Mexico Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

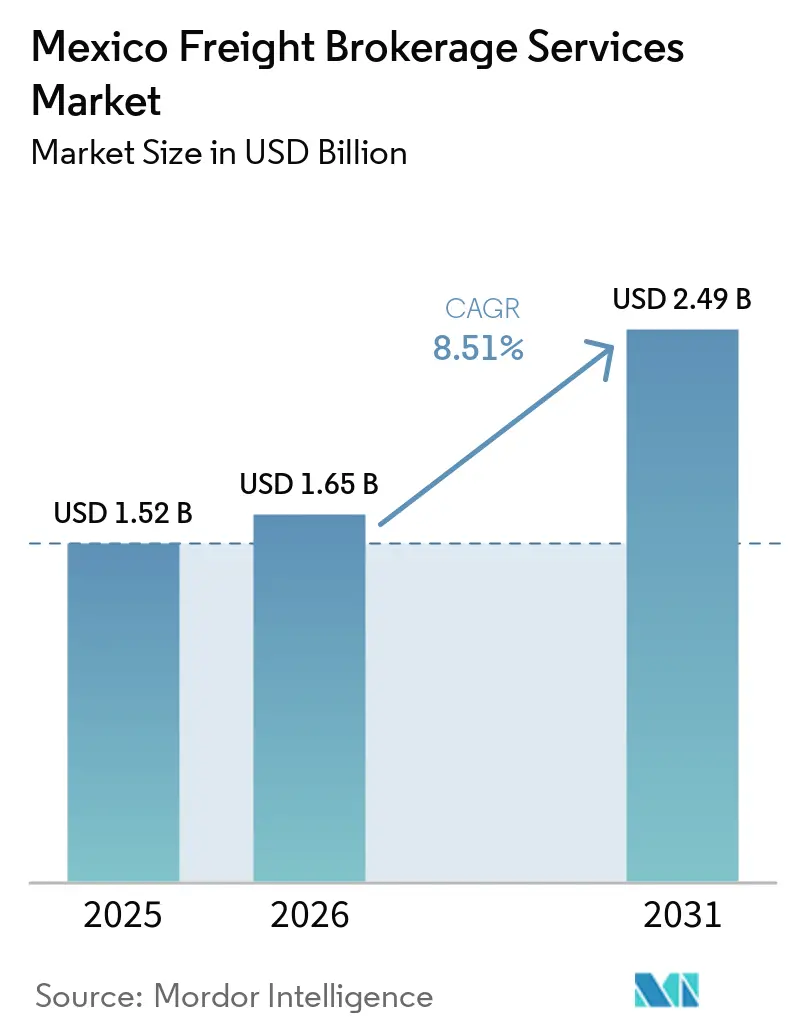

| Base Year Market Size (2025) | USD 1.52 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Freight Brokerage Services Market Analysis by Mordor Intelligence

The Mexico freight brokerage services market size is projected to expand from USD 1.52 billion in 2025 and USD 1.65 billion in 2026 to USD 2.49 billion by 2031, registering a CAGR of 8.51% between 2026 and 2031.

Mexico’s evolving consumer base, its deepening e-commerce penetration, and federally backed infrastructure upgrades are steering freight flows away from a purely maquiladora export model toward a mixed domestic-consumption and nearshoring profile. Digital customs modernization and ESG-linked procurement policies further differentiate the Mexico freight brokerage services market from peers, rewarding intermediaries that invest in API connectivity, carrier compliance tools, and carbon-tracking dashboards. E-commerce-driven Less-than-Truckload (LTL) volumes, the build-out of cold-chain capacity for agri-food exports, and new trade corridors anchored by the Interoceanic Corridor are reshaping lane densities and pricing dynamics. Although diesel price swings and tighter subcontractor audits compress margins, the Mexico freight brokerage services market continues to attract strategic investment from traditional brokers, digital start-ups, and asset-based hybrids seeking scale efficiencies.

Key Report Takeaways

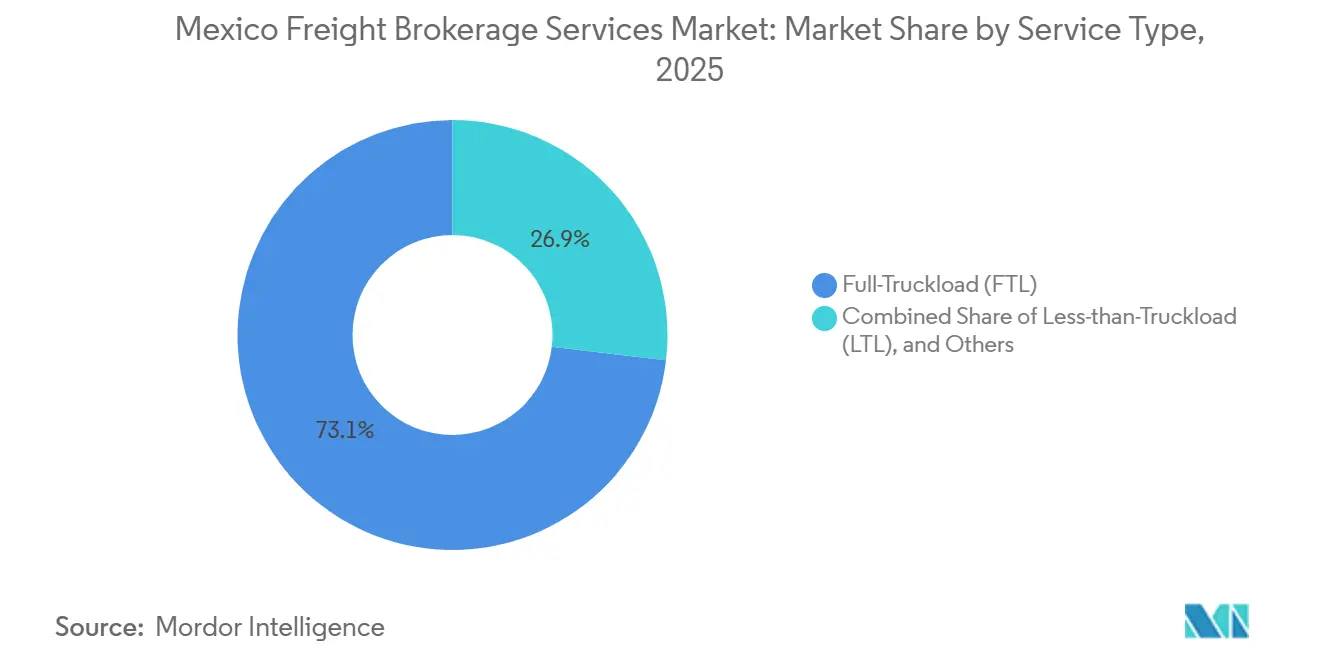

- By service, Full-Truckload operations commanded 73.12% of the Mexico freight brokerage services market share in 2025, whereas Less-than-Truckload is advancing at a 10.26% CAGR through 2031.

- By equipment, dry vans held 46.40% of the Mexico freight brokerage services market size in 2025, while refrigerated vans are forecast to expand at 10.57% CAGR through 2031.

- By haul length, long-haul routes exceeded a 63.81% share of the Mexico freight brokerage services market size in 2025; local routes under 100 miles posted the fastest 12.60% CAGR to 2031.

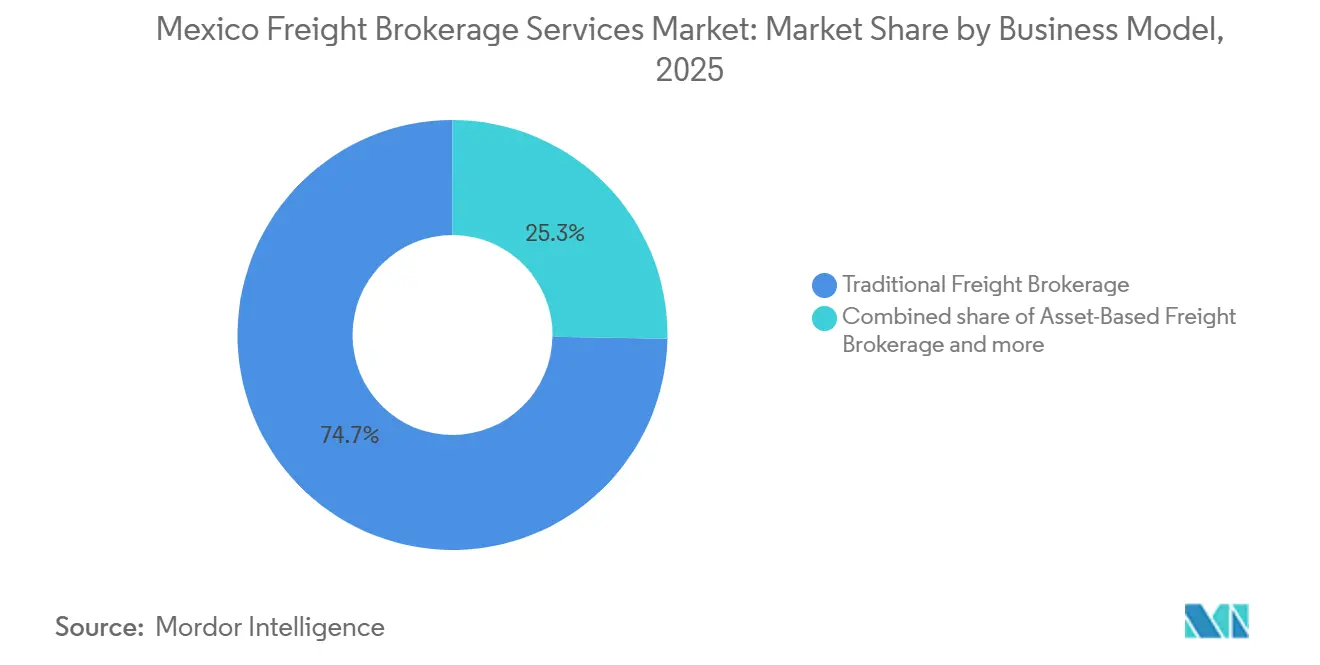

- By business model, traditional brokers retained 74.71% market share in 2025, yet digital platforms are the fastest-growing at a 28.02% CAGR.

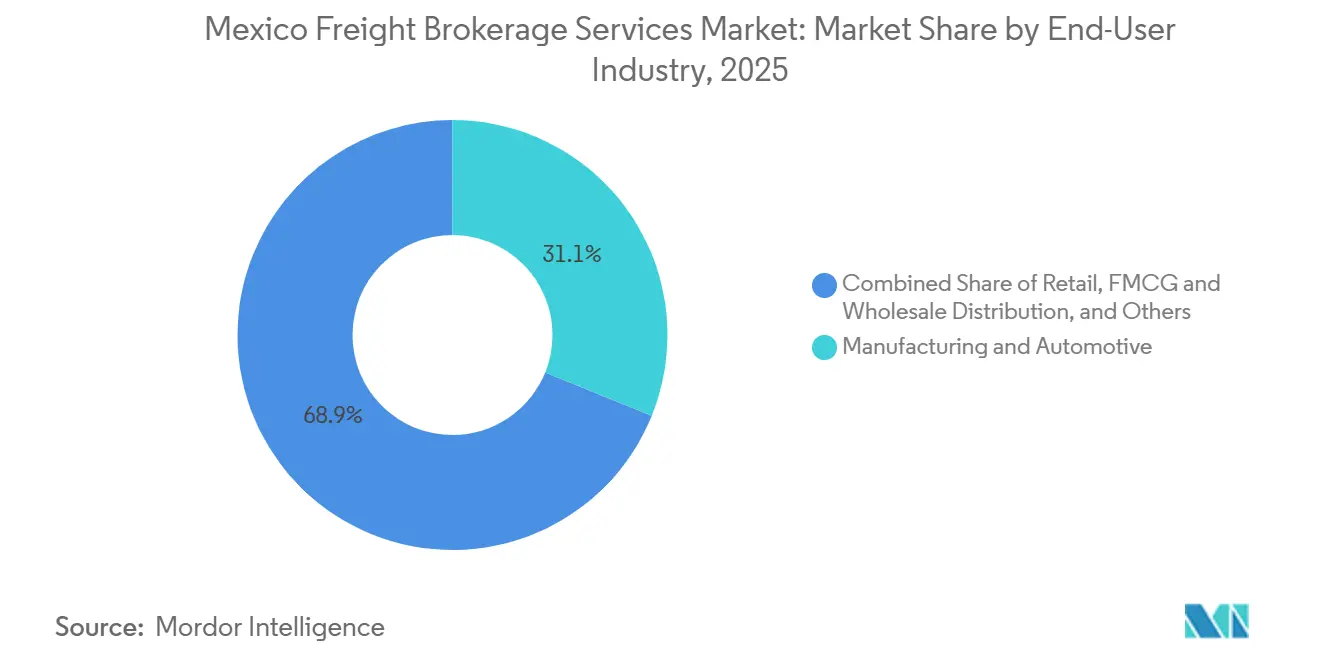

- By end-user, manufacturing and automotive captured 31.13% of the Mexico freight brokerage services market share in 2025; e-commerce and 3PL fulfillment are growing at a 21.10% CAGR.

- By customer size, large enterprises contributed 68.13% revenue in 2025, whereas small businesses under USD 10 million in turnover climb at 15.57% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with Mexico being one of the contributors. Our global freight brokerage services market size represents that cumulative total.

Mexico Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive domestic B2C e-commerce fueling LTL brokerage volumes | +2.3% | National, metro and emerging middle-class regions | Short term (≤ 2 years) |

| Rapid cold-chain capacity build-out for agri-food exports | +1.7% | Pacific coast states, Michoacan, Jalisco | Medium term (2-4 years) |

| Federal highway and port modernization is unlocking new corridors | +1.9% | Interoceanic Corridor, Pacific and Gulf ports | Long term (≥ 4 years) |

| Blockchain-enabled customs clearance pilots | +1.1% | Northern border crossings, USMCA lanes | Medium term (2-4 years) |

| ESG-linked freight procurement mandates | +0.9% | National, multinationals | Medium term (2-4 years) |

| Embedded “broker-in-a-box” APIs inside SME ERPs | +0.6% | National, SME hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive Domestic B2C E-Commerce Fueling LTL Brokerage Volumes

Mexico’s online retail outlay is on track to reach USD 70 billion by 2027, rising 23% each year and multiplying small-parcel and LTL loads that require dense consolidation, dynamic routing, and real-time visibility services delivered by freight brokers. Metropolitan demand dominates today, yet secondary cities quickly gain share as broadband and digital wallets expand. Seasonal peaks such as Buen Fin generate profitable spot-rate spikes for intermediaries maintaining diversified carrier rosters. Shippers, especially SMEs, gravitate to self-service portals that promise transparent pricing, boosting the Mexico freight brokerage services market’s digital adoption curve[1]“E-commerce in Mexico is projected to reach $70 billion by 2027,” THELOGISTICSWORLD, thelogisticsworld.com.

Rapid Cold-Chain Capacity Build-Out for Agri-Food Exports

Mexico’s record avocado and berry exports, supported by Lineage Logistics’ USD 380 million cold-storage expansion in 2025, sustain double-digit growth in temperature-controlled lanes. Brokers adept at NOM-251 and FDA compliance capture premium loads by safeguarding in-transit integrity through IoT sensors and proactive exception management. Rising organic and specialty crop volumes further elevate refrigerated van utilization, reinforcing the Mexico freight brokerage services market’s margin upside in cold-chain niches.

Federal Highway and Port Modernization Projects Unlocking New Freight Corridors

The USD 50 billion Interoceanic Corridor, along with port upgrades at Manzanillo, Veracruz, and Lazaro Cardenas, redirects traffic into fresh east-west lanes and shortens reliance on congested northern crossings. Early-entry brokers cement carrier partnerships, gaining first-mover route density before rate competition intensifies. Industrial parks flanking these hubs promise captive drayage and last-mile demand, scaling the Mexico freight brokerage services market beyond its historical clusters[2]“Ventanilla Única de Comercio Exterior,” Government of Mexico, gob.mx.

Blockchain-Enabled Customs Clearance Pilots Cutting Border Dwell Times

VUCEM’s single-window digitalization alongside blockchain trials slashes inspection queues and enhances predictability, a capability brokers monetize through tighter delivery SLAs and working-capital relief for shipper inventories. Smaller intermediaries leverage the open platform to compete on international lanes without in-house customs teams, further democratizing the Mexico freight brokerage services industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diesel price volatility compressing take-rate margins | -1.4% | National, fuel-intensive corridors | Short term (≤ 2 years) |

| Stricter subcontractor labor-law audits | -1.0% | National, metro enforcement zones | Medium term (2-4 years) |

| Scarce domestic venture funding for freight-tech | -0.8% | Mexico City and Monterrey tech hubs | Long term (≥ 4 years) |

| Rising cyber-intrusions on broker TMS platforms | -0.6% | National, cloud-centric operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Diesel Price Volatility Compressing Take-Rate Margins

Volatile diesel prices in Mexico significantly impact freight brokers, particularly on shorter 500-mile routes where fuel costs represent a large share of carrier expenses. Fixed-rate contracts quickly become unprofitable during fuel price surges, forcing brokers to choose between simplicity and margin protection. Opting for fuel-indexed pricing reduces financial risk by adjusting to market fluctuations but adds complexity for shippers. This complexity undermines the straightforward service experience that traditionally differentiates brokerages.

Stricter Subcontractor Labor-Law Audits Increasing Compliance Overhead

Stricter subcontractor audits in Mexico are increasing brokerage costs as brokers must now verify micro-carriers' compliance with labor, social security, and tax obligations. This process adds onboarding paperwork and extra checks, increasing the risk of rejecting noncompliant operators and leading to higher compliance overheads and a reduced pool of low-cost, informal carriers. Consequently, sourcing affordable spot capacity has become more difficult. Digital documentation workflows lower friction but favor scaled intermediaries with deeper IT budgets, nudging the Mexico freight brokerage services market toward gradual consolidation[3]“Highway Modernization Projects 2025-2026,” Secretariat of Infrastructure, Communications and Transportation, gob.mx.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Momentum Reshapes the Mix

LTL’s 10.26% CAGR underscores how fragmented e-commerce deliveries tilt freight patterns toward smaller, more frequent loads. The Mexico freight brokerage services market size for LTL is set to expand faster than Full-Truckload through 2031 as online sellers demand agile networks that consolidate parcel-level demand into cost-efficient line-haul moves. Traditional FTL, while still commanding 73.12% market share in 2025, now coexists with hybrid models where brokers pair trunk FTL hauls with terminal-based LTL cross-docking to preserve speed without inflating cost. Advanced routing engines, load board APIs, and real-time pricing transparency enable brokers to fine-tune lane profitability, giving digital entrants an edge in this dynamic segment.

LTL’s rise increases the need for urban micro-fulfillment centers, reverse logistics solutions, and surge-capacity planning around flash-sale events. These capabilities feed a virtuous cycle of data acquisition and algorithmic optimization, reinforcing network effects for brokers that secure volume density first. Conversely, smaller legacy agents risk disintermediation unless they leverage white-label digital marketplaces or join cooperative networks to aggregate freight[4]“Terminal Modernization and Capacity Expansion Completion,” Port Authority, puertomanzanillo.com.mx.

By Equipment Type: Refrigerated Vans Secure Premium Margins

Refrigerated vans’ forecast 10.57% CAGR reflects persistent cold-chain demand driven by agricultural exports and pharmaceutical output. The Mexico freight brokerage services market share of refrigerated capacity is set to climb as infrastructure giants such as Lineage and Americold anchor warehouse networks along produce corridors. Temperature deviation alerts, embedded in broker telematics dashboards, support contractual KPIs tied to shelf-life preservation, legitimizing higher brokerage fees. Dry vans retained a 46.40% market share that scale advantages for general cargo, yet rate volatility is muted compared to reefer equipment, where seasonal harvest peaks spur spot-rate spikes.

Regulatory scrutiny under NOM-251 and US FDA rules elevates compliance costs, erecting entry barriers that favor brokers with in-house quality-assurance teams. Flatbeds, step-decks, and tankers remain stable niches serving construction, machinery, and liquid-bulk logistics, but their fragmented nature limits technology ROI, steering most digital investment toward dry and refrigerated segments.

By Haul Length: Local Routes Capture E-Commerce Windfall

Local hauls under 100 miles top growth at 12.60% CAGR as brands position inventory closer to consumers and gig-economy delivery models flourish. Route density inside Mexico City, Guadalajara, and Monterrey expands, allowing brokers to pivot from long-haul dependence toward multi-stop, same-day circuits that maximize driver and vehicle utilization. The Mexico freight brokerage services market size attached to local hauls will outpace regional and long-haul brackets between 2026 and 2031.

Long-haul lanes keep 63.81% market share, underpinning cross-border exports and north-south manufacturing corridors, yet they now face modal competition from truck-rail intermodal solutions. Regional hauls supply connective tissue between inland clusters and dual-coast ports, giving brokers options to flex capacity when fuel or chassis shortages hit long-distance segments.

By Business Model: Digital Platforms Accelerate but Hybrids Thrive

Digital freight platforms accelerate at 28.02% CAGR, automating tender, rate, and track-and-trace workflows for Mexico’s SME shipper base. Traditional agencies still dominate the market share at 74.71% in 2025, through legacy relationships, complex exception handling, and credit guarantees that digital-only players struggle to replicate at scale. Consequently, a hybrid future emerges where incumbents plug API layers into core TMS stacks while pure-plays recruit veteran operators to manage escalations, carving the Mexico freight brokerage services industry into high-touch and high-velocity tiers.

Asset-based brokers hedge capacity risk with owned fleets, winning strategic manufacturing contracts that prize reliability. Agent-model firms leverage commission-based sales footprints, extending reach without high fixed costs but absorbing brand-control challenges when service failures occur.

By End-User Industry: Manufacturing Holds Volume, E-Commerce Fuels Growth

Automotive and industrial manufacturing maintain a 31.13% market share, feeding steady northbound loads into the United States supply chains. Yet the e-commerce and 3PL segment, scaling at 21.10% CAGR, contributes the bulk of incremental brokerage revenue, adding SKU complexity and delivery-speed pressure that reward sophisticated load orchestration.

Agriculture, supported by cold-chain networks, and pharmaceuticals, demanding GDP-compliant handling, join construction and energy customers to round out a diversified demand base that insulates the Mexico freight brokerage services market from sector-specific slowdowns.

By Customer Size: SMEs Democratize Brokerage Demand

SMEs under USD 10 million in turnover show a 15.57% CAGR, empowered by cloud TMS portals and embedded ERP freight widgets that flatten the learning curve of tendering a load. Although average ticket size lags enterprise accounts, the sheer number of SME shippers dilutes concentration risk and builds recurring revenue.

Large enterprises, controlling 68.13% of the 2025 market share, continue to award multi-year contracts but now expect ESG reporting, lane-level carbon data, and cyber-resilience assurances before signing.

Geography Analysis

Freight generation migrates from the historical Norte maquiladora belt to the Bajio triangle of Guanajuato, Queretaro, and Aguascalientes, where automotive and aerospace OEMs balance export orientation with proximity to Mexico City’s consumption basin. The Mexico freight brokerage services market size attributable to this central cluster grows steadily as dual-direction flows reduce empty-mile penalties and improve carrier yield.

The Interoceanic Corridor’s 10 planned industrial parks promise east-west connectivity, buoying brokerage demand for drayage and inland distribution around Salina Cruz and Coatzacoalcos. Shippers exporting through Manzanillo and Veracruz gain direct Asia links, unlocking Mexico-centric distribution strategies that rely less on the United States gateways.

Northern states such as Nuevo Leon and Chihuahua retain critical mass with cross-border flows, yet congestion and compliance costs push some traffic southward. Pacific coast agricultural states, including Jalisco, Sinaloa, and Michoacan, sustain reefer brokerage volumes. Urban agglomerations drive last-mile brokerage intensity, making city-pair analytics and local carrier dispatch capabilities indispensable for competitive differentiation across the Mexico freight brokerage services market.

Coverage of the freight brokerage services market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America and Europe, alongside detailed country-level intelligence for Canada, Brazil, Spain, Netherlands, Poland, Saudi Arabia, and South Africa, each shaped by local operating conditions.

Competitive Landscape

The market is moderately fragmented, with global heavyweights (C.H. Robinson, RXO, J.B. Hunt ICS) coexisting alongside domestic leaders (Traxion, Promologistics) and rising digital challengers such as Nuvocargo. Traditional brokers shore up defenses through proprietary TMS upgrades, carrier payment platforms, and bilingual customer service hubs, while pure-play digitals secure venture rounds despite Mexico’s thin capital pools, aiming to automate every tender-to-settle step.

Cold-chain brokerage has emerged as a high-margin niche, where incumbents leverage infrastructure alliances with Lineage and Americold to offer end-to-end temperature monitoring that smaller rivals struggle to bankroll. Cybersecurity investments differentiate enterprise-facing brokers, as ransomware incidents prompt Fortune 500 shippers to vet partners’ SOC-2 readiness.

Consolidation accelerates when compliance overhead, fuel-indexed pricing complexity, and technology capex requirements outstrip micro-agents' cash flows. Still, specialist boutiques focusing on high-touch pharmaceutical freight, oversized project cargo, or mountainous last-mile routes maintain defensible positions through service intimacy.

Mexico Freight Brokerage Services Industry Leaders

Traxion

C.H. Robinson Worldwide Inc.

RXO Inc.

Arrive Logistics

BlueGrace Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: RXO integrated local Mexican carrier APIs into its proprietary platform, elevating real-time load visibility for cross-border customers.

- January 2026: Arrive Logistics rolled out lane-level carbon tracking for Mexico-U.S. corridors, enabling shippers to audit Scope 3 emissions against ESG procurement mandates.

- May 2025: J.B. Hunt ICS teamed with Mexican rail operators to provide integrated truck-rail offerings linking Bajío plants to Gulf ports.

- April 2025: Lineage Logistics finalized the first tranche of its USD 380 million cold-storage program, adding 2.5 million ft³ of capacity across Michoacan and Jalisco to backstop produce exports and drug distribution.

Mexico Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid and Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing and Automotive |

| Construction and Infrastructure Projects |

| Oil, Gas, Mining and Chemicals |

| Agriculture and Food / Beverage |

| Retail, FMCG and Wholesale Distribution |

| Healthcare and Pharmaceuticals |

| E-commerce and 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid and Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing and Automotive |

| Construction and Infrastructure Projects | |

| Oil, Gas, Mining and Chemicals | |

| Agriculture and Food / Beverage | |

| Retail, FMCG and Wholesale Distribution | |

| Healthcare and Pharmaceuticals | |

| E-commerce and 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How fast is digital brokerage expanding in Mexico?

Digital platforms are the fastest-growing model, posting a 28.02% CAGR between 2026 and 2031 on the back of API-enabled booking and real-time visibility.

Which freight segment benefits most from Mexico’s e-commerce boom?

Less-than-Truckload leads growth with a 10.26% CAGR as fragmented online orders require consolidation and flexible routing.

Why are refrigerated vans critical to brokers?

Agricultural exports and pharmaceutical output push refrigerated van demand to a 10.57% CAGR, allowing brokers with cold-chain expertise to earn premium margins.

What is the impact of the Interoceanic Corridor project?

The USD 50 billion east-west corridor unlocks new lanes that reduce northern border congestion, creating early-mover advantages for brokers that establish carrier networks there.

How do labor-law audits affect brokerage margins?

Mandatory subcontractor compliance checks raise onboarding costs and may limit access to low-rate micro-carriers, squeezing margins for brokers lacking scale.

Which customer tier is growing fastest?

Small businesses under USD 10 million in sales rise at a 15.57% CAGR as cloud tools democratize access to professional freight services.

Page last updated on: