Bahrain Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

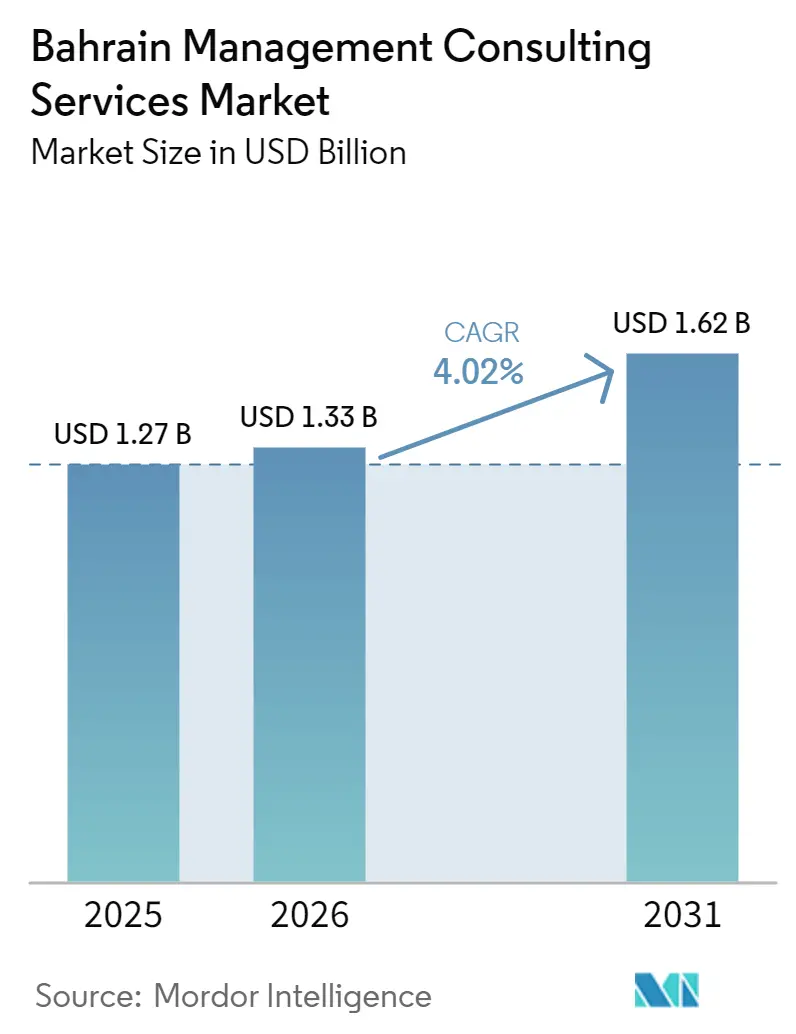

| Base Year Market Size (2025) | USD 1.27 Billion |

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Management Consulting Services Market Analysis by Mordor Intelligence

The Bahrain management consulting services market size is expected to grow from USD 1.27 billion in 2025 to USD 1.33 billion in 2026 and is forecast to reach USD 1.62 billion by 2031 at 4.02% CAGR over 2026-2031. Recent momentum reflects government procurement linked to Bahrain Economic Vision 2030, widening adoption of digital-first programs across banking and telecommunications, and fast-rising demand for ESG advisory that aligns with evolving Central Bank of Bahrain disclosure rules. Strategy consulting continues to anchor revenue as family-owned conglomerates pursue succession roadmaps and sovereign wealth funds fine-tune portfolios, while digital transformation consulting is gaining pace as projects shift from technology pilots toward measurable automation results. Large enterprises dominate spending because compliance-heavy sectors such as financial services and energy rely on ongoing advisory support, yet small and medium-sized enterprises are strengthening demand thanks to Tamkeen’s 2026-2030 incentives and stricter value-added-tax oversight. Competitive intensity is increasing as Big Four networks scale up local headcount and regional boutiques capture niche mandates, pressuring margins and talent pipelines across the Bahrain management consulting services market.

Key Report Takeaways

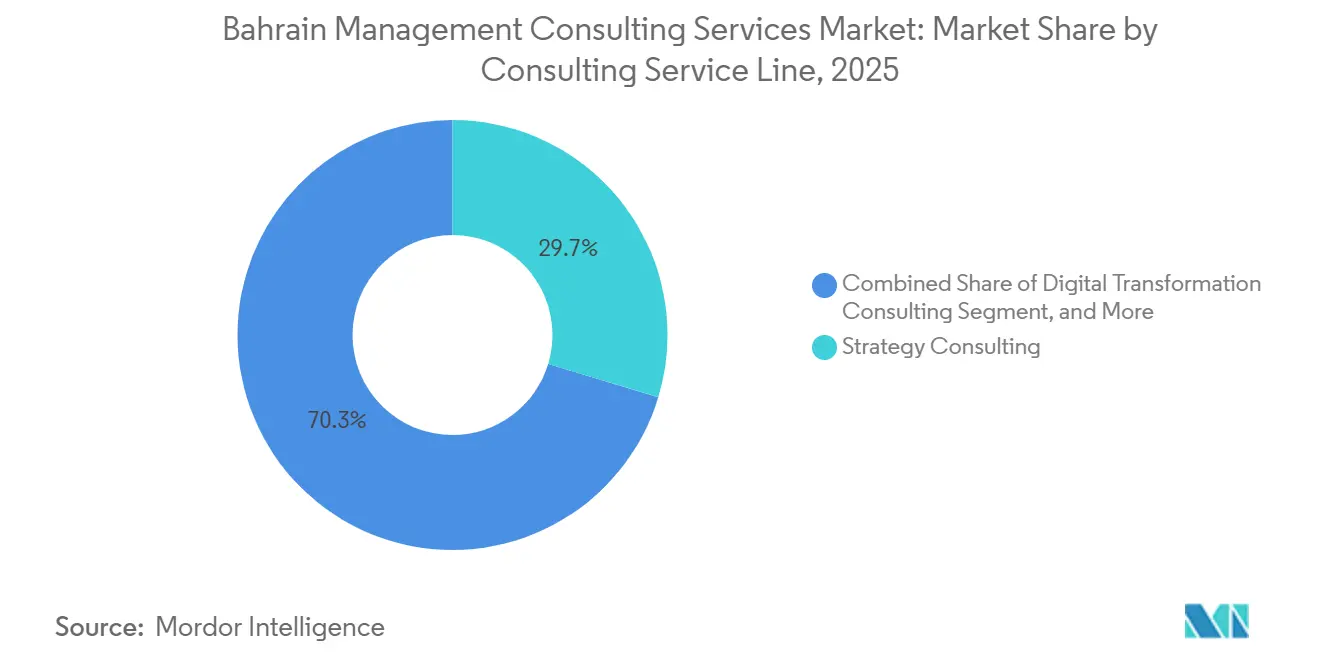

- By consulting service line, strategy consulting led with 29.68% of Bahrain management consulting services market share in 2025, while digital transformation consulting is projected to advance at a 4.53% CAGR through 2031.

- By organization size, large enterprises accounted for 61.42% of the Bahrain management consulting services market size in 2025, whereas small and medium-sized enterprises are forecast to expand at a 4.38% CAGR during 2026-2031.

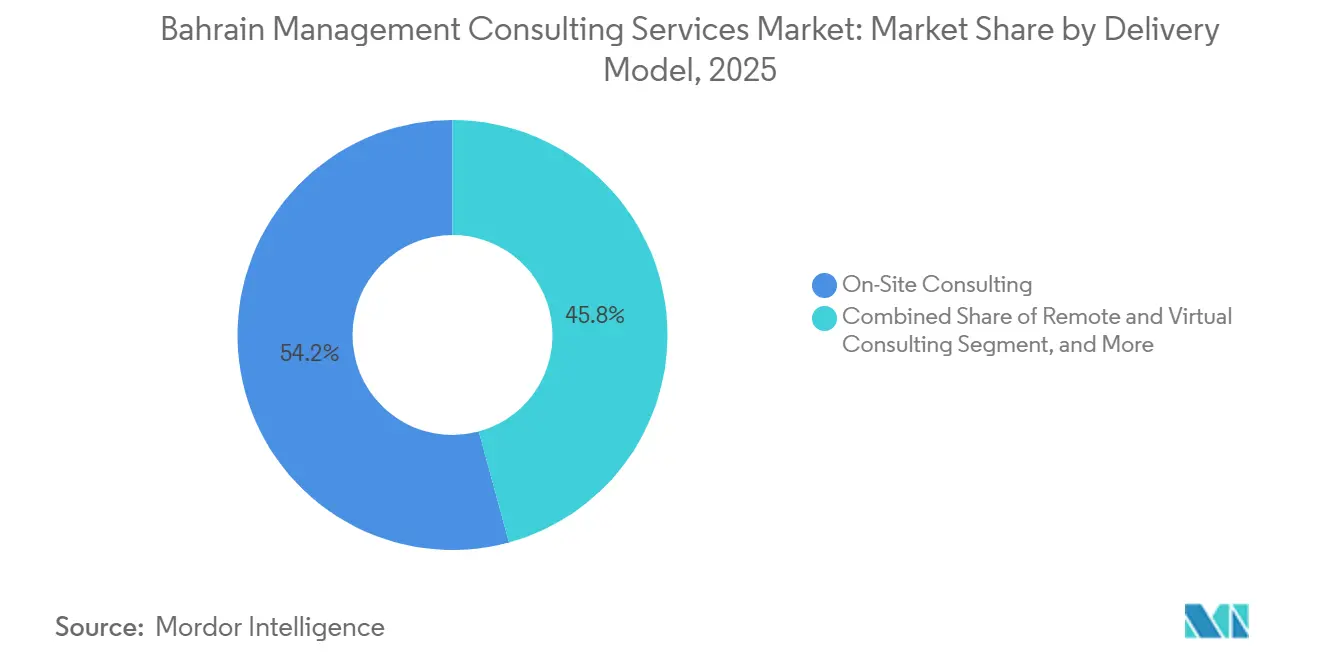

- By delivery model, on-site consulting retained 54.23% of Bahrain management consulting services market share in 2025, and remote and virtual consulting is expected to record the fastest 4.68% CAGR to 2031.

- By end user, the public sector held 25.13% of Bahrain management consulting services market size in 2025, while healthcare is poised to register the highest 4.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bahrain Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Public-Sector Spending Under Bahrain Economic Vision 2030 | +1.2% | National, concentrated in Manama and industrial zones | Medium term (2-4 years) |

| Acceleration of Digital-First Projects Across BFSI and Telecom | +1.0% | National, with spill-over to GCC cross-border mandates | Short term (≤2 years) |

| Big Four One-Stop ESG Advisory Bundles Win Rapid Traction | +0.8% | National, aligned with CBB ESG Module and Bahrain Bourse guidelines | Medium term (2-4 years) |

| Growing SME Demand for Performance-Improvement Consulting Amid VAT Compliance | +0.7% | National, particularly retail, hospitality, and light manufacturing | Short term (≤2 years) |

| Surge in Family-Business Succession Mandates Driving Strategy and HR Work | +0.4% | National, with regional influence from Saudi and Kuwaiti family offices | Long term (≥4 years) |

| Regional Sovereign Wealth Funds’ Vendor-Development Programs Favor Local Boutiques | +0.3% | National, with Mumtalakat and GCC SWF co-investment activity | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Public-Sector Spending Under Bahrain Economic Vision 2030

Government procurement continues to underpin growth in the Bahrain management consulting services market. The Tender Board awarded USD 3 billion across 1,538 contracts during the first nine months of 2025, including USD 1.1 billion for services and USD 835 million for engineering consultancy.[1]Tender Board, “Bahrain Awards Tenders Valued at USD 3 Billion in First Nine Months of 2025,” Tender Board, tenderboard.gov.bh More than 20 agencies are executing 49 initiatives under the National Digital Economy Strategy, driving a steady pipeline for program design, change management, and regulatory advisory assignments. KPMG, WSP, and Trowers and Hamlins are already embedded in Bahrain’s first 150 MW utility-scale solar project scheduled for commercial operation in 2027, illustrating how energy diversification projects translate into multiyear consulting engagements. Tamkeen’s 2026-2030 roadmap, which pledges support for 300,000 employment opportunities and BHD 920 million (USD 2.44 billion) in financing, extends advisory work in workforce planning and SME productivity improvement. Faster bid-cycle processing, 98.9% of requests resolved within 14 days in Q1 2024, reduces onboarding friction and accelerates revenue capture for consultancies active in public-sector tenders.

Acceleration of Digital-First Projects Across BFSI and Telecom

Banks and telecom operators are prioritizing digital transformation to comply with regulatory mandates and unlock operational efficiencies, generating robust demand within the Bahrain management consulting services market. The Central Bank of Bahrain’s 2025 stablecoin framework obliges license applicants to develop end-to-end AML, custody, and reserve-asset governance, fueling advisory needs in policy design and systems architecture. Islamic banking assets climbed to USD 61.7 billion by mid-2024, and institutions are deploying AI-driven onboarding and Sharia-compliant product automation that require workflow redesign and data-governance expertise.[2]Central Bank of Bahrain, “Central Bank of Bahrain Issues Framework for Regulating Stablecoin Issuance,” Central Bank of Bahrain, cbb.gov.bh Although 79% of Bahrain CEOs believe their technology landscape supports AI integration, only one-third of digital initiatives have met targets, prompting firms to seek external advisers to recover stalled projects. Accenture estimates that AI accounts for 18% of planned digital spending through 2030, channeling consulting opportunities toward productivity-lift quantification rather than isolated technology pilots. Financial-sector case studies such as GFH Financial Group’s Temenos core-banking rollout provide replicable blueprints that consultancies leverage when pitching similar digital upgrades.

Big Four One-Stop ESG Advisory Bundles Win Rapid Traction

Tightening disclosure expectations are propelling integrated sustainability mandates across the Bahrain management consulting services market. The Central Bank’s ESG Module folds climate and social metrics into capital-adequacy and risk-appetite frameworks, while the Bahrain Bourse Reporting Guide is becoming a de facto listing prerequisite. In response, Big Four firms are offering bundled services that cover scenario analysis, value-creation mapping, audit readiness, and investor communications. EY runs a global network of more than 2,500 sustainability specialists who connect ESG strategy to deal advisory, whereas KPMG Bahrain emphasizes Sharia-compliant ESG risk reviews for banks and energy companies. BDO Bahrain positions its cross-industry ESG solutions around IFRS Sustainability Standards and TCFD alignment, winning mandates in logistics and real estate. Early adopters such as Bapco Energies, which published a national transition-finance framework, demonstrate how first movers gain capital-market advantages, incentivizing additional corporates to engage advisers for end-to-end ESG roadmaps.

Growing SME Demand for Performance-Improvement Consulting Amid VAT Compliance

VAT and financing pressures are steering small and medium-sized enterprises toward structured advisory support, expanding the addressable base of the Bahrain management consulting services market. Since VAT increased to 10% in 2022, companies exceeding BHD 37,500 (USD 99,734) of annual revenue must maintain robust tax-control frameworks. Engagement data show that VAT audit support often starts at BHD 500 (USD 1,326) for pre-audit checks and rises to BHD 1,500 (USD 3,979) for full representation, indicating a clear willingness to pay for compliance certainty. Tamkeen’s latest strategy earmarks 92,000 enterprise opportunities and subsidized financing that hinges on productivity benchmarks, prompting SMEs to hire consultants for operations redesign and digital bookkeeping. Moore Bahrain reports more than 100 VAT implementation projects completed since 2000, while the Tender Board’s SME-targeted tender window, launched mid-2025, reduces entry barriers to public-sector contracts and heightens demand for bid-management advisory. Parallel upskilling initiatives that aim to train 50,000 Bahrainis in AI by 2030 further widen the market for curriculum design and workforce-planning consultancies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Bilingual (Arabic-English) Senior Consultants Inflates Project Costs | -0.6% | National, acute in financial services and public-sector advisory | Short term (≤ 2 years) |

| Intensifying Price Competition From UAE-Based Firms Servicing Bahrain Remotely | -0.5% | National, most visible in digital transformation and IT advisory | Short term (≤ 2 years) |

| Delays in Government E-Tender Payments Squeeze Consulting Cashflows | -0.3% | National, firms reliant on public-sector contracts | Medium term (2-4 years) |

| Brain-Drain as Bahraini Consultants Relocate to Saudi Giga-Projects | -0.2% | National, outflows to Riyadh and NEOM | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Bilingual (Arabic-English) Senior Consultants Inflates Project Costs

The talent gap remains the most immediate brake on the Bahrain management consulting services market. In 2025, 90% of GCC organizations cited skill shortages and 38% blamed low salary competitiveness, forcing firms to pay premiums for senior bilingual professionals.[3]Hays Middle East, “Hays Middle East Releases Hays GCC Salary Guide 2026,” Longbridge, longbridge.com PwC’s pledge to add 250 Bahraini hires to its Manama hub has produced only modest progress, underscoring the difficulty of scaling a local pipeline. High reliance on expatriates persists, with 80% of private-sector jobs held by foreign workers, and Bahrainization quotas now impose BHD 250 (USD 663) annual levies on each non-Bahraini employee. This cost burden inflates project pricing, stretches delivery timelines, and narrows profit margins, especially for compliance-heavy engagements in banking and government.

Intensifying Price Competition From UAE-Based Firms Servicing Bahrain Remotely

Remote delivery models are placing downward pressure on fee rates. Dubai-headquartered providers use lower overheads to undercut Bahrain-domiciled rivals while maintaining bilingual service teams.[4]Al Fahad IT Consulting, “Zoho Implementation and CRM Experts Saudi Arabia UAE and Bahrain,” Al Fahad IT Consulting, al-fahad.biz Employer-of-Record platforms have normalized cross-border staffing, letting boutiques test the Bahraini market before opening local entities.[5]EWS Limited, “The 2026 State of Global Remote Work: Tax, Compliance, and EOR Predictions,” EWS Limited, ews-limited.com As a result, remote and virtual consulting is forecast to log the quickest 4.68% CAGR to 2031. Bahrain clients, keen to curb costs yet sustain quality, increasingly accept hybrid structures, compelling local firms to revisit pricing models and invest in virtual collaboration infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Strategy Dominates, Digital Transformation Scales

Strategy consulting captured 29.68% of Bahrain management consulting services market share in 2025, reflecting steady demand for family-business succession planning and sovereign-fund portfolio realignment. Large cross-border transactions, such as the potential merger between National Bank of Bahrain and BBK, keep high-stakes deal advisory in focus. Digital transformation consulting, forecast to advance at 4.53% CAGR, benefits from rising adoption of AI in banking and telecom workflows. Fewer than one in three regional digital initiatives have hit performance targets, so boards now emphasize clear governance metrics and change-management roadmaps before approving new budgets.

The Bahrain management consulting services market size for operations and HR advisory continues to grow as state-owned energy majors expand refinery capacity and tighten Bahrainization quotas. Financial advisory teams are also busy with capital-structure reviews after Mumtalakat’s downgrade to “B,” heightening refinancing and creditor-negotiation needs. Risk and compliance specialists gain recurring revenue from new Central Bank operational-resilience mandates that require bi-annual penetration tests and one-hour incident reporting.

By Organization Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises accounted for 61.42% of Bahrain management consulting services market size in 2025, driven by continuous compliance cycles in banking and energy. GFH Financial Group alone held assets of USD 12.20 billion and relies on constant advisory input for digital core-banking upgrades and Sharia structuring. State-owned Bapco Energies, overseeing upstream to LNG logistics, engages multidisciplinary teams for project finance and carbon-transition roadmaps.

SMEs are projected to post a 4.38% CAGR through 2031. Tamkeen’s new strategy earmarks 92,000 enterprise opportunities and links subsidized loans to measurable productivity gains, prompting smaller firms to engage consultants for VAT readiness, digital bookkeeping, and procurement capability building. The Tender Board’s SME-only tender windows and hotline further level the playing field, bringing fresh advisory revenue to boutique consultancies focused on bid preparation.

By Delivery Model: On-Site Remains Primary, Remote Gains Traction

On-site engagements still held 54.23% of Bahrain management consulting services market share in 2025 as regulators and boards prefer physical presence for sensitive governance work. PwC’s expanded Manama hub underscores client appetite for in-country senior-partner access. Complex energy projects, such as the 150 MW Bilaj Al Jazayer solar farm, also demand on-the-ground oversight during execution phases.

Remote consulting, however, is the fastest-growing format. Cross-border video workshops, cloud-based data rooms, and GCC-wide bilingual delivery teams reduce travel costs and enhance time-to-value, particularly for mid-market clients balancing budget constraints with transformation urgency. Hybrid models that blend strategy kick-offs on site with remote analytics and progress monitoring are becoming the norm across the Bahrain management consulting services market.

By End-User Industry: Public Sector Commands Spend, Healthcare Outpaces Growth

Public-sector entities retained 25.13% of Bahrain management consulting services market size in 2025. The USD 3 billion tender pipeline covering digital government, SME enablement, and renewable-energy initiatives assures sustained consulting demand. Ministries also team up with global advisers on AI-driven sustainability programs that can unlock regional investment inflows.

Healthcare is forecast to rise at 4.46% CAGR, lifted by National Health Regulatory Authority rules that push clinics to adopt digital patient-acquisition and operations-management systems. Al Farabi Advisory claims its AI tools generate 25-40% revenue lifts within 12 months for multi-specialty centers. Banking, insurance, telecom, energy, and manufacturing keep engaging advisers for ESG, cyber-resilience, and efficiency drives, ensuring a diversified demand base.

Geography Analysis

Bahrain’s consulting activity is concentrated in Manama, home to most Big Four offices, regulators, and financial institutions. Financial services contribute roughly 17% of GDP while oil and gas add 16%, depicting a diversified economy that supports steady advisory requirements. Foreign direct investment reached USD 1.8 billion in 2024, with Saudi and UAE inflows spurring cross-border transaction work and joint-venture structuring.

Special economic zones, including Bahrain International Investment Park and Bahrain Logistics Zone, grant 100% foreign ownership and duty-free GCC access, attracting manufacturing and logistics players that need operational advisory and Bahrainization compliance support. The United States Trade Zone near Khalifa bin Salman Port finished phase-one infrastructure in late 2024, opening a consulting niche around U.S. supply-chain optimization and market-entry planning.

Regional talent flows shape the market. Saudi gigaprojects lure seasoned Bahraini consultants with premium wages, deepening local capacity shortages. Meanwhile, UAE-based boutiques leverage remote models to serve Bahrain, triggering fee compression yet raising delivery speed expectations. These push-and-pull forces underscore why local firms are investing in remote-delivery toolkits and cross-border collaboration protocols.

Competitive Landscape

The Bahrain management consulting services market is moderately fragmented. Big Four networks secure large public-sector and bank mandates, global strategy houses win complex M&A and transformation projects, and specialized boutiques fill sector-niche gaps. PwC’s April 2025 hub expansion targets 250 national hires to reinforce compliance and ESG capabilities. McKinsey’s role in the National Bank of Bahrain-BBK merger talks attests to ongoing appetite for top-tier transaction advice. Bain’s AI-powered sustainability prototypes for the Ministry of Sustainable Development show how data-science muscle differentiates bidders on public-private initiatives.

Local disruptors are emerging. SGC Management Consultants positions itself as an independent governance specialist, Vertical Integration Consultancy leverages free Balanced Scorecard training to capture SMB leads, and Al Farabi Advisory integrates AI modules into healthcare operations, boasting rapid payback period. As ESG and AI governance workloads expand, depth of sector knowledge and bilingual delivery capacity will separate winners from followers.

Bahrain Management Consulting Services Industry Leaders

PwC Middle East

KPMG Bahrain

Deloitte Middle East

EY Bahrain

McKinsey and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: McKinsey appointed joint adviser by National Bank of Bahrain and BBK for a potential merger.

- February 2026: Fitch downgrades Mumtalakat to “B,” increasing restructuring advisory demand.

- January 2026: TNP Consultants opens Riyadh and Manama offices to deepen GCC presence.

- December 2025: Bain and Ministry of Sustainable Development launch AI-powered SME sustainability tool.

Bahrain Management Consulting Services Market Report Scope

The Bahrain Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current value of Bahrain's management consulting services market?

The Bahrain management consulting services market size is USD 1.27 billion for 2025 and is projected at USD 1.33 billion in 2026.

Which consulting service line is growing fastest in Bahrain?

Digital transformation consulting is expected to expand at a 4.53% CAGR through 2031, the highest among service lines.

Why are SMEs increasing their spending on consulting?

Higher VAT compliance demands and Tamkeen's subsidized financing programs push SMEs to seek professional advice on operations, tax, and digital bookkeeping.

How are remote delivery models affecting pricing?

UAE-based firms deliver projects virtually into Bahrain, reducing overhead and placing downward pressure on traditional on-site fee structures.

Which end-user industry will post the quickest growth?

Healthcare is projected to grow at a 4.46% CAGR through 2031 due to digital patient-acquisition mandates from the National Health Regulatory Authority.

What factors limit market expansion?

A shortage of bilingual senior consultants and rising competition from cross-border remote providers are the primary restraints.

Page last updated on: