Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

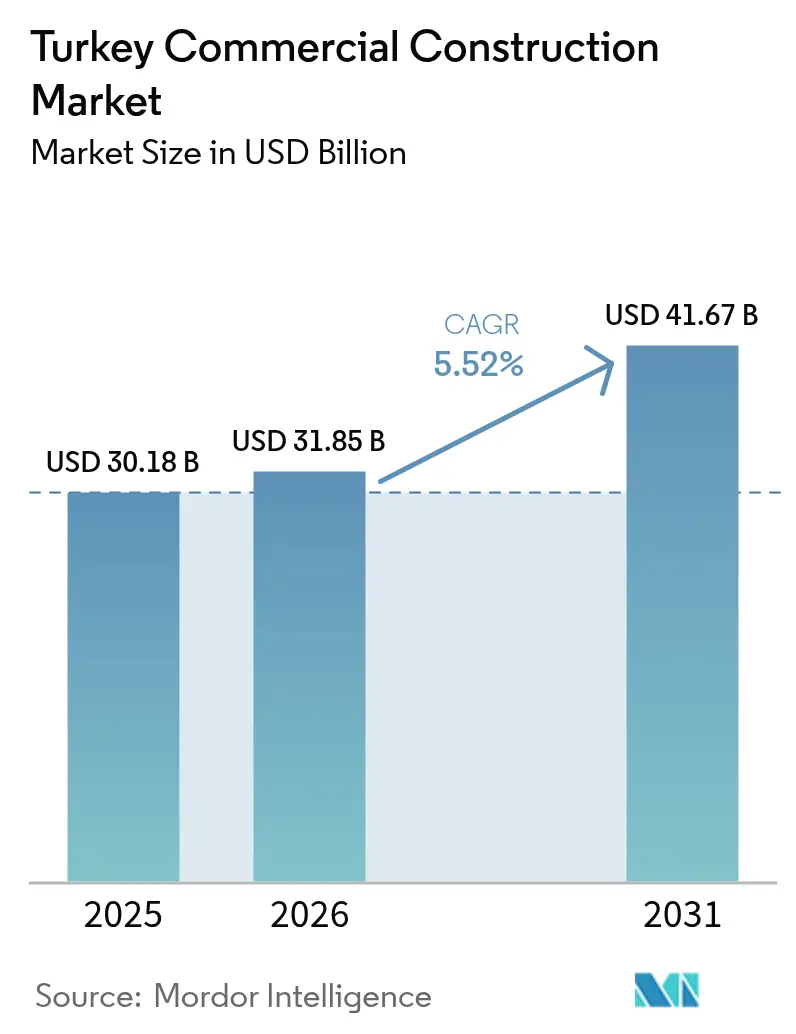

| Base Year Market Size (2025) | USD 30.18 Billion |

| Market Size (2026) | USD 31.85 Billion |

| Market Size (2031) | USD 41.67 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

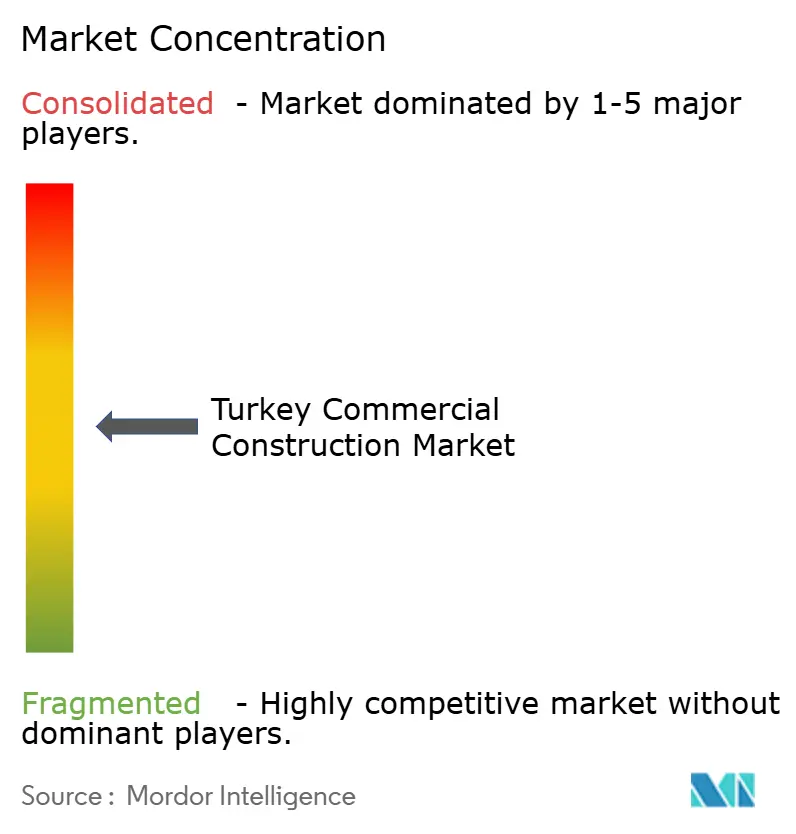

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Commercial Construction Market Analysis by Mordor Intelligence

Turkey Commercial Construction Market size in 2026 is estimated at USD 31.85 billion, growing from 2025 value of USD 30.18 billion with 2031 projections showing USD 41.67 billion, growing at 5.52% CAGR over 2026-2031. Private capital continues to fund two-thirds of new projects, yet the 2025 federal budget channels an additional USD 20.86 billion into disaster-resilience and urban-transformation work, reinforcing the market’s medium-term momentum. Robust gross domestic product growth averaging 5.4% between 2003 and 2023, a median population age of 31 years, and more than USD 204 billion of public-private partnership (PPP) infrastructure deals since 1986 are enlarging demand for offices, retail centers, and logistics hubs. Logistics construction is pacing ahead as e-commerce volumes climb, while seismic-retrofit mandates are igniting a sizable renovation pipeline. Currency volatility and permitting bottlenecks still weigh on developer margins, yet rising LEED uptake and government green-taxonomy rules are nudging supply toward higher-quality, energy-efficient stock.

Key Report Takeaways

- By commercial sector type, retail led with 37.25% revenue share in 2025, while industrial & logistics is projected to grow at a 6.73% CAGR through 2031.

- By construction type, new-build work accounted for 74.15% of the Turkey commercial construction market share in 2025; renovation registers the fastest 6.48% CAGR to 2031.

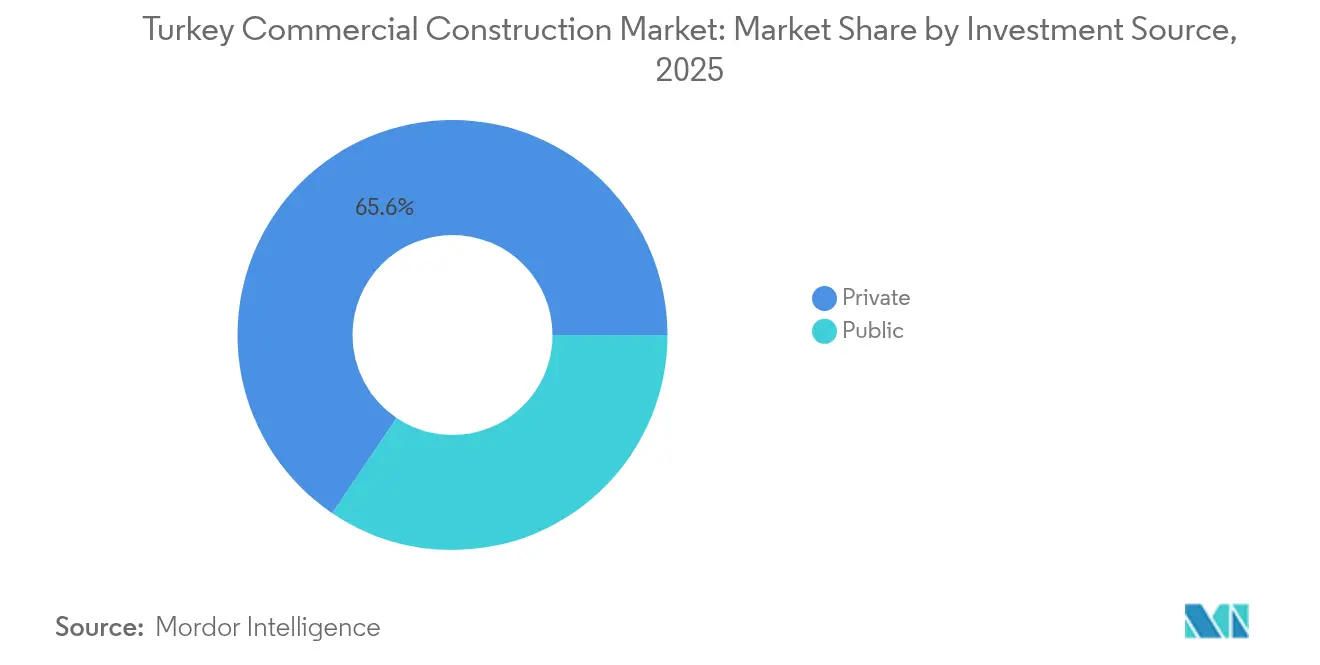

- By investment source, private funding dominated 65.55% of the Turkey commercial construction market size in 2025, whereas public expenditure is expected to advance at a 6.22% CAGR through 2031.

- By city, Istanbul held 42.15% of the 2025 value; Izmir is on course for the quickest 6.9% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Commercial Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic recovery and rising business activity | +1.2% | Istanbul, Ankara, Izmir | Medium term (2-4 years) |

| Rapid urbanization boosting mixed-use demand | +0.9% | Nationwide, strongest in big three cities | Long term (≥ 4 years) |

| Government infrastructure outlays | +0.8% | Nationwide, metro corridors | Medium term (2-4 years) |

| E-commerce-led logistics expansion | +0.7% | Major and secondary cities | Short term (≤ 2 years) |

| High office occupancy in Istanbul | +0.5% | Istanbul metro area | Short term (≤ 2 years) |

| Supportive green-building policies | +0.4% | Early adopters in large cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Economic recovery and rising business activity

Turkey's economic recovery is gaining momentum, driven by improved macroeconomic stability and rising business activity. Turkey's macroeconomic landscape has found stability, thanks to upgrades from leading rating agencies, bolstered foreign-exchange reserves, and a significantly reduced current-account deficit. This newfound stability has rejuvenated corporate confidence. As a result, multinationals, particularly in finance, technology, and professional services, are expanding their presence in Istanbul and Ankara. The National Digital Transformation Strategy (2024-2028) is now honing in on attracting foreign direct investment (FDI) in sectors like semiconductors, AI, and e-commerce. These sectors, in turn, necessitate specialized labs, data centers, and flexible office spaces. With employment on the rise and household incomes improving, retailers are opting for larger spaces, and developers are hastening the launch of grade-A projects. However, the trajectory of this progress is contingent on maintaining a disinflationary approach that safeguards purchasing power and ensures credit remains affordable. Turkey's ability to sustain this growth will depend on its commitment to these economic strategies[1]Central Bank of the Republic of Türkiye, “Balance of Payments Statistics December 2024,” cbrt.gov.tr.

Rapid urbanization boosting mixed-use demand

Rapid urbanization in Turkey is reshaping the real estate landscape, driving the demand for mixed-use developments. Every year, Turkey's cities welcome approximately one million new residents. This influx tightens the supply of downtown land and amplifies the demand for integrated complexes that blend offices, retail, and residential spaces. Urban-renewal corridors in Ankara and Izmir are already showcasing these integrated schemes. Meanwhile, the Halkalı-Kapıkule high-speed line has spurred a 5-8% rise in property prices across Thrace, leading to the emergence of transit-oriented malls and co-working clusters. The Smart Cities Department, operating under the Environment Ministry, is aligning zoning regulations with digital infrastructure. This initiative promotes the integration of IoT-ready specifications and eco-friendly materials by private developers. As urban centers evolve, suburban nodes and satellite towns are expected to increasingly cater to the demand for neighborhood-scale commercial hubs, marking a significant shift in Turkey's urban development.

Government infrastructure outlays

Turkey continues to demonstrate its commitment to infrastructure development through significant investments and ambitious projects. Since 1986, Turkey has committed a staggering USD 204 billion to Public-Private Partnership (PPP) projects, highlighting its ambitious infrastructure goals. In 2024, nearly half (49%) of the spending is earmarked for rail projects. By 2028, the ongoing motorway program aims to expand tolled lanes to an impressive 4,728 kilometers. Major undertakings, like the USD 15 billion Istanbul Canal and the construction of 740 kilometers of new tunnels, are not just standalone projects; they're catalyzing the development of adjacent hotel plots, logistics land banks, and premium office spaces. Additionally, the 2025 budget allocates a significant USD 20.86 billion for disaster-risk reduction, attracting contractors with expertise in resilient commercial constructions. These efforts underline Turkey's vision for a robust and future-ready infrastructure landscape.

E-commerce-led logistics expansion

The rapid growth of e-commerce is significantly influencing logistics strategies in Turkey. As online retail volumes surge, site selection is transforming. Academic models have identified Konya, Eskisehir, and Ankara OIZs as the top trio for cost-effective logistics, thanks to their highway connectivity and closeness to major consumption zones. Developers are now prioritizing features like automated storage, multi-temperature bays, and customs-bonded areas for cross-border trade. Additionally, mixed-retail outlet centers linked to airports are catering to the "shop & ship" demand from travelers. With the rise of same-day delivery expectations, there's an increasing demand for mid-box distribution sheds in secondary cities. The evolving logistics landscape underscores the critical role of infrastructure and innovation in meeting e-commerce demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency depreciation & inflation | -0.8% | Import-reliant provinces | Short term (≤ 2 years) |

| Complex permitting procedures | -0.6% | Large metros | Medium term (2-4 years) |

| High material & labor costs | -0.5% | Nationwide | Short term (≤ 2 years) |

| Earthquake-driven compliance expenses | -0.4% | Western & Southern high-seismic zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency depreciation & inflation

Currency depreciation and inflation continue to pose significant challenges for developers, impacting project costs and financial planning. In the face of rising price pressures, the 2025 fiscal plan anticipates a robust 50.37% growth in tax receipts. Cement, rebar, and façade packages are already feeling the pinch. Projects relying on imported HVAC systems and lift equipment find themselves vulnerable to the whims of exchange-rate fluctuations. As a result, developers are increasingly turning to hedging strategies or localizing their procurement. Meanwhile, elevated policy rates are tightening financial conditions, leading to extended payback periods for speculative builds. In this challenging landscape, sophisticated inventory controls and just-in-time deliveries have emerged as crucial levers for cost containment. Adapting to these dynamics will be critical for developers to sustain profitability and manage risks effectively.

Earthquake-driven compliance expense

Earthquake-driven compliance expenses are becoming a critical concern for Turkey's construction sector. Turkey's 2018 Building Seismic Code mandates heightened design and construction standards, particularly challenging for high-rise offices and critical service centers. While retrofitting the nation's vulnerable structures is projected to cost USD 500 billion over two decades, the recent 2023 Kahramanmaraş tragedy serves as a stark reminder of the dire consequences of inaction. Though measures like advanced structural analysis, seismically isolated foundations, and stringent inspections inflate initial costs, they promise significant savings in long-term liabilities and insurance expenses. Proactive compliance with these regulations is essential to safeguard lives and mitigate financial risks in the future.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commercial Sector Type: Logistics Gains Ground on Dominant Retail

Retail remained the largest slice of the Turkey commercial construction market with a 37.25% share in 2025, buoyed by population density and rising disposable incomes. Developers continue to refresh prime high-street assets, yet many new malls embed dark-store wings and micro-fulfillment nodes to serve hybrid shoppers. The industrial & logistics category is the clear growth engine, forecast to expand at 6.73% CAGR through 2031 as cross-border e-commerce and near-shoring lift warehouse demand.

Most recent leases involve 30,000–70,000 m² big-box units in the Marmara and Central Anatolia regions, coordinated with highway extensions and rail freight spurs. Brands such as Trendyol and Hepsiburada have pre-let entire phases of speculative parks, ensuring cash flow for developers. Offices follow with a stable pipeline driven by Istanbul’s finance focus, while mixed-use schemes add hospitality and entertainment functions to diversify revenue.

By Construction Type: New-Build Dominance Faces Seismic-Led Retrofit Wave

New projects captured 74.15% of 2025 spending, confirming Turkey’s appetite for fresh stock that meets modern sustainability and digital criteria. Iconic ground-ups like the Istanbul Canal-adjacent trade zone integrate smart grids and district cooling from day one. Renovation is catching up, advancing at a 6.48% CAGR as asset owners implement mandated seismic upgrades and energy-efficiency retrofits.

The Turkey commercial construction market size tied to renovation projects is projected to widen sharply once municipal enforcement accelerates in 2026. Over one-third of all Turkish LEED certificates already involve existing-building overhauls, signalling developer willingness to modernise rather than rebuild. World Bank-funded pilots demonstrate that blended seismic-plus-energy improvements can lower lifecycle costs, unlocking green financing at preferential rates.

By Investment Source: Public Spend Narrows Gap with Private Capital

Private developers provided 65.55% of funding in 2025, leveraging competitive tax policies and the depth of domestic contractors. Banks typically require 40% pre-lease covenants, but foreign institutions now offer green-labelled credit for assets that meet EU taxonomy thresholds, widening liquidity pools. Public capital, forecast to rise at a 6.22% CAGR, underpins transport nodes, science parks, and post-quake rebuilding.

The budgeted USD 20.86 billion disaster-resilience envelope is channelled through ministries via turnkey contracts that favour firms with proven seismic credentials. PPP concessions on tollways and airports continue to draw institutional investors, creating anchor infrastructure around which private mixed-use complexes cluster. Blended-finance structures lower the overall cost of capital, helping the Turkey commercial construction market balance commercial returns with socio-economic goals.

Geography Analysis

Istanbul’s pre-eminent 42.15% share reflects its role as Turkey’s commercial gateway and beneficiary of headline projects such as the USD 15 billion canal and the partially delivered Finance Center. These undertakings stimulate auxiliary builds—premium offices, luxury hotels, airport-integrated malls—cementing the metropolis as the prime node of the Turkey commercial construction market. Izmir, distinguished by undersea cable landing points and industrial free-zone status, records the fastest 6.9% CAGR, with data-centric facilities and trade-related warehouses mushrooming around Aliaga and Menemen.

Ankara commands steady demand rooted in its political prominence and improved rail connectivity; the passenger uplift from 15 million to 60 million journeys annually sparks retail concourses and hotel flags at transit stations. Thrace-side municipalities enjoy spill-overs from the Halkalı-Kapıkule high-speed corridor, where logistics parks spring up adjacent to new junctions. Enhanced bridge and tunnel networks—740 kilometers of tubes and 488 kilometers of spans added since 2003—shorten freight times, incenting developers to plant regional distribution depots.

Adoption of smart-city blueprints widens beyond the “big three,” as Bursa, Konya and Gaziantep roll out open-data platforms and district energy grids. Between 2025 and 2030, over one-quarter of new LEED applications emerge outside Istanbul, signaling a maturing environmental consciousness nationwide. Aggregated, these dynamics build a geographically diversified pipeline that anchors the Turkey commercial construction market’s long-run resilience.

Regulatory Landscape

Commercial construction in Turkey is shaped by centralized permitting and compliance under the Ministry of Environment, Urbanization and Climate Change, with Building Inspection Law No. 4708 requiring structured third-party controls. Contractor market access is determined through the Regulation on the Classification and Registration of Building Contractors, which links eligibility to economic, financial, and technical capacity, alongside mandatory national standards and technical requirements that become binding when adopted through ministry instruments.

Project planning and approvals also reflect environmental and cost-benchmark rules used across commercial builds. The Environmental Impact Assessment (EIA) Regulation, amended in March 2026 (Official Gazette No. 33187), updates administrative implementation methods for covered projects, which changes schedule risk and documentation requirements for larger developments. Separately, the 2026 Building Construction Unit Costs communique took effect from January 1, 2026 and provides the official unit-cost framework used in architectural and engineering service fee calculations, while Yüksek Fen Kurulu (YFK) technical specifications continue to be updated for key building systems and materials, including thermal insulation updates in late 2025.

Value Chain Analysis

Turkey’s commercial construction value chain is anchored by developers and EPC/GC contractors that secure land, financing, permitting, and pre-leases, before contracting architecture and engineering services and a broad subcontractor base for structural, MEP, façade, and fit-out scopes. Large domestic firms, including ENKA, Ronesans, Limak, and peers, often span multiple roles, from contracting and project management to selective development and concession participation, which concentrates control over timelines and procurement even as currency and interest-rate volatility tightens operating conditions.

Upstream inputs combine strong local supply in core materials with exposure to imported building systems, particularly HVAC, lifts, and specialized equipment. That mix creates cost and availability risk when FX moves sharply. Bottlenecks across the chain also include tight credit conditions, elevated labor costs amplified by specialized demand linked to post-earthquake work, and permitting complexity in major metros. On the demand and delivery side, public entities such as the General Directorate of State Hydraulic Works (DSI) remain important tendering counterparts for large programs, which can catalyze adjacent commercial buildouts. Private tenants in logistics and technology further push specification upgrades, including automation-ready warehouses, resilient power, and digital-ready buildings.

Competitive Landscape

The Turkey commercial construction market is moderately concentrated. Domestic champions such as ENKA İnşaat, Rönesans, and Limak continue to dominate headline contracts, yet partnerships with foreign majors like Salini Impregilo reveal a cooperative posture on technically demanding rail and tunnel works. ENKA’s 63.88% jump in 2024 sales and 123.79% operating-profit surge underscore the earnings capacity for firms that straddle domestic PPP concessions and export engineering services[3]Ministry of Trade, “Top Turkish Construction Services Exporters 2024,” ticaret.gov.tr.

Digital capabilities are differentiators: early adopters of BIM, drone surveying, and digital twins mark out cost and schedule advantages, especially under tight margin conditions created by currency swings. AI-enhanced design is nascent; however, pilot rollouts in hospital complexes show error-rate drops that appeal to public procurers. Sustainability credentials further stratify bidders, with LEED-experienced contractors commanding premiums in multinational tenancy deals.

Market entry barriers stem from seismic-code complexity and a still-opaque permitting maze, but capital requirements remain moderate compared with Western Europe. The combined top five hold roughly 45-50% of annual billings, indicating moderate concentration. Niche disruptors focused on green-retrofit services and smart building systems are expected to clip market share from traditional heavy civil players over the next cycle.

Turkey Commercial Construction Industry Leaders

ENKA İnsaat ve Sanayi A.S.

Rönesans Holding

Yapı Merkezi Holding

Limak Holding

GAP İnşaat

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Green and digital compliance is emerging as a commercial opportunity for contractors and developers that can deliver measurable performance and the documentation requirements used in public and institutional-financed projects. The 2026 Presidential Annual Program outlines a twin transformation agenda across industry and construction, explicitly referencing AI-enabled workflows, UAV-based site monitoring, 3D-printed structures, and lower-carbon materials such as carbon-neutral concrete. Alongside this, BIM adoption efforts are being advanced through government-led workshops and integration work under the Ministry of Environment, Urbanization and Climate Change, which supports demand for BIM-capable design, coordination, and construction management services.

Large transport and strategic facilities activity is also creating commercial construction whitespace around hubs, and supporting specialized building types such as maintenance, logistics, and resilient utilities. In February 2026, Turkey secured USD 6.75 billion in foreign financing for the 125-kilometer Northern Ring Railway Project (Gebze-Halkali). In January 2026, groundbreaking was reported for a 100 billion TL investment program across eight locations tied to Turkish Airlines and the Ministry of Transport, including a wide-body aircraft engine maintenance center at Istanbul Airport. On the renovation side, enforcement-driven seismic and energy upgrades represent a near-to-medium term pipeline, supported by ongoing public disaster-resilience funding already embedded in the market context and by owners pursuing combined retrofit scopes to qualify for green-labeled financing structures.

Recent Industry Developments

- July 2026: Limak Holding established a dedicated Real Estate Investment Department to centralize management of its property activities and to expand its commercial and mixed-use portfolio in Turkey and abroad. This organizational move signals a more structured investment approach that can accelerate project origination and execution across offices, retail-led mixed use, and income-producing assets.

- May 2026: ENKA announced that its 852 MW Kırklareli Natural Gas Combined Cycle Power Plant entered operation following successful acceptance tests completed on 26 March 2026. New large-scale generation capacity strengthens grid reliability for energy-intensive commercial facilities and supports developers targeting data centers, logistics parks, and other power-sensitive formats.

- June 2024: Salini Impregilo formed a joint venture with Kolin Insa̧at to secure a USD 552 million contract for a 153-kilometer section of the high-speed railway corridor linking Istanbul toward the Bulgarian border. The EU-financed, multi-year rail package expands construction activity along the route and supports spillover commercial development around stations and logistics nodes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of commercial building activity in Turkey, counted as spending on new builds and renovations for income generating or service focused facilities such as offices, retail, hospitality, and institutional buildings.

Scope exclusions: It does not count residential buildings, linear infrastructure (roads, rail, utilities), or purely industrial heavy projects that are not treated as commercial building work.

Segmentation Overview

- By Commercial Sector Type

- Office

- Retail

- Industrial and Logistics

- Others

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By City

- Istanbul

- Ankara

- Izmir

- Rest of Turkey

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the boundary of what counts as commercial construction in Turkey, and to anchor the model to visible demand and supply indicators. We mainly review public statistics and releases such as TURKSTAT construction output and permits, the Ministry of Treasury and Finance budget documents, the Central Bank of the Republic of Turkey macro series, and trade bodies and city level development agencies where available.

To keep the model grounded, we also track project and pipeline signals through items such as official tender portals, public procurement announcements, and municipal zoning and urban transformation updates, followed by company annual reports, investor presentations, and reputable business press. Where needed, paid database subscriptions are used only to organize company financials, run structured news screening, and check patents and public contract references tied to materials and construction methods. The desk sources named here are illustrative, and many other public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and short surveys help us validate what is actually being built, what is delayed, and how budgets are being repriced across major commercial categories. We speak with developers, general contractors, subcontractors, consultants, and materials distributors across Turkey so that the desk signals can be corrected for real execution timing, cost escalation, and renovation intensity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 29% | |

| Smaller Players: 19% | Managers: 59% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where construction output, permits, and pipeline signals are reconstructed into a Turkey commercial spending pool, and then filtered into commercial building types based on observed project mix. Once that pool is formed, we corroborate totals with selective bottom-up checks, such as sampled project values by category, channel checks on typical cost per square meter, and sanity tests using contractor revenue exposure to commercial work.

Several practical inputs shape the sizing each year, including building permit trends for non-residential stock, office and retail development intensity in large cities, hotel and institutional project starts, renovation share driven by urban transformation and seismic resilience work, and materials and labor cost movements that shift nominal project value. Because the market is reported in USD, we treat exchange-rate timing carefully by aligning conversion windows with the spending period, and then checking if the implied USD value matches what local stakeholders see in contracts.

For forecasting, scenario analysis is used because commercial construction in Turkey can swing with financing conditions and policy triggers. The scenarios are anchored to consensus views from primary respondents on project starts, repricing behavior, and delay risk, and then moderated using macro indicators such as interest rates, inflation, and public budget direction.

Data Validation & Update Cycle

Validation is done through multiple cross-checks so that one noisy data series does not drive the final number. We compare the modeled totals against independent signals like non-residential permits, construction cost indexes, large project announcements, and the year-to-year change implied by contractor and developer commentary, and then anomalies are reviewed before sign-off.

If a large variance is seen by category or city, analysts re-check assumptions, revisit currency conversion timing, and re-contact a small set of respondents to confirm what changed on the ground. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the most current view available.

Mordor Intelligence's Turkey Commercial Construction Market Size Measured Against Other Published Estimates

Published market sizes for Turkey commercial construction can differ even when the topic label looks the same, because the counted spend can shift with scope choices, currency conversion timing, and how price escalation is applied to multi-year projects. Differences also show up when one estimate leans on announced pipeline values, while another relies more on executed spending.

The biggest gap drivers in this market are usually whether renovation and retrofit work is fully counted, how Istanbul versus the rest of Turkey is weighted in the project mix, and how USD values are converted during high volatility periods. A refresh-led model that re-checks FX windows and updates cost per square meter assumptions (instead of carrying older price curves forward) tends to reduce overstatement during sudden repricing, and that refresh discipline is the reason the 2025 USD total on this page differs from some other figures, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 30.18 B (2025) | |

| Industry Association A | USD 34.60 B (2025) | Often uses announced project pipeline and tender values as a proxy for annual spend, which can overcount projects that slip, get resized, or get re-tendered in a volatile pricing year. |

| Global Consultancy B | USD 27.40 B (2025) | May apply conservative USD conversion and slower cost escalation, and sometimes excludes a wider share of renovation and retrofit work that is active in commercial stock upgrades. |

Overall, the spread is mainly explained by what gets treated as executed spend versus pipeline value, plus how USD timing and repricing are handled. By tying the number to observable permits, project progress checks, and updated unit-cost logic, our estimate stays traceable to clear drivers that can be rechecked each refresh cycle.

Key Questions Answered in the Report

What is the current size of the Turkey commercial construction market?

The market was valued at USD 31.85 billion in 2026 and is projected to climb to USD 41.67 billion by 2031.

Which segment leads the Turkey commercial construction market?

Retail construction held the largest 37.25% share in 2025, though industrial & logistics is the fastest-growing at a 6.73% CAGR.

How will seismic regulations affect future construction costs?

Mandatory compliance with the Turkish Building Seismic Code 2018 raises upfront costs but lowers long-term risk, with a national retrofit budget estimated at USD 500 billion over 20 years.

Why is Izmir considered a high-growth city for commercial projects?

Strategic investments such as the Vodafone-DAMAC data center and superior cable connectivity are propelling Izmir to a market-leading 6.9% CAGR through 2031.

How significant is public funding in the Turkey commercial construction market?

Although private capital supplied 65.55% of 2025 investment, public expenditure is set to increase at 6.22% CAGR, driven largely by disaster-resilience and transport megaprojects.

What role do green-building policies play in shaping new developments?

Turkey’s impending Green Taxonomy and rising LEED adoption incentivize developers to integrate energy-efficient materials and renewable systems, enhancing asset value and financing options.

Page last updated on: