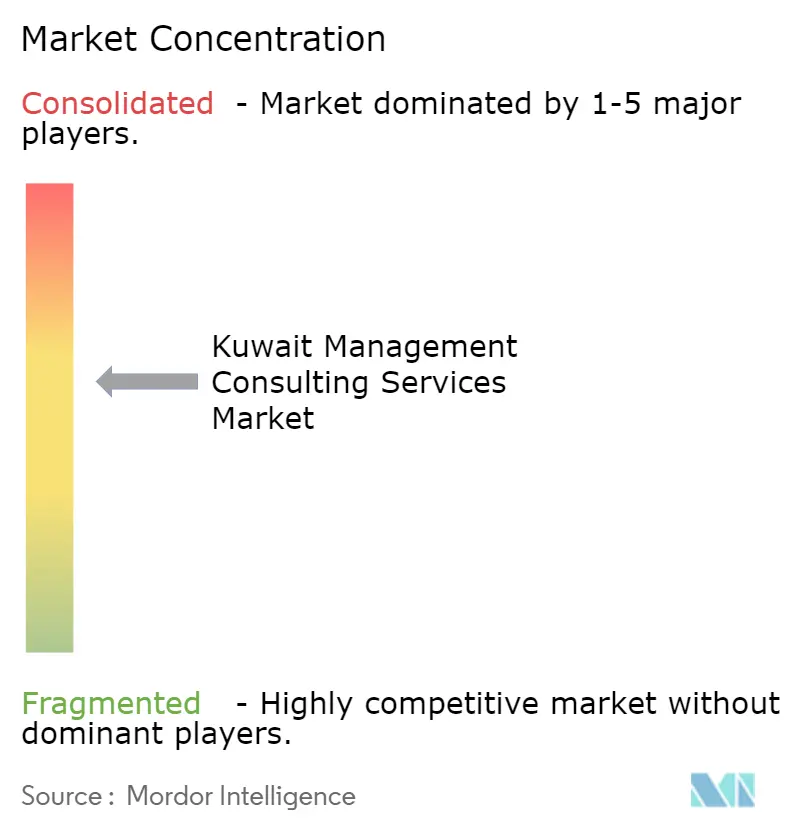

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Management Consulting Services Market Analysis by Mordor Intelligence

The Kuwait management consulting services market size is projected to expand from USD 1.34 billion in 2025 and USD 1.40 billion in 2026 to USD 1.71 billion by 2031, registering a 4.08% CAGR between 2026 to 2031. Demand is rotating from long-range strategy toward tax, risk, and restructuring work as the 15% corporate income tax compels clients to hard-wire governance infrastructure. Public-private partnership mandates under Vision 2035, especially Shagaya solar and Silk City, are enlarging opportunity pools for international firms with project-finance depth, while local boutiques win Arabic-language stakeholder work. Hybrid delivery is normalizing as firms trim expatriate visa costs, but on-site presence still anchors government engagements during Ramadan and summer. Competitive pressure is rising as global technology integrators bundle software subscriptions with advisory, compressing margins for traditional time-and-materials projects.

Key Report Takeaways

- By consulting service line, strategy consulting led with a 31.42% Kuwait management consulting services market share in 2025, yet risk and compliance consulting is forecast to grow fastest at a 4.86% CAGR through 2031.

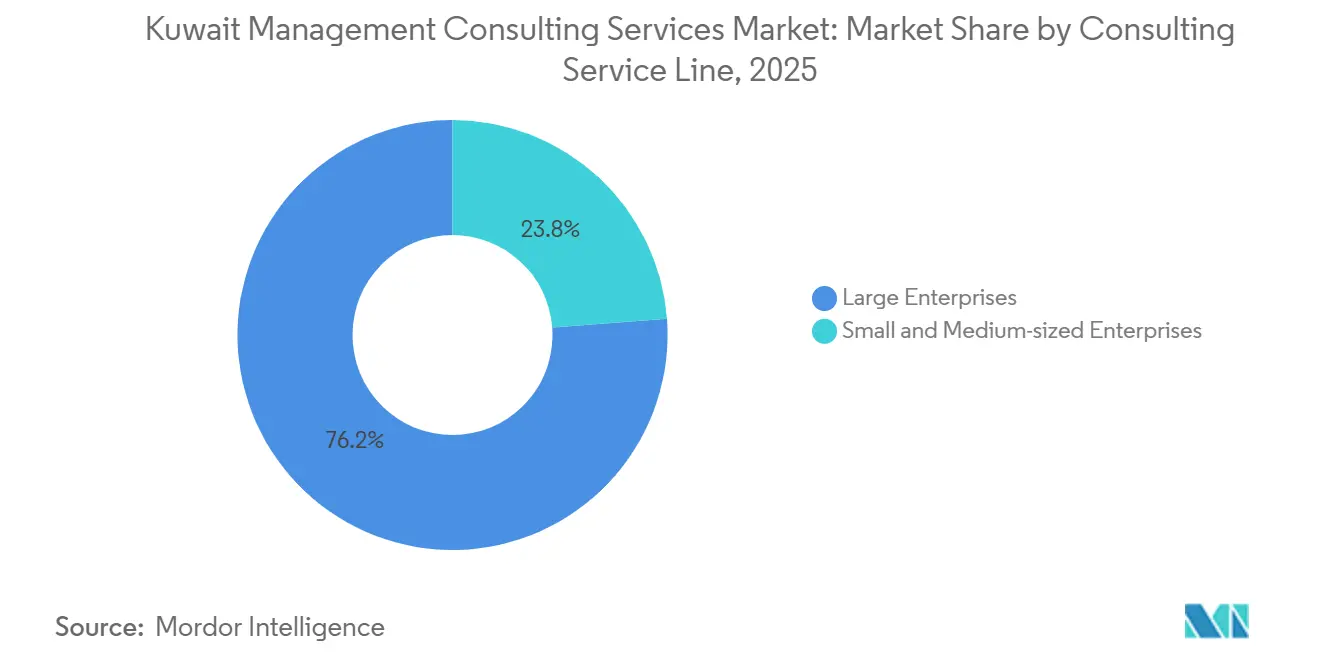

- By organization size, large enterprises dominated with 65.73% of Kuwait management consulting services market size in 2025, while the SME segment is advancing at a 4.21% CAGR on the back of National Fund digitization grants.

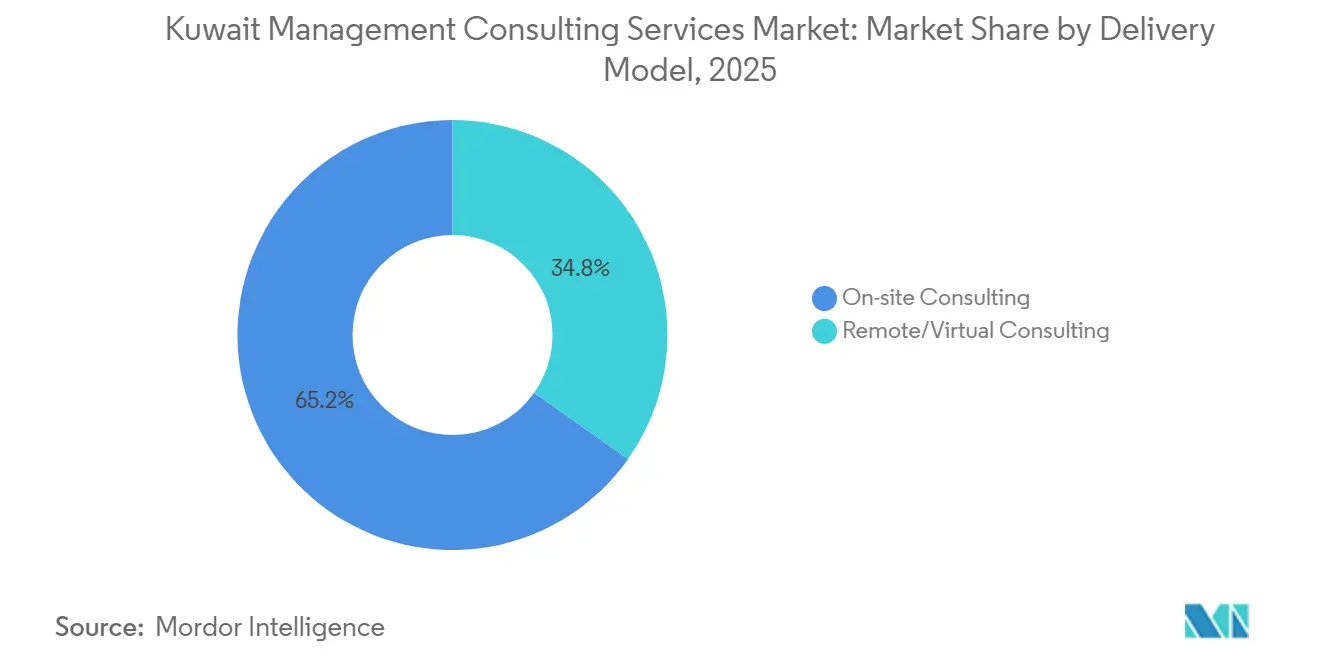

- By delivery model, on-site consulting held 58.11% share in 2025, but remote and virtual workstreams are expanding at a 4.37% CAGR as hybrid staffing reduces travel overhead.

- By end-user industry, banking and insurance is pacing the field with a projected 4.63% CAGR during 2026-2031, overtaking the public sector’s 23.07% spending share logged in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kuwait Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Government Programs Drive Consulting Spend | +1.2% | National, early gains in Kuwait City, Hawalli, Salmiya | Medium term (2-4 years) |

| Mandatory 15% Corporate Income Tax Spurs Tax and Restructuring Advisory Demand | +1.0% | National, concentrated in Kuwait City financial district | Short term (≤ 2 years) |

| Vision 2035 PPP Pipeline Accelerates Large Strategy and Implementation Engagements | +0.9% | National, Jahra Governorate (Shagaya), Silk City corridor | Long term (≥ 4 years) |

| Accelerating Cloud Migration Across BFSI and Energy Sectors Boosts Technology Consulting | +0.7% | National, BFSI hub in Kuwait City, energy in Ahmadi | Medium term (2-4 years) |

| Under-Served SME Digitization Grants Niche Opportunities for Local Boutiques | +0.3% | National, Farwaniya, Jahra SME clusters | Medium term (2-4 years) |

| Emergence of AI-Native Arabic-Language Models Triggers Specialized GenAI Consulting Demand | +0.2% | National, early adoption in public sector and sovereign entities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-First Government Programs Drive Consulting Spend

Kuwait has committed to delivering every public service through digital channels by 2035, channeling USD 30 billion into identity, portal, and data-exchange projects. The Ministry of Interior’s unified platform, launched in 2025, collapsed visa, residency, and traffic workflows into a single interface and cut average processing time from 14 days to 48 hours. Ministries now require advisors to fuse Arabic-language legal analysis with cloud-architecture design, a capability set few expatriate-heavy practices offer. Contract clauses mandate 70% Kuwaiti staffing and bilingual deliverables, rewarding firms that already employ national talent.[1]Central Agency for Information Technology, “CAIT Kuwait Digital Programs,” cait.gov.kw Advisory scope spans API governance, zero-trust security, and legacy mainframe retirement, creating sticky multi-year workstreams that elevate the Kuwait management consulting services market.

Mandatory 15% Corporate Income Tax Spurs Tax and Restructuring Advisory Demand

The 2025 tax law applied a flat 15% rate to foreign entities and high-revenue Kuwaiti corporations, igniting urgent demand for transfer-pricing, entity-rationalization, and withholding-tax advice.[2]“Kuwait Corporate Income Tax Guide 2025,” Fincirc Insights, fincirc.com Big Four firms scaled Kuwait tax practices by 30-40% inside twelve months, importing specialists from Dubai and Riyadh to file Q1 2026 returns. Multinationals reopened holding-company maps, evaluating shifts to Bahrain or UAE free zones, while family conglomerates hired advisors to reshape partnerships into limited-liability vehicles without diluting founder control. Continuous ministerial circulars on deductibility and exemptions locked many clients into annual retainer models, propelling compliance revenue beyond initial forecasts.

Vision 2035 PPP Pipeline Accelerates Large Strategy and Implementation Engagements

The Kuwait Authority for Partnership Projects is steering more than USD 150 billion of transport, utilities, and urban assets to market. Shagaya’s 1.6 gigawatt solar tranches alone require consortia to model 30-year offtake economics, environmental baselines, and Ministry interconnects, tilting awards toward international advisors with Abu Dhabi and Riyadh renewables pedigrees.[3]Edward James, “Kuwait Issues Shagaya Solar RFP,” MEED, guest.meed.com Silk City’s USD 132 billion blueprint still sits at the feasibility desk, yet legal-zoning and free-zone governance work is already underwriting strategy backlogs. Energy-transition horizons stretch beyond fossil efficiency into hydrogen export and carbon capture, sustaining long-dated advisory pipelines that anchor Kuwait management consulting services market growth.

Accelerating Cloud Migration Across BFSI and Energy Sectors Boosts Technology Consulting

Core-banking overhauls at National Bank of Kuwait, Gulf Bank, Boubyan Bank, and Ahli Bank of Kuwait have moved treasury, trade, and retail ledgers onto cloud cores that slash processing times from days to hours. Follow-on work spans API integration, data-governance frameworks, and phishing-resilient identity layers mandated by the Central Bank of Kuwait. In energy, Kuwait National Petroleum Company’s predictive-maintenance program and Kuwait Oil Company’s AI Innovation Center are pulling analytics and machine-learning specialists into brownfield petro-assets. Vendors such as ServiceNow and Oracle now co-sell licenses with embedded change-management sprints, intensifying competition for implementation share but enlarging total contract value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Shortages in Cyber-Security and Data Science Inflate Delivery Costs | -0.8% | National, acute in Kuwait City IT sector | Short term (≤ 2 years) |

| Oil-Price Volatility Delays Discretionary Public-Sector Budgets | -0.6% | National, concentrated in public-sector ministries and parastatals | Medium term (2-4 years) |

| Family-Owned Conglomerates' Cultural Resistance Limits Project Scope | -0.3% | National, prominent in retail, real estate, logistics family groups | Long term (≥ 4 years) |

| Fragmented SME Base Raises Client-Acquisition Costs for Mid-Tier Firms | -0.2% | National, Farwaniya, Jahra, SME-dense governorates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Shortages in Cyber-Security and Data Science Inflate Delivery Costs

Kuwait ranked 78th on the 2024 National Cyber Security Index, exposing gaps that consulting firms must close with expatriate hires or premium-priced nationals.[4]National Cyber Security Index, “Kuwait,” ncsi.ega.ee Public-sector salary bumps of up to 40% for IT staff in 2025 pulled scarce talent out of private consulting benches, forcing firms to renegotiate fixed-price contracts into time-and-materials terms. Senior cyber professionals decamped to Saudi Arabia and UAE for tax-free packages, driving 25-30% attrition at Big Four cyber units. Average data-science vacancies now sit unfilled for 6-8 months, delaying AI rollouts for banking and energy clients that require Arabic-language NLP and on-shore data residency. Stop-gap academies and cross-border rotations offer partial relief but cannot fully offset wage inflation.

Oil-Price Volatility Delays Discretionary Public-Sector Budgets

Brent crude averaged USD 75 per barrel in 2025, below Kuwait’s USD 85 fiscal breakeven, widening the deficit to 8.2% of GDP and triggering a USD 2 billion cut in capital outlays.[5]“Kuwait Budget Deficit 2025,” Kuwait Times, kuwaittimes.com Ministries shifted from multi-year transformation programs to short diagnostic studies funded from operating budgets, slicing average project value by up to 40%. The long-planned oil-sector restructuring tender remains frozen until parliamentary appropriation clears, illustrating the political drag on even nationally strategic mandates. Firms are diversifying into private banking, telecom, and family offices to cushion revenue swings, but practice reskilling entails 12-18 month investment lags.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Momentum Overtakes Classical Strategy

Risk and compliance consulting is forecast to post the fastest 4.86% CAGR during 2026-2031, a trajectory that edges the segment toward a larger slice of Kuwait management consulting services market size than historical patterns suggested. The new tax code, heightened anti-money-laundering rules, and emergent AI-audit directives keep pipelines full even as oil prices gyrate. Big Four teams added headcount and enterprise text-analytics tools to monitor rolling ministerial circulars, converting one-off tax filings into recurring retainers that shield fee revenue from project lumpiness.

Traditional strategy consulting retained a 31.42% Kuwait management consulting services market share in 2025, yet engagement tenure compressed as clients demanded six-month feasibility sprints rather than nine-month transformations. Digital transformation workstreams won incremental share from core-banking and energy analytics upgrades that bundle cloud migration with workflow automation. Operations, HR, and financial-advisory practices remained steady, largely tethered to oil-sector efficiency and Kuwaitization compliance. Multi-disciplinary teams marrying compliance and tech now capture larger wallet share, demonstrating a durable pivot in service-line mix.

By Organization Size: SME Digital Grants Lift Local Boutiques

Large enterprises commanded 65.73% of Kuwait management consulting services market size in 2025, anchored by government, banking, and energy majors that award multi-year mandates. Yet the SME segment is advancing at a 4.21% CAGR as National Fund subsidies tie customs clearances and grant disbursements to demonstrable digitization milestones. Local boutiques price modular packages in Kuwaiti dinars, allowing cash-constrained owners to match spend with milestone receipts.

Family-owned conglomerates remain reluctant to commission board-level succession or governance work, confining many large-enterprise engagements to tactical IT upgrades. By contrast, SMEs in Farwaniya and Jahra embrace off-the-shelf ERP and e-commerce builds that deliver quick ROI, widening the client footprint for Arabic-speaking consultants. Regulatory rumblings around a new family-trust law could unlock deferred governance projects, but until enacted, boutique traction will stay rooted in compliance-linked digitization.

By Delivery Model: Hybrid Staffing Redefines Cost Curves

On-site engagements retained 58.11% share of Kuwait management consulting services market size in 2025, but remote and virtual workstreams are projected to grow at a 4.37% CAGR through 2031 as firms formalize hybrid models that keep strategic touchpoints in country while shifting data engineering and documentation to offshore centers. Visa quotas and rising apartment rents in Kuwait City amplify the savings, letting partners re-price long projects as milestone-based packages that bundle two to three on-site sprints per quarter. High-security government and family-business clients still demand Arabic-language advisors physically present during Ramadan and budget-defense meetings, anchoring a floor under travel volumes even as the broader delivery mix tilts digital.

Hybrid models also help firms comply with Kuwaitization rules that require 70% national staffing on public contracts, because remote technical experts do not count toward local headcount caps. Workflow-automation platforms such as ServiceNow and UnifyApps enable consultants in Dubai or Riyadh to configure sandbox environments, then hand configuration scripts to Kuwait-based teams for final deployment. As success stories multiply, clients accept that diagnostic, design, and user-training phases can happen over secured video links, reserving on-site presence for go-live and stakeholder workshops. The pattern is now spilling into energy, banking, and healthcare, cementing hybrid execution as the structural growth engine of the Kuwait management consulting services market.

By End User Industry: Financial Services Sets the Pace

Banking and insurance logged the strongest 4.63% CAGR outlook for 2026-2031, propelled by open-banking directives and Central Bank resiliency tests that compel core-system overhauls, API orchestration, and cyber hardening. National Bank of Kuwait’s cloud-native treasury platform, Gulf Bank’s digital-lending suite, and Boubyan Bank’s Temenos deployment each generated multi-year follow-on mandates in data governance, customer-journey redesign, and fraud analytics, pushing the segment toward a greater slice of Kuwait management consulting services market share by the decade’s end. Consultants with Arabic-language compliance and IFRS-17 actuarial skills command fee premiums as insurers modernize reporting stacks ahead of 2027 filing deadlines.

The public sector still accounts for 23.07% of 2025 spend but has slowed new awards amid oil-price volatility, shifting advisors into tactical feasibility and performance-diagnostic work with shorter payment cycles. Energy projects, especially in Ahmadi, channel digital-twin, predictive-maintenance, and hydrogen-economics assignments to technology-heavy practices. Telecommunications, healthcare, and manufacturing add episodic bursts tied to 5G densification, electronic-medical-records rollouts, and Industry 4.0 pilots. Retail, real estate, and logistics remain largely tied to family-business cash cycles, commissioning ecommerce or warehouse-management builds when liquidity and generational leadership transitions align. Viewed in aggregate, the sector diversity cushions cyclical risks yet underscores why specialized capability benches, not generic strategy blueprints, are the future revenue engine for Kuwait management consulting services market size.

Geography Analysis

Kuwait City anchors roughly two-thirds of national consulting outlays, driven by ministries, sovereign entities, and the headquarters of top financial institutions. The financial district’s tower cluster funnels strategy, tax, and digital-core migrations into year-round pipelines, while adjacent Sharq and Mirqab neighborhoods host boutique advisory firms that serve Arabic-language compliance and governance needs. Foreign practices base expatriate partners here to secure quick access to Central Bank workshops and Parliament briefings, a proximity that sustains premium bill rates even as hybrid staffing trims weekly in-country headcounts.

Hawalli and Salmiya, home to dense clusters of retail and hospitality SMEs, are the fastest-growing satellite nodes, buoyed by National Fund digitization grants that subsidize cloud point-of-sale, inventory, and HR modules. Local boutiques opened storefront offices near the Fourth Ring Road to deliver Arabic-only training and after-sales support within same-day driving distance, capturing contracts the Big Four often decline as uneconomic. Farwaniya’s logistics parks and Jahra’s Shagaya Renewable Energy Park extend the map westward, spawning supply-chain optimization, environmental-impact, and project-finance workstreams that will mature as Shagaya’s 1.6 gigawatt build-out moves from EPC to operations between 2027 and 2030.

Ahmadi remains the fulcrum for energy-sector advisory, with Boston Consulting Group and KBR embedding cross-functional teams inside Kuwait National Petroleum Company and Kuwait Oil Company sites. Looking north, the USD 132 billion Silk City megaproject could redraw the geographic revenue mix if master-planning advances to procurement after 2027, potentially shifting board-level engagements and free-zone governance work to Subiya in Jahra Governorate. Until then, Kuwait City retains primacy, but the centrifugal pull of renewable energy, SME digitization, and transport corridors ensures a progressively multi-node demand landscape that diversifies Kuwait management consulting services market size exposure across the nation.

Competitive Landscape

The market sits in a moderately concentrated band where the Big Four, McKinsey, Bain, Boston Consulting Group, and Strategy and collectively hold an estimated 55-60% revenue share, leaving the balance to mid-tier networks and local boutiques. International firms defend position by productizing AI accelerators and cloud-migration toolkits that cut diagnostic cycles from weeks to days, a defensive play against vendor-led advisory bundles coming from ServiceNow, Oracle, and Microsoft.

Boutiques strike back with Arabic-first delivery, fixed-price modular offerings, and proximity to Farwaniya and Jahra clients. Symloop’s KWD 12 000 (USD 39 000) six-month Digital Professional tier and Alientics’ 90% paperwork-reduction case study exemplify the value narrative that resonates with cash-sensitive SMEs. Mid-tier internationals such as Grant Thornton and Protiviti exploit capacity gaps and independence conflicts at the Big Four to win bank-regulatory and internal-audit mandates, solidifying a three-tier ecosystem rather than a simple big-versus-small dichotomy.

Talent shortages are the battlefield equalizer. Firms that can rotate cyber and data-science experts through the Gulf without breaching Kuwaitization caps secure a hiring moat. Bain’s partnership with G42’s Inception gives it access to an Abu Dhabi AI lab, while PwC’s pact with UnifyApps embeds low-code workflow diagnostics into standard proposals. As clients embrace outcome-based contracts, the blend of domain accelerators, hybrid resourcing, and bilingual compliance determines wallet share, making adaptability the decisive competitive lever for Kuwait management consulting services market.

Kuwait Management Consulting Services Industry Leaders

PwC Kuwait (PricewaterhouseCoopers International Ltd.)

KPMG Advisory W.L.L.

Deloitte and Touche Al-Wazzan and Co.

Ernst and Young Kuwait Consulting W.L.L.

McKinsey and Company Middle East, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kuwait Authority for Partnership Projects issued the RFP for the 500 MW Al Dibdibah and Al Shagaya Phase III-Zone 2 solar PV IPP, appointing Ernst and Young, DLA Piper, and DNV as advisors.

- March 2026: PwC and Strategy and launched a strategic alliance with UnifyApps to deliver remote process-mining and on-site automation rollouts that compress delivery timelines by up to 25%.

- February 2026: Gulf Bank received Central Bank approval to hire Grant Thornton for digital-banking transformation and merger-scenario analysis.

- January 2026: Boston Consulting Group secured a digital-transformation mandate with Kuwait National Petroleum Company covering predictive maintenance and AI-driven exploration analytics.

Kuwait Management Consulting Services Market Report Scope

The Kuwait Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the projected size of Kuwait’s management consulting services market by 2031?

It is forecast to reach USD 1.71 billion by 2031, expanding at a 4.08% CAGR from 2026.

Which consulting service line is growing fastest in Kuwait?

Risk and compliance consulting leads with a projected 4.86% CAGR for 2026-2031, propelled by the 15% corporate income tax and tighter anti-money-laundering rules.

How are delivery models evolving in the Kuwaiti consulting scene?

Hybrid models combine remote diagnostics with targeted on-site sprints, trimming visa and travel costs while meeting cultural expectations for face-to-face engagement.

Why is banking outpacing the public sector in consulting spend growth?

Core-system cloud migrations, open-banking regulations, and Central Bank resiliency tests are driving multi-year digital-transformation mandates across Kuwaiti banks.

What is the key talent challenge facing consulting firms in Kuwait?

Acute shortages of cybersecurity and data-science professionals inflate wage costs and extend project timelines, especially for AI and analytics engagements.

Which regions beyond Kuwait City show rising consulting demand?

Hawalli, Salmiya, Farwaniya, and Jahra are growing quickly thanks to SME digitization grants, logistics expansions, and renewable-energy projects.

Page last updated on: