Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.35 Trillion |

| Market Size (2026) | USD 1.41 Trillion |

| Market Size (2031) | USD 1.76 Trillion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

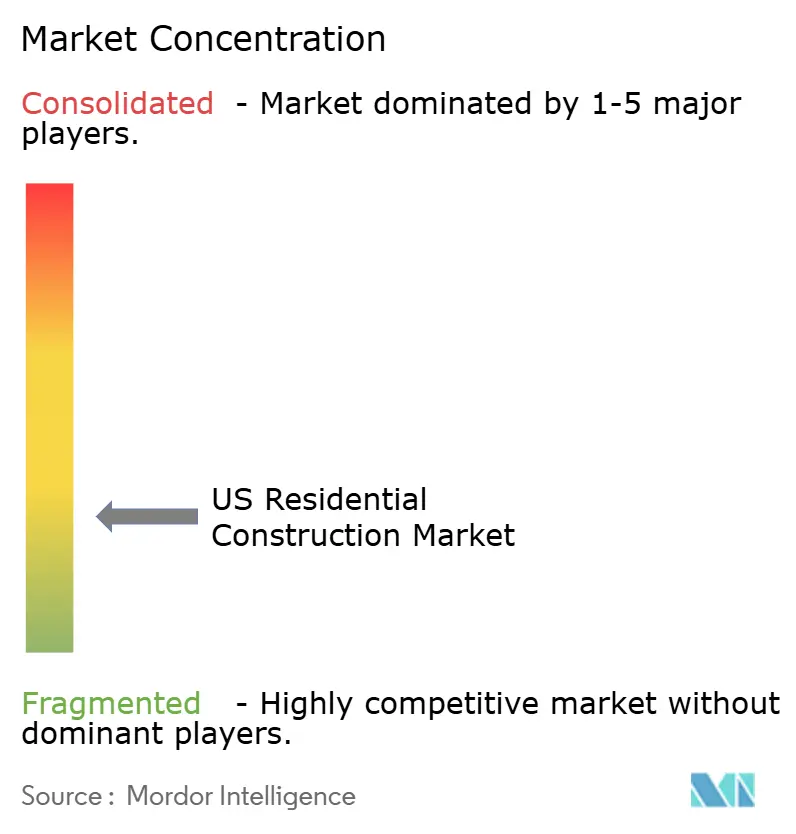

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Residential Construction Market Analysis by Mordor Intelligence

The US residential construction market size in 2026 is estimated at USD 1.41 trillion, growing from 2025 value of USD 1.35 trillion with 2031 projections showing USD 1.76 trillion, growing at 4.53% CAGR over 2026-2031. Robust demographic momentum, larger institutional capital allocations, and accelerated technology adoption anchor this expansion, even as developers navigate cyclical mortgage-rate shifts. Migration toward Sun Belt metros, supportive zoning reforms, and federal energy-efficiency incentives widen the demand base. Builders increasingly differentiate through prefabrication, 3-D printing, and data-driven project management platforms, while shifting insurance and water-supply risks compel geographic diversification. Collectively, these forces recast the US residential construction market as a strategic infrastructure opportunity rather than a short-cycle, rate-sensitive play.

Key Report Takeaways

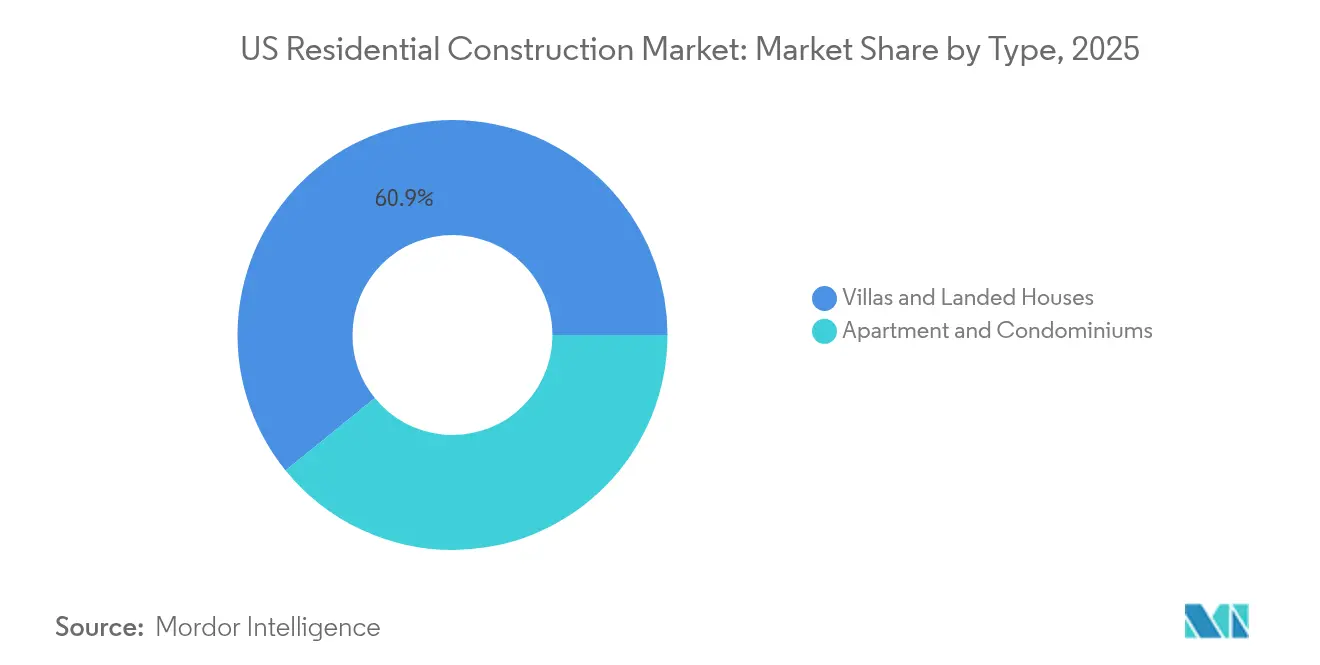

- By type, villas and landed houses accounted for 60.85% of the US residential construction market size in 2025; apartments and condominiums are forecast to expand at a 6.02% CAGR through 2031.

- By construction type, new-build activity represented 69.05% of the US residential construction market share in 2025, whereas renovation is projected to grow at a 5.61% CAGR through 2031.

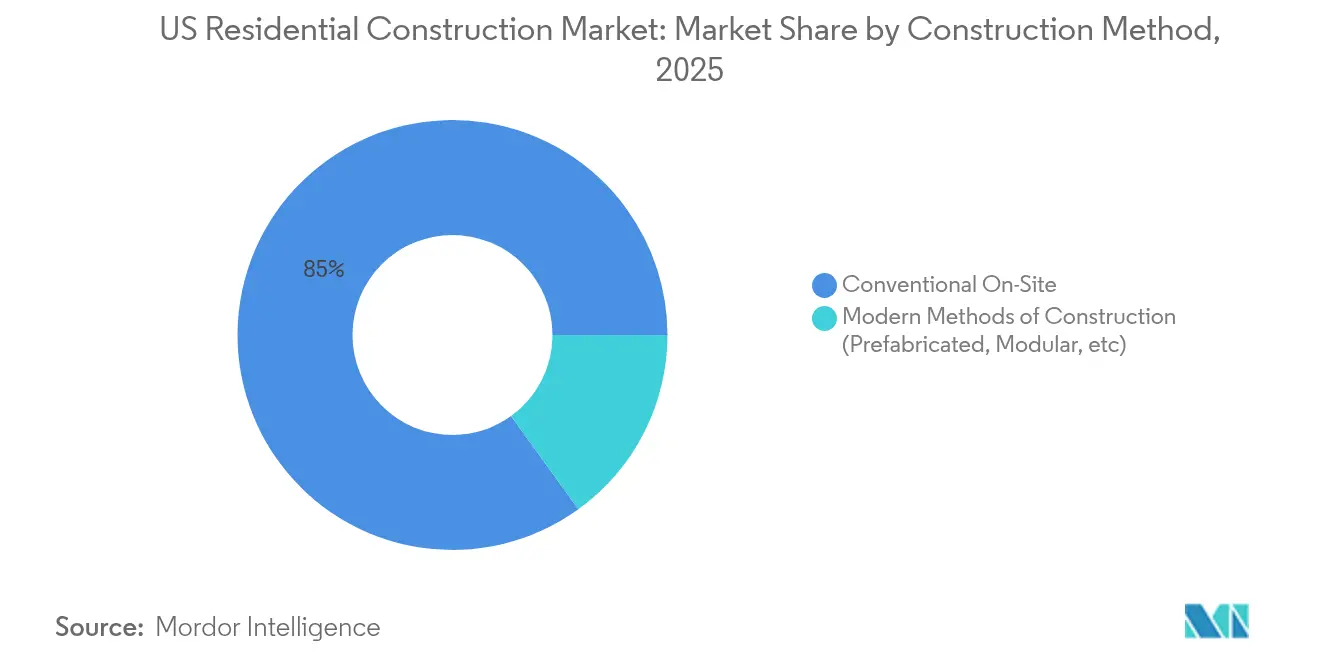

- By construction method, conventional on-site techniques comprised 84.95% of the US residential construction market size in 2025; modern methods of construction are growing at a 7.62% CAGR through 2031.

- By investment source, private capital captured 91.92% of the US residential construction market share in 2025, while public funding is set to rise at a 6.63% CAGR through 2031.

- By region, the Southeast held 41.12% of the US residential construction market share in 2025, while the West is advancing at a 5.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling mortgage rates improve affordability | +1.2% | National, with stronger impact in Northeast and West | Medium term (2-4 years) |

| Millennial household formation surge | +0.8% | National, concentrated in Southeast and West growth corridors | Long term (≥ 4 years) |

| Institutional build-to-rent capital inflows | +0.7% | Southeast and West primary markets, expanding to secondary metros | Medium term (2-4 years) |

| Aging housing stock fuels remodeling | +0.6% | National, with emphasis on Northeast and Midwest legacy markets | Long term (≥ 4 years) |

| State-level zoning reforms for higher density | +0.5% | West Coast states, expanding to Northeast progressive municipalities | Long term (≥ 4 years) |

| IRA heat-pump tax credits accelerate retrofits | +0.4% | National, with higher adoption in cold-climate regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Falling Mortgage Rates Improve Affordability

Mortgage rates trending down from 7% to near-6% by late 2025 restores roughly 15% additional buying power, stimulating new-home demand across price points. The easing rate backdrop loosens the “rate-lock” that kept existing owners sidelined, pushing more buyers toward new construction. First-time purchasers now form the majority of funded loans and favor energy-efficient, tech-ready dwellings. Builders respond with smaller footprints and smart-home packages, especially in job-rich secondary metros. The combined effect is a broader, more resilient demand curve, cushioning the US residential construction market against future rate volatility.

Millennial Household Formation Surge

Millennials aged 28-43 will contribute roughly 70% of new household creation through 2030, driving structural demand that transcends short-term economic swings. Their preference for walkable, amenity-rich communities accelerates higher-density projects near transit nodes. The cohort’s digital expectations make touchless entry, solar integration, and app-based maintenance indispensable. Sun Belt metros such as Austin and Raleigh draw outsized interest due to lower living costs and robust job pipelines. This demographic wave underpins long-run volume visibility across both single-family and multifamily segments[1]U.S. Department of the Treasury, “IRA Home Energy Rebates,” home.treasury.gov.

Institutional Build-to-Rent Capital Inflows

Institutional investors deploy more than USD 50 billion annually into single-family rental and build-to-rent (BTR) communities, reshaping product standards and volume requirements. BTR developments favor standardized floor plans, durable finishes, and centralized maintenance, raising per-unit costs but enhancing lifecycle economics. Capital concentration in Sun Belt metros pushes construction capacity to its limits, prompting greater use of modular and panelized solutions. Investors’ focus on predictable cash flows further lifts demand for low-carbon, low-maintenance materials. As a result, the BTR wave embeds a new, stable customer segment within the US residential construction market.

Aging Housing Stock Fuels Remodeling

The median US home is roughly 40 years old, and 38% of dwellings pre-date 1980, requiring major system upgrades. Energy-efficiency retrofits spurred by federal credits average USD 25,000-50,000 and include heat-pump installations now eligible for 30% tax incentives. Renovations frequently reach project values on par with new builds in land-constrained metros, effectively expanding construction workloads. Contractors that balance renovation and ground-up pipelines can mitigate cyclical swings, while specialized trades HVAC, insulation, and electrical, see sustained demand and wage premiums. The retrofit boom thus adds a secular layer to the US residential construction market growth profile.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortages | -0.9% | National, with acute impacts in high-growth Sun Belt markets | Medium term (2-4 years) |

| Volatile material costs | -0.6% | National, with regional variations based on transportation costs | Short term (≤ 2 years) |

| Insurance-premium spikes in climate-risk zones | -0.4% | Coastal regions and wildfire-prone areas in West | Long term (≥ 4 years) |

| Water-scarcity building moratoriums | -0.3% | Southwest region, particularly Arizona and Nevada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages

Construction payrolls remain nearly 400,000 workers below their 2007 peak, inflating wages by 15-20% in fast-growing metros. Scarcity in specialized trades elongates schedules and forces builders to retain larger in-house teams or pay premium rates to subcontractors. Immigration policy uncertainty compounds regional gaps, particularly in Texas and Florida. These pressures accelerate investment in robotics, prefabrication, and 3-D printing, yet ramp-up periods limit near-term relief. Consequently, labor scarcity drags on projected output and margins across the US residential construction market.

Volatile Material Costs

Lumber prices have oscillated between USD 300 and 1,200 per thousand board feet since 2023, undermining cost visibility. Steel, concrete, and copper likewise swing on global supply disruptions and tariff shifts, adding 8-12% budget risk. Large public builders hedge with forward contracts, whereas small contractors absorb margin shocks or reprice jobs mid-cycle. Regional freight disparities further widen delivered-cost gaps, nudging development toward material-adjacent markets. Persistent volatility tempers risk appetite within the US residential construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Apartments Lead Urban Density Shift

Apartments and condominiums captured 39.15% of 2025 output, trailing single-family formats yet posting the segment’s fastest 6.02% CAGR to 2031, powered by zoning liberalization and institutional capital demand. Investor appetite for scale-ready, rent-generating assets and millennial preferences for walkable communities converge to lift multifamily pipelines in transit-oriented corridors. Projects increasingly integrate co-working lounges, EV-ready parking, and centralized package lockers to serve digital lifestyles.

Single-family construction adapts through smaller lots, paired homes, and community amenities that mimic urban convenience. Builders such as D.R. Horton have rolled out detached rental lines in Texas and Florida, reflecting cross-pollination between segments. Land availability and appraisal norms still anchor villas and landed houses at 60.85% of 2025 volume, but higher-density formats steadily chip away as municipalities pursue housing-supply mandates. Overall, product-mix evolution widens the addressable US residential construction market.

By Construction Type: Renovation Accelerates

New-build activity retained a 69.05% share in 2025, yet renovation projects expanded faster at a 5.61% CAGR on the back of aging stock and tax-credit support. Energy-retrofit packages, kitchen expansions, and accessory-dwelling-unit conversions push typical budgets above USD 75,000, rivaling entry-level new builds. Contractors specializing in occupied-home workflows gain pricing power and repeat business.

Project pipelines swell in legacy Northeast and Midwest neighborhoods where land scarcity curtails ground-up development. Builders such as Lennar have launched dedicated remodeling divisions to hedge cycle risk and meet customer demand. The robust retrofit niche, therefore, deepens the resilience of the US residential construction market size.

By Construction Method: Modern Techniques Gain Ground

Conventional on-site processes accounted for 84.95% of 2025 output, but modern methods, modular, panelized, and 3-D printed, are growing at a 7.62% CAGR to 2031. Off-site fabrication slashes on-site labor by up to 40% and curtails weather delays, appealing in high-wage and climate-variable regions.

Large national builders partner with tech startups to scale panel plants and robotic framing lines. HUD’s USD 600,000 research grants for 3-D printed homes in Alaska spotlight policy support. Although code acceptance and freight logistics still constrain adoption, modern techniques are poised to lift quality and speed, reinforcing productivity across the US residential construction industry.

By Investment Source: Private Capital Dominates

Private entities funded 91.92% of 2025 spending, but public investment is accelerating at a 6.63% CAGR via HUD grants and state housing bonds. Federal programs such as the USD 225 million PRICE initiative target manufactured-housing community upgrades, catalyzing contractor demand in affordability-constrained regions.

Public–private partnerships pair municipal land with builder expertise to meet inclusionary mandates. States like California layer tax-exempt bonds and density bonuses, while Florida leans on private BTR ecosystems. The blended financing mix enlarges the funnel of shovel-ready projects, enhancing liquidity across the US residential construction market.

Geography Analysis

The Southeast maintained a 41.12% share in 2025, buoyed by corporate relocations, population inflows, and pro-growth zoning. Florida’s metro corridors from Orlando to Tampa lead permit issuances, while Georgia and North Carolina attract logistics and tech employers that underpin housing demand. Streamlined approvals and abundant developable land allow large master-planned communities to scale rapidly, sustaining volume even amid credit-cycle noise.

In contrast, the West posts the fastest 5.71% CAGR through 2031 despite elevated regulatory overhead. California’s density mandates, Oregon’s duplex allowances, and Colorado’s water-conservation incentives reshape format mix toward townhomes and mid-rise apartments. Phoenix developers navigate water-availability tests yet still launch 10,000-plus unit pipelines, often leveraging modular-frame solutions to offset labor scarcity. Technology-sector wages in Seattle and Silicon Valley support premium pricing, cushioning margin risks from stringent green-building codes.

The Northeast’s resurgence shows 57.9% monthly and 109.3% year-over-year housing-start gains, reversing years of underbuilding. Pennsylvania’s chronic shortage triggers by-right approvals and infrastructure earmarks, while Massachusetts expands transit-oriented zoning to spur mixed-use blocks. Retrofits of pre-war housing in New York City and Boston absorb specialized trades, limiting labor leakage to new-build tracts. The Midwest and Southwest maintain steady trajectories near the national average, balancing affordability and available acreage without the boom-and-bust extremes seen elsewhere. Altogether, regional diversity distributes risk and opportunity across the US residential construction market.

Competitive Landscape

Competition remains fragmented, with regional specialists holding strong municipal relationships while national giants exploit scale advantages in land and procurement. D.R. Horton, Lennar, and PulteGroup leverage bulk-buy power to hedge commodity swings, whereas local firms win on bespoke design and customer intimacy. Technology adoption differentiates across the board: AI-driven estimating, VR sales tours, and BIM-enabled clash detection compress cycle times and error rates[3]U.S. Securities and Exchange Commission, “D.R. Horton 10-K,” sec.gov.

Strategic acquisitions accelerate consolidation; Sekisui House’s USD 4.9 billion purchase of M.D.C. Holdings created the fifth-largest builder and imported Japanese zero-energy techniques to U.S. sites. Asahi Kasei’s takeover of ODC Construction secures specialty framing capacity in Florida’s tight labor market. Simultaneously, boutique firms form land-bank JVs or convert to BTR specialists, catering to institutional mandates while avoiding volume race dynamics.

Product innovation also reshapes contestable ground. Manufactured-housing leaders roll out HUD-compliant models with site-built aesthetics, expanding affordability reach. Builders in wildfire zones adopt steel framing, cementitious siding, and fire-resistant landscaping to restore insurer confidence. Overall, competitive intensity pivots from sheer lot counts toward technology, risk management, and capital-partner alignment, a shift that strengthens the structural underpinnings of the US residential construction market.

US Residential Construction Industry Leaders

D.R. Horton

Lennar Corp.

PulteGroup

NVR

Taylor Morrison

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sekisui House finalized its USD 4.9 billion M.D.C. Holdings acquisition, creating a 15,067-closing platform across 16 states.

- December 2024: HUD issued a temporary waiver on Build America, Buy America solar-module rules to expedite USD 20 billion in domestic manufacturing plans.

- September 2024: HUD released final rules revising Manufactured Home Construction and Safety Standards, effective Mar 2025.

- August 2024: Asahi Kasei Homes acquired Florida-based ODC Construction to bolster framing and foundation capacity

US Residential Construction Market Report Scope

Residential construction is a process that involves the expansion, renovation, or construction of a new home or spaces intended to be occupied for residential purposes. These spaces can be anything from rental spaces, condominiums, and luxury mansions, to single-family housing projects. The United States residential construction market is segmented by Type (Single Family, and Multi-Family), by Construction Type (New Construction and Renovation), and by City (New York City, Los Angeles, San Francisco, Washington DC, Miami, and Other Cities). The report offers market sizes and forecasts for the United States residential construction market (in USD Billion) for all the above segments.

By Type

| Apartment & Condominiums |

| Villas and Landed Houses |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Region

| Northeast (New York, Massachusetts, Pennsylvania, etc.) |

| Midwest (Illinois, Ohio, Michigan, etc.) |

| Southeast (Florida, Georgia, North Carolina, etc.) |

| West (California, Washington, Colorado, etc.) |

| Southwest (Texas, Arizona, New Mexico, etc.) |

| By Type | Apartment & Condominiums |

| Villas and Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) | |

| By Investment Source | Public |

| Private | |

| By Region | Northeast (New York, Massachusetts, Pennsylvania, etc.) |

| Midwest (Illinois, Ohio, Michigan, etc.) | |

| Southeast (Florida, Georgia, North Carolina, etc.) | |

| West (California, Washington, Colorado, etc.) | |

| Southwest (Texas, Arizona, New Mexico, etc.) |

Key Questions Answered in the Report

What is the current size of US residential construction in 2026?

Spending stands at USD 1.41 trillion in 2026.

What growth rate is forecast for US residential construction through 2031?

Total spending is projected to reach USD 1.76 trillion by 2031, translating into a 4.53% CAGR.

Which region leads US residential construction output?

The Southeast accounts for 41.12% of 2025 activity and maintains the top regional position.

Which product segment is expanding the fastest?

Apartments and condominiums are advancing at a 6.02% CAGR through 2031, outpacing all other formats.

How much of total spending is funded by private capital?

Private investors provide 91.92% of 2025 outlays, making them the dominant funding source.

Which construction method is gaining ground the quickest?

Modern methods of construction—such as modular and panelized building—are growing at a 7.62% CAGR through 2031.

Page last updated on: