Egypt Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

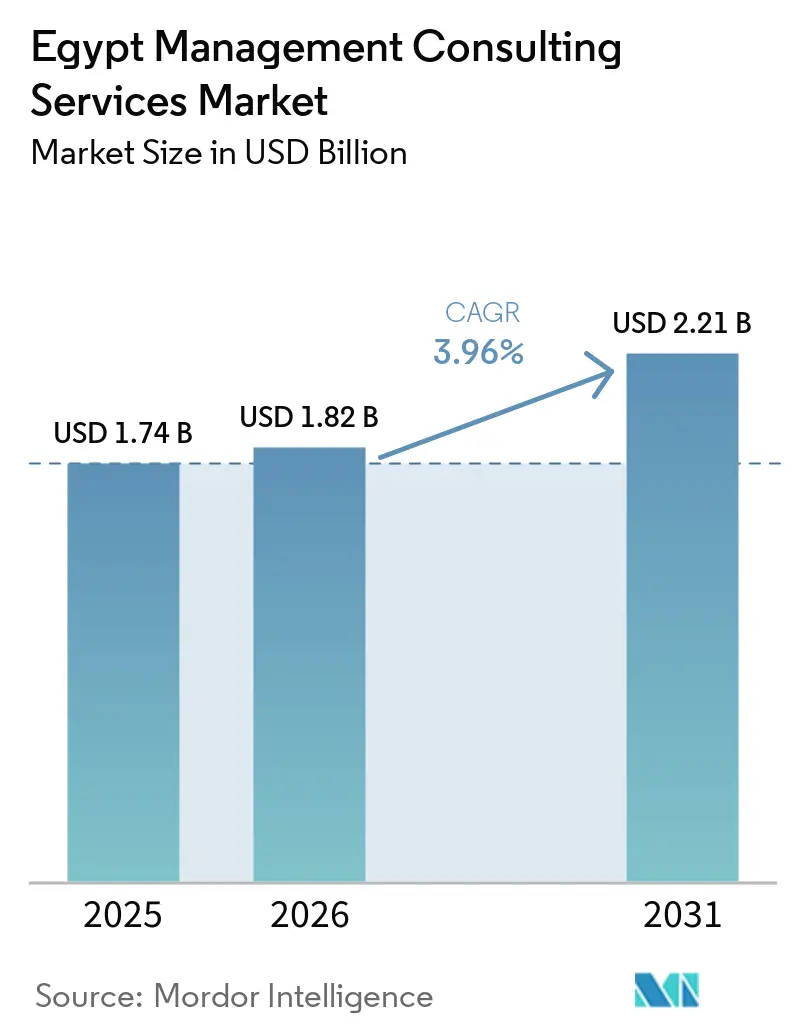

| Base Year Market Size (2025) | USD 1.74 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Management Consulting Services Market Analysis by Mordor Intelligence

The Egypt management consulting services market size is projected to be USD 1.74 billion in 2025, USD 1.82 billion in 2026, and reach USD 2.21 billion by 2031, growing at a CAGR of 3.96% from 2026 to 2031. Demand is being reshaped by Vision 2030-linked diversification projects, rising foreign direct investment, and an enterprise shift to hybrid delivery that blends on-site workshops with remote execution. Currency volatility and persistent inflation are forcing clients to prioritize engagements that deliver rapid cost savings, yet the introduction of mandatory ESG disclosure rules is unlocking new advisory budgets. International firms are expanding Egyptian delivery centers to serve Middle East, Africa, and European clients, while local specialists are capturing share in Arabic-language AI and sustainability reporting. Overall, advisory opportunities are moving from pure technology roll-outs toward integrated digital-plus-compliance programs, keeping the Egypt management consulting services market on a moderate but resilient growth trajectory.

Key Report Takeaways

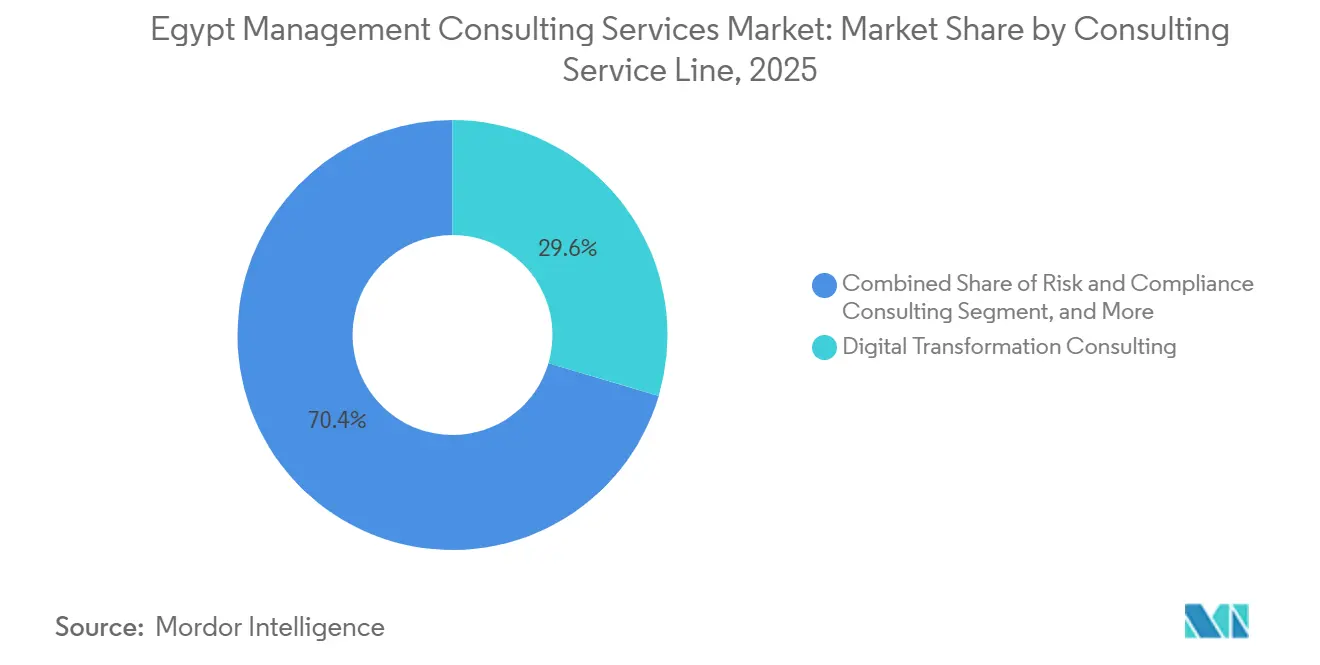

- By consulting service line, digital transformation consulting led with 29.57% revenue share in 2025 while risk and compliance consulting is forecast to expand at a 4.16% CAGR through 2031.

- By organization size, large enterprises held 62.88% share in 2025, whereas small and medium-sized enterprises are projected to grow at a 3.98% CAGR over 2026-2031.

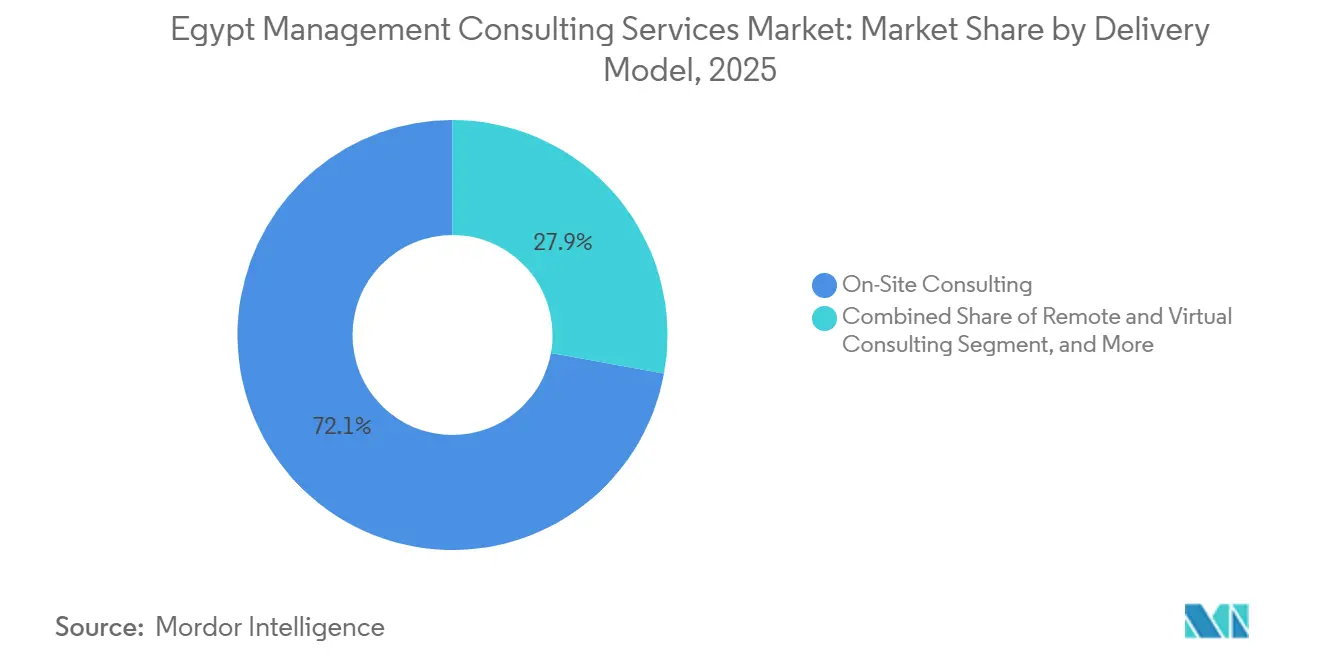

- By delivery model, on-site consulting accounted for 72.13% of revenue in 2025, while remote and virtual consulting is set to increase at a 4.23% CAGR to 2031.

- By end user industry, banking and insurance contributed 21.48% of demand in 2025 and healthcare is advancing at a 4.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Enterprise Transformation Roadmap Adoption | +1.2% | National, concentrated in Cairo, Alexandria, New Administrative Capital | Medium term (2-4 years) |

| Government-Backed Vision 2030 Economic Diversification Programs | +0.9% | National, with spillover to regional shared-services hubs | Long term (≥ 4 years) |

| Capital-Market Liberalization Attracting Foreign Investment Inflows | +0.7% | National, particularly Cairo financial district and free zones | Short term (≤ 2 years) |

| Post-COVID Near-Shoring of Shared-Services Centers to Egypt | +0.5% | National, early gains in Cairo, Alexandria, and Smart Village clusters | Medium term (2-4 years) |

| Exploding Local Start-Up Ecosystem Needing Scale-Up Advisory | +0.4% | National, concentrated in Cairo and emerging tech hubs | Medium term (2-4 years) |

| Mandatory ESG Disclosure Rules Driving Compliance Consulting | +0.3% | National, affecting listed companies and non-bank financial institutions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-First Enterprise Transformation Roadmap Adoption

Enterprises have shifted from isolated upgrades to multi-year transformation roadmaps that integrate cloud, data, and automation. The Central Bank’s digital financial identification system, MIDBANK’s core-banking revamp, and ADCB Egypt’s payments hub signal production-scale deployments that require governance frameworks and legacy integration. ITIDA’s 74 export agreements targeting USD 9 billion in digital services by 2026 validate Egypt’s nearshore appeal. Consulting firms are responding by opening delivery centers and training academies, such as IBM Consulting’s five-year AI skills collaboration with MCIT. Growth is steady because digital programs now bundle compliance and change-management elements that resist commoditization.

Government-Backed Vision 2030 Economic Diversification Programs

Vision 2030 channels capital into renewable energy, advanced manufacturing, and healthcare, each demanding specialized advisory. Cutting oil arrears to USD 1.2 billion by April 2026 signaled fiscal discipline that lifted investor confidence. McKinsey’s February 2026 roadmap highlights sectors that could improve the trade balance by up to USD 17 billion, creating a clear pipeline for consultants. Boston Consulting Group’s work on agricultural supply chains shows advisors embedded in policy design rather than waiting for tenders. The multi-year horizon underpins predictable demand even though execution risks remain.[1]Daily News Egypt Staff, “Eighteen U.S. and Global Firms Eye Egyptian Investments,” dailynewsegypt.com

Capital-Market Liberalization Attracting Foreign Investment Inflows

Flexible exchange rates and relaxed ownership caps drew USD 11 billion of FDI in 2025, notably the USD 35 billion Ras El-Hekma project. New legal structures for venture capital and green-bond issuance are spawning mandates in valuation, due diligence, and post-merger integration. Yet portfolio flows are volatile, as shown by USD 7 billion in Treasury-bill outflows in early 2026, pushing consultants to deliver quick, measurable ROI. Decision No. 36-2026 on carbon disclosure directly links liberalization to ESG compliance services.[2]General Authority for Investment and Free Zones, “Decision No. 36 of 2026,” investinegypt.gov.eg

Post-COVID Near-Shoring of Shared-Services Centers to Egypt

Time-zone alignment with Europe and multilingual talent are drawing BPO and shared-services centers from higher-cost locales. Konecta’s USD 100 million commitment for a generative AI hub and TTEC’s recent capacity expansions illustrate the trend. Site selection, talent strategy, and process re-design projects are accelerating as companies look to stabilize supply chains close to end markets. Advisory firms are also incubating startups, illustrated by Wider Consulting’s plan to launch 50 ventures by 2026, blending consulting with venture building.[3]Konecta Communications, “Konecta Signs MoU with ITIDA,” konecta.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent FX Volatility Impacting Consulting Budgets | -0.6% | National, acute in import-dependent sectors | Short term (≤ 2 years) |

| Talent Attrition to GCC and EU Markets | -0.5% | National, concentrated in Cairo and Alexandria professional clusters | Medium term (2-4 years) |

| Informal Economy’s Low Consulting-Spend Penetration | -0.3% | National, particularly in retail, construction, and agriculture | Long term (≥ 4 years) |

| AI Self-Service Strategy Platforms Cannibalizing Entry-Level Projects | -0.2% | National, affecting digital-native sectors first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent FX Volatility Impacting Consulting Budgets

The EGP weakened from 47.7 to 54.26 per USD in early 2026, while energy import bills tripled, squeezing corporate liquidity. Although the Central Bank cut policy rates and inflation fell, real borrowing costs remain high, leading clients to defer non-essential projects. Consultants are adopting phased deliverables and local-currency pricing to ease pain, but margins remain under pressure. Simultaneously, demand for treasury and hedging advisory rises, creating a paradox of need versus affordability.

Talent Attrition to GCC and EU Markets

Rising Gulf salaries continue to lure mid-level and senior consultants, with each 1% of emigrating professionals estimated to cost 5.7% of GDP. Global majors and local firms compete for the same pool, intensifying wage inflation. Training initiatives, IBM and MCIT, Microsoft and MCIT, and the Central Bank’s AI for Banking Diploma, aim to replenish skills, but benefits are medium term. Scarcity is acute in ESG reporting, AI governance, and Arabic NLP, where demand is surging.[4]Consultancy-me Editorial, “Injaz Consulting Group Named Delivery Partner,” consultancy-me.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Risk and Compliance Pushes Past Pure Technology

Risk and Compliance Consulting is projected to grow at a 4.16% CAGR to 2031, the fastest among all lines, as Decision No. 36-2026 mandates carbon disclosure for listed companies. The Egypt management consulting services market share held by digital transformation consulting was 29.57% in 2025, signaling maturity yet moderating expansion. Advisory firms are packaging digital, risk, and ESG in unified offerings that defend pricing even as standalone technology work commoditizes. Local boutiques such as Foresight Consulting are capitalizing on sustainability mandates, while global majors cross-sell risk frameworks into existing transformation accounts.

The Egypt management consulting services market size attached to financial advisory remains episodic but lucrative, following FDI inflows and landmark deals such as Ras El-Hekma. Operations consulting is gaining relevance in manufacturing, where inflation makes efficiency critical. HR consulting demand is buoyed by retention challenges, especially for AI talent. Over the forecast period, bundled digital-plus-compliance engagements are expected to anchor revenue resilience.

By Organization Size: Formalization and Venture Capital Lift SMEs

Large enterprises commanded 62.88% of 2025 revenue, yet SMEs are forecast to record a 3.98% CAGR as startup funding scales and tax digitization deepens. Government initiatives such as the USD 1 billion fund-of-funds and 130% growth in venture capital to USD 614 million in 2025 broaden the advisory addressable base. Wider Consulting’s investment exemplifies how firms marry consulting with venture incubation to capture SME demand.

The Egypt management consulting services market size flowing to SMEs remains smaller than that of corporates, yet growth potential is significant once informal businesses register for digital tax. Consulting firms are curating standardized toolkits, fractional CFO services, and shared training platforms to match SME budgets. Large corporates will continue to dominate high-complexity strategy and M&A work, but SMEs provide a scalable pipeline for compliance and digital enablement services.

By Delivery Model: Hybrid Consulting Becomes the Norm

On-site delivery retained 72.13% share in 2025 because strategy formulation and change management still rely on face-to-face work. However, remote and virtual consulting is logged at a 4.23% CAGR, catalyzed by cost pressure and maturing collaboration technology. Hybrid models send senior advisors on-site for critical phases but shift analytics, documentation, and testing to Egypt-based centers. PwC’s 400-person innovation center and Deloitte’s Cairo hub illustrate this pivot.

The Egypt management consulting services market size tied to fully remote execution should continue to expand within IT advisory and data analytics. Meanwhile, hybrid engagements help defend margins by optimizing utilization across local and offshore pools. Currency depreciation makes on-site work relatively more expensive for dollar-billed clients, further tipping the balance toward mixed delivery.

By End User Industry: Digital Health Propels Healthcare Up the Rankings

Banking and insurance contributed 21.48% of 2025 revenue, anchored by core-banking transformations and payments modernization. Healthcare is set to outpace all other verticals with a 4.09% CAGR, powered by the National Digital Health Strategy 2025-2029 and expansion of universal coverage. The Egypt management consulting services market share directed to public-sector ministries also remains meaningful as government agencies pursue tax digitization, customs automation, and AI governance.

Telecoms and IT remain strong consulting buyers, demonstrated by IBM Consulting’s five-year AI skills program and Telecom Egypt’s OSS overhaul. Manufacturing clients seek supply-chain resilience and cost optimization amid currency swings. Energy and resources firms increasingly request renewable-project advisory, positioning consultants at the center of Egypt’s energy transition.

Geography Analysis

Greater Cairo anchors the Egypt management consulting services market, housing ministries, multinational headquarters, and the New Administrative Capital. Alexandria and Smart Village clusters supply additional demand and talent. Vision 2030 diversification and USD 11 billion of 2025 FDI validate Egypt’s role as a regional hub for shared services. ITIDA’s aim of USD 9 billion in digital exports by 2026 positions consulting delivery centers as core export generators.

Egypt’s integration into Middle East and Africa supply chains, coupled with initiatives such as the East Mediterranean Gas Forum, expands the market’s regional relevance. The February 2026 launch of the sovereign Karnak language model and the AI-Share initiative embed Egypt in cross-border AI collaboration, increasing consulting demand in localization and governance.

Nevertheless, currency instability, talent migration, and a sizable informal economy restrain growth. Suez Canal revenue declines and higher energy import bills compress client budgets, directing spending toward cost-saving mandates. The success of government reforms, tax digitization, private investment zones, and universal health coverage, will determine how broadly the Egypt management consulting services market penetrates beyond its core metropolitan strongholds.

Competitive Landscape

The Egypt management consulting services market is moderately fragmented. Global majors, PwC, Deloitte, EY, KPMG, McKinsey, BCG, Bain, Accenture, IBM Consulting, expand local headcount to leverage cost advantages and multilingual talent. PwC invested USD 10 million in its Cairo technology center, hiring 400 experts, while Deloitte committed USD 30 million to scale its hub toward 5,000 employees. Capgemini’s April 2025 announcement of an AI Center of Excellence that will double its staff to 1,200 showcases confidence in Egypt’s delivery capability.

Regional specialists like Oliver Wyman, Roland Berger, and Kearney focus on high-value strategy mandates in energy and transport. Local firms, including Grant Thornton Egypt, Nile Capital Consulting, Pharos Consultancy, and Foresight Consulting, differentiate through ESG expertise and Arabic-language AI. Foresight’s partnership with GAFI to prepare annual sustainability reports exemplifies this specialization.

Emerging players blend consulting with technology platforms. SolvFast offers an AI-enabled suite that challenges entry-level transformation projects, while Wider Consulting deploys USD 14.3 million to seed startups it can later advise. Talent development partnerships, IBM with MCIT, Microsoft with MCIT, and Accenture with Cassava Technologies, illustrate how firms invest in national AI strategies to secure future demand.

Egypt Management Consulting Services Industry Leaders

McKinsey & Company Inc.

Boston Consulting Group Ltd.

Deloitte Touche Tohmatsu Ltd.

Accenture plc

Bain & Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Eighteen U.S. and global firms, including GE Healthcare, Philips, and Lockheed Martin, explored Egyptian investments after the government cut oil arrears to USD 1.2 billion, bolstering demand for transaction and regulatory advisory.

- March 2026: Wider Consulting announced a USD 14.3 million plan to create 50 startups across Egypt and Saudi Arabia by end-2026, integrating accelerator services into its advisory model.

- February 2026: MCIT and ITIDA launched Karnak, a 30-80 billion-parameter national language model, unveiling AI tutor, legal assistant, and healthcare diagnostics use cases at the Ai Everything MEA summit.

- February 2026: McKinsey released a report identifying 11 priority sectors that could lift Egypt’s trade balance by USD 13-17 billion, guiding sector-focused consulting engagements.

Egypt Management Consulting Services Market Report Scope

The Egypt Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| Strategy Consulting | Operations Consulting |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Egypt management consulting services market and how fast is it growing?

The market stands at USD 1.82 billion in 2026 and is forecast to reach USD 2.21 billion by 2031, posting a 3.96% CAGR during 2026-2031.

Which consulting service line is expanding the fastest in Egypt?

Risk and compliance consulting leads growth with a projected 4.16% CAGR through 2031, propelled by new ESG disclosure mandates.

Why are hybrid delivery models gaining traction among Egyptian consulting clients?

Hybrid setups cut travel costs, tap Egypt-based talent pools, and enable firms to assign senior staff on-site only for critical phases, improving efficiency without sacrificing client proximity.

How does Vision 2030 influence consulting demand?

Vision 2030 funnels public and private capital into diversified sectors that require advisory on regulation, financing, and execution, securing multi-year pipelines for consulting engagements.

What challenges constrain consulting growth in Egypt?

Currency volatility, talent migration to GCC and EU markets, and the large informal economy curb consulting budgets and talent availability, tempering otherwise solid demand drivers.

Which industry vertical is likely to outpace others in consulting spend growth?

Healthcare is projected to record the fastest growth, supported by the National Digital Health Strategy 2025-2029 and the roll-out of universal health insurance.

Page last updated on: