South Africa Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

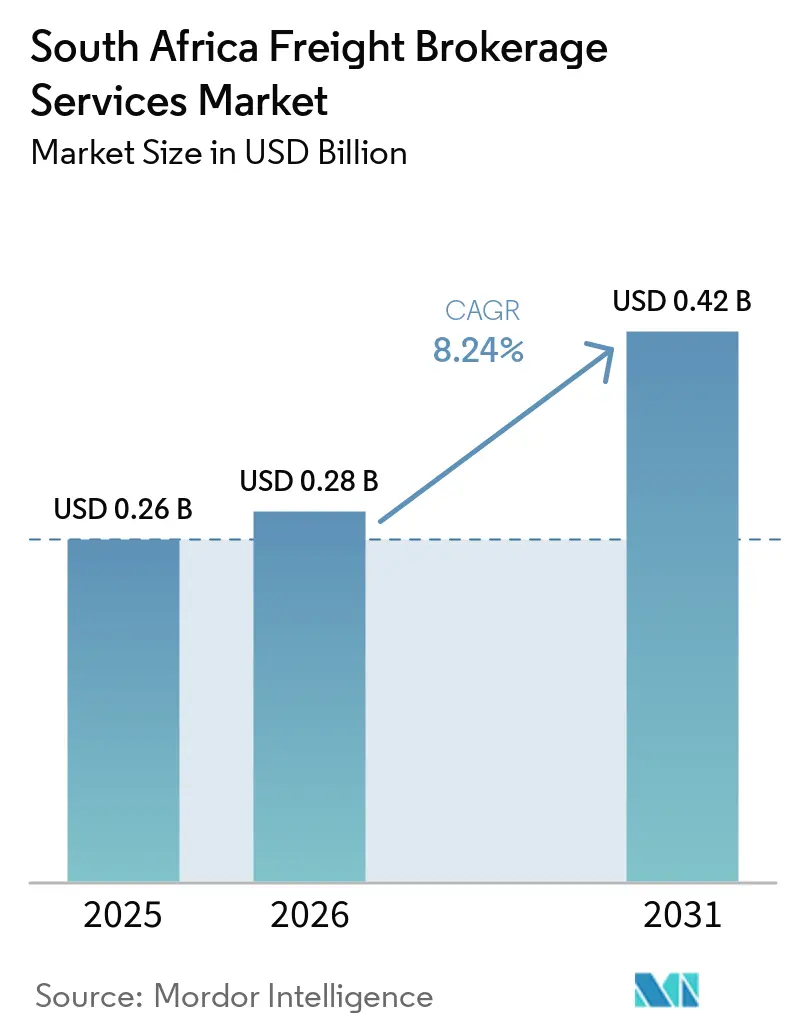

| Base Year Market Size (2025) | USD 0.26 Billion |

| Market Size (2026) | USD 0.28 Billion |

| Market Size (2031) | USD 0.42 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Freight Brokerage Services Market Analysis by Mordor Intelligence

The South Africa freight brokerage services market size was valued at USD 0.26 billion in 2025 and estimated to grow from USD 0.28 billion in 2026 to reach USD 0.42 billion by 2031, at a CAGR of 8.24% during the forecast period (2026-2031). This expansion reflects rapid digitalization, fresh rail-slot access for private operators, and strict electronic documentation mandates that collectively reshape how intermediaries create and capture value. Nationwide adoption of electronic consignment notes reduces border dwell times, while green-finance incentives accelerate an early shift toward battery-electric trucks in urban areas. Freight brokers that couple rail and road capacity now command premium pricing on long-haul export corridors because rail economics cut 30-40% off road costs. At the same time, AfCFTA-driven tariff phasedowns stimulate cross-border less-than-truckload (LTL) flows, giving consolidators a new profit pool. Brokers that fail to digitize documentation or hedge fuel and currency volatility face thinning margins as carbon-linked diesel surcharges and persistent rand swings heighten operating risk.[1]Source: Republic of South Africa Department of Transport, “National Freight Logistics Strategy,” transport.gov.za

Key Report Takeaways

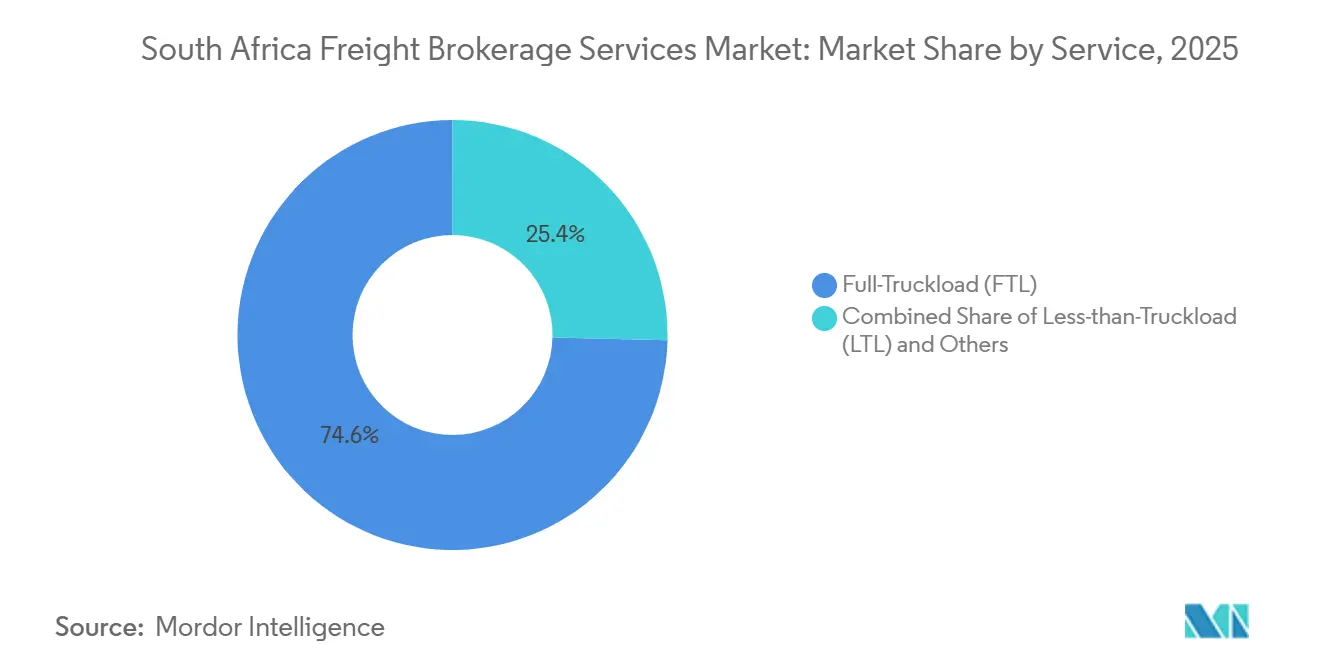

- By service, full-truckload (FTL) transport led with 74.62% of the South Africa freight brokerage services market share in 2025; LTL consolidation is projected to advance at an 11.25% CAGR through 2031.

- By equipment type, dry vans accounted for 41.81% share of the South Africa freight brokerage services market size in 2025, while refrigerated vans are set to expand at an 11.81% CAGR.

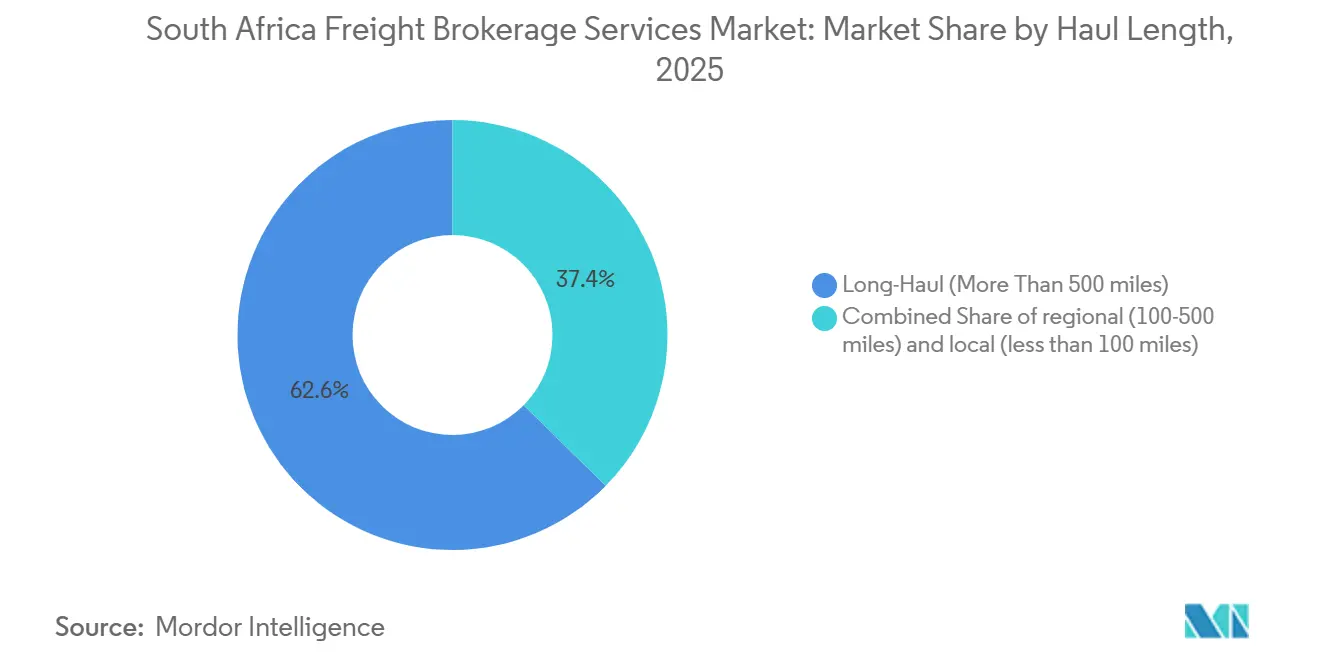

- By haul length, long-haul routes captured 64.48% share in 2025; local hauls under 100 miles are on track for a 13.98% CAGR.

- By business model, traditional brokerage held 84.09% share in 2025, whereas digital freight platforms are forecast to surge at a 27.77% CAGR.

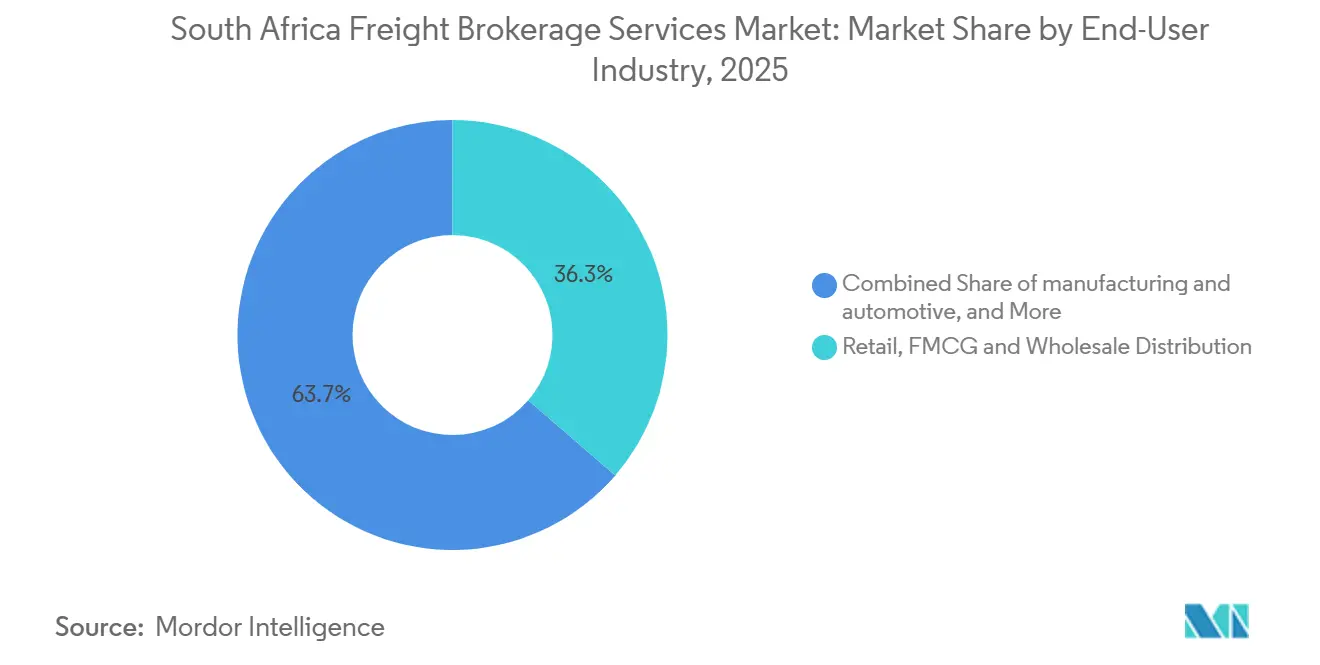

- By end-user industry, retail and fast-moving consumer goods (FMCG) commanded 36.33% of 2025 revenue; e-commerce and third-party fulfillment led growth at a 22.25% CAGR.

- By customer size, large enterprises contributed 73.94% in 2025, yet small businesses with under USD 10 million revenue will climb at a 16.57% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide freight brokerage services market outlook captures this forward trajectory.

South Africa Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Private-sector rail-slot public-private partnerships (PPPs) unleashing intermodal brokerage capacity | +1.9% | National, focused on Gauteng–KwaZulu-Natal–Western Cape corridors | Medium term (2-4 years) |

| Rapid electrification of truck fleets spurred by green-finance tax rebates | +1.6% | Urban centers such as Johannesburg, Cape Town, Durban, and Pretoria | Short term (≤ 2 years) |

| Nationwide eCMR and e-Waybill mandate enabling real-time load visibility | +1.3% | National, early adoption in Gauteng and Western Cape | Short term (≤ 2 years) |

| AfCFTA tariff phase-down boosting South Africa-origin regional LTL corridors | +1.1% | Border provinces such as Limpopo, Mpumalanga, and Northwest | Medium term (2-4 years) |

| cGMP vaccine and biologics build-out raising temperature-validated lanes | +0.8% | Pharmaceutical hubs such as Gauteng, Western Cape | Long term (≥ 4 years) |

| Automotive SEZ export corridors driving just-in-sequence parts flows | +0.7% | Eastern Cape (Coega, East London) and Gauteng | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Private-Sector Rail-Slot PPPs Unleashing Intermodal Brokerage Capacity

South Africa’s rail liberalization plan lets private operators bid for track slots, finally giving brokers a cost-efficient alternative to road-only haulage. Early concessions on the Gauteng-to-port corridors allow intermodal specialists to shave 30-40% off per-ton costs on distances beyond 500 km. Brokers that integrate rail line-haul with road first- and last-mile delivery are now winning export contracts in mining and agriculture because shippers gain both savings and lower carbon footprints. Transparent, non-discriminatory slot pricing further reduces information gaps that once favored the incumbent rail operator. As private capacity scales, intermodal margins are expected to widen, reinforcing the projected uplift in the South Africa freight brokerage services market.

Rapid Electrification of Truck Fleets Spurred by Green-Finance Tax Rebates

While major cities like Johannesburg, Cape Town, and Durban have committed to future clean air frameworks under the C40 Cities declaration, active low-emission zones have not yet been rolled out, meaning regulatory pushes toward battery-electric trucks remain in the planning phases. While imported medium and heavy commercial trucks still face a 20% duty, the 150% investment allowance for local electric vehicle (EV) production, effective March 2026, makes domestic fleets more affordable. Development-bank green-finance lines further cut borrowing costs. Brokers that secure early EV capacity command premium urban-delivery contracts from multinational brands that rate suppliers on emissions. Short-range applications match current battery limits, so near-term gains concentrate on local routes. Over time, wider EV adoption cushions brokers against carbon-linked diesel surcharges, supporting sustained growth in the South Africa freight brokerage services market.[2]National Treasury, “Budget Review 2026,” treasury.gov.za

Nationwide eCMR / e-Waybill Mandate Enabling Real-Time Load Visibility

Digitized customs declarations and enhanced Electronic Data Interchange (EDI) compliance became strictly enforced under the SARS Registration, Licensing, and Accreditation (RLA) system in 2025, linking broker transport-management systems directly to South African Revenue Service customs platforms. Automated clearance slashes border dwell times and reduces documentation errors. Furthermore, API integrations linking private fleet telematics to these automated customs workflows provide real-time location tracking that helps deter cargo theft on high-risk corridors. Larger brokers rapidly deployed application-program-interface (API) connectors, trimming administrative labor and billing cycles. Smaller, manual operators now face consolidation pressure because compliance costs rise while their service speed lags. This regulatory push, therefore, deepens digital penetration and lifts the overall South Africa freight brokerage services market size.[3]South African Revenue Service, “eCMR Implementation Guidelines,” sars.gov.za

AfCFTA Tariff Phase-Down Boosting South Africa-Origin Regional LTL Corridors

While exports to immediate SACU neighbors like Botswana and Namibia are already duty-free, the broader AfCFTA implementation focuses on reducing non-tariff barriers and phasing down tariffs for South African industrial exports to broader, non-SADC continental markets. Shippers are switching from infrequent full-truckload (FTL) moves to regular smaller batches, freeing working capital and favoring LTL consolidators. Driven by SME digitization and retail supply chain optimization rather than new tariffs, brokers equipped with modern cross-border documentation tools are increasingly aggregating Gauteng-origin freight bound for Botswana, Namibia, and Zimbabwe. Furthermore, AfCFTA's push to harmonize continental customs processes aims to gradually reduce specialized-broker barriers, intensifying competition yet expanding revenue pools across the South Africa freight brokerage services market.[4]African Union Commission, “AfCFTA Tariff Schedules,” au.int

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid load-shedding causing warehouse and reefer downtime surcharges | -1.4% | National, severe in Gauteng, Western Cape, KwaZulu-Natal | Short term (≤ 2 years) |

| Carbon-tax Phase 2 compliance inflating diesel fleet operating costs | -1.1% | National, heavier effect on long-haul corridors | Medium term (2-4 years) |

| Rand exchange-rate volatility complicating contract freight pricing | -0.9% | Import-export corridors—Gauteng-Durban, Gauteng-Cape Town | Short term (≤ 2 years) |

| Surge in ransomware attacks on transport-management platforms | -0.6% | National, concentrated among digital brokers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Load-Shedding Causing Warehouse and Reefer Downtime Surcharges

Unplanned power cuts force warehouses and refrigerated fleets to burn costly diesel in backup generators, adding USD 0.10-0.15 per mile on temperature-controlled lanes. Freight brokers often absorb these surcharges to keep contract rates predictable, squeezing margins on pharmaceutical and fresh-produce runs. Solar and battery retrofits are underway, but capital intensity favors large facilities, leaving smaller depots exposed. Until grid reliability improves, load-shedding remains a top risk restraining profitability within the South Africa freight brokerage services market.

Carbon-Tax Phase 2 Compliance Inflating Diesel Fleet Operating Costs

The carbon levy jumps from USD 7.9 per metric-ton CO₂ in 2024 to USD 8.7 in 2026, directly lifting diesel prices by nearly USD 0.03 per liter. Carriers with older Euro 3-4 engines pass costs upstream, and brokers must decide whether to raise shipper rates or see profit erode. Long-haul corridors feel the most pain because alternative powertrains are not yet range-viable. Medium-term, brokers with early access to low-emission equipment gain a pricing edge, but near-term carbon-cost uncertainty drags down the South Africa freight brokerage services market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Consolidation Gains Traction

The full-truckload segment dominated 2025 with 74.62% of revenue, driven by bulk mining exports and large agricultural consignments that still justify entire vehicle hire. Nonetheless, less-than-truckload services are accelerating at an 11.25% CAGR through 2031 as AfCFTA tariff relief encourages smaller, more frequent cross-border orders. Digital marketplaces pool fragmented loads into consolidated trucks, trimming empty miles and raising asset utilization. Broker apps that provide customs pre-clearance and real-time status updates are winning contracts from SMEs keen to expand regionally without investing in logistics staff. This shift steadily increases the weight of LTL within the South Africa freight brokerage services market.

Over the next five years, pharmaceuticals and fast-moving consumer goods will propel temperature-controlled LTL demand, where brokers secure premium yields by guaranteeing GDP compliance. Traditional FTL players are responding with zone-pricing and shared-truck solutions, but technology-led specialists remain ahead on dynamic routing and tariff automation. As these features spread, margin gaps will narrow, yet the superior growth trajectory of LTL is set to stay a central theme across the South Africa freight brokerage services industry.

By Equipment Type: Refrigerated Capacity Tightens

Dry vans retained the largest 41.81% slice of 2025 revenue because they handle the widest cargo mix from packaged foods to electronics. The fastest-growing refrigerated van category is forecast to clock an 11.81% CAGR on the back of vaccine, biologics, and high-value produce logistics. Strict GDP and Hazard Analysis and Critical Control Point (HACCP) standards require sensors and digitally logged temperature trails, restricting qualified supply and enabling brokers who manage certified fleets to secure superior margins. These specialized fleets are expanding, yet diesel-generator costs during load-shedding episodes compress profitability.

Heavy-haul flatbeds and tankers occupy niche roles in construction and chemicals, but their cyclical volumes limit growth relative to reefer assets. Investments in solar-assisted refrigeration units and lithium-battery telematics should cut fuel-burning costs by 8-10% from 2027 onward, giving early adopters a competitive edge. Consequently, refrigerated equipment will exert an outsized influence on premium yield within the broader South Africa freight brokerage services market.

By Haul Length: Local Routes Surge on Urban Density

Long-haul lanes exceeding 500 miles ended 2025 with a commanding 64.48% share, a reflection of inland mines and farms feeding coastal export ports. Yet local hauls below 100 miles are projected to rise fastest at a 13.98% CAGR as e-commerce same-day delivery and automotive SEZ shuttle runs multiply. Battery-electric trucks fit these city-centric routes perfectly because they can recharge overnight and avoid carbon levies that hammer diesel units. Brokers specializing in tight urban radii are bundling pick-ups and drops into milk-runs that cut dwelling time and uplift truck turns per day.

Mid-range 100–500-mile corridors balance distance and flexibility and may face modal shift once private rail slots mature. Long-haul providers, meanwhile, look to intermodal contracts that blend rail cost efficiencies with road reach, protecting their volume stronghold. Nevertheless, local urban expansion is likely to add both density and frequency, cementing city routes as a growth engine inside the South Africa freight brokerage services market.

By Business Model: Digital Platforms Disrupt Traditional Structures

Conventional brokerage still held 84.09% revenue leadership in 2025, leveraging deep carrier relationships and problem-solving skills for complex loads. Digital platforms, however, will post a blistering 27.77% CAGR through 2031 as real-time pricing and instant capacity booking resonate with procurement teams chasing transparency. API integrations with customs and transport-management software remove manual paperwork, shaving overhead and error rates. Platform brokers also attract small shippers that previously fell below minimum volume thresholds.

Hybrid asset-light models, where brokers own select equipment, are emerging to guarantee capacity on peak lanes. Agent-based networks help expand territorial reach without heavy capex, but managing brand uniformity across independent contractors remains a challenge. While incumbents invest in their own platforms, first-mover apps have set user-experience standards, ensuring digital models continue carving share inside the South Africa freight brokerage services market.

By End-User Industry: E-Commerce Outpaces Traditional Retail

Retail, FMCG, and wholesale distribution finished 2025 at 36.33% of revenue thanks to established store replenishment cycles and nationwide branch footprints. E-commerce and 3PL fulfillment, however, will accelerate at a 22.25% CAGR as online penetration surpasses 7% of retail sales by 2031. Multichannel merchants now outsource fulfillment to specialist warehouses near major metros, requiring brokers agile enough to manage small, time-definite shipments.

Automotive and manufacturing lanes command premium rates because component flows penalize line downtime. Pharmaceuticals layer in temperature-control and compliance fees, enhancing yield. Agriculture, while seasonal, lifts volumes in export harvest months, balancing capacity utilization. As digital shopping keeps climbing, brokers tuned to parcel-compatible LTL and last-mile demands will shape revenue mix shifts within the South Africa freight brokerage services market.

By Customer Size: SME Digitization Accelerates Access

Large enterprises dominated 2025 with a 73.94% contribution, underpinned by multi-year contracts and volume guarantees that anchor broker cash flows. Yet the under USD 10 million revenue SME cohort is forecast to rise at 16.57% CAGR because digital freight apps remove legacy barriers such as credit checks and relationship prerequisites. Instant quotes and transparent tracking let small firms ship ad hoc without committing to annual volumes.

Mid-market shippers, typically lacking in-house logistics teams, represent an underserved pool ripe for managed-transport solutions that bundle freight brokerage, customs, and warehousing. As compliance rules around eCMR become more user-friendly, SMEs gain further autonomy, driving transaction counts higher. Consequently, customer diversification bolsters resilience within the South Africa freight brokerage services industry while supporting inclusive market growth.

Geography Analysis

Gauteng, home to Johannesburg and Pretoria, anchors the largest slice of the South Africa freight brokerage services market, benefiting from its industrial concentration, air-cargo hubs, and road-rail interchanges linking inland production to Durban and Cape Town ports. Premium automotive and pharmaceutical accounts headquartered here demand high-spec just-in-sequence and GDP-compliant transport, lifting brokerage yields above national averages. Grid constraints remain acute, yet significant rooftop solar uptake is beginning to stabilize warehouse uptime, fostering confidence among global shippers.

KwaZulu-Natal ranks second thanks to Durban’s container port, handling roughly 60% of the nation’s container throughput, which fuels steady long-haul transfers along the N3 corridor to Gauteng. Infrastructure bottlenecks and periodic port congestion have pushed forwarders to explore private-sector rail slots, with financial models projecting significant cost savings on heavy, non-urgent freight once private rail operations officially commence in April 2027. Broader compliance with SARS digitized customs declarations (EDI) has shortened customs clearance windows at the Mozambique and Eswatini borders, nurturing regional LTL growth and expanding the South Africa freight brokerage services market size.

Western Cape emerges as the fastest-growing provincial market with a projected CAGR topping 10% through 2031, spurred by agricultural exports, wine logistics, and burgeoning vaccine fill-finish operations around Cape Town. Seasonality historically hampered capacity planning, but predictive analytics are now aligning reefer supply with harvest peaks. Solar-backed cold-storage additions also mitigate power interruptions, a key selling point for pharmaceutical producers pivoting to high-mix, lower-volume biologics. Together, these provincial dynamics deepen geographic diversification and fortify national momentum.

The freight brokerage services market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America and Europe. This is complemented by country-specific insights for Canada, Poland, Germany, Spain, Spain, Netherlands, and Saudi Arabia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Competition in the South Africa freight brokerage services market remains moderately fragmented; the top five players jointly command under 40% of revenue, leaving room for specialists and start-ups. Bidvest International Logistics, Grindrod Logistics, and DSV lead on scale, but fast-growing digital players such as Freightify and Toll Group’s platform have raised customer expectations for instant quotes and end-to-end visibility. Incumbents answer with acquisitions such as Commercial Cold Holdings’ (CCH) aggressive 2024–2025 absorption of operators like CCS Logistics, which heavily consolidated the regional temperature-controlled market, while Grindrod’s intermodal push leverages new rail slots on the Gauteng-Durban line.

Strategic priorities now center on API ecosystems. Kuehne+Nagel’s early integration with the SARS modernized Electronic Data Interchange (EDI) system successfully streamlined customs clearance on pilot lanes, winning just-in-time electronics contracts. OneLogix is actively structuring future intermodal rail partnerships, promising similar gains for bulk miners seeking carbon cuts once private rail operations commence in 2027. Smaller brokers pursue vertical niches. City Logistics embeds temperature sensors for fish exports, whereas SEZ-focused specialists curate micro-fleets timed to automotive takt cycles, charging penalty-backed premiums.

Cybersecurity has become a differentiator after several high-profile ransomware shutdowns. Global players like Geodis deployed zero-trust architectures and real-time backup replication, marketing high-availability platform uptime that swayed risk-averse pharmaceutical shippers. Environmental, social, and governance (ESG) credentials also influence bid wins; major regional players like Bidvest International Logistics leverage their ISO 14001 certifications to gain an edge in corporate tenders where emissions scorecards account for up to 15% of evaluation weightings. With technology, compliance, and sustainability now intertwined, agility defines staying power in the South Africa freight brokerage services market.

South Africa Freight Brokerage Services Industry Leaders

DSV

Bidvest International Logistics

Imperial Logistics (DP World)

DHL Group

Kuehne+Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DHL Group received unconditional approval from the South African Competition Commission to acquire Vital Distribution Solutions, as well as Vital Fleet and Staffing Logistics. This strategic move significantly expands DHL’s domestic brokerage and contract logistics capabilities, adding a massive fleet and a network of specialized warehouses. The partnership integrates Vital’s deep expertise in the FMCG and retail sectors with DHL’s global network, creating a combined entity capable of providing end-to-end "local-to-global" supply chain solutions.

- February 2026: Kuehne+Nagel issued direct operational mandates to its global network, including its South African freight forwarding divisions, to immediately review tariff classifications, validate origin data, and prepare Automated Commercial Environment (ACE) filing teams. This is to ensure shippers avoid margin compression and penalties under the new multi-tiered international tariff frameworks.

- November 2025: DSV officially launched its first operational 8-ton electric truck at its South African headquarters in Gauteng. This initiative is part of an expanded sustainability roadmap that includes adding several new Volvo electric tractors to its South African fleet by the end of 2025 and into early 2026. The move aligns with DSV’s broader global strategy to integrate heavy electric commercial vehicles into urban operations alongside investments in on-site solar and Battery Energy Storage Systems (BESS).

- November 2025: Bidvest International Logistics launched its 2026 Youth Employment Service (YES) Program. The initiative provides unemployed South African youth with a comprehensive 12-month paid training program, delivering practical workplace experience across BIL’s major port and airport locations. The curriculum focuses on air and sea freight handling, road transport, customs clearance, and warehouse management.

South Africa Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid & Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing & Automotive |

| Construction & Infrastructure Projects |

| Oil, Gas, Mining & Chemicals |

| Agriculture & Food / Beverage |

| Retail, FMCG & Wholesale Distribution |

| Healthcare & Pharmaceuticals |

| E-commerce & 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid & Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing & Automotive |

| Construction & Infrastructure Projects | |

| Oil, Gas, Mining & Chemicals | |

| Agriculture & Food / Beverage | |

| Retail, FMCG & Wholesale Distribution | |

| Healthcare & Pharmaceuticals | |

| E-commerce & 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How fast is digitization expanding across South Africa freight brokerage?

Digital platforms are forecast to post a 27.77% CAGR through 2031, far outpacing traditional models as shippers demand instant pricing and e-documentation.

What is driving demand for refrigerated transport capacity?

Investments in biologics and vaccine manufacturing, plus rising fresh-produce exports, are propelling refrigerated vans at an 11.81% CAGR.

How do AfCFTA tariffs influence brokerage opportunities?

Tariff reductions of up to 15 percentage points are shifting exporters toward smaller, more frequent LTL shipments, boosting cross-border consolidator revenue.

Which province offers the fastest growth potential?

Western Cape leads with a projected double-digit CAGR due to agricultural exports and new pharma fill-finish facilities near Cape Town.

How will carbon-tax hikes affect freight rates?

The tax rises to about USD 8.7 per ton CO₂ in 2026, increasing diesel costs and encouraging brokers to adopt low-emission trucks or rail alternatives.

Are SMEs gaining better access to brokerage services?

Yes, transparent digital platforms remove volume thresholds, letting firms with revenue under USD 10 million grow shipments at a 16.57% CAGR.

Page last updated on: