Russia Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.43 Billion |

| Market Size (2026) | USD 17.02 Billion |

| Market Size (2031) | USD 20.3 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

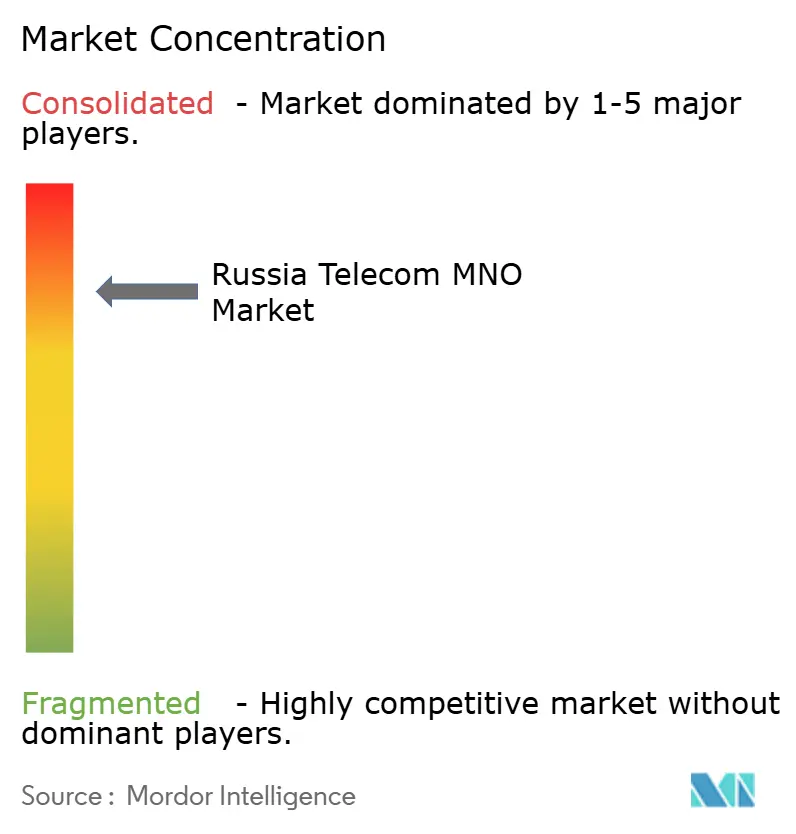

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Telecom MNO Market Analysis by Mordor Intelligence

The Russia Telecom MNO Market size was valued at USD 16.43 billion in 2025 and estimated to grow from USD 17.02 billion in 2026 to reach USD 20.3 billion by 2031, at a CAGR of 3.59% during the forecast period (2026-2031).

This reflects a pivot from subscriber acquisition to revenue-per-user maximization. Operators are spending more on network quality, spectrum refarming, and domestic equipment trials while managing sanctions-driven supply shifts. Mobile services generated RUB 976 billion in 2024, an 8.9% jump that highlighted the Russia telecom MNO market’s resilience amid macro-economic pressure [1]CNews, “Минцифры: итоги года для российской телеком-отрасли,” CNews.ru. Domestic 5G research funding, aggressive fixed-mobile convergence bundles, and industrial demand for private LTE are moving revenue growth away from basic connectivity toward enterprise and ecosystem services. Meanwhile, tariff inflation and energy-related opex headwinds threaten margins, pushing operators to accelerate AI-led efficiency programs and diversify into fintech, media, and IoT services. Infrastructure build-out reached 125,800 new base stations in 2024, underscoring the Russia telecom MNO market’s long-term commitment to coverage and capacity upgrades [2]ComNews, “За 2024 г. операторы ‘большой четверки’ возвели 125,8 тыс. базовых станций,” Comnews.ru.

Key Report Takeaways

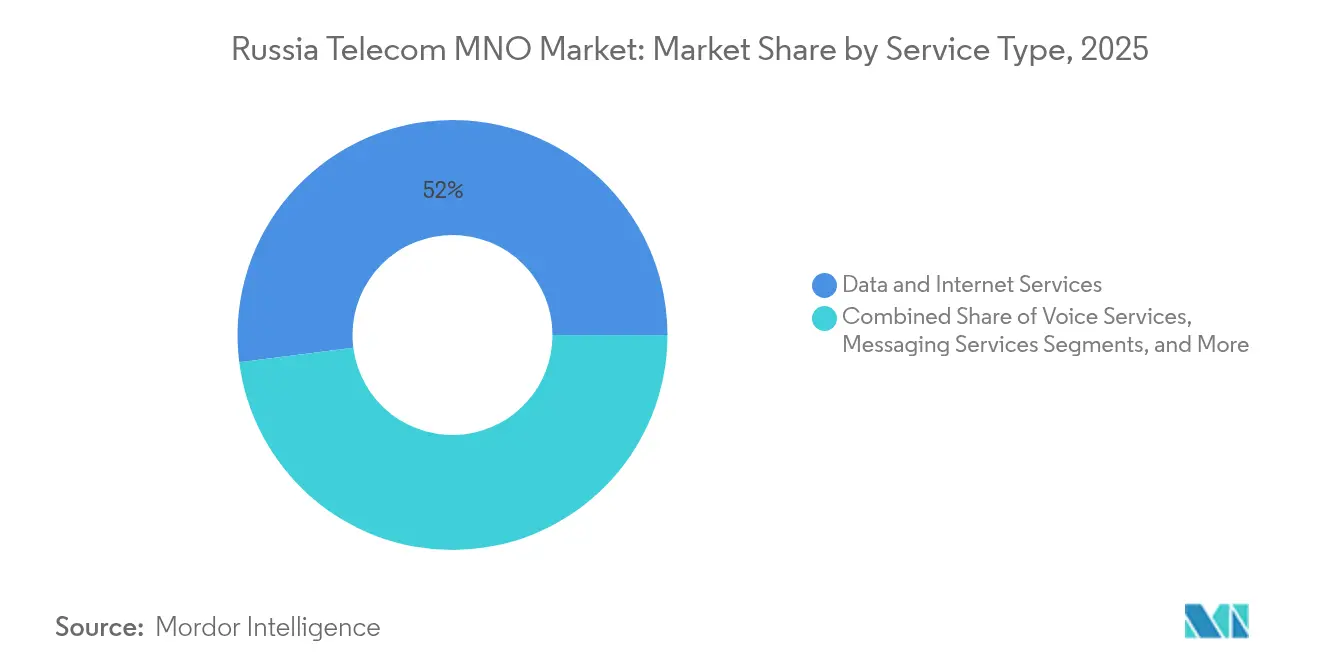

- By service type, data and internet services led with 52.03% of the Russia telecom MNO market share in 2025; IoT and M2M services are projected to expand at a 3.61% CAGR through 2031.

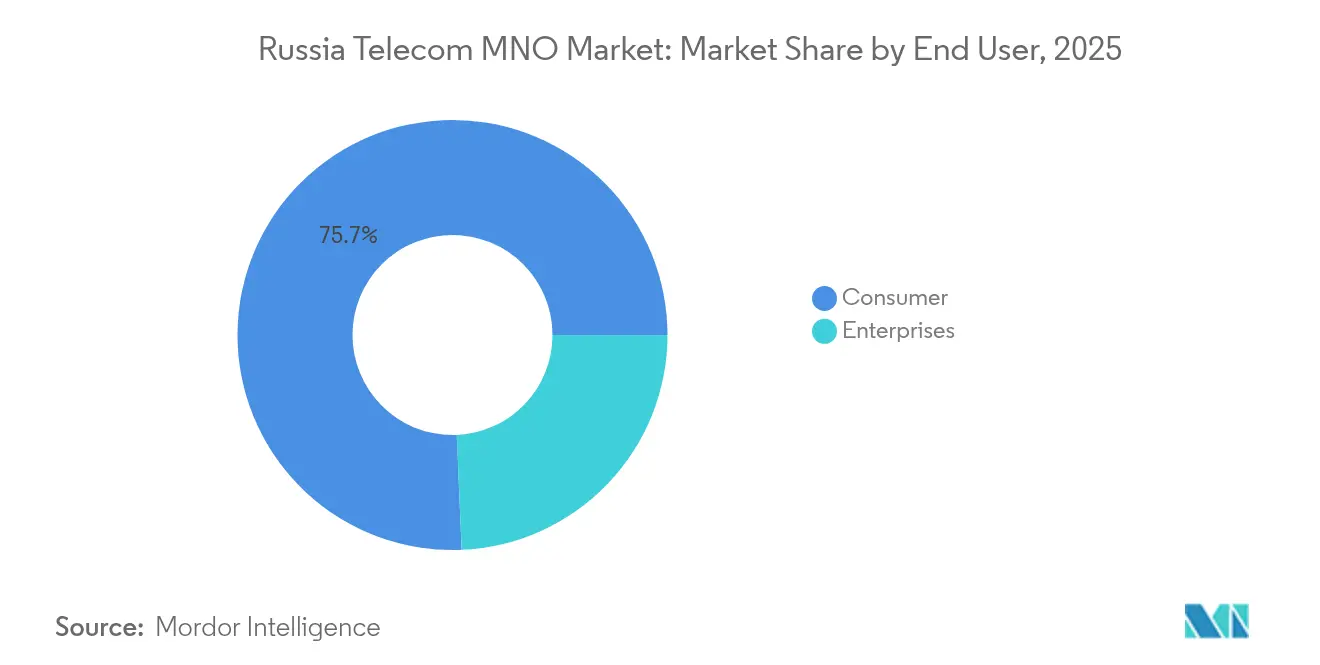

- By end user, consumer offerings accounted for 75.68% share of the Russia telecom MNO market size in 2025, while enterprise services are advancing at a 3.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile data traffic fueled by affordable unlimited data plans | +0.8% | National, with concentration in Moscow and St. Petersburg | Short term (≤ 2 years) |

| Government impetus on 5G roll-out and spectrum re-farm | +0.6% | Major cities initially, expanding to regional centers | Medium term (2-4 years) |

| Rapid expansion of fixed-mobile-convergence bundles lifting ARPU | +0.5% | Urban areas with fiber infrastructure coverage | Medium term (2-4 years) |

| Explosion of enterprise private-LTE networks for critical infrastructure | +0.4% | Industrial regions, mining areas, manufacturing hubs | Long term (≥ 4 years) |

| Monetization of AI-driven network-slicing for industrial IoT corridors | +0.3% | Smart city initiatives in major metropolitan areas | Long term (≥ 4 years) |

| Migration of IT workloads to domestic cloud hubs boosting B2B backhaul demand | +0.4% | Data center locations in Moscow, St. Petersburg, Novosibirsk | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in mobile data traffic fueled by affordable unlimited data plans

Unlimited bundles keep subscriber churn low while lifting traffic 13.9% year-on-year in 2024. MTS’s March 2025 “MTS Most of all” 100 GB offer illustrates how operators monetize volume without compromising network load because LTE refarming has raised spectral efficiency [3]MTS, “Встречайте тариф МТС Больше всех,” Primorye.mts.ru. The strategy resembles global moves toward data-centric pricing while local regulation forbids scarcity-based throttling. MegaFon’s 12% speed gain after refarming confirms capacity headroom for further traffic growth [4]MegaFon, “МегаФон ускорил на 12% мобильный интернет в России,” Corp.megafon.ru. Higher usage feeds advertising and VAS upsells, increasing blended ARPU enough to offset inflation-driven cost hikes.

Government impetus on 5G roll-out and spectrum re-farm

Regulators removed 5G usage fees in 2024, cut domestic base-station funding, but mandated 6% locally built equipment by end-2025. Although the 3.4-3.8 GHz band remains military, the 4.4-4.99 GHz allocation aligns Russia with China and Japan, reducing vendor costs. Moscow’s 1 Gbit/s domestic antenna trial shows indigenous tech viability. Operators expect standalone 5G launches by 2028 on home-grown RAN, which will anchor long-run competitiveness and lower geopolitical risk.

Rapid expansion of fixed-mobile-convergence bundles lifting ARPU

Fixed internet revenues rose 11% to RUB 279 billion in 2024, a sign that quad-play bundles resonate with urban households. Convergence lets operators cross-sell media, fintech, and smart-home services under a single bill, boosting stickiness. MegaFon’s infrastructure partnership with SberMobile accelerates regional footprint without duplicating fiber capex. Unified licensing and VAT incentives support the bundle push, helping offset tariff-regulated consumer price caps. AI-enabled churn prediction further lifts lifetime value by 3-10% estimated margin expansion over five years.

Explosion of enterprise private-LTE networks for critical infrastructure

Industrial digitization is generating new B2B revenue pools beyond public connectivity. MTS’s LTE deployment at Kovdorsky GOK mine achieved reliable low-latency links in underground conditions. Domestic suppliers such as Bulat and Irteya are piloting ruggedized RAN solutions acceptable under sanctions, limiting dependence on Huawei. Enterprises value security and deterministic performance, agreeing to multiyear managed-service contracts that insulate operators from consumer ARPU volatility.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| International sanctions limiting access to advanced RAN equipment | -0.9% | National, with greater impact on network expansion projects | Medium term (2-4 years) |

| SIM-card saturation amid low population growth | -0.6% | National, particularly affecting rural and secondary cities | Long term (≥ 4 years) |

| Rising energy tariffs squeezing network-opex margins | -0.5% | National, with regional variations in electricity pricing | Short term (≤ 2 years) |

| Mandatory domestic encryption standards delaying new service launches | -0.4% | National, affecting all operators equally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

International sanctions limiting access to advanced RAN equipment

The 2023 exit of Nokia and Ericsson removed the fastest upgrades for LTE-A and early 5G, leaving operators to pivot toward Chinese and nascent domestic suppliers. “Gray” imports fill gaps but raise capex and lengthen maintenance cycles. Roskomnadzor’s localization mandates push operators to co-develop radios with Russian vendors, a move that secures sovereignty yet slows optimal deployment.

Rising energy tariffs squeezing network-opex margins

Frequency fees in the 694-790 MHz band jumped to RUB 700 million yearly per operator, adding USD 260 million system-wide cost in 2024. Electricity price inflation compounds site-level expenses, yet regulators cap consumer tariff hikes. Operators now prioritize energy-efficient radios and renewable micro-grids, but payback horizons extend beyond three years, keeping pressure on EBITDA.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data-Centric Revenue Momentum Continues

Data and internet services held 52.03% of Russia's telecom MNO market share in 2025, dwarfing legacy voice on both revenue and traffic metrics. The Russia telecom MNO market size associated with data services is forecast to expand as video, gaming, and fintech apps deepen user engagement. IoT and M2M remain niche at 4% of revenue today, yet lead growth with a 3.61% CAGR as industrial clients automate supply chains.

Service diversification speeds up ARPU gains. Operators bundle PayTV, cloud storage, and cybersecurity to extract a higher wallet share while maintaining flat nominal tariffs. Domestic content quotas channel OTT traffic to local platforms, increasing cache hit rates and lowering international transit costs. Edge computing pilots under 4.9 GHz spectrum further elevate the Russia telecom MNO market’s enterprise opportunity, particularly for manufacturing quality control and smart-city surveillance.

By End User: Enterprise Digital Transformation Ups the Stakes

Consumer activity represented 75.68% of the Russia telecom MNO market size in 2025, but incremental growth is slowing as SIM penetration exceeds 190%. The enterprise cohort, although smaller, is on track for a 3.92% CAGR to 2031 owing to private networks, cloud backhaul, and zero-trust security services. Industrial customers choose multiyear contracts, lifting revenue visibility and lowering churn relative to prepaid consumer accounts.

Government digitization grants favor Russian suppliers, insulating operators from foreign rivals and positioning mobile incumbents as end-to-end ICT partners. Managed SD-WAN, SASE security, and IIoT analytics add high-margin recurrent fees. Conversely, consumer wallets feel an inflationary squeeze; average monthly spend rose only 4% to RUB 391 in 2024 while CPI climbed faster, forcing operators to seek value creation through ecosystem subscribers rather than price hikes.

Geography Analysis

Moscow and St Petersburg generate close to 45% of Russia's telecom MNO market revenues due to dense populations and corporate headquarters demand. Urban LTE-Advanced coverage reaches 99% of households, enabling premium unlimited plans and early 5G pilots. Base-station density exceeds 2,000 sites per million inhabitants, ensuring consistent median download speeds above 40 Mbps.

Industrial regions like Lipetsk, Sverdlovsk, and Murmansk host private LTE build-outs supporting mining and metallurgy. These deployments lift the local Russia telecom MNO market size through long-term service contracts and backhaul sales. Novosibirsk emerges as a domestic cloud node, drawing fiber upgrades that spill over into consumer FTTx adoption. Regional energy subsidies partially offset rising electricity tariffs, helping operators maintain EBITDA in Siberia and the Far East.

Rural areas still face 15-20 Mbps speeds because of sparse backhaul and high power costs. The Digital Development Ministry’s 2025–2027 program obliges operators to extend 4G to 1,500 underserved settlements, using subsidies and shared passive infrastructure. Integration of newly incorporated territories adds regulatory obligations such as roaming removal while demanding significant capex for tower reinforcement and fiber runs.

Competitive Landscape

Four national licensees, MTS, MegaFon, Beeline (VimpelCom), and T2 Russia, dominate a major share of the Russia telecom MNO market revenues, driving an oligopolistic environment where network investments outweigh price wars. Consolidation, such as Rostelecom’s control of T2 Russia, strengthens bargaining power with equipment vendors and regulators. Operators differentiate through ecosystems: MTS integrates fintech, media, and tele-medicine; MegaFon focuses on throughput leadership and wholesale MVNO deals; Beeline ramps AI-based churn mitigation; T2 Russia leverages new adtech assets for micro-targeted offers.

International sanctions shift procurement dynamics but also reduce foreign competitive threats. Huawei now supplies most new macro radios while domestic firms grow in rural turnkey projects. Virtual network operators like SberMobile broaden retail choice without undermining host-operator revenues, generating incremental wholesale income. AI orchestration of spectrum and power improves cost per gigabyte, a critical factor as tariffs remain politically sensitive.

Investment discipline heightens as capex-to-sales ratios fall from 23% in 2023 to 19% in 2025 as shared infrastructure and domestic equipment discounts kick in. Operators co-site 60% of new rural towers, freeing funds for 5G core migration. Enterprise verticals receive dedicated sales teams and revenue-share models with systems integrators. Aggressive energy-efficiency retrofits, including lithium battery swaps and solar supplements, target 20% cut in site power consumption by 2028.

Russia Telecom MNO Industry Leaders

MobileTeleSystems PJSC (MTS)

MegaFon PJSC

T2 Russia

Beeline (PJSC VimpelCom)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MegaFon raised median download speed by 12% to 43.74 Mbps and expanded coverage 17.4% after LTE refarming in Moscow.

- July 2025: Moscow trialed a fully Russian-made 5G antenna that delivered 1 Gbit/s throughput.

- June 2025: Federal funding for domestic base stations trimmed to RUB 20.3 billion, with private-sector input lifted to RUB 70.7 billion; serial production slated for 2027.

- March 2025: MTS launched “MTS More Than All” bundle with unlimited on-net calls, 100 GB data, 2,000 off-net minutes, and 100 SMS.

- December 2024: T2 Russia bought adtech firms Yabbi, Redllama, and Plazkart to boost digital services.

Russia Telecom MNO Market Report Scope

Telecommunication involves transmitting information at a speed akin to face-to-face conversations. It encompasses exchanging data, voice, and video over long distances through electronic mediums.

The report covers Russian telecom MNO market companies, and the market is segmented by service (voice services (wired and wireless), data and messaging services, and OTT and pay TV services).

The report offers market sizes and forecasts in value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Russia telecom MNO market in 2026?

The Russia telecom MNO market size is USD 17.02 billion in 2026.

What is the growth outlook through 2031?

Revenue is projected to reach USD 20.3 billion by 2031, reflecting a 3.59% CAGR.

Which service category currently leads revenue?

Data and internet services hold 52.03% Russia telecom MNO market share in 2025.

Why are private LTE networks gaining traction?

Industrial firms seek secure, low-latency connectivity and operators offer turnkey managed services that meet sovereignty requirements.

How are sanctions affecting network upgrades?

Western vendor exits force reliance on Chinese and domestic equipment, raising near-term capex and moderating performance gains.

What strategy helps operators offset rising energy costs?

They deploy energy-efficient radios and pursue tower-sharing to lower power per gigabyte while maintaining coverage obligations.

Page last updated on: