Oman Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

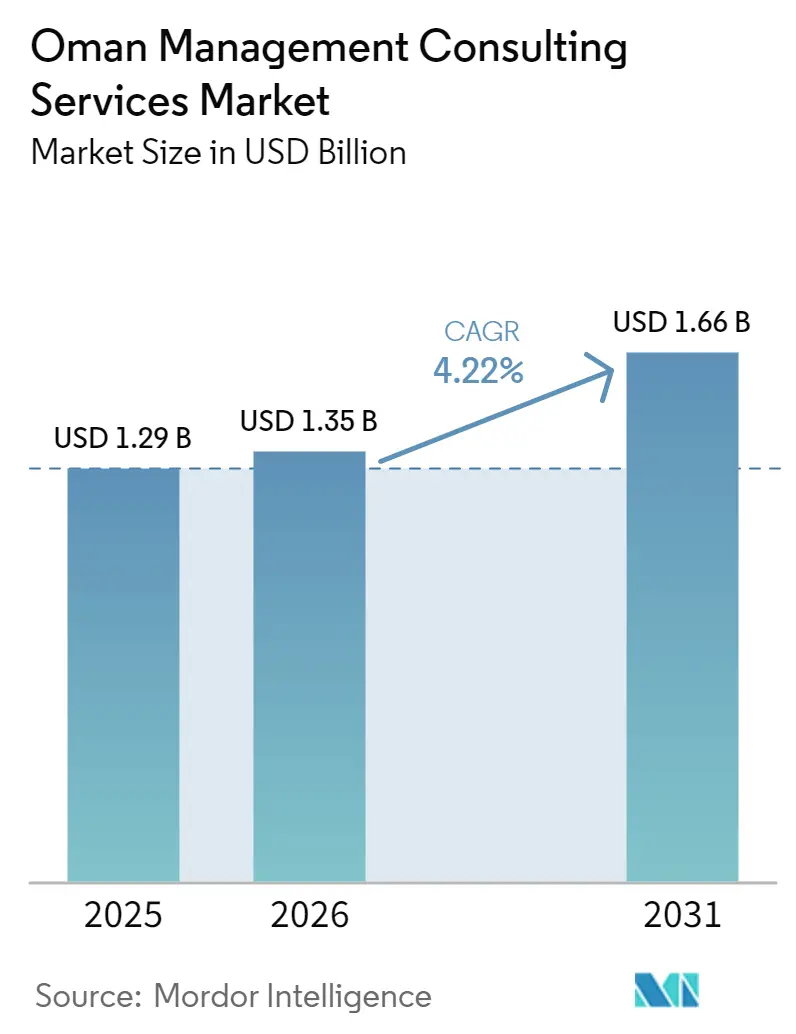

| Base Year Market Size (2025) | USD 1.29 Billion |

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

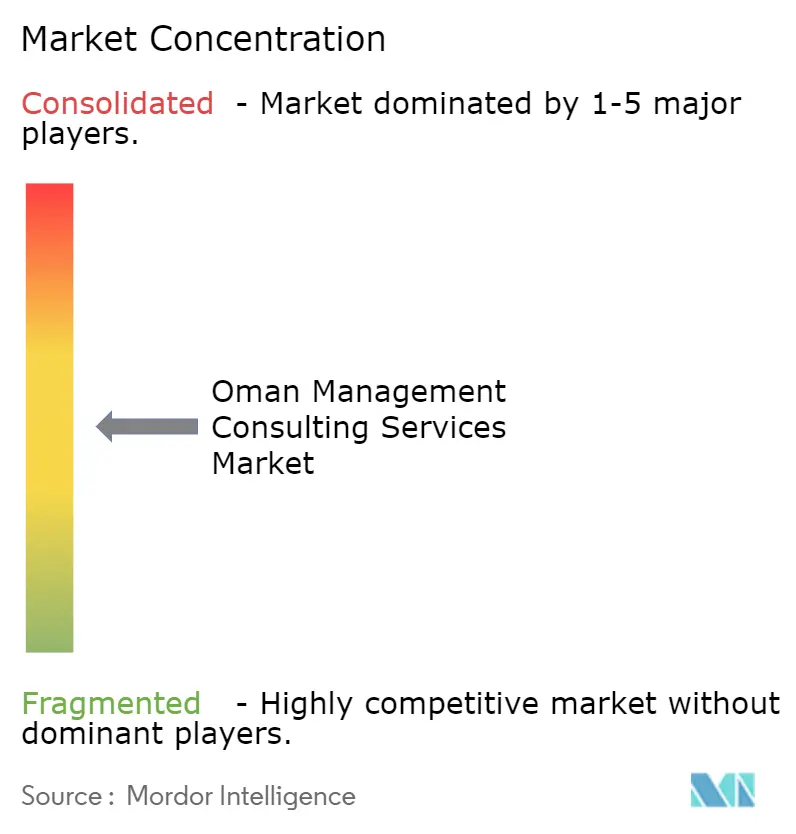

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Management Consulting Services Market Analysis by Mordor Intelligence

The Oman management consulting services market size is projected to expand from USD 1.29 billion in 2025 and USD 1.35 billion in 2026 to USD 1.66 billion by 2031, registering a CAGR of 4.22% between 2026 to 2031. Robust fiscal surpluses allow ministries and state-owned enterprises to fund advisory-intensive programs that translate Vision 2040 objectives into measurable performance gains. Rapid digitalization of 2,680 government procedures is exposing a skills gap that fewer than 3% of the workforce can currently bridge, preserving long-run demand for change-management and upskilling engagements. A USD 3.12 billion five-year ICT outlay and more than 20 active PPP tenders are broadening the client base beyond oil and gas into healthcare, logistics, and green hydrogen. Moderate competitive intensity lets global incumbents capture complex mandates while agile local boutiques win price-sensitive mid-market work, collectively supporting healthy fee growth across the Oman management consulting services market.

Key Report Takeaways

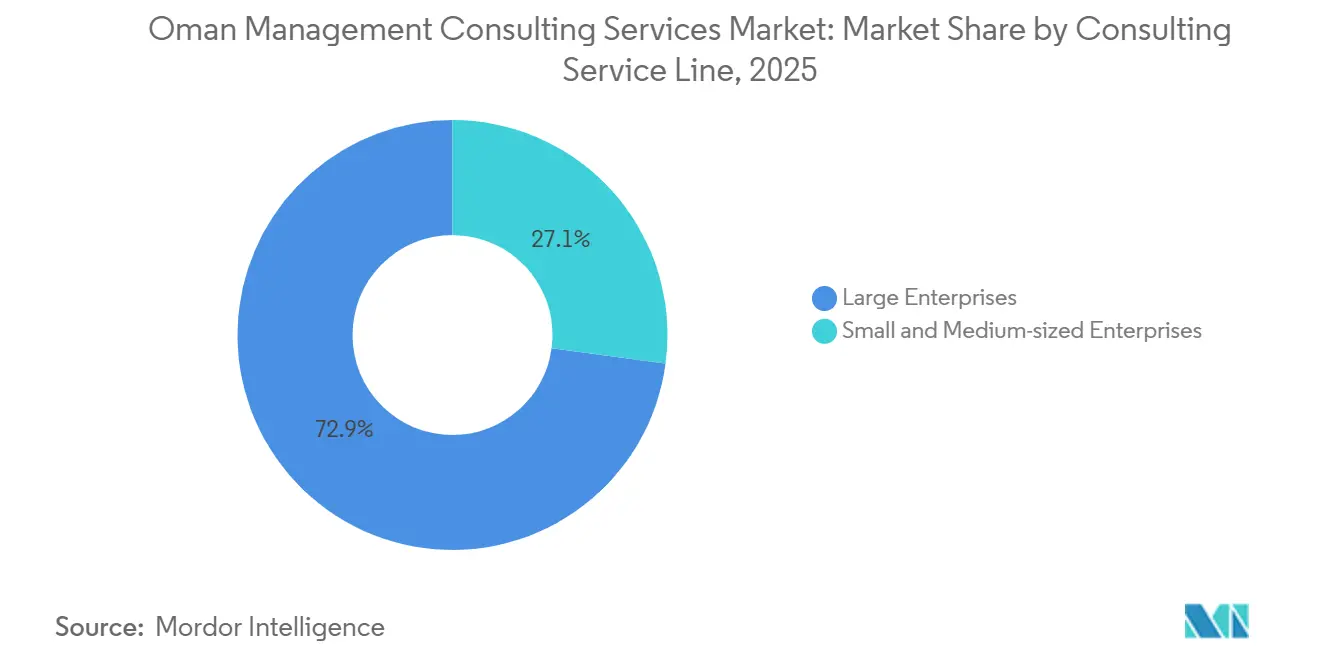

- By consulting service line, Strategy Consulting led with 32.17% of the Oman management consulting services market share in 2025, while Digital Transformation Consulting is advancing at a 4.74% CAGR through 2031.

- By organization size, Large Enterprises accounted for 63.89% of spending in 2025 and Small and Medium-Sized Enterprises are expanding at a 4.31% CAGR through 2031.

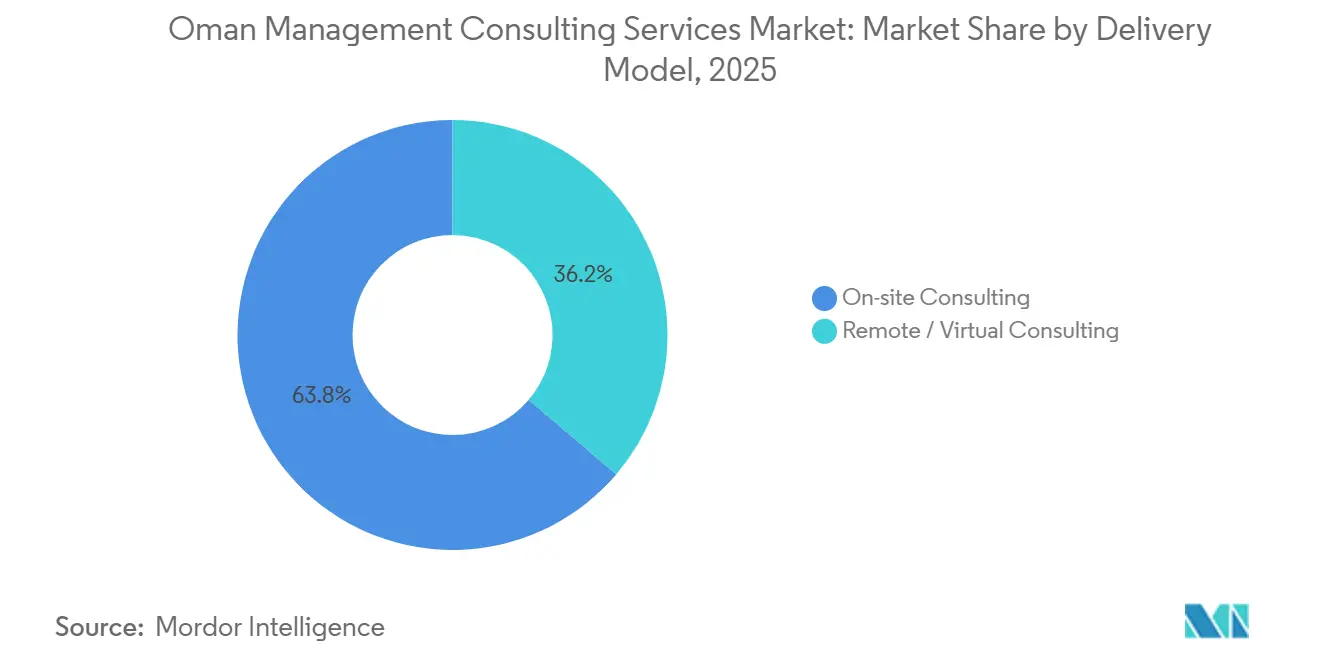

- By delivery model, On-Site Consulting held 71.02% of client expenditure in 2025, whereas Remote and Virtual Consulting is set to grow at a 4.63% CAGR to 2031.

- By end-user industry, the Public Sector contributed 26.32% of demand in 2025 and Healthcare is projected to rise at a 4.58% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2040 Public-Sector Diversification Push | +1.2% | National, early gains in Muscat, Sohar, Duqm | Long term (≥ 4 years) |

| Accelerating Digital-Transformation Spending | +1.1% | National, concentrated in Muscat and industrial zones | Medium term (2-4 years) |

| Rising PPP and FDI Project Pipeline | +0.9% | National, focus on Muscat, Duqm, Dhofar | Medium term (2-4 years) |

| Tightening Compliance With “Omanisation” Quotas | +0.5% | National, acute in banking, energy, manufacturing | Short term (≤ 2 years) |

| SME Financing Surge Driving Advisory Demand | +0.3% | National, concentration in Muscat and Al Batinah | Medium term (2-4 years) |

| Growing Demand for ESG Strategy Alignment | +0.2% | National, led by Muscat Stock Exchange entities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2040 Public-Sector Diversification Push

Vision 2040 has moved from planning into execution, prompting ministries and newly corporatized agencies to seek external expertise in KPI design, program governance, and cross-agency coordination. Non-oil sectors already supply 72.4% of GDP, yet operational capabilities lag strategic ambition, driving recurring demand for outcome-based consulting frameworks. More than 20 PPP tenders launched in 2026, covering healthcare, waste-to-energy, and digital-government platforms, all of which require transaction-advisory support. The Investment Court, operational since 2025, is shortening dispute-resolution timelines and lowering perceived risk for foreign consultancies. A OMR 1.3 billion (USD 3.38 billion) fiscal surplus provides budgetary room for advisory-heavy initiatives in green hydrogen, logistics, and tourism.[1]Oman Observer, “Oman Records Budget Surplus of RO1.3bn in 9M 2025,” omanobserver.om Firms that embed sector-specific operating models rather than generic toolkits are winning multi-year retainer mandates.

Accelerating Digital-Transformation Spending

A OMR 1.2 billion (USD 3.12 billion), five-year ICT commitment is pushing enterprise IT spend toward USD 1.42 billion in 2026, yet only 3% of workers possess advanced technology skills. Consultancies are therefore delivering end-to-end programs that blend cloud migration with change-management and workforce upskilling. Interoperability gaps among the 2,680 digitalized public procedures compel agencies to hire advisors for data-governance and citizen-experience redesign.[2]Oman Observer, “Oman Records Budget Surplus of RO1.3bn in 9M 2025,” omanobserver.om Phased rollout of Fawtara e-invoicing and the National Health Data Platform is triggering ERP overhauls and clinical workflow redesign. Regional surveys show 84% AI adoption but only 11% value realization, underscoring the monetization gap that specialized digital-transformation consultancies aim to close.

Rising PPP and FDI Project Pipeline

Oman’s active PPP list now exceeds 20 projects worth over USD 1 billion, spreading advisory opportunities across financial modeling, risk allocation, and contract structuring. Governance reforms, most notably the Investment Court and improved corruption-perception scores, have lowered entry barriers for international investors.[3]Oman Observer, “Oman Advances Over 20 PPP Projects in 2026,” omanobserver.om Duqm Port’s Terminal 3 expansion and OQ’s fully operational refinery create downstream supply-chain and workforce-planning engagements. The green-hydrogen roadmap calls for electrochemical process engineering and blended-finance expertise, niches where domestic capability is scarce. Water-security initiatives grounded in nature-based solutions add another layer of feasibility studies and PPP-framework design work.

Tightening Compliance With “Omanization” Quotas

Private-sector Omanisation compliance reached 42.8% in 2025, and sectoral targets as high as 70% are accelerating demand for HR strategy, succession planning, and competency-based training.[4]Oman Observer, “Omanisation in Private Sector Reaches 42.8% in September,” omanobserver.om Skills shortages persist: Sohar’s petrochemical cluster needs up to 400 new technical professionals annually but universities graduate fewer than 100 chemical engineers. Consultancies are designing dual-track programs that pair expatriate experts with Omani trainees to meet quota timelines. Competitive salary gaps, 20-30% below offers in Saudi Arabia and the UAE, require compensation-benchmarking advice. Enterprises also engage advisors to navigate Resolution 38/2023, which stipulates 90% local representation in administrative roles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price-Sensitivity and Internal Capability Build-Up | -0.4% | National, acute in SME and mid-market segments | Medium term (2-4 years) |

| Shortage of Specialized Local Talent | -0.3% | National, concentrated in Sohar, Duqm, technical sectors | Long term (≥ 4 years) |

| Lengthy Public-Sector Procurement Cycles | -0.2% | National, impacting government and SOE engagements | Short term (≤ 2 years) |

| Relationship-Driven Buying Culture Limits Formal Tenders | -0.1% | National, prevalent in private and family-owned enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price-Sensitivity and Internal Capability Build-Up

SMEs and many mid-market firms favor low-cost local advisors or internal teams, compressing fee rates and shortening mandate durations. State-owned enterprises have also created in-house strategy units that reduce external spend on routine projects. Competitive tenders regularly see local boutiques underbid global firms by 30-40% for standardized ISO or compliance work, compelling multinationals to chase only high-complexity engagements. Riyada’s incubators now bundle advisory with subsidized finance, further squeezing commercial demand in the sub-USD 50,000 bracket. Consultants therefore differentiate through deep sector expertise and proven value capture rather than brand prestige alone.

Shortage of Specialized Local Talent

Fewer than 3% of Omani workers hold advanced ICT skills, and STEM graduates often lack job-ready competencies, forcing consultancies to absorb long onboarding periods before staff become billable. Sohar and Duqm each report vacancy rates above 60% for niche process-safety and maritime roles.[5]KiTalent Research Team, “Sohar’s Petrochemical Complex Produces World-Class Output but Cannot Produce the Workforce to Run It,” kitalent.com High expatriate salary premiums, coupled with regional talent migration to Dubai and Riyadh, inflate delivery costs and extend project timelines. Training-provider shortages mean firms must invest directly in academy-style programs or remote centers of excellence. Persistent gaps threaten scalability of the Oman management consulting services market, making talent strategy a board-level priority for both clients and advisory firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Strategy Remains Core While Digital Scales Quickly

Strategy Consulting held 32.17% of the Oman management consulting services market share in 2025, reflecting ministries and state-owned enterprises that need sector roadmaps, KPI frameworks, and governance models. Digital Transformation Consulting is projected to expand at a 4.74% CAGR through 2031 because only 3% of the workforce can support the cloud, data, and AI platforms already procured. Operations advisory demand clusters around Sohar and Duqm, where petrochemical and logistics clients seek lean supply-chains and process-safety upgrades. HR Consulting continues to ride tightening Omanisation quotas, which now require some industries to achieve 60-70% local staffing. Financial-advisory and risk practices benefit from the wave of PPP financings and new ESG mandates.

Digital work is becoming the default cross-cutting theme that links every other service line, meaning that few engagements proceed without at least a modest technology component. Strategy houses now embed analytics pods to keep their grip on the largest slice of the Oman management consulting services market size. Mid-tier firms target template-driven ISO certifications and compliance checks, freeing global incumbents to chase multimillion-dollar transformation programs. Growing PPP and green-hydrogen pipelines are generating blended teams that combine transaction, regulatory, and sustainability skills. As a result, the service-mix gap between boutique and multinational providers is widening, even though price competition stays intense.

By Organization Size: Large Enterprises Dominate but SME Momentum is Building

Large Enterprises captured 63.89% of 2025 spend because listed corporates and energy majors outsource complex digital-and-ESG mandates that often exceed USD 100,000 per engagement. These companies hold board-level budgets that shield consulting outlays from the price compression seen lower down the pyramid. The Oman management consulting services market size attributable to Small and Medium-Sized Enterprises is smaller yet expanding at a 4.31% CAGR as Riyada’s 2026-2030 plan channels subsidized advisory to 130,359 registered firms. SMEs typically purchase discrete projects such as business-plan drafting, ISO audits, or Omanisation compliance checklists priced below USD 50,000. Local boutiques and mid-tier networks use relationship capital and shorter delivery cycles to win this volume-driven business.

Internal capability build-ups at state-owned enterprises are squeezing share-of-wallet for routine strategy work, redirecting external advisors toward higher-complexity tasks. Multinationals respond by offering hybrid delivery that pairs offshore centers of excellence with onsite stakeholder workshops, maintaining relevance without inflating fees. Boutique players counter with fixed-fee packages and rapid turnaround, appealing to cash-constrained SMEs. Over the forecast horizon, SME formalization and mandatory ESG reporting will steadily shift the Oman management consulting services market share toward the mid-market, even as corporates continue to anchor overall revenue. The coexistence of premium and value tiers therefore creates a barbell structure that favors specialists at both ends.

By Delivery Model: On-Site Still Leads, Remote Gains Sustainable Traction

On-Site consulting commanded 71.02% of 2025 expenditure because personal relationships and cultural norms favor face-to-face trust-building, especially within the public sector. The format also benefits from the country’s compact geography, where most client sites are a short flight or drive from Muscat. Remote and Virtual Consulting is, however, the fastest-growing model at a 4.63% CAGR as clients seek cost relief and scarce offshore expertise. Hybrid engagements that combine kickoff workshops in person with remote analytics and design sprints now account for a rising slice of the Oman management consulting services market size. Technology partners like Datamount and global firms such as Deloitte exemplify this blended approach.

Talent shortages further propel remote delivery, allowing firms to tap regional specialists without permanent relocation. Digital upskilling inside client organizations reduces resistance to screen-based collaboration, shrinking the cultural gap that once limited virtual formats. Fee structures are beginning to reflect this trend, with time-and-materials contracts replaced by milestone-linked pricing that rewards outcome rather than hours spent onsite. Yet many government ministries still insist on physical presence for final sign-offs, a factor that will keep on-site options dominant through 2031. The net result is a deliberate but irreversible pivot toward mixed-mode projects that optimize reach, talent, and cost.

By End-User Industry: Public Sector Anchors Spend, Healthcare Accelerates Fastest

The Public Sector delivered 26.32% of overall demand in 2025 because Vision 2040 execution tasks, digital-government rollouts, PPP structuring, and organizational redesign, require constant advisory input. State budgets backed by a OMR 1.3 billion (USD 3.38 billion) surplus provide ample funding for these engagements. Healthcare is the fastest-growing vertical at a 4.58% CAGR thanks to a OMR 1 billion (USD 2.6 billion) 2026 allocation for the National Health Data Platform and PACS integration. IT and telecommunications clients elevate cybersecurity and cloud migration projects, while manufacturing in Sohar needs operational-excellence and Omanisation roadmaps. Banking and insurance hire consultants to meet 60-70% localization targets and comply with new ESG disclosures.

Healthcare’s surge broadens the Oman management consulting services market share beyond its traditional government nucleus, offering mid-tier IT specialists a foothold through workflow redesign and clinician-training mandates. Energy transition initiatives in green hydrogen and carbon capture also beckon, opening slots for niche engineering and project-finance advisors. Tourism developments in Salalah and Mussandam sustain demand for feasibility studies and destination marketing. As industry diversification deepens, consultants with multi-disciplinary teams that can bridge policy, technology, and human-capital gaps will capture outsized wallet share. The industry mix, therefore, is set to become more balanced, even while public entities remain the single largest buyer of advisory services.

Geography Analysis

Muscat houses an estimated 55-60% of the Oman management consulting services market because ministries, exchanges, and most corporate headquarters cluster in the capital. This concentration enables dense advisor-client interaction and fuels a localized talent ecosystem. Sohar ranks second, where a petrochemical workforce of up to 15,000 and annual demand for 300-400 new engineers generate continuous process-optimization and Omanisation advisory needs.

Duqm is emerging as a third pole. Terminal 3’s 2 million TEU capacity addition and the refinery’s full operation create project-finance and workforce-planning engagements, while a looming green-hydrogen complex promises niche electrochemical consulting. Dhofar, centered on Salalah, attracts tourism-strategy and logistics mandates, exemplified by Horwath HTL feasibility studies for mixed-use resorts. Al Batinah’s SME-heavy coastal belt requires business-plan preparation and compliance support under Riyada programs, adding midsized opportunities to the Oman management consulting services market footprint.

Regional shocks also influence consulting demand. Red Sea disruptions diverted cargo toward Duqm, spiking short-term logistics advisory. Conversely, project delays, such as the PDH/PP complex’s postponed FID, momentarily thin Duqm’s pipeline, illustrating how single assets can sway local consulting volumes within the broader Oman management consulting services market.

Competitive Landscape

The market remains moderately fragmented. The Big Four dominate complex government and energy mandates through global frameworks and local benches. Strategy houses, McKinsey, BCG, Bain, Strategy&, deploy fly-in teams from Dubai and Riyadh for high-value transformation projects. Mid-tier networks such as Grant Thornton, BDO, Crowe, and Moore leverage competitive pricing and relationship capital to win SME work. Local boutiques like Tanfidh Consulting and Horwath HTL specialize in hospitality, PPP implementation, and family-business advisory, rounding out the Oman management consulting services industry.

Strategic moves underline capacity expansion. PwC added 62 regional partners in June 2025. Deloitte allied with Datamount for cybersecurity in September 2025. KPMG’s e-invoicing toolkits cement compliance leadership. Grant Thornton’s April 2025 cross-border merger grants Omani clients access to 13,000 specialists worldwide. Technology adoption also differentiates players: BDO invests in generative-AI dashboards, and BCG’s Digital Ventures hub in Dubai extends rapid-prototyping capability.

White-space opportunities abound in AI scale-up, ESG strategy, and green-hydrogen finance, yet talent scarcity and price pressure temper margin expansion. Overall, competitive intensity balances between brand-driven global players and nimble local specialists, sustaining a dynamic but not cut-throat environment in the Oman management consulting services market.

Oman Management Consulting Services Industry Leaders

PricewaterhouseCoopers International Limited

Deloitte Touche Tohmatsu Limited

Ernst & Young Global Limited

KPMG International Limited (Cooperative)

McKinsey & Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: KPMG expanded its Amman office to operate as a regional hub, enhancing cross-border advisory capacity for clients in Oman, Jordan, and neighboring markets.

- February 2026: Roland Berger issued a Gulf-wide AI adoption study showing 84% usage but only 11% scaled value realization.

- January 2026: KPMG Oman released a granular analysis of the 2026 state budget to guide public-finance prioritization.

- November 2025: Roland Berger appointed Kenan Nouwailati as Senior Partner for Middle East operations, reinforcing its regional transformation practice.

Oman Management Consulting Services Market Report Scope

The Oman Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Oman management consulting services market size and its growth outlook?

The market is valued at USD 1.35 billion in 2026 and is projected to reach USD 1.66 billion by 2031, expanding at a 4.22% CAGR.

Which consulting service line is growing fastest in Oman?

Digital Transformation Consulting is forecast to rise at a 4.74% CAGR as enterprises invest in cloud, AI, and data analytics.

How are Omanisation policies affecting consulting demand?

Stricter quotas are lifting demand for HR strategy and training programs as companies seek to align workforce plans with regulatory targets.

What regions outside Muscat are creating notable advisory opportunities?

Sohar's petrochemical hub and Duqm's expanding port and refinery projects drive operational-excellence, project-finance, and workforce-planning mandates.

Which end-user industry is expected to grow the fastest?

Healthcare consulting is projected to advance at a 4.58% CAGR due to a OMR 1 billion (USD 2.6 billion) 2026 budget and nationwide health data initiatives.

How competitive is the consulting landscape in Oman?

The market is moderately fragmented; global Big Four firms dominate complex mandates while agile local boutiques capture price-sensitive SME work.

Page last updated on: