Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

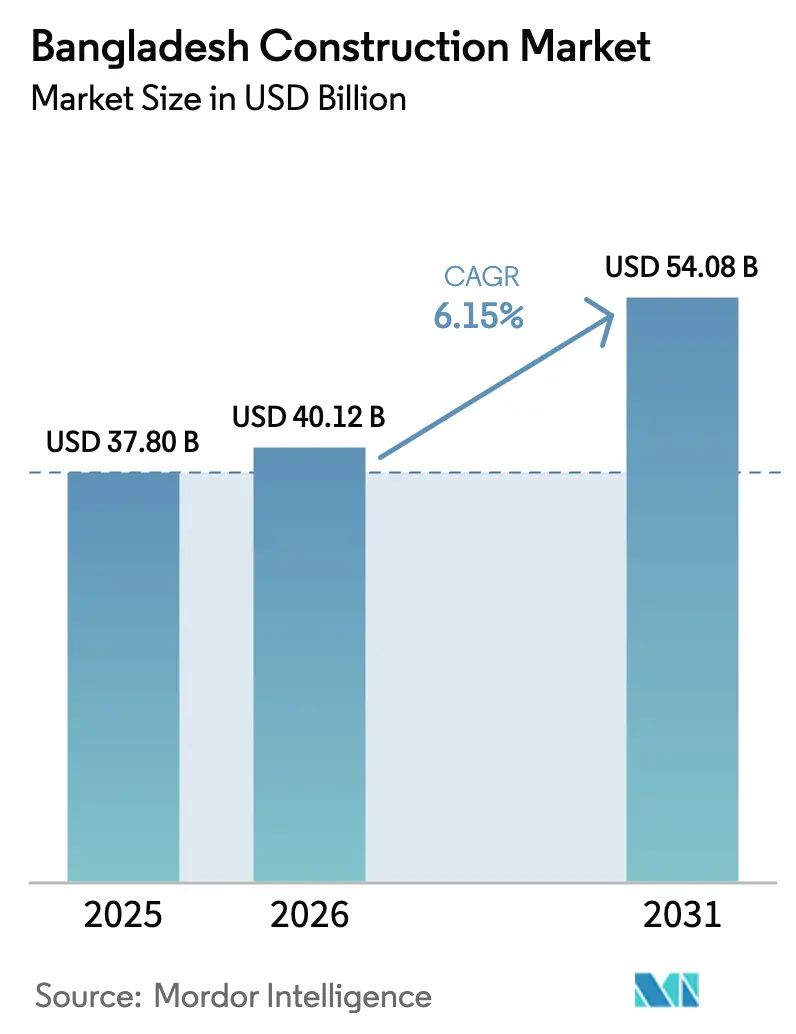

| Base Year Market Size (2025) | USD 37.80 Billion |

| Market Size (2026) | USD 40.12 Billion |

| Market Size (2031) | USD 54.08 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

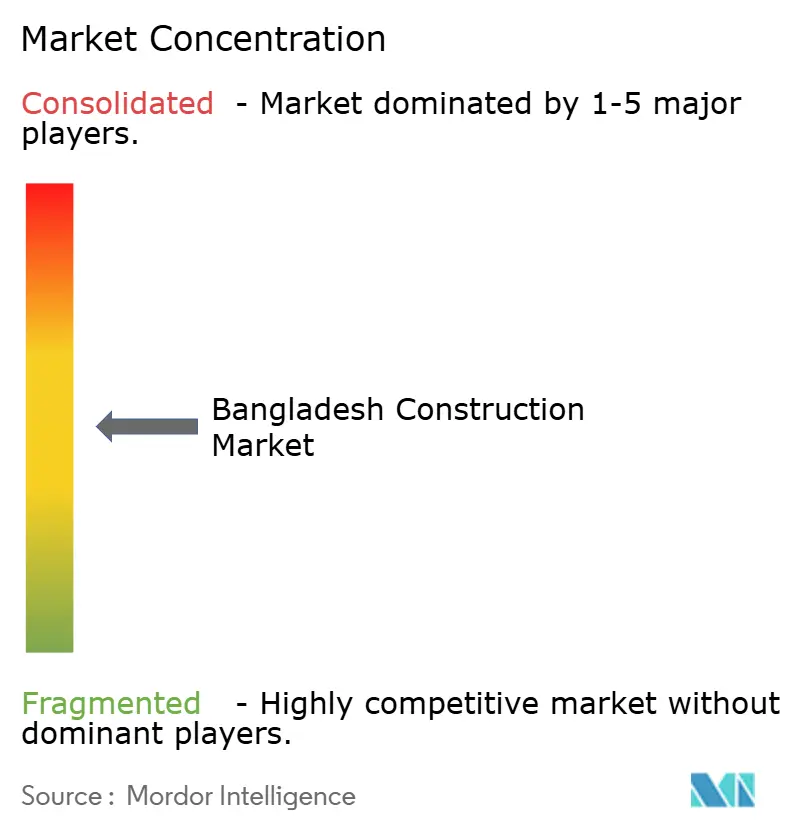

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Construction Market Analysis by Mordor Intelligence

The Bangladesh Construction Market size was valued at USD 37.80 billion in 2025 and is estimated to grow from USD 40.12 billion in 2026 to reach USD 54.08 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

A sizable project pipeline funded by both the annual development program and private real-estate groups is sustaining double-digit bid volumes, while the government’s shift toward contractor-facilitated engineering-procurement-construction (EPC) models continues to accelerate order inflows into the Bangladesh construction market. Steady urbanization, now crossing 39% of the national population, feeds large apartment schemes around Dhaka, Gazipur, and Chattogram, even as factory landlords in export processing zones commission warehouses to meet fast-moving consumer goods (FMCG) and apparel exports. The Bangladesh construction market is also seeing EPC contractors bundle digital design, prefabrication, and modular units to control project timelines amid costlier imported cement clinker and steel. Growing competition among domestic conglomerates and Chinese EPC giants keeps tender prices competitive but has raised demand for equipment leasing and skilled subcontractors in the Bangladesh construction market.

Key Report Takeaways

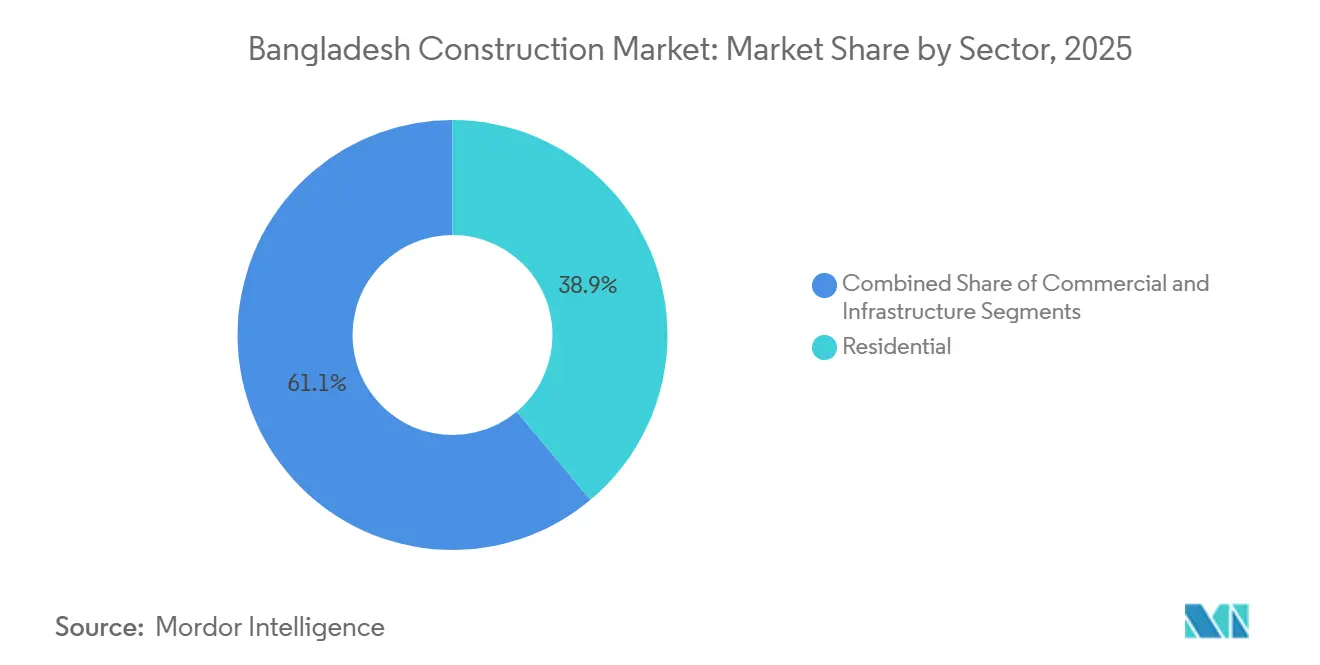

- By sector, residential led with 38.9% revenue share of the Bangladesh construction market in 2025; infrastructure is projected to expand at a 6.94% CAGR through 2031.

- By construction type, new construction held 77.8% of the Bangladesh construction market share in 2025, while renovation is forecast to grow at a 6.61% CAGR over 2026-2031.

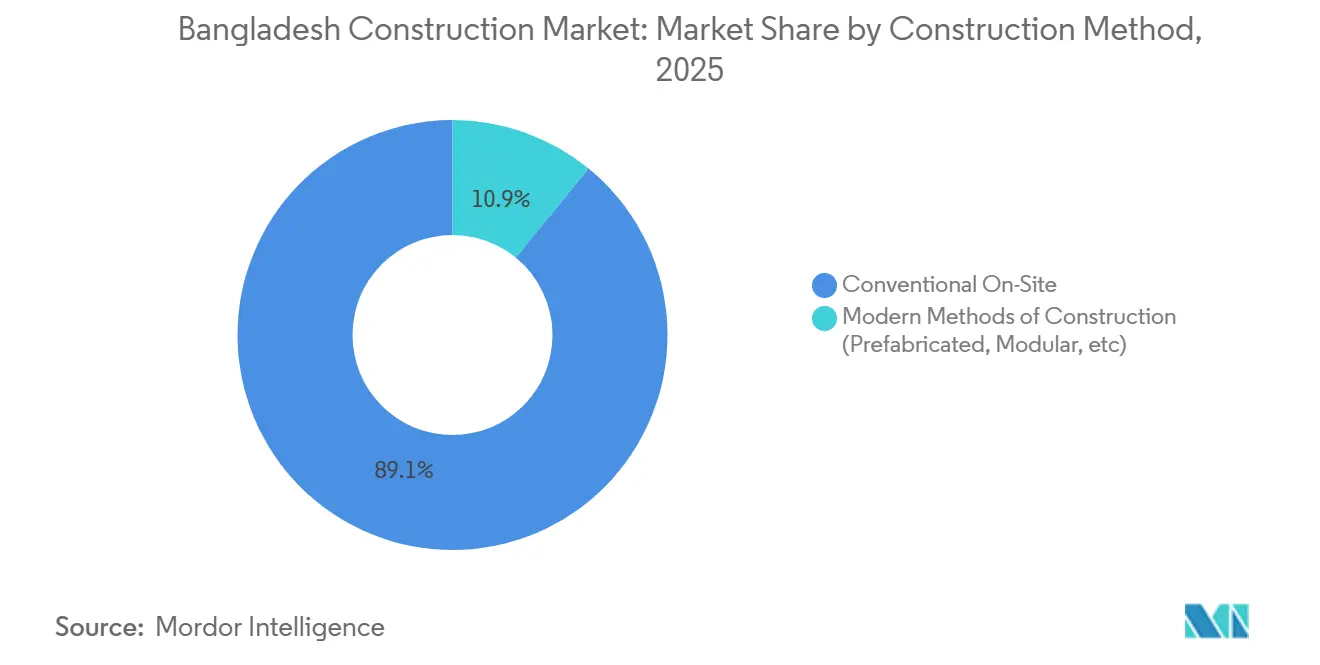

- By construction method, conventional on-site activity accounted for 89.1% of the Bangladesh construction market size in 2025; modern methods of construction are advancing at a 7.03% CAGR to 2031.

- By investment source, private funding dominated with a 55.3% share of the Bangladesh construction market size in 2025; public investment represents the fastest trajectory at 6.55% CAGR.

- By geography, Dhaka captured a 48% share of the Bangladesh construction market size in 2025, while Khulna records the highest forecast growth at 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large public infrastructure programs | +1.1% | National corridors | Long term (≥ 4 years) |

| Rapid industrial expansion | +1.0% | EPZ clusters | Medium term (2–4 years) |

| Urban housing demand | +0.9% | Dhaka & Chattogram | Long term (≥ 4 years) |

| Growth in power and energy projects | +0.8% | Nationwide | Medium term (2–4 years) |

| Rising private commercial investment | +0.7% | Tier-1 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Large Public Infrastructure Programs Expanding Demand for Contractors and EPC Services

Mega schemes such as the Dhaka Elevated Expressway, the Padma Bridge Rail Link, and the Chattogram–Cox’s Bazar rail corridor are awarding multi-year lots that cover bridges, depots, utility relocation, and signaling. These packages elevate backlogs for domestic leaders like Abdul Monem Ltd and Concord Group, while also creating joint-venture opportunities with China Railway Group Bangladesh JV and Larsen & Toubro’s local unit. The financing mix combines concessional lending from the Asian Development Bank with sovereign bonds, insulating milestones from currency swings. Contractors that can integrate prefabricated girders and advanced piling techniques have moved up pre-qualification lists, thereby reinforcing a virtuous cycle of higher margins and specialist subcontractor demand. The sustained pipeline keeps workforce deployment above 4 million laborers in the Bangladesh construction market[1]Asian Development Bank, “South Asia Subregional Economic Cooperation Railway Investment Program,” adb.org .

Rapid Industrial Expansion Increasing Factories, Warehouses, and Utility Construction

Bangladesh’s robust garment export trajectory and the shift toward light engineering have spurred 100 new industrial sheds in the last 18 months across the Savar, Mirsarai, and Ishwardi zones. Large logistic developers such as Summit Communications Infrastructure and GPH Ispat Construction Services are standardizing 30-meter clear-span steel warehouses that integrate rooftop solar and energy-efficient insulation. The demand for utility tie-ins—gas, captive power, and effluent plants—has widened the scope of EPC revenues beyond pure civil works. Material suppliers benefit from higher galvanised sheet volumes, but spot LNG price volatility keeps factory owners keen on shorter construction schedules. This virtuous industrial-real-estate loop feeds incremental steel demand of nearly 800,000 tons per year, anchoring a sizeable portion of the Bangladesh construction market[2]Bangladesh Export Processing Zones Authority, “Industrial Land Allocation Report 2026,” bepza.gov.bd .

Urban Housing Demand Driving Apartment and Township Project Launches

Annual household formation in metropolitan Dhaka alone exceeds 120,000 units, while formal apartment supply hovers at 40,000 units. Developers such as Bashundhara Group and Navana Construction Ltd responded with township blueprints on the city’s periphery that include schools, clinics, and community malls. Flexible mortgage tenures up to 20 years, and the central bank’s refinance window on green buildings, lower entry costs for middle-income buyers. Strong presales allow contractors to adopt just-in-time concrete batching, limiting idle capital in a high-interest environment. Modular bathrooms and pre-cast beams trim floor cycles from 14 to 10 days, enhancing turnover and embedding modern methods of construction into the Bangladesh construction market[3]Ministry of Housing and Public Works, “National Housing Policy Update 2026,” mohpw.gov.bd .

Growth in Power and Energy Projects Supporting Civil and Industrial Construction Activity

The Bangladesh Power Development Board has awarded EPC contracts exceeding USD 3.6 billion for gas-fired, solar, and transmission upgrades since 2025. Substation foundations, turbine halls, and access roads feed sizable concrete and rebar demand, while brownfield capacity additions catalyze specialized retrofitting services. Spectra Engineers Ltd and Sino Hydro Corporation Bangladesh collectively secured over 1 GW of turnkey orders, integrating 3-D laser scanning for clash detection and shortening outage windows. Energy-driven infrastructure absorbs surplus labor during off-peak housing cycles, smoothing revenue volatility for medium-sized contractors. Forward pipelines include 600 km of high-voltage lines that will anchor civil works opportunities through 2028, strengthening the Bangladesh construction market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency depreciation and costlier imports | -0.9% | Nationwide | Short term (≤ 2 years) |

| Financing constraints, higher borrowing costs | -0.8% | Private developers | Medium term (2–4 years) |

| Land acquisition and permitting delays | -0.7% | Expansion corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Depreciation and Import Dependence Increasing Material and Equipment Costs

The Bangladeshi taka depreciated 6.4% against the U.S. dollar between 2025 and 2026, pushing up ex-factory cement and rebar prices, since 25% of clinker and nearly all heavy machinery rely on imports. Contractors struggle to pass through variation costs on fixed-price government contracts, compressing margins across the Bangladesh construction market. Developers who secured letters of credit before the devaluation enjoy a temporary buffer, but upcoming packages face escalated input quotes. In response, procurement teams extend tender validity only 60 days and hedge critical imports in forward markets. The shift also encourages local cement grinding capacity and steel billet expansions to dampen future foreign-exchange exposure.

Financing Constraints and Higher Borrowing Costs Delaying Private Construction Projects

Policy rate hikes totaling 175 basis points since late 2025 lifted commercial loan rates to 13%-14%, straining cash-flow-based project finance. Small and mid-scale developers shelved at least 40 planned condominium towers in Dhaka’s fringe suburbs due to reduced presales and pricier bridge loans. Contractors pivot toward public-sector road packages to maintain equipment utilization, but public-private balance sheets tighten overall liquidity in the Bangladesh construction market. Banks now demand a minimum 30% equity cushion, elongating financial close timelines by up to six months. A gradual shift toward Sukuk and green bonds is observable among large conglomerates, though take-up remains nascent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Remains the Revenue Mainstay

Residential activity commanded 38.9% of the Bangladesh construction market share in 2025 as developer pipelines responded to sustained urban migration and household formation. Condominium clusters along Uttara and Bashundhara R/A reported average floor-price increases of 8% in 2025, improving developer cash flows for reinvestment. The sector benefits from government refinancing lines that cover 5% interest rebates for certified green buildings, encouraging the wider use of solar glass and low-VOC paints. Large builders like Mir Akhter Hossain Ltd have invested in pre-cast floor slabs to accelerate handover cycles, which helps retain early-bird buyers in a competitive mortgage environment.

Infrastructure is projected to be the fastest-growing sector at a 6.94% CAGR between 2026-2031. Port, railway, and expressway expansions, jointly financed by multilateral agencies and the government, account for 62% of this incremental value. Contractors adopt building information modeling (BIM) and drone-based progress monitoring, limiting rework and claims. As a result, infrastructure wins in the Bangladesh construction market stimulate ancillary demand for cement grinding, aggregate quarries, and geotextile suppliers, enhancing multiplier effects on regional economies.

By Construction Type: New Construction Dominates Project Value

New construction represented a commanding 77.8% share of the Bangladesh construction market size in 2025, reflecting a young building stock and limited brownfield retrofits. Accelerated permit clearances for schools and hospitals under the Fast-Track Project initiative further tilted volumes toward greenfield sites. EPC firms standardize blockwork and composite slabs to reduce shuttering cycles, improving gross margins despite wage inflation.

Renovation is forecast to grow at a 6.61% CAGR to 2031 as legacy textile and food-processing plants upgrade to meet environmental and safety audits. Tax rebates covering 20% of retrofit costs under the upcoming Building Energy Efficiency Act catalyze demand for chiller replacements and envelope refurbishments. This niche rewards specialist subcontractors and material companies offering low-carbon cement and recyclable façade panels, broadening the service palette in the Bangladesh construction market.

By Construction Method: Conventional On-Site Work Still Prevails

Traditional on-site techniques accounted for 89.1% of the Bangladesh construction market share in 2025, owing to abundant labor, easy access to raw materials, and familiarity among local crews. Slab-on-grade and column-beam systems remain the default for low-rise residential and institutional projects, sustaining demand for timber formwork and on-site batching plants.

Modern methods of construction are poised for a 7.03% CAGR through 2031 as contractors internalize cost overruns tied to weather delays and rework. Prefabricated bridge girders on the Padma and Meghna corridors demonstrate 20%-time savings versus cast-in-situ solutions. Chinese EPC houses transfer modular tunnel-boring and segment-lining expertise to local partners, while domestic groups invest in concrete slip-form machinery. Wider adoption is expected once standard design codes for modular components are published by the Housing and Building Research Institute, shaping the innovation curve of the Bangladesh construction market.

By Investment Source: Private Capital Leads but Public Funding Gains Momentum

Private investors supplied 55.3% of overall outlays for the Bangladesh construction market in 2025, spearheaded by conglomerates diversifying into real estate and logistics. Developer consortia secure mezzanine funding through non-bank financial institutions that bundle mortgage portfolios into asset-backed securities. Corporate issuers such as Bashundhara Group placed a USD 150 million sukuk in 2025, earmarked for mixed-use high-rises and data centers, reflecting growing capital-market sophistication.

Public investment is expected to expand at a 6.55% CAGR to 2031, driven by sovereign spending on connectivity, climate-resilient embankments, and urban water treatment. Budget allocations under the 8th Five-Year Plan cross USD 75 billion, with nearly one-third tagged for construction. Local content requirements for steel and cement, when combined with a growing reliance on framework contracting, create predictable demand patterns that lessen price volatility and deepen supply-chain integration in the Bangladesh construction market.

Geography Analysis

Dhaka contributed 48% of the Bangladesh construction market size in 2025, cementing its role as the epicenter of residential towers, corporate campuses, and transit-oriented developments. Ongoing metro rail extensions and the expansion of Hazrat Shahjalal International Airport sustain robust tender pipelines, keeping tower cranes visible across the skyline. Land scarcity forces developers into vertical formats, raising average tower heights and fueling the adoption of high-strength concrete mixes.

Khulna, forecast to grow at 7.12% CAGR over 2026-2031, benefits from the Rupsha rail bridge, Mongla Port dredging, and eco-tourism projects along the Sundarbans buffer zone. Improved connectivity shortens supply-chain nodes for jute, shrimp, and ship-building clusters, stimulating factory expansions and worker housing demand. Local governments offer expedited land conversion permits and property tax holidays to court investors, gradually diversifying the regional economic base and integrating new entrants into the Bangladesh construction market.

Other regions, such as Chattogram and Sylhet, continue steady growth aligned with export-handling and remittance-fueled housing, yet remain secondary to the twin engines of Dhaka and Khulna. As inland river port PPPs mature, contractors position equipment yards along the Padma-Jamuna corridor, lowering mobilization times for multi-site builds and capturing cross-district efficiencies.

Competitive Landscape

Competition in the Bangladesh construction market revolves around a three-tier hierarchy. First-tier conglomerates—Bashundhara Group, Abdul Monem Ltd, and Concord Group—hold diversified portfolios spanning cement, steel, and real-estate development, enabling vertical cost control. They routinely form joint ventures with Chinese engineering companies to bid for mega infrastructure lots, leveraging imported know-how for complex geotechnical challenges.

Mid-tier firms such as Max Infrastructure Ltd, Navana Construction Ltd, and Spectra Engineers Ltd focus on transportation and utility projects under USD 200 million, where local relationship capital and price competitiveness outweigh technology depth. These players sped up capacity investments, adding mobile asphalt plants and European tower cranes to meet tighter project delivery windows. Bank guarantee ceilings, however, limit their exposure to simultaneous large packages.

Specialist contractors—including GPH Ispat Construction Services and Rahimafrooz Construction & Engineering—anchor niche verticals such as steel erection and renewable-energy balance-of-plant. Their agility allows rapid deployment in industrial corridors, capturing repeat orders from foreign direct investors seeking turn-key reliability. Across all tiers, environmental, social, and governance (ESG) compliance now shapes pre-qualification scores, nudging companies toward ISO 45001 safety certifications and ESG reporting, an emerging differentiator in the Bangladesh construction market.

Bangladesh Construction Industry Leaders

Bashundhara Group

Mir Akhter Hossain Ltd

Abdul Monem Ltd

Max Infrastructure Ltd

Navana Construction Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Government of Bangladesh initiated the Padma Barrage Project, a major water infrastructure project on the Padma River with an estimated cost of BDT 50,443 crore (USD 4.6 billion). The project is designed to improve irrigation, store water, and support power generation, helping strengthen long-term water management infrastructure in the country.

- October 2025: The European Investment Bank (EIB) approved EUR 160 million (USD 172 million) in additional financing for two water security projects in Dhaka. These projects aim to improve the city’s water supply and sanitation infrastructure.

- August 2025: The Mawlana Bhasani Bridge in Rangpur Division was inaugurated with a construction cost of BDT 925 crore (USD 84 million). The bridge improves transportation and connectivity across the Teesta River, supporting regional infrastructure development.

Bangladesh Construction Market Report Scope

By Sector

| Residential | Apartments / Condominiums |

| Villas / Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial & Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, Others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc.) |

By Investment Source

| Public |

| Private |

By Geography

| Dhaka |

| Chittagong |

| Khulna |

| Rest of Bangladesh |

| By Sector | Residential | Apartments / Condominiums |

| Villas / Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial & Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, Others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc.) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Dhaka | |

| Chittagong | ||

| Khulna | ||

| Rest of Bangladesh | ||

Key Questions Answered in the Report

How fast is overall construction activity expected to grow in Bangladesh during 2026-2031?

It is projected to expand at a 6.15% CAGR, lifting the Bangladesh construction market size to USD 54.08 billion by 2031.

Which sector currently generates the highest construction spending?

Residential developments deliver 38.9% of the total 2025 value, driven by sustained urban housing demand.

Where is the strongest regional growth expected?

Khulna is forecast to lead with 7.12% CAGR as port, rail, and eco-tourism investments scale up.

What construction method is gaining traction for productivity gains?

Modern methods of construction, including prefabricated and modular solutions, are advancing at a 7.03% CAGR through 2031.

How are contractors responding to currency-driven cost pressures?

Firms hedge import exposures, localize material sourcing, and adopt prefabrication to compress build times and protect margins.

Which companies hold notable influence in large infrastructure awards?

Bashundhara Group, Abdul Monem Ltd, Concord Group, and their joint ventures with Chinese EPC firms consistently capture mega-project packages.

Page last updated on: