Qatar Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

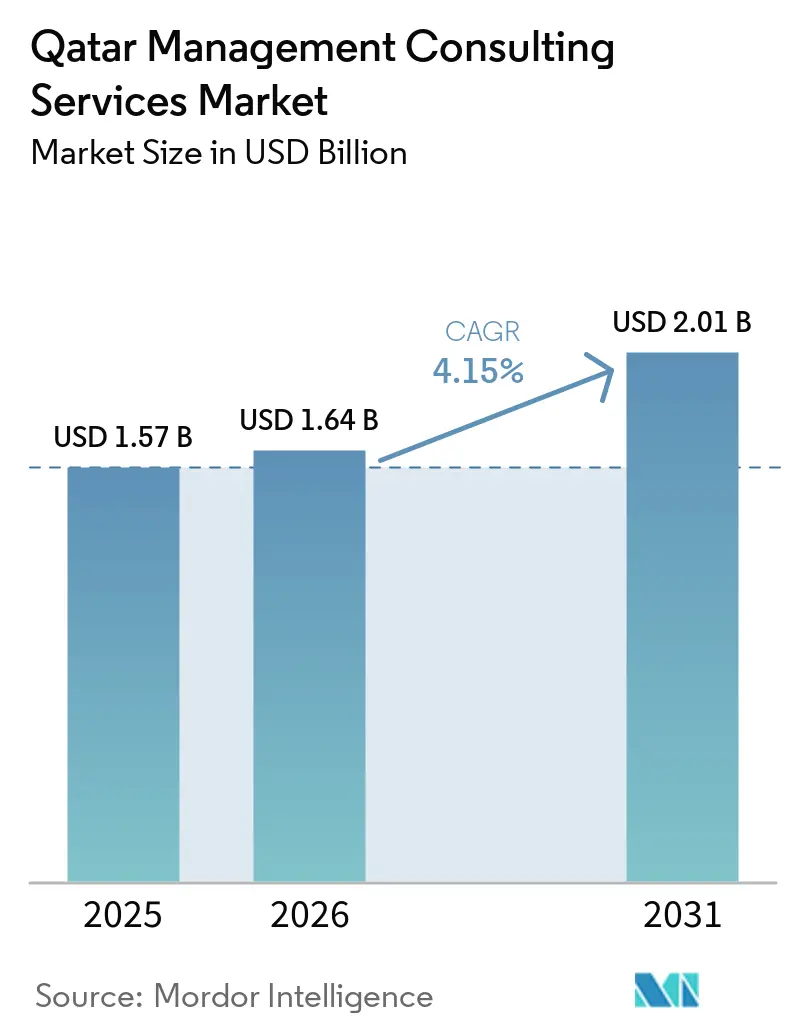

| Base Year Market Size (2025) | USD 1.57 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

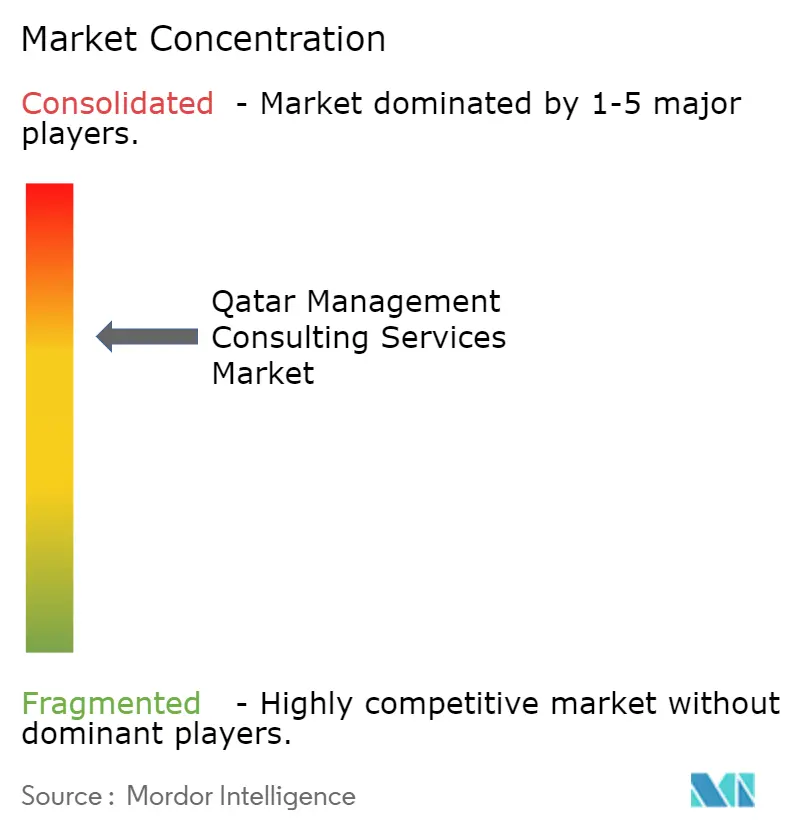

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Management Consulting Services Market Analysis by Mordor Intelligence

The Qatar management consulting services market size was valued at USD 1.57 billion in 2025 and is estimated to grow from USD 1.64 billion in 2026 to reach USD 2.01 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031). Macroeconomic stability, the nation’s pivot from pre-FIFA infrastructure build-out toward knowledge-economy objectives, and a steady pipeline of government digital mandates underpin medium-term growth. Strategy engagements still dominate revenue, yet public bodies and state-owned enterprises now request cloud migration blueprints, data governance frameworks, and artificial intelligence roadmaps more frequently than classic corporate strategy projects. Mandatory environment, social, and governance disclosure rules, together with sovereign-cloud data-residency requirements, further elevate demand for compliance, cyber-risk, and sustainability advisory. Intensifying rivalry among Big Four audit affiliates, global strategy houses, and specialized boutiques is already compressing margins, which in turn accelerates adoption of outcome-based pricing and hybrid delivery models that combine remote execution with selective on-site workshops. Throughout the outlook period, the Qatar management consulting services market is expected to remain resilient even during budget tightening cycles because advisory support has become embedded in government diversification programs and North Field expansion projects.

Key Report Takeaways

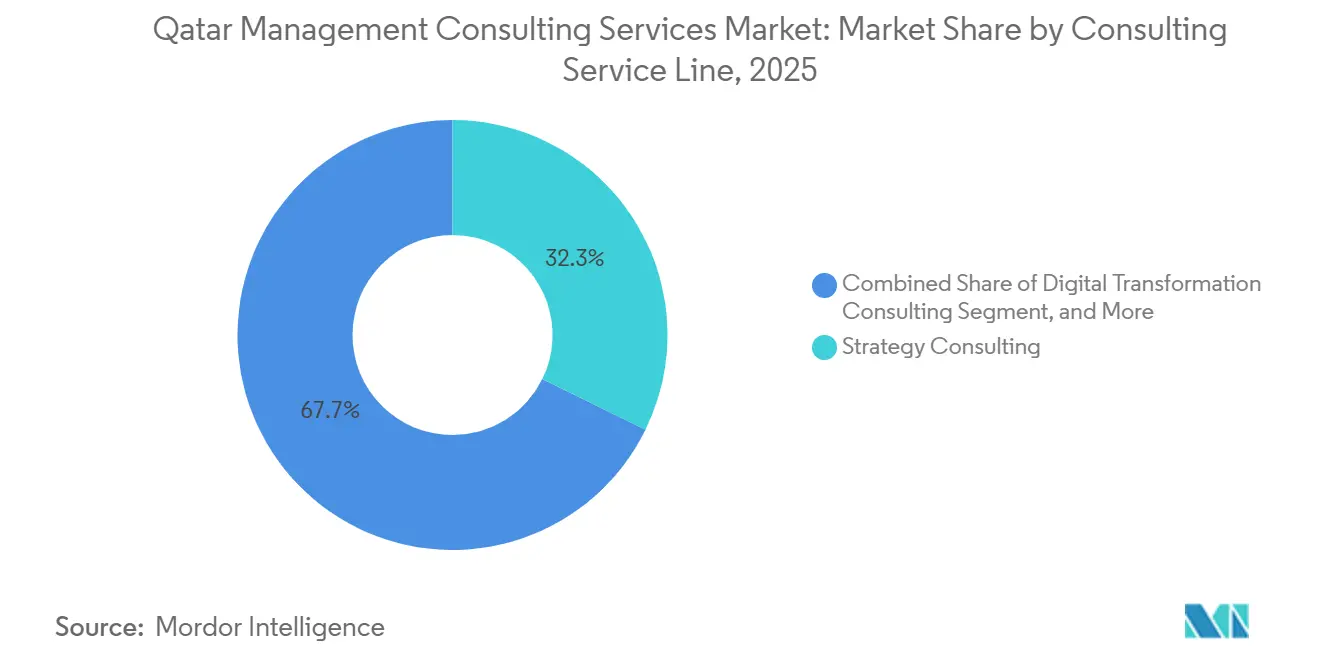

- By consulting service line, Strategy Consulting led with a 32.27% share in 2025 while Digital Transformation Consulting is projected to record the fastest 4.34% CAGR through 2031, reflecting the state’s decision to digitize 90% of public services by 2030.

- By organization size, Large Enterprises accounted for 60.84% of 2025 revenue, yet Small and Medium-Sized Enterprises are on track for a 4.23% CAGR through 2031 as Qatar Development Bank financing accelerates.

- By delivery model, On-Site Consulting held 47.98% of spending in 2025, but Remote and Virtual Consulting shows the highest 4.38% CAGR thanks to sovereign-cloud architecture mandates under Data Privacy Law No. 13/2016.

- By end user industry, the Public Sector contributed 24.48% of 2025 spend, whereas Energy and Resources is expected to expand at a leading 4.26% CAGR through 2031 as North Field expansion boosts liquefied natural gas capacity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Qatar National Vision 2030 Diversification Agenda | +1.2% | National, concentrated in Doha, Al Rayyan, and Qatar Free Zones | Long term (≥4 years) |

| Government-Led Digital-Transformation Mandates | +1.0% | National, early adoption in public sector and state-owned enterprises | Medium term (2-4 years) |

| Post-FIFA Infrastructure and Events Advisory Demand | +0.6% | National, spill-over to hospitality, transport, and tourism | Short term (≤2 years) |

| Mandatory ESG Reporting Spurs Sustainability Consulting | +0.5% | National, focus on Qatar Financial Centre and Qatar Exchange-listed entities | Medium term (2-4 years) |

| Privatization Pipeline in Utilities Drives Carve-Out Advisory | +0.4% | National, water, electricity, waste management | Long term (≥4 years) |

| Qatar Free Zones Expansion Fuels Cross-Border Relocation Consulting | +0.3% | Ras Bufontas, Umm Alhoul, Qatar Science and Technology Park | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Qatar National Vision 2030 Diversification Agenda

The Third National Development Strategy launched in 2024 commits to a 36% compound annual growth rate in small and medium-sized enterprise contributions to non-hydrocarbon GDP, thereby creating recurring demand for operations, financial, and digital advisory.[1]Planning and Statistics Authority Qatar, “Third National Development Strategy,” PSA.GOV.QA Commercial banks must channel 7% of credit to the small and medium segment, yet outstanding loans represented only 4% of private-sector lending in 2021, widening the advisory-rich financing gap. The National Funding Gate platform, introduced in 2025, unifies access to venture capital, incubation, and Qatar Development Bank programs, positioning consultancies to design credit-structuring methodologies and risk frameworks.[2]Qatar Development Bank, “Annual Report 2025,” QDB.QA PwC’s May 2025 small and medium forum and Rowwad Advisory’s niche positioning illustrate how the Qatar management consulting services market has already realigned portfolios around diversification goals.

Government-Led Digital-Transformation Mandates

Digital Agenda 2030 targets 90% digitization of government services and has already reached 74% adoption of the Hukoomi platform with 2,300 online servicesA. ISO 20000-1, 27001, and 9001 certifications earned by the Ministry in 2025 require process reengineering and security audits that favor consultancies offering change-management expertise. A Smart Government Steering Committee coordinates 15+ tech agreements and 20+ training programs, producing a steady pipeline for cloud migration, zero-trust, and secure access service edge engagements. The December 2025 agreement among the Ministry, OpenAI, and PwC to build a national AI ecosystem is expected to anchor multi-year advisory contracts in model governance and data ethics.[3]Qatar Ministry of Communications and Information Technology, “Digital Agenda 2030,” MCIT.GOV.QA

Post-FIFA Infrastructure and Events Advisory Demand

Qatar spent USD 220 billion on World Cup infrastructure, and repurposing these assets now drives assignments covering facility optimization and public-private partnership structuring. Boutique firm Legacy Advisory guides stadium conversions, while Parsons continues program-management support for transport corridors. Event-hub ambitions, including Formula 1 and MotoGP contracts, keep feasibility studies and sponsorship advisory in demand. Clifford Chance’s concession advisory showcases legal-financial overlap that cross-disciplinary consultancies monetize.

Mandatory ESG Reporting Spurs Sustainability Consulting

International Financial Reporting Standards Sustainability Disclosure Standards S1 and S2 became mandatory for all Qatar Financial Centre-licensed firms in January 2026, obliging listed entities to disclose climate risks and greenhouse-gas footprints.[4]Qatar Financial Centre Regulatory Authority, “IFRS Sustainability Disclosure Standards,” QFCRA.COM Parallel Qatar Central Bank guidance for banks intensifies need for materiality assessment and carbon accounting frameworks. KPMG’s 2024 assurance workshops and PwC-Strategy&-UnifyApps’ 2025 MOU on AI-driven sustainability demonstrate how the Qatar management consulting services market is embedding tech platforms into ESG offerings North Field West, integrating 1.1 million tpa carbon-capture and solar power, amplifies demand for life-cycle assessments and carbon-credit structuring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil Price Volatility Drives Budget Uncertainty | -0.8% | National, highest impact on public sector and state-owned enterprises | Short term (≤2 years) |

| Qatarization Limits Foreign Consultant Deployment | -0.6% | National, stricter in private sector and Free Zones | Medium term (2-4 years) |

| Competition From GCC Boutiques Compresses Fees | -0.3% | National, spill-over from United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| Data Residency Regulations Restrict Cross-Border Delivery | -0.2% | National, acute in Qatar Financial Centre and cloud services | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Oil Price Volatility Drives Budget Uncertainty

The 2026 fiscal plan forecasts USD 60.5 billion in spending and a QAR 21.8 billion (USD 5.99 billion) deficit, built on a conservative USD 60 per-barrel assumption.[5]Qatar Ministry of Finance, “Budget 2026,” MOF.GOV.QA Ministries postpone discretionary projects when hydrocarbon receipts dip, squeezing fee pools for strategy and operations work. North Field output is expected to lift 2026 revenues by 33%, yet timing gaps force consultancies to adopt outcome-based pricing that reduces near-term revenue certainty. Scenario-planning and cost-optimization requests partially offset spending restraints, but margin pressure persists.

Qatarization Limits Foreign Consultant Deployment

Law No. 12/2024 mandates 50% Qatari staffing in administrative roles and 30% in technical positions, with penalties of up to QAR 100,000 (USD 27,472).[6]Qatar Ministry of Labour, “Qatarization Law No. 12/2024,” MOL.GOV.QA Talent shortages in cyber-security and advanced analytics force firms to accelerate graduate programs and invest in local certification, raising delivery costs. The Knowledge Transfer initiative involving 13 global firms eases skill gaps yet does not fully offset the immediate supply-demand mismatch. Local leadership appointments, such as Roland Berger’s 2025 hire of Nizar Hneini, illustrate how firms adapt governance models to maintain project eligibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Surges Ahead

Digital Transformation Consulting is projected to log the fastest 4.34% CAGR through 2031, reflecting cloud-first directives, artificial-intelligence pilots, and zero-trust security rollouts within government entities. This acceleration narrows the historical gap with Strategy Consulting, which retained a 32.27% Qatar management consulting services market share in 2025 despite slower growth. Strategy still wins large public contracts, yet execution-oriented mandates dominate new tenders as ministries request prototype development, data-platform engineering, and agile training.

The Qatar management consulting services market size tied to operations engagements expands in tandem with North Field megaprojects that require supply-chain modeling and predictive-maintenance systems. HR advisory demand climbs because Qatarization compliance compels firms to redesign talent acquisition, while risk and compliance specialists secure steady work auditing sovereign-cloud deployments under Data Privacy Law No. 13/2016. Boutique real-estate and events advisors retain niche roles, but large frameworks increasingly bundle environmental, social, and governance analytics, pushing smaller players to partner with tech vendors for relevance.

By Organization Size: SMEs Gain Momentum

Large Enterprises commanded 60.84% of 2025 revenue as state-owned conglomerates and Qatar Financial Centre-licensed institutions signed multi-year frameworks. However, the Qatar management consulting services market is witnessing a shift as small and medium-sized enterprises receive bigger Qatar Development Bank cheques, rising to QR 2 billion (USD 549 million) in 2025. The National Funding Gate and SMEs Go Digital initiatives funnel advisory-ready leads to consultancies proficient in lean finance, e-commerce enablement, and low-code automation.

While legacy firms cultivate long-cycle engagements, specialized boutiques such as Rowwad Advisory capture entrepreneurial segments by offering modular toolkits priced for liquidity-constrained founders. Small and medium-sized enterprise credit is forecast to widen to QR 50.8 billion (USD 13.95 billion) by 2028, suggesting healthy future pipelines for regulatory-compliance, risk, and turnaround advisory. The Qatar management consulting services industry consequently diversifies revenue streams beyond state entities.

By Delivery Model: Remote Engagement Accelerates

On-Site delivery retained 47.98% of 2025 spend because cultural norms still favor in-person workshops. Yet the sovereign-cloud push, reinforced by Data Privacy Law No. 13/2016, made secure remote consulting the fastest-growing format at a 4.38% CAGR. Microsoft Azure Qatar and Google Cloud Doha regions now host low-latency environments, enabling design-thinking sprints, virtual boardrooms, and managed analytics without breaching residency rules.

Hybrid models dominate long-duration transformations, mixing kickoff charrettes in Doha with sprint reviews over video. This structure slashes travel overhead while sustaining relationship intimacy. The Qatar management consulting services market size for remote services is likely to keep expanding as 99% internet penetration and near-universal contactless-payment adoption normalize digital collaboration.

By End User Industry: Energy Ups the Pace

Public-sector bodies absorbed 24.48% of advisory budgets in 2025 as ministries advanced Digital Agenda 2030 deliverables. North Field build-out pushes Energy and Resources toward a 4.26% CAGR, making it the standout vertical. Engineering, procurement, and construction contractors require project-management offices, carbon accounting, and supply-chain de-risking services to hit simultaneous expansion and decarbonization targets.

Qatar Central Bank’s FinTech Strategy propels banking and insurance consulting in open banking, cyber-security, and regulatory technology. Meanwhile, telecommunications operators pursue 5G monetization, leading to demand for edge-computing business cases and artificial-intelligence-enabled customer experience mapping. Real estate and retail remain smaller slices of the Qatar management consulting services market, but stable occupancy levels and mall repositionings keep boutiques such as ValuStrat engaged.

Geography Analysis

Consulting demand clusters in Doha’s Central Business District, Al Rayyan’s education corridor, and Qatar Free Zones that offer 100% foreign ownership and tax holidays. Over 1,000 entities registered with the Qatar Financial Centre by 2025, each requiring business-setup, regulatory, and governance guidance. The Free Zones Authority expanded Ras Bufontas and Umm Alhoul in 2025 to attract logistics and tech manufacturing, generating relocation and carve-out advisory opportunities

North Field’s 126 million tpa LNG capacity target positions Qatar as the foremost global exporter, drawing western EPC contractors that seek local project-management support, environmental permitting, and joint-venture structuring. Capital Economics estimates a 13% GDP surge in 2026 once first gas flows, unlocking fiscal space for fresh transformation programs. Legacy World Cup assets continue generating facility-optimization and event-planning mandates as Doha bids for the Asian Games and secures annual Formula 1 races.

Regional rivalry from larger United Arab Emirates and Saudi markets encourages aggressive discounting, yet Qatar’s sovereign-cloud and Qatarization rules create protective moats. The Knowledge Transfer scheme requiring foreign firms to co-train nationals ensures that intellectual property stays inside the country, fostering a locally grounded Qatar management consulting services market capable of exporting know-how across the Gulf.

Competitive Landscape

The Qatar management consulting services market exhibits moderate concentration. Big Four arms, PwC, Deloitte, EY, and KPMG,hold the majority of framework agreements, especially in audit-adjacent risk and finance domains. Strategy pure-plays McKinsey, Boston Consulting Group, and Bain have countered by enlarging Doha offices and pitching integrated digital transformation blueprints. Boston Consulting Group exceeded 70 professionals in 2025 and targets 100 by late 2026, while Roland Berger appointed a Qatar lead and added a partner in 2026, signaling a multi-player arms race.

Eight firms, including Deloitte and PwC, secured Qatar Financial Centre cyber-security accreditation, gaining a regulatory moat in risk advisory. Technology alliances differentiate competitors: PwC-Strategy& teamed with UnifyApps for AI-driven ESG automation in 2025, and Accenture partnered with Qatar Airways on the AI Skyways project in 2025. Boutique outfits, ValuStrat in real estate, Mezzan in family-business governance, retain pockets of expertise but face fee compression as larger rivals deploy proprietary analytics and automation at scale.

Emerging disruptors include Ibtechar, specializing in innovation-lab orchestration, and Hacking HR, which launched a Doha chapter in 2026 to tackle talent-development and Qatarization compliance. Alvarez and Marsal’s 2026 office opening introduces turnaround and restructuring specialism, adding to competitive churn. Heightened rivalry stimulates consolidation discussions among mid-tier players seeking scale advantages across the Qatar management consulting services industry.

Qatar Management Consulting Services Industry Leaders

PwC Middle East

Deloitte Middle East

EY Qatar

KPMG Qatar

McKinsey & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: PwC Middle East partnered with the TASMU Accelerator, committing QR 200,000 (USD 54,945) in prize funds and bespoke digital-transformation advisory for local startups.

- February 2026: Boston Consulting Group reported a 10-percentage-point jump in organizations at the “emerging” stage of AI adoption in Qatar

- February 2026: KPMG Qatar unveiled its Learning Academy to support tax, audit, and advisory upskilling aligned with Qatarization mandates.

- February 2026: Alvarez and Marsal inaugurated its fifth Middle East office in Doha to deliver restructuring and performance-improvement services, followed by a memorandum with delivery app Snoonu to mentor startups.

Qatar Management Consulting Services Market Report Scope

The Qatar Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the size of the Qatar management consulting services market in 2026 and 2031?

The market is estimated at USD 1.64 billion in 2026 and is forecast to reach USD 2.01 billion by 2031.

Which consulting service line is growing fastest in Qatar?

Digital Transformation Consulting is projected to register the strongest 4.34% CAGR between 2026-2031.

How does Qatarization impact consulting firms?

Law No. 12/2024 compels firms to fill at least 50% of administrative and 30% of technical roles with nationals, increasing training costs and local hiring.

Why is energy a high-growth vertical for consultants in Qatar?

North Field expansion projects raise liquefied natural gas capacity to 126 million tpa by 2027, generating extensive project-management and sustainability advisory demand.

What drives remote consulting adoption in Qatar?

Sovereign-cloud data-residency rules under Law No. 13/2016 and nearly universal internet access enable secure virtual engagements with lower travel costs.

Which factors make SMEs an attractive segment for consultants?

Qatar Development Bank financing, National Funding Gate access, and the Third National Development Strategys 36% small and medium-enterprise growth target fuel advisory needs in finance, compliance, and digital adoption.

Page last updated on: