Middle East Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

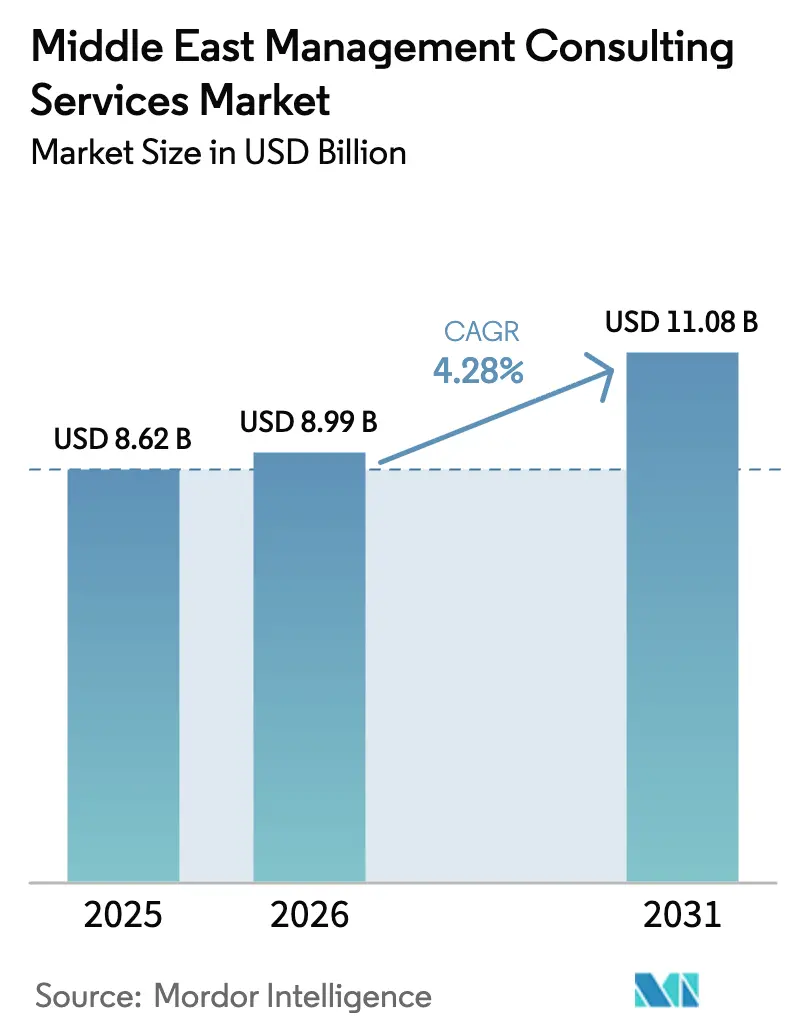

| Base Year Market Size (2025) | USD 8.62 Billion |

| Market Size (2026) | USD 8.99 Billion |

| Market Size (2031) | USD 11.08 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

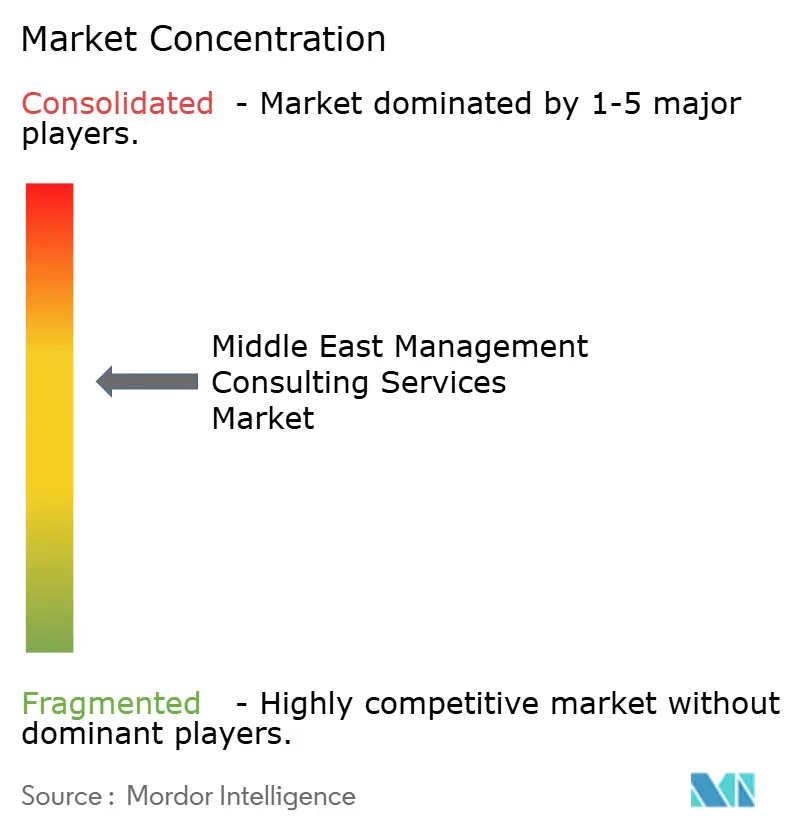

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Management Consulting Services Market Analysis by Mordor Intelligence

The Middle East management consulting services market size in 2026 is estimated at USD 8.99 billion, growing from 2025 value of USD 8.62 billion with 2031 projections showing USD 11.08 billion, growing at 4.28% CAGR over 2026-2031. Demand moves in step with large‐scale diversification programs, mega‐projects, and public-sector digitization that depend on external expertise for design, execution, and performance monitoring. Saudi Arabia and the UAE, through Vision 2030 and Vision 2031, account for most spending, yet consulting needs are broadening across Qatar, Kuwait, and Oman as those economies invest in smart infrastructure and decarbonization. Cloud-first mandates, rising cyber-risk, and a surge of sustainability regulations keep operational and technology consulting bookings robust, while a talent shortage and growing in-house strategy teams put selective pressure on prices and margins. Competition centers on the Big Four and the MBB firms, but mid-tier specialists are winning assignments in ESG, family business governance, and SME digital enablement.[1]U.S. Department of Commerce, “Saudi Arabia – Digital Economy,” trade.gov

Key Report Takeaways

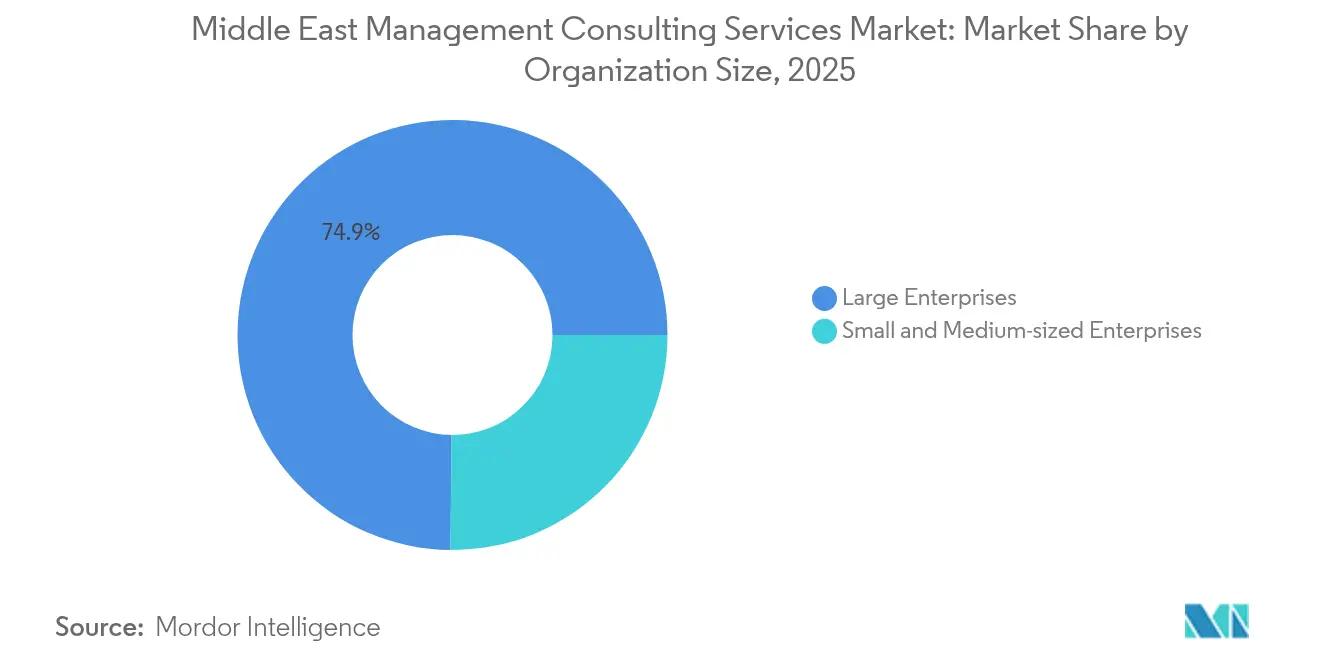

- By organization size, large enterprises held 74.85% of Middle East management consulting services market share in 2025 while SMEs are projected to expand at an 7.25% CAGR through 2031.

- By service type, operations consulting captured 26.82% revenue share in 2025; strategy consulting is forecast to expand at a 4.98% CAGR to 2031.

- By delivery model, on-site engagements accounted for 55.40% share of the Middle East management consulting services market size in 2025, whereas remote and virtual engagements are advancing at a 9.68% CAGR through 2031.

- By end-user industry, financial services commanded 11.64% share of the Middle East management consulting services market size in 2025, and healthcare is progressing at a 5.52% CAGR to 2031.

- By geography, Saudi Arabia led with 45.72% of Middle East management consulting services market share in 2025, while the UAE shows the fastest projected CAGR at 5.31% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation spend by GCC governments | +1.20% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Economic-diversification agendas (Vision 2030, UAE Vision 2031) | +1.80% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Cloud-first mandates by large enterprises | +0.70% | Global | Short term (≤ 2 years) |

| Expansion of giga-projects demanding complex program management | +1.10% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Professionalisation of family-owned conglomerates | +0.90% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Rising demand for ESG and sustainability advisory | +1.00% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Diversification Agendas Drive Structural Consulting Demand

Saudi Arabia’s Vision 2030 and the UAE’s Vision 2031 continue to influence every major advisory tender. Riyadh earmarked USD 24.8 billion for digital infrastructure and reached 99% internet penetration, creating a constant pipeline for regulatory, capability-building, and performance-management projects. The Saudi Data and Artificial Intelligence Authority has already trained 45,000 professionals and plans to train another 25,000 women in data and AI, generating long-tail skills-gap work for consultants. In the UAE, government targets call for AED 3 trillion GDP and AED 800 billion in non-oil exports by 2031, which forces ministries to re-engineer processes and attract outside advisors for governance benchmarking.[2]UAE Government, “‘We the UAE 2031’ vision,” u.ae Because domestic consulting capacity remains thin outside the banking sector, multinational firms and regional boutiques alike find steady demand for public-sector strategy, policy design, and delivery assurance.

Digital Transformation Spend Accelerates Government Modernization

GCC states treat cloud adoption as a cost-saving and service-quality necessity. Bahrain’s Information and eGovernment Authority documented 30-90% IT cost reductions after migrating core workloads to the cloud. Saudi Arabia’s Digital Government Authority lifted its UN e-government ranking from 52nd in 2021 to 31st in 2022 and now supervises regulatory sandboxes for AI, IoT, and blockchain. The national Government Service Bus routes 6,000 digital services and processes 3 billion transactions yearly, obliging ministries to seek ongoing integration and cybersecurity guidance.[3]Ministry of Communications and Information Technology Saudi Arabia, “Government Service Bus Transactions,” my.gov.sa As each milestone triggers new performance benchmarks, specialists in agile governance, enterprise architecture, and data stewardship gain multi-year contracts that lock in predictable fee streams.

Giga-Project Complexity Demands Specialized Program Management

Projects such as NEOM, the Red Sea, and Qiddiya involve combined budgets above USD 1 trillion. NEOM alone expects to spend USD 500 billion, and consultancy briefs span urban design, smart utilities, and circular economy frameworks. Atkins secured a five-year delivery-partner role for THE LINE to coordinate construction logistics for a linear city projected to house 9 million residents. Activities range from contractor selection to integrated command-and-control systems, requiring multidisciplinary teams that mix engineering, digital twins, and sustainability metrics. The long timelines, overlapping governance layers, and multiple funding sources invite continuous advisory input on risk management, stakeholder alignment, and progress auditing.

Rising ESG and Sustainability Advisory Demand

Four out of five large Middle Eastern companies now report formal sustainability strategies, up from 64% in 2023, yet 60% of executives admit frameworks remain incomplete\. Regional climate pledges, including the UAE Net-Zero 2050 strategy and Saudi Arabia’s circular-carbon road map, push corporations toward disclosure standards that mirror EU and U.S. rules. Consulting assignments focus on carbon-accounting baselines, green-finance structuring, and renewable-power feasibility. KPMG projects GCC sustainable-finance assets to post 31.1% annualized growth through 2032, presenting a profitable runway for specialized ESG practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe regional talent crunch and high consultant attrition | -0.80% | Global | Short term (≤ 2 years) |

| Growing in-house strategy teams reducing external spend | -0.60% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Political volatility in select Middle-East markets | -0.50% | Regional hotspots | Short term (≤ 2 years) |

| Price-sensitive SME segment limiting premium fees | -0.40% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hydrocarbon Price Volatility Affecting Fiscal Outlays

Annual turnover at Big Four offices edges toward 20%, magnified by stagnant 2024 compensation packages. Governments lure mid-career consultants with higher, tax-free salaries, draining project leadership pools and forcing firms to recruit globally only to face visa quotas and localization rules. Saudization mandates compel foreign firms to maintain specific local-to-expat ratios, raising payroll and training costs while complicating staffing for rapid mobilizations. Clients experience longer proposal cycles and higher day rates as firms attempt to offset attrition with subcontractors and offshore delivery hubs.

Skilled-Consultant Supply Gap and Wage Inflation

Explosive demand for cloud architects, data scientists, and ESG analysts outpaces regional supply, spurring aggressive recruitment from Europe and North America. Average GCC remuneration for data roles now exceeds European equivalents by up to 59%, according to a 2024 study tracking tech-talent migration. Wage inflation erodes partner-level margins, while local content rules compel firms to fast-track national talent skilling despite a shallow labour pool. The tension elevates retention risk and necessitates investment in academies and remote-delivery models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Large Corporations Anchor Multi-Year Pipelines

Large enterprises controlled 74.85% of the Middle East management consulting services market in 2025 thanks to the capital intensity of transformation programs. Projects tied to Vision 2030 often exceed USD 100 million and demand integrated teams covering strategy, technology, and change management over several years. Complex ownership structures and sovereign wealth fund oversight add governance layers that favour experienced brand-name advisors. Tight delivery deadlines and public scrutiny reinforce a preference for firms with deep benches, risk-mitigation frameworks, and audit-ready documentation standards.

SMEs, though price-sensitive, represent a fertile frontier. Government portals such as Saudi Arabia’s Monsha’at provide subsidized advisory vouchers, encouraging smaller firms to pursue ISO certifications, e-commerce adoption, and succession planning. The segment’s 7.25% CAGR through 2031 outpaces the overall Middle East management consulting services market. Yet average engagement values remain modest, prompting consultancies to develop modular toolkits and virtual delivery to keep utilization high without diluting margins. Digital self-service platforms, prerecorded workshops, and outcome-based pricing resonate with SME owners who seek rapid, affordable solutions.

By Service Type: Operations Dominates, Technology Accelerates

Operations consulting maintained a 26.82% revenue share in 2025 as energy, logistics, and family-owned conglomerates pursued cost efficiency, compliance, and supply-chain resilience. Consultants deploy lean methodologies, control-tower analytics, and workforce upskilling to unlock productivity and standardize governance. The Middle East management consulting services market size for operations projects is projected to grow steadily as privatization efforts require post-deal integration support.

Strategy consulting is the clear momentum play, growing at a 4.98% CAGR. Saudi Arabia’s ICT outlays climbed to USD 40.9 billion in 2025, equal to 4.1% of GDP, underpinned by cybersecurity, AI, and cloud migration mandates. Advisory scopes now cover zero-trust architectures, generative-AI use-case road maps, and sovereign-cloud compliance. Strategy and HR consulting also enjoy durable demand, particularly for public-sector workforce nationalization and family-business succession.

By Delivery Model: On-Site Leadership Persists While Remote Takes Root

In-person work will remain dominant because relationship building, and cultural context carry high importance in the Gulf. Ministries often stipulate local office presence for bidders and request weekly on-site steering meetings. These requirements kept on-site engagements at 55.40% of the Middle East management consulting services market size in 2025.

Remote and hybrid models nonetheless expand at 9.68% CAGR. Post-pandemic clients accept virtual design sprints, cloud-based PMOs, and AI-enabled document review that cut travel cost and accelerate turnaround. Telehealth success stories prove digital service acceptance; Saudi telehealth spend is expected to reach USD 415.4 million in 2025. Firms now bundle virtual advisory with regional “fly-in pods” that appear at critical milestones, balancing cost savings with face-to-face moments of truth.

By End-User Industry: Financial Services Still Prime, Healthcare Rises Fast

Banks and insurers contribute 11.64% of 2025 consulting spend, driven by open-banking rules, Basel III adoption, and rapid fintech partnerships. Projects span core-system modernization, digital identity, Sharia-compliant product design, and enterprise-risk overhaul. Tight regulatory deadlines, combined with cyber-resilience stress testing, sustain premium day rates, making financial services a cornerstone of the Middle East management consulting services market.

Healthcare shows the fastest CAGR at 5.52%. GCC governments invest heavily in hospital PPPs, national health-information exchanges, and value-based-care pilots. The regional healthcare IT market could reach USD 7.9 billion by 2028, requiring consultants in clinical informatics, revenue-cycle digitization, and genomic research partnerships. Energy, manufacturing, real estate, and hospitality each add niche opportunities ranging from green-hydrogen road maps to smart-hotel operating models.

Geography Analysis

Saudi Arabia generated 45.72% of regional revenue in 2025, positioning the Kingdom as the anchor client for most global firms. The state’s Public Investment Fund funnels billions into tourism, sports, and advanced-manufacturing projects, ensuring ongoing advisory demand even while the PwC advisory ban signals heightened scrutiny over deliverable quality and conflict-of-interest safeguards. National data-sovereignty rules and compliance with Saudization quotas require consultants to invest in local delivery centers and Arabic-language capability, cementing the Kingdom’s leverage over supplier terms. Outreach to secondary cities such as Jeddah and Dammam diversifies pipelines beyond Riyadh mega-projects, adding mid-market engagements in logistics hubs and industrial clusters.

The UAE posts the highest forecast growth at 5.31% CAGR to 2031. Dubai remains a regional headquarters magnet, enabling firms to serve Gulf, Africa, and South Asia clients from one tax-efficient location. Non-oil GDP reached AED 1.322 trillion in the first nine months of 2024, with construction, fintech, and e-commerce generating steady advisory spend. Abu Dhabi’s sovereign entities press for portfolio-company operational turnaround and global expansion strategies, while federal regulators pilot ESG disclosure protocols that ripple through audit and advisory lines. The country’s free-zone model and Golden Visa program attract specialist boutiques, intensifying price competition yet broadening skill availability.

Qatar, Kuwait, Oman, and Bahrain collectively form a fast-maturing second tier. Post-World-Cup Qatar invests in knowledge-economy clusters and energy-transition infrastructure, giving rise to procurement optimization and PMO-as-a-service contracts. Kuwait upgrades ports and refineries, generating opportunities in EPC contract management and workforce localization. Oman targets green hydrogen, prompting demand for feasibility studies and supply-chain risk assessments, while Bahrain leans on regulatory-tech sandboxes to stay competitive as a financial hub. Together, these markets diversify revenue streams and hedge consultants against single-country exposure within the overall Middle East management consulting services market.

Competitive Landscape

Market power concentrates in roughly a dozen international brands, led by McKinsey and Company, Boston Consulting Group, Bain and Company, Deloitte, PwC, EY, and KPMG. Combined, those players account for a majority of public-sector transformation and technology-enablement contracts across the GCC. McKinsey’s two-decade presence secures high-profile mandates such as Vision 2030 KPIs and NEOM economic modelling, leveraging proprietary data to differentiate. BCG invests in AI accelerators and country-specific thought leadership, exemplified by its “GCC AI Pulse” series that informs executive briefings. Deloitte and EY benefit from multidisciplinary platforms that unify audit, tax, and advisory, appealing to clients seeking one-stop compliance and transformation partners.

Second-tier challengers carve out niche positions. Kearney partners with ALPHA10X to inject predictive analytics into due-diligence projects, winning cross-border M and A work in energy transition. Oliver Wyman deepens risk-management credentials among regional banks and insurers, while Atkins and DGA Group secure long-duration engineering PMO contracts linked to giga-projects. Technology specialists such as Searce tap demand for cloud modernization and AI Ops, using lower cost bases to undercut incumbents on digital transformation bids. Local champions emerge in Saudi Arabia and the UAE, benefitting from localization policies and government procurement preferences that stipulate local-ownership thresholds.

Regulatory risk shapes the playing field. PwC’s temporary suspension illustrates the downside of governance lapses, forcing rivals to scale capacity quickly to absorb displaced demand. Data-privacy laws, transfer-pricing scrutiny, and anti-corruption regimes heighten compliance costs, favouring firms with strong internal controls. Meanwhile, long-term trends toward outcome-based pricing and co-innovation partnerships are eroding classic time-and-materials models. Competitive success increasingly depends on cloud-native delivery assets, regional talent academies, and ecosystem alliances with hyperscale’s or specialized analytics vendors.

Middle East Management Consulting Services Industry Leaders

McKinsey & Company, Inc.

PricewaterhouseCoopers International Limited

Deloitte Touche Tohmatsu Limited

The Boston Consulting Group, Inc.

KPMG International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Accenture agreed to acquire Maryville Consulting Group to bolster technology-strategy offerings [CONSULTING.US].

- May 2025: Kyndryl reported record signings of USD 18.2 billion, with consulting revenue up 45% year-over-year [KYNDRYL.COM].

- April 2025: IBM bought data-and-AI specialist Hakkoda, adding 350 consultants to its AI practice [CONSULTING.US].

- April 2025: EY partnered with NVIDIA to embed AI agents in new consulting services [CONSULTINGMAG.COM].

Middle East Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types (include implementation consulting, function-specific consulting, and industry-specific consulting, among others) |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

| Saudi Arabia |

| United Arab Emirates |

| Bahrain |

| Kuwait |

| Oman |

| Qatar |

| Rest of Middle East |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types (include implementation consulting, function-specific consulting, and industry-specific consulting, among others) | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-User Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Bahrain | |

| Kuwait | |

| Oman | |

| Qatar | |

| Rest of Middle East |

Key Questions Answered in the Report

How large is the Middle East management consulting services market in 2026?

The market is valued at USD 8.99 billion in 2026 and is projected to reach USD 11.08 billion by 2031.

Which country contributes the most consulting revenue in the region?

Saudi Arabia leads with 45.72% of total consulting revenue thanks to mega-projects and Vision 2030 spending.

Which consulting service line is growing the fastest?

Strategy consulting posts the highest growth at a 4.98% CAGR through 2031 as clients migrate to cloud and adopt AI.

What delivery model is gaining traction after COVID-19?

Remote and virtual engagements are expanding at a 9.68% CAGR as clients accept digital collaboration tools.

Why are sustainability services in demand?

Net-zero pledges and new disclosure rules push firms to seek help with carbon accounting, green finance, and ESG reporting.

What is the biggest operational challenge for consultancies?

A pronounced talent shortage coupled with high attrition inflates staffing costs and elongates project timelines.

Page last updated on: