Saudi Arabia Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

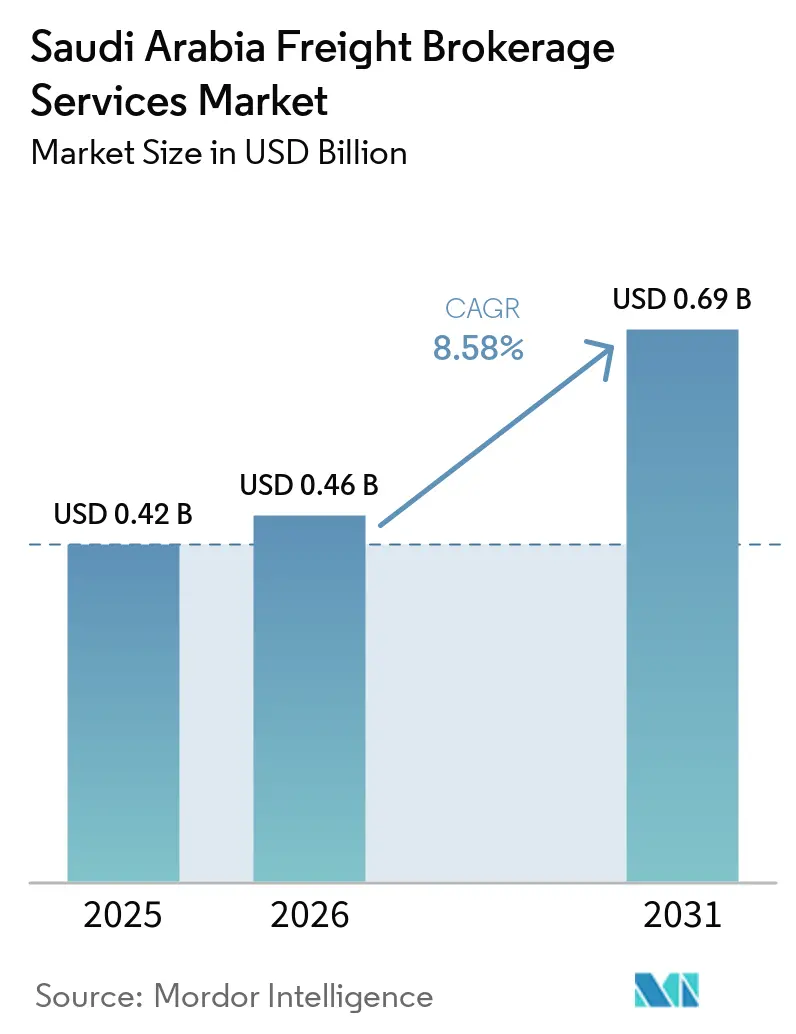

| Base Year Market Size (2025) | USD 0.42 Billion |

| Market Size (2026) | USD 0.46 Billion |

| Market Size (2031) | USD 0.69 Billion |

| Growth Rate (2026 - 2031) | 8.58% CAGR |

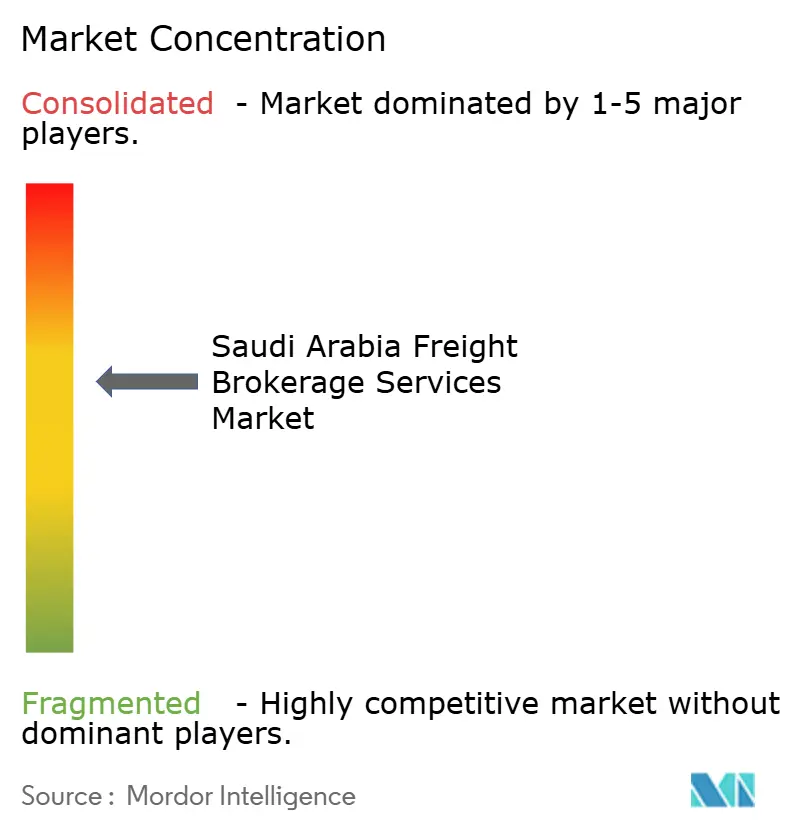

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Freight Brokerage Services Market Analysis by Mordor Intelligence

The Saudi Arabia freight brokerage market size was valued at USD 0.42 billion in 2025 and is estimated to grow from USD 0.46 billion in 2026 to reach USD 0.69 billion by 2031, at a CAGR of 8.58% during the forecast period (2026-2031). The ongoing rollout of 59 government-backed logistics centers under the National Industrial Development and Logistics Program (NIDLP) is dispersing freight generation into secondary cities, reshaping network design in the Saudi Arabia freight brokerage market. Mandatory e-transport documentation, phased in nationwide through 2026, is accelerating digital platform adoption while sidelining manual operators unable to meet real-time data-sharing requirements.

Key Report Takeaways

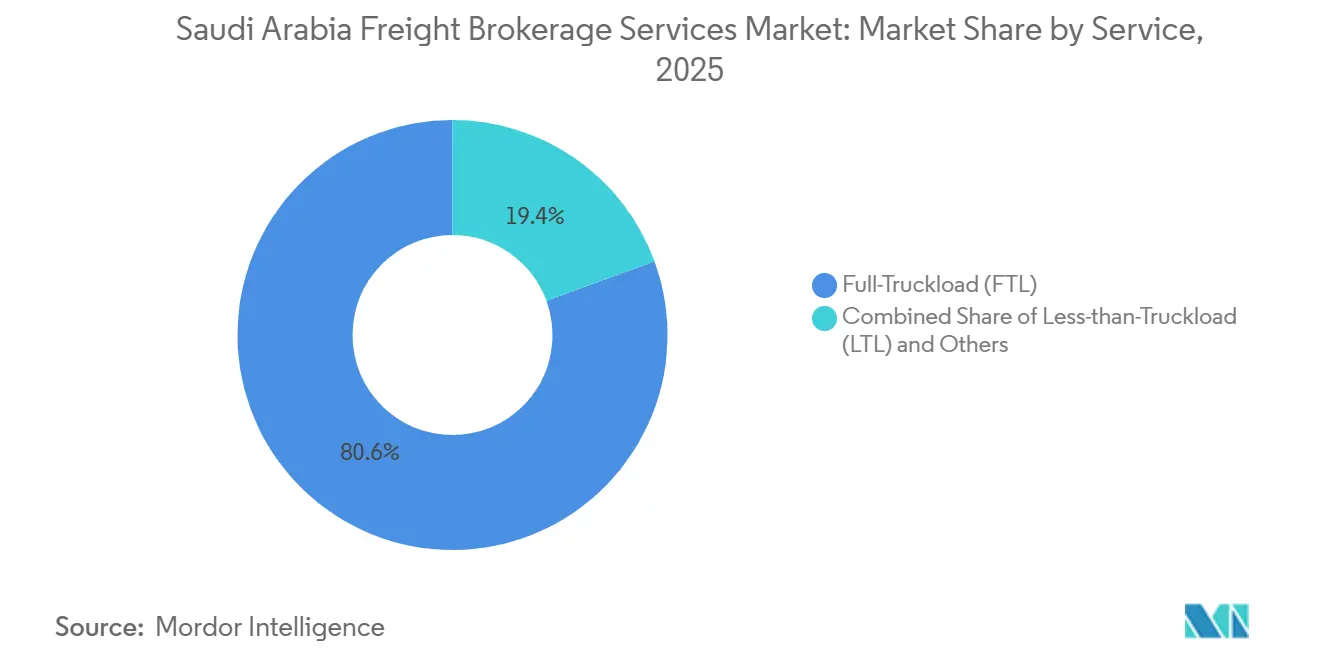

- By service, full-truckload held 80.58% of Saudi Arabia freight brokerage market share in 2025, while less-than-Truckload is projected to advance at an 11.26% CAGR through 2031.

- By equipment type, dry van segment accounted for 32.25% of the Saudi Arabia freight brokerage market in 2025, and refrigerated vans are expanding at a 14.53% CAGR through 2031.

- By haul length, long-haul captured 68.06% of the Saudi Arabia freight brokerage market share in 2025, whereas local services are forecast to grow at 13.97% CAGR through 2031.

- By business model, traditional brokers accounted for 89.10% of 2025 revenue, while digital freight brokerage is surging at a 29.07% CAGR over 2026-2031.

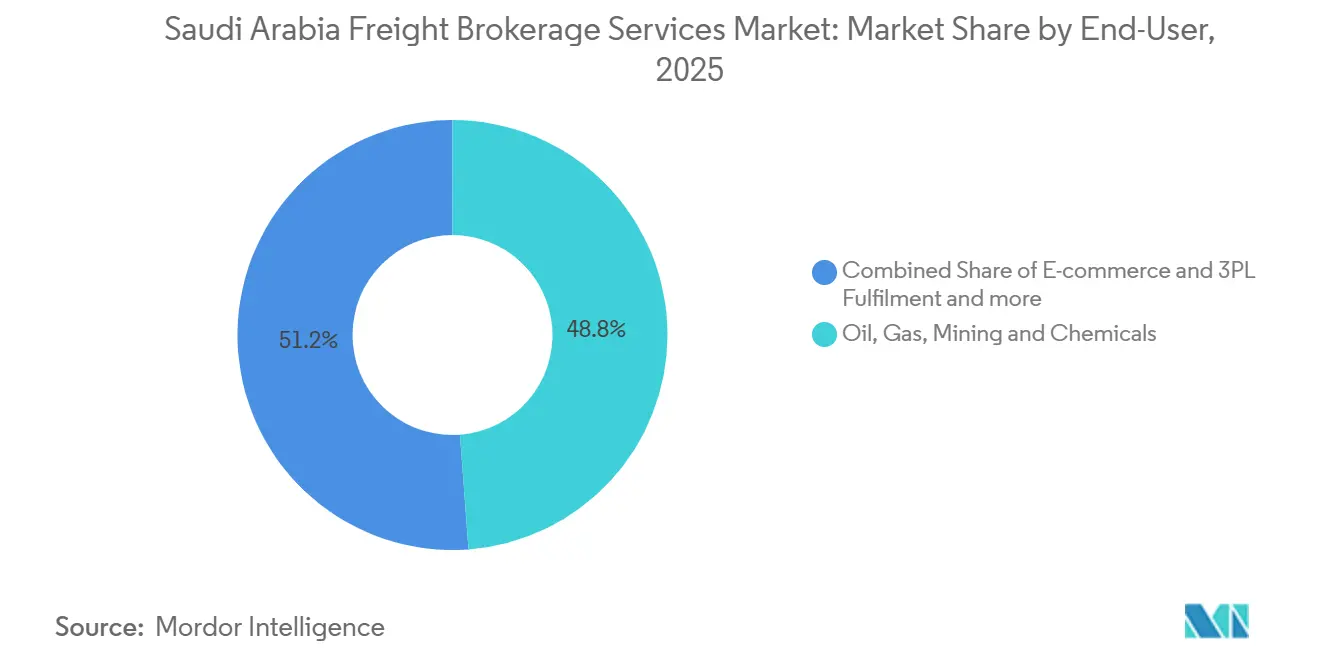

- By end-user, oil, gas, mining & chemicals led with a 48.83% share in 2025, while e-commerce & 3PL fulfillment are advancing at a 23.82% CAGR through 2031.

- By customer size, large enterprise shippers held 82.16% of the 2025 value, and small business demand is projected to climb at 18.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi arabia holds a defined position within a broader international distribution. The freight brokerage services market share data by Mordor Intelligence maps that allocation across all contributing countries and regions, globally.

Saudi Arabia Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Roll-out of 59 Government-Backed Logistics Centers | 1.3% | National, with concentration in Tabuk, Jazan, Hail, and Al-Baha | Long term (≥ 4 years) |

| Belt & Road China–KSA Freight Corridor Expansion | 1.1% | National, focused on Red Sea ports and cross-border land routes | Medium term (2-4 years) |

| Surge in 3PL / 4PL Contract-Logistics Outsourcing | 1.4% | National, led by Riyadh and Eastern Province industrial zones | Medium term (2-4 years) |

| Port Automation & Capacity Upgrades at Jeddah / Dammam | 0.9% | Western and Eastern Provinces, port-adjacent logistics clusters | Short term (≤ 2 years) |

| Mandatory e-Transport Digital Freight Documentation | 1.2% | National, with phased enforcement beginning in major cities | Short term (≤ 2 years) |

| Cooling-Chain Demand from High-Value Date & Produce Exports | 0.8% | Al-Ahsa, Qassim, Madinah agricultural zones to port corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Roll-out of 59 Government-Backed Logistics Centers

New multimodal hubs ranging from 50,000 to 200,000 m² are decentralizing freight origins, forcing brokers to extend coverage beyond the Riyadh-Jeddah-Dammam triangle and stimulating lane creation inside the Saudi Arabia freight brokerage market. The Jazan Economic City site alone generates roughly 450 daily truckloads, each requiring brokerage coordination for inbound raw materials and outbound finished goods. Standardized yard-management systems embedded at the centers allow brokers to plug APIs directly into dock-scheduling workflows, which cuts dwell times and sharpens asset turns. Mid-tier brokers adopt asset-light collaboration models with regional carriers to secure last-mile capacity without breaching capital limits. As the network matures, nodes in Tabuk and Hail are expected to siphon volume from conventional corridors, flattening capacity spikes and spreading earnings opportunities more evenly across the Saudi Arabia freight brokerage market.

Belt & Road China–KSA Freight Corridor Expansion

China–Saudi bilateral trade climbed to USD 106 billion in 2025, driving 2.8 million TEUs through Red Sea ports and intensifying broker demand for port-to-door services. Dedicated China service berths at Jeddah processed 1.2 million TEUs, compelling intermediaries to master multimodal documentation and Mandarin language skills for smoother discharge planning. Bonded zones at Riyadh and Dammam airports open duty-deferred re-export channels that expand margin pools beyond pure transport coordination. Brokers brandishing Chinese partnerships secure volume priority and insulate customers from customs bottlenecks, strengthening customer stickiness inside the Saudi Arabia freight brokerage market[1]China Daily, “China–Saudi Arabia Trade Reaches New Heights in 2025,” chinadaily.com.cn.

Surge in 3PL / 4PL Contract-Logistics Outsourcing

Contract-logistics penetration advanced to 38% of total logistics spend in 2025 as shippers shifted inventory risk to professional operators. NEOM alone awarded USD 800 million in multi-year contracts embedding brokerage services across inbound materials and inter-site moves. 4PL control-tower models elevate integration requirements, redirecting competition toward visibility dashboards, exception management, and predictive analytics that guide dynamic carrier selection. Brokers investing in real-time transportation management systems convert operational data into performance insights, anchoring recurring revenue streams within the Saudi Arabia freight brokerage market.

Port Automation & Capacity Upgrades at Jeddah / Dammam

Automation programs worth USD 1.6 billion at Jeddah Islamic Port slashed container dwell to 2.8 days in 2025, enhancing reliability for automotive parts, pharmaceuticals, and perishables. Dammam’s Phase-2 expansion added 2.5 million TEU capacity and gate processing that is 60% faster, letting brokers compress buffer times and promise narrower delivery bands. Integration with the National Single Window condenses customs clearances, amplifying throughput and supporting premium pricing strategies across the Saudi Arabia freight brokerage market[2]Saudi Ports Authority, “Port Automation Initiatives Deliver Efficiency Gains,” ports.gov.sa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Squeeze from Vertically Integrated 3PL Competitors | -1.5% | National, most acute in Riyadh and Eastern Province | Short term (≤ 2 years) |

| Labor Localization (Saudization) Driving Turnover Costs | -1.1% | National, with a higher impact in specialized roles | Medium term (2-4 years) |

| Planned Toll-Road Pricing Reform Elevating Line-haul Costs | -0.8% | National, focused on major intercity corridors | Medium term (2-4 years) |

| Rail Wagon / Container Spec Mismatch Limiting Intermodal Growth | -0.6% | Riyadh-Dammam and Riyadh-Jeddah rail corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin Squeeze from Vertically Integrated 3PL Competitors

Integrated operators such as Almajdouie and Naqel bundle warehousing with captive fleets, undercutting spot rates by up to 20% and dragging broker gross margins toward single digits. The CEVA-Almajdouie venture escalates pressure by combining global reach with domestic trucks, shrinking addressable revenue for pure intermediaries. Niche specialization in hazardous, oversized, or time-critical freight remains the refuge for independents within the Saudi Arabia freight brokerage market.

Labor Localization (Saudization) Driving Turnover Costs

Training pipelines lag demand, inflating onboarding costs and constraining capacity expansion. Large brokers co-develop curricula with vocational institutes to secure talent pipelines, but ROI materializes over multi-year horizons, weighing on EBITDA in the Saudi Arabia freight brokerage market. This also delays scaling of specialized roles, creating bottlenecks in handling complex or high-value shipments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Consolidation Expertise Drives LTL Acceleration

Less-than-Truckload volumes are forecast to grow at an 11.26% CAGR, outpacing the Saudi Arabia freight brokerage market average as e-commerce fragmentation multiplies sub-pallet consignments requiring consolidation hubs. Full-Truckload still dominated with 80.58 % of the Saudi Arabia freight brokerage market share in 2025, supported by energy, petrochemical, and bulk industrial flows. High-frequency LTL shipments through cross-dock terminals in Riyadh and Jeddah lift trailer utilization and raise yield per mile. Digital platforms exploit algorithmic load-pairing to cut empty miles, creating price advantages over manual brokers.

Carriers aligned with LTL-focused brokers install telematics and dock-scheduling APIs to handle multi-stop routing without service lapses. E-commerce merchants migrate away from courier networks for heavier 40-100 kg consignments, funneling incremental loads into the Saudi Arabia freight brokerage market. FTL brokers, under margin pressure, cross-sell partial-load consolidation to defend wallet share. Conversely, LTL providers tap dedicated contract lanes when run-cut density warrants upgrading to full-truck services, blurring traditional lines between categories within the Saudi Arabia freight brokerage market.

By Equipment/Trailer Type: Cold Chain Infrastructure Fuels Reefer Growth

Refrigerated Vans are expanding at a 14.53% CAGR, the fastest of any trailer class, outstripping the overall Saudi Arabia freight brokerage market growth as pharmaceutical imports and premium date exports demand unbroken cold chains. Dry Vans commanded 32.25% of the Saudi Arabia freight brokerage market size in 2025, servicing high-volume FMCG and industrial inputs. IoT-enabled reefers that log ambient deviations help brokers satisfy European and Asian buyers’ traceability requirements. Tanker moves, though niche, anchor stable revenue corridors between Jubail’s chemical plants and Dammam port, where Saudi Arabia's freight brokerage market share retention depends on safety compliance expertise.

Flatbed fleets serving construction projects at NEOM, Qiddiya, and the Red Sea Project carry oversized modules requiring police escorts and bridge-engineering sign-offs. As Vision 2030’s manufacturing clusters mature, demand for specialized equipment, such as double-deck car carriers and bulk cement pneumatic trailers, adds product-line depth. Brokers that bundle reefer and dry capacity in the same bid package win end-to-end contracts, locking in repeat volume inside the Saudi Arabia freight brokerage market.

By Haul Length: Urban Densification Accelerates Local Services

Local hauls under 100 miles are slated for 13.97% CAGR to 2031 as dark stores, urban micro-fulfillment centers, and multi-drop e-grocery deliveries proliferate. Yet Long-Haul corridors over 500 miles retained 68.06% of Saudi Arabia freight brokerage market share in 2025, reflecting sparse rail competition and concentrated industrial nodes. Smart dispatch tools cut city-center congestion exposure, raising daily trip counts for local operators even as fuel costs edge up. Regional lanes bridging 100-500 miles underpin feedstock transfers between secondary cities and coastal export hubs, gaining relevance as NIDLP logistics centers ramp up throughput within the Saudi Arabia freight brokerage market.

Autonomous truck pilots on the Riyadh-Dammam axis could carve 3-4% out of line-haul labor costs by 2028, but regulatory approval remains uncertain. Brokers diversify by blending local same-day routes with traditional trunk hauls, evening cash-flow volatility, and extracting incremental revenue from back-haul repositioning inside the Saudi Arabia freight brokerage market.

By Business Model: Platform Economics Disrupt Traditional Relationships

Traditional brokers maintained 89.10% revenue control in 2025, yet digital intermediaries are lifting the Saudi Arabia freight brokerage market share quarter by quarter through instant quoting and automated carrier matching. With 29.07% CAGR projected, digital players formalize previously opaque price discovery, squeezing spread per load but scaling volume. Hybrid incumbents bolt on SaaS modules covering e-transport compliance to preserve legacy shipper ties while enhancing operational accuracy.

Asset-based brokerage, dominant in energy and petrochemicals, guarantees capacity during peak refinery turnarounds, commanding uplift on contracted rates. Agent models supply geographic reach in peripheral provinces, though platform APIs now simulate similar coverage without human franchisees. Compliance deadlines for e-waybills function as a forcing mechanism that shepherds late adopters onto shared tech rails throughout the Saudi Arabia freight brokerage market.

By End-User Industry: Diversification Challenges Energy Dominance

Oil, gas, mining & chemicals held 48.82% of Saudi Arabia freight brokerage market share in 2025, yet its growth is in low single digits. E-commerce & 3PL fulfillment leads expansion with 23.82% CAGR, fueled by online retail penetration that hit 12% of total sales in 2025. Manufacturing & automotive lanes grow as localization programs require inbound CKD kits and outbound finished vehicles. Construction logistics remains cyclical but resilient, given multi-billion-dollar giga-projects.

Healthcare & pharmaceuticals necessitate GDP-compliant reefer fleets, introducing accreditation barriers that shelter margins. Retail, FMCG & Wholesale continue steady volume accrual tied to population growth, while Agriculture & Food/Beverage benefit from export-oriented greenhouse output. Shippers diversify modal mixes, incentivizing brokers to broaden carrier rosters and value-added services, deepening maturity inside the Saudi Arabia freight brokerage market.

By Customer Size: Digital Platforms Democratize SMB Access

Large enterprise shippers represented 82.16% of cargo volume in 2025, reflecting decades-long carrier relationships and centralized procurement control. Yet small business demand climbs at 18.18% CAGR as self-service booking portals lower entry thresholds. Mid-Market firms in the USD 10-100 million bracket seek blended service bundles, spot capacity, plus analytics that digital brokers deliver at competitive price-points. Customer-experience parity across tiers promotes volume diversification, distributing risk, and underpinning the resilience of the Saudi Arabia freight brokerage market.

SMB shippers value quick credit decisions and pay-as-you-go terms that bypass letter-of-credit paperwork. Large enterprises still mandate EDI hooks and KPI scorecards, demanding tech investments that only scale with significant throughput. Consequently, brokers segment service levels while maintaining unified data backbones, leveraging versatility to defend share across the Saudi Arabia freight brokerage market spectrum.

Geography Analysis

Saudi Arabia’s Riyadh-Jeddah-Dammam axis concentrates roughly 75% of freight, reflecting industrial production, consumer markets, and port connectivity. The Eastern Province leads industrial freight thanks to Saudi Aramco’s hydrocarbon flows and SABIC’s petrochemical clusters, drawing steady brokerage demand for bulk ISO tanks and project cargo. Riyadh, the administrative hub, sustains high outbound volumes of consumer goods, while Jeddah Islamic Port handled 4.2 million TEUs in 2025, anchoring import-heavy broker lanes.

Western Province gains momentum from King Abdullah Economic City’s 180,000 m² logistics zone, operational since Q2 2025, providing cost-effective cross-dock space for SME shippers. Secondary nodes such as Tabuk, Jazan, Hail, and Al-Baha emerge as freight magnets as NIDLP hubs sprinkle capacity across hinterlands, extending the reach of the Saudi Arabia freight brokerage market. Northern borders with Jordan and Iraq open over-the-road export lanes, yet processing lags limit throughput compared with GCC corridors[3]King Abdullah Economic City, “Logistics Zone Operational Launch,” kaec.net .

NEOM’s construction peaks at 12,000 daily truckloads in 2025, creating unprecedented brokerage opportunities in the northwest. The Red Sea Project and Qiddiya developments induce similar but smaller surges in the western corridor. Airport cargo upgrades at Riyadh and Tabuk improve multimodal options, enabling brokers to splice air legs into surface chains, enhancing service differentiation across the Saudi Arabia freight brokerage market.

Mordor Intelligence delivers a comprehensive view of the freight brokerage services market across all major regions such as North America and Europe, alongside country-level analysis for Russia, Germany, Canada, Mexico, Spain, Spain, and Netherlands, each offering a view of the local market realities.

Competitive Landscape

Roughly 150 active intermediaries populate the Saudi Arabia freight brokerage market, producing moderate fragmentation. Integrated 3PLs such as Almajdouie, Naqel Express, and CEVA-Almajdouie leverage owned fleets to compress contract prices, eroding stand-alone brokers’ margins to sub-10% on spot lanes[4]CEVA Logistics, “Almajdouie Joint Venture Finalization,” cevalogistics.com. Digital challengers TruKKer, Trukkin, and Homoola harness algorithmic carrier matching and real-time tracking to cut transaction friction, scaling rapidly in commoditized FTL segments.

Niche specialists concentrate on hazardous materials, oversized cargo, pharmaceutical cold chain, and Belt & Road corridor traffic that reward regulatory fluency and multi-lingual coordination skills. Technology adoption delineates winners: AI-enabled route-optimization engines, blockchain documentation, and predictive demand analytics separate forward-looking brokers from legacy paper-based shops. Regulatory moves mandating e-transport documentation accelerate shake-out, with smaller brokers either adopting white-label platforms or exiting the Saudi Arabia freight brokerage market.

Partnerships and M&A activity intensify: DHL’s minority stake in AJEX strengthens express synergies, Maersk’s Jeddah logistics park integrates port warehousing with inland trucking, and Four Winds’ JCtrans tie-up enlarges global reach. Joint ventures coalesce around giga-project logistics, with DSV and NEOM forming a dedicated vehicle to manage northwestern construction freight. Price wars persist in commoditized lanes, but capability gaps in compliance-heavy sectors preserve healthier contribution margins.

Saudi Arabia Freight Brokerage Services Industry Leaders

ADQ

ADQ

Ceva Logistics

Almajdouie Logistics

Naqel Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Saudi Arabia enforced mandatory National Address requirements for all parcel shipments, compelling logistics providers and freight intermediaries to standardize shipment-level address data at the time of booking.

- October 2025: Saudi Post (SPL) signed a strategic agreement with SAL Logistics Services to integrate airmail handling and cargo operations. The partnership enhances end-to-end logistics capabilities and supports national supply chain integration goals.

- July 2025: Agility Logistics expanded its global footprint through Menzies Aviation’s acquisition of G2 Secure Staff in the aviation services sector. The move enhances air cargo handling capabilities, indirectly strengthening logistics flows into Saudi Arabia.

- February 2025: DHL acquired a minority stake in AJEX, enhancing express delivery synergies for brokers needing door-to-door capacity.

Saudi Arabia Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid & Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing & Automotive |

| Construction & Infrastructure Projects |

| Oil, Gas, Mining & Chemicals |

| Agriculture & Food / Beverage |

| Retail, FMCG & Wholesale Distribution |

| Healthcare & Pharmaceuticals |

| E-commerce & 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid & Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing & Automotive |

| Construction & Infrastructure Projects | |

| Oil, Gas, Mining & Chemicals | |

| Agriculture & Food / Beverage | |

| Retail, FMCG & Wholesale Distribution | |

| Healthcare & Pharmaceuticals | |

| E-commerce & 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How large will freight brokerage revenue in Saudi Arabia be by 2031?

The Saudi Arabia freight brokerage market size is projected to reach USD 0.69 billion by 2031, reflecting 8.58% annual growth from 2026.

Which customer segment is expanding fastest?

Small Businesses under USD 10 million revenue are growing at an 18.4% CAGR as digital platforms lower entry barriers for professional freight coordination.

What is driving the surge in refrigerated transportation demand?

Rising pharmaceutical imports and premium date exports, coupled with new cold-storage capacity at Jeddah and Riyadh, are propelling Refrigerated Van demand at 14.8% CAGR.

How will mandatory e-transport documentation affect brokers?

Universal e-waybill enforcement by Q4 2026 forces legacy brokers to adopt digital systems, benefiting tech-enabled platforms that already meet compliance requirements.

Which geographic areas outside the main corridor are gaining traction?

Secondary cities such as Tabuk, Jazan, Hail, and Al-Baha are attracting freight flows as 59 government-backed logistics centers decentralize the network.

What competitive strategies are leading brokers deploying?

Market leaders combine AI-powered route optimization, captive carrier capacity, and blockchain documentation to defend margins amid price pressure from digital entrants.

Page last updated on: