Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

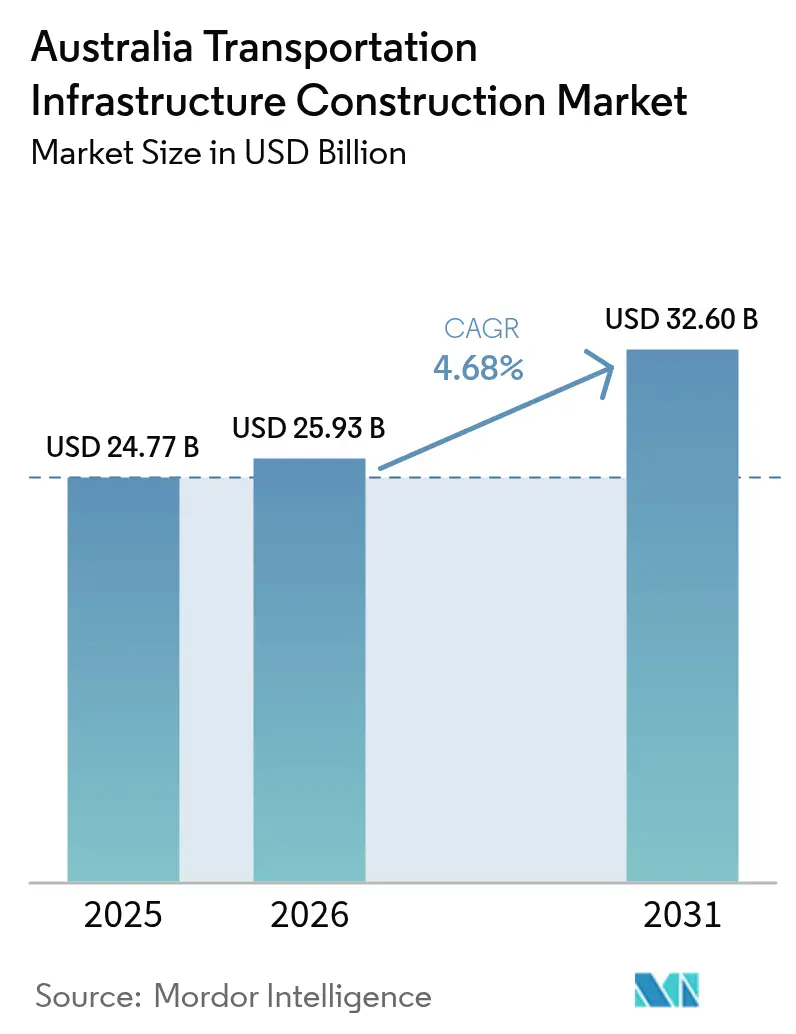

| Base Year Market Size (2025) | USD 24.77 Billion |

| Market Size (2026) | USD 25.93 Billion |

| Market Size (2031) | USD 32.6 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

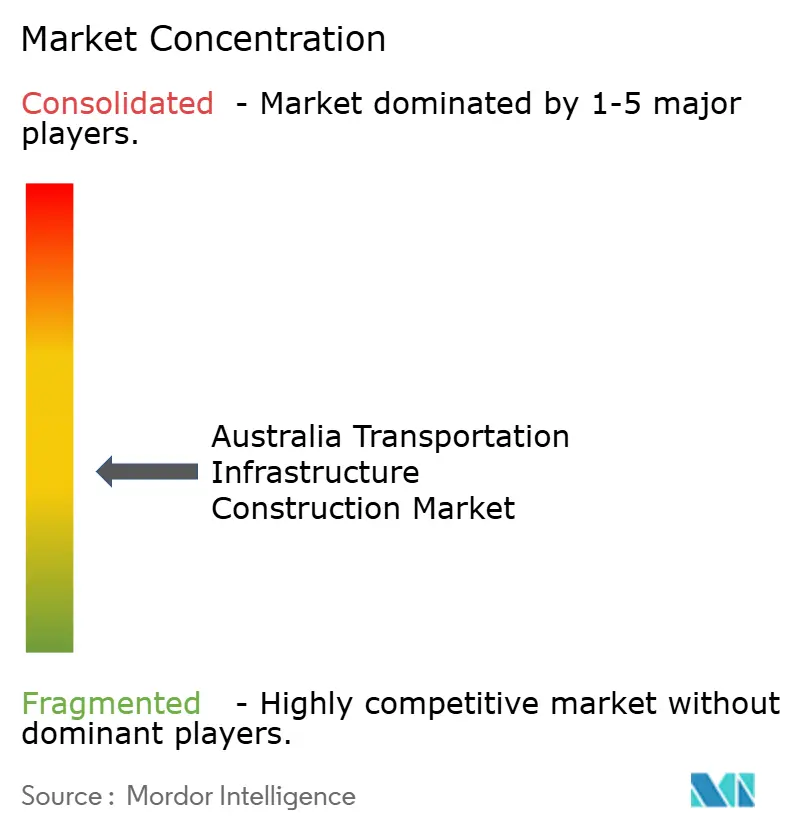

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

The Australia Transportation Infrastructure Construction Market size in 2026 is estimated at USD 25.93 billion, growing from 2025 value of USD 24.77 billion with 2031 projections showing USD 32.6 billion, growing at 4.68% CAGR over 2026-2031.

Government budget certainty, intermodal freight integration, decarbonization imperatives, and defense-driven northern upgrades collectively underpin this steady expansion.[1]Australian Government, "Infrastructure Investment Program 2025-26," Department of Infrastructure, Transport, Regional Development, Communications and the Arts, infrastructure.gov.au Rail electrification programs, higher-capacity port interfaces, and the adoption of digital twins continue to attract capital, even as labor shortages push wage agreements to record levels. Private investors accelerate their participation through sophisticated public-private partnership structures that mitigate construction risk while expanding long-term yield opportunities. At the same time, megaproject cost management and insurance premiums for climate-exposed assets remain material constraints, prompting stronger governance frameworks and expanded contingency allowances across new and renovation projects.

Key Report Takeaways

- By type, roadways led with 51.05% revenue share in 2025; railways are projected to expand at a 5.43% CAGR through 2031.

- By construction type, new construction held a 64.12% share in 2025, while renovation is advancing at a 5.18% CAGR to 2031.

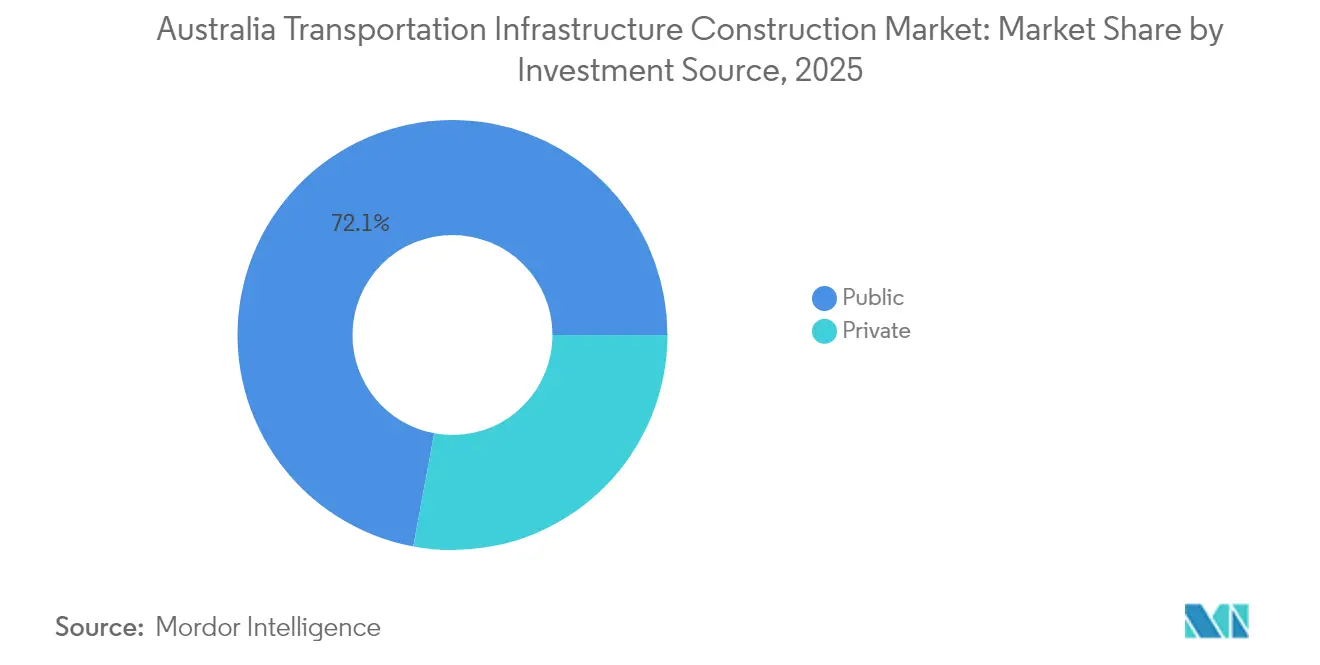

- By investment source, public funding accounted for 72.08% of the Australian transportation infrastructure construction market share in 2025, whereas private investment is predicted to expand at a 5.78% CAGR through 2031.

- By geography, New South Wales led with 29.45% revenue share in 2025; Queensland is forecast to grow at a 5.94% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Federal & State Budget Allocations | +1.2% | National, with a concentration in NSW and Queensland | Medium term (2-4 years) |

| Fast-tracking of Inland Rail and Western Sydney projects | +0.8% | NSW, Queensland, Victoria corridors | Long term (≥ 4 years) |

| Surge in inter-modal freight demand | +0.6% | National freight corridors, port connectivity zones | Medium term (2-4 years) |

| Decarbonisation mandates driving rail electrification | +0.5% | Urban centers and interstate corridors | Long term (≥ 4 years) |

| Digital twins & BIM mandates improving cost certainty | +0.4% | Major metropolitan projects, government contracts | Medium term (2-4 years) |

| Defence-led northern road upgrades (DAR Initiative) | +0.3% | Northern Territory, Far North Queensland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Federal & State Budget Allocations Drive Infrastructure Pipeline Acceleration

Federal and state allocations of USD 17.1 billion for road and rail in the 2025-26 cycle anchor a USD 120 billion rolling pipeline that shifts spending toward proactive capacity creation[2]Infrastructure Australia, “Market Capacity Report 2024,” Infrastructure Australia, infrastructureaustralia.gov.au. Western Australia’s METRONET uses a USD 6 billion four-year commitment to synchronize rail, road, and station precinct upgrades. Queensland’s Transport and Roads Investment Program applies a similar whole-of-network philosophy, coordinating federal Infrastructure Investment Program funds with state delivery mechanisms. Tier-1 contractors’ share of awarded work rose to 59% in 2025 as governments bundled large, complex packages that favor companies capable of digital design integration and full-life asset management.

Fast-tracking of Inland Rail and Western Sydney Projects Creates Integrated Transport Corridors

The Inland Rail’s 1,700-kilometer freight spine and the Sydney Metro Western Sydney Airport line exemplify corridor-level planning that merges rail, road, and airport interfaces. Inland Rail seeks to shift significant freight from truck to rail and cut transit times under 24 hours while supporting decarbonization goals. The Western Sydney program layers a USD 5.25 billion rail package with USD 2.3 billion in complementary road works to serve a future 2 million-resident catchment. Early delivery of Perth’s Forrestfield-Airport Link demonstrates the economic multiplier effect of such integrated models.

Surge in Inter-modal Freight Demand Reshapes Infrastructure Investment Priorities

Domestic freight volumes are projected to rise 26% from 2020 to 2050, with road freight up 77% and rail freight up 5.7%, compelling investment in integrated terminals and port linkages. The Moorebank Logistics Park and the Port of Brisbane’s USD 3.5 billion channel upgrade highlight how combined rail-road-port interfaces reduce landside congestion and boost freight efficiency. Cruise-enabled wharf enhancements such as Brisbane’s Luggage Point terminal reinforce the trend toward multi-use port precincts.

Decarbonization Mandates Accelerate Rail Electrification and Clean Transport Infrastructure

Transport contributes 21% of national greenhouse emissions; a net-zero target for 2050 positions electrified rail, EV charging corridors, and hydrogen distribution assets as construction priorities[3]Department of Climate Change, Energy, the Environment and Water, “Rewiring the Nation Program Overview,” DCCEEW, dcceew.gov.au. Aurizon’s USD 50 million Future Fleet Fund supports battery and hydrogen locomotive pilots. The Rewiring the Nation program allocates USD 20 billion for transmission lines vital to rail electrification and EV charger rollout, though community opposition to new corridors presents schedule risk.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortage & wage inflation | -1.1% | National, acute in NSW and Victoria | Short term (≤ 2 years) |

| Cost blow-outs in megaproject tunnelling | -0.7% | Major metropolitan areas with tunnelling projects | Medium term (2-4 years) |

| Community opposition to green-field corridor acquisition | -0.4% | Rural and peri-urban areas, transmission corridors | Medium term (2-4 years) |

| Rising insurance premiums for climate-exposed assets | -0.3% | Northern Australia, coastal infrastructure zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Shortage and Wage Inflation Constrain Project Delivery Capacity

Infrastructure build-out needs an extra 90,000 workers, yet construction trades face an aging workforce, limited migration inflows, and competing demand from the housing sector[4]Department of Employment and Workplace Relations, “National Skills Priority List 2025,” DEWR, dewr.gov.au. Three-year union agreements in NSW lift wages 26%, pushing base compensation for level-three trades to USD 237,000, while Queensland’s comparable deal raises hourly carpenter rates above AUD 65 by 2027. Government apprenticeship incentives and industry-linked training programs aim to address pipeline gaps but will support medium-term rather than immediate labor supply.

Cost Blow-outs in Megaproject Tunneling Threaten Investment Returns and Future Funding

Projects over USD 1 billion have averaged 30% overruns since 2001, adding USD 34 billion to taxpayer exposure. Sydney Metro’s City and Southwest line jumped from USD 11.5 billion to over USD 20 billion due to ground conditions and safety upgrades, while Metro West shows a similar escalation. Inland Rail costs followed a comparable trajectory from USD 4.4 billion to USD 31.4 billion, underscoring the need for stronger demand forecasting and stage-gated approvals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Railways Acceleration Challenges Roadways Dominance

Roadways generated more than half of 2025 revenue, yet railways display the strongest growth pulse at 5.43% CAGR. The Inland Rail program alone underpins a transition toward modal balance by targeting a doubling of Melbourne-Brisbane rail freight by 2050. Western Sydney Airport’s airfield and apron packages elevate requirements for high-capacity access roads and metro spurs, while port and inland waterway investment concentrates on deeper channels and quay upgrades to handle larger vessels. Digital design techniques and predictive maintenance embed cost control, positioning rail and port assets for sustained share gains within the Australian transportation infrastructure construction market.

The Australian transportation infrastructure construction market size for railways is projected to expand faster than roadways, thanks to emissions targets, integrated freight corridors, and a national rail manufacturing plan that raises local content thresholds. By contrast, the Australian transportation infrastructure construction industry’s roadway segment pursues asset safety and resilience upgrades rather than pure capacity expansion. Ports and inland waterways secure a niche by modernizing cruise and container infrastructure, and the airways segment sees steady spending tied to Western Sydney International Airport’s phased roll-out and parallel runway rehabilitation programs at major east-coast gateways.

By Construction Type: Renovation Gains Momentum Despite New Construction Leadership

New construction captured a 64.12% share in 2025 as governments favored headline projects such as Inland Rail and Sydney Metro over incremental upgrades. Renovation, however, posts a 5.18% CAGR through 2031 as asset managers prioritize safety barriers, flood resilience, and digital condition monitoring to stretch lifecycle performance. The Bruce Highway safety series exemplifies this shift, channeling USD 7.2 billion into lane widening, bridge strengthening, and intelligent transport systems.

Within the Australian transportation infrastructure construction market, renovation spending also escalates due to climate resilience requirements and the rise of performance-based maintenance contracts that bundle renewal works with operation. New construction remains essential for emerging growth corridors in Queensland and northern Australia, yet faces tighter cost scrutiny. The Australian transportation infrastructure construction market size for renovation assets thus narrows the gap with greenfield spending over the forecast horizon.

By Investment Source: Private Sector Momentum Challenges Public Dominance

Public entities contributed 72.08% of the 2025 value as the federal Infrastructure Investment Program and state budgets continued to dominate. Nevertheless, private capital accelerates at a 5.78% CAGR driven by pension funds and global builders pursuing inflation-linked returns. The Melbourne Metro Tunnel, North East Link, and Western Ridge Crusher illustrate a robust appetite for availability-based or demand-risk concession models that allocate geotechnical and interface risk between parties.

Hybrid funding models nurture depth in the Australian transportation infrastructure construction market by leveraging private delivery expertise while maintaining public policy oversight. The Australian transportation infrastructure construction market share of PPP transactions widens as governments cap direct balance-sheet exposure. Risk-sharing provisions around cost escalation and carbon abatement become standard clauses, enabling timelier financial close and construction mobilization despite persistent macro-volatility.

Geography Analysis

New South Wales holds 29.45% of the 2025 value thanks to the USD 63 billion Sydney Metro portfolio, port rail shuttles, and Western Sydney International Airport precinct alignment. Integrated planning between Transport for NSW and federal agencies streamlines approvals, yet cumulative cost overruns temper future funding flexibility. The state also trialed digital twins at Gadigal Station to improve asset commissioning and maintenance.

Queensland records the highest growth path at 5.94% CAGR through 2031, spurred by Bruce Highway upgrades, Olympic corridor preparations, and the Logan-Gold Coast Faster Rail program. The state deploys freight-oriented upgrades to boost supply-chain efficiency while investing in climate-resilient roads across cyclone-prone northern zones. Port of Brisbane’s channel deepening and rail-road interface packages further secure trade competitiveness.

Victoria focuses on metropolitan de-bottlenecking via the USD 15.8 billion North East Link and Suburban Rail Loop early works, while Western Australia emphasizes resource-sector connectivity under METRONET and the Pilbara haulage initiative. Northern Territory exploits defense investment through DAR corridors, and Tasmania leverages the Marinus underwater interconnector to support renewable export ambitions. Collectively, these projects embed regional specialization and underpin the Australian transportation infrastructure construction market’s diversified growth profile.

Competitive Landscape

The market remains moderately fragmented, scoring 6 on a 10-point concentration scale, as the top five players command roughly 60% of aggregate value. Tier-1 contractors such as CPB Contractors, John Holland, and Lendlease Engineering consolidate shares by integrating design, delivery, and operations capabilities that satisfy government preferences for single-interface contracting. Webuild’s acquisition of Clough introduces additional tunneling and hydro expertise, aligning with sustainable mobility mandates.

Specialist firms excel in marine works, rail systems, and high-voltage transmission, enabling joint ventures that blend complementary scope and risk profiles. Digital twin technology and BIM proficiency become pivotal selection criteria, rewarding bidders able to deliver transparent cost forecasting and construction sequencing. Workforce development partnerships with vocational institutes mitigate labor shortfalls, while modular construction and automated tunneling machines help offset wage inflation.

Elevation of climate resilience and emissions reduction in tender assessments encourages contractors to retrofit equipment fleets with low-emission plant and to pilot hydrogen or renewable-diesel powered machinery. Insurance carriers’ tighter underwriting for flood and fire exposure heightens emphasis on adaptive design, opening advisory opportunities for engineering consultancies embedded within consortia. Overall, executives adopt balanced portfolios spanning high-profile megaprojects and smaller renovation frameworks to de-risk backlog volatility within the Australian transportation infrastructure construction market.

Australia Transportation Infrastructure Construction Industry Leaders

-

CPB Contractors

-

Lendlease

-

Hutchinson Builders

-

John Holland

-

Fulton Hogan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: CIMIC Group companies opened the city section of Sydney Metro, delivering 21 stations on an automated service with four-minute peak headways and engaging more than 1,000 local suppliers.

- August 2025: Marinus Link Stage 1 reached Final Investment Decision, unlocking cross-state renewable trading and forecast USD 1 billion in avoided carbon costs.

- June 2025: Webuild completed the purchase of Clough, adding over AUD 6 billion in Australian infrastructure backlog focused on rail and hydropower.

- May 2025: CIMIC’s Sedgman and CPB Contractors secured a USD 757 million contract for BHP’s Western Ridge Crusher, integrating a 30 Mtpa crusher and 12-kilometer conveyor in the Pilbara.

Australia Transportation Infrastructure Construction Market Report Scope

The transportation infrastructure construction market includes construction activities for transportation facilities of road, rail, air, and sea ports, which involves reforming existing constructions, building new infrastructures, and extending or demolishing projects.

A complete assessment of the Australian Transportation Infrastructure Construction Market includes an assessment of the economy market overview, market size estimation for key segments, and emerging trends in the market segments in the report. The report sheds light on the market trends like growth factors, restraints, and opportunities in this sector. The competitive landscape of the Australian Transportation Infrastructure Construction Market is depicted through the profiles of active, vital players. The report also covers the impact of COVID-19 on the market and future projections.

Australia's transportation infrastructure construction market is segmented by type (roadways, railways, waterways, and airlines).

The report offers market size and forecasts for the Australian transportation infrastructure construction industry in terms of value (USD) for all the above segments.

By Type

| Roadways |

| Railways |

| Airways |

| Ports and Inland Waterways |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By Geography

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| Rest Of Australia |

| By Type | Roadways |

| Railways | |

| Airways | |

| Ports and Inland Waterways | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By Geography | New South Wales |

| Victoria | |

| Queensland | |

| Western Australia | |

| Rest Of Australia |

Key Questions Answered in the Report

How large will the Australian transportation infrastructure construction market be by 2031?

The market is forecast to reach USD 32.6 billion by 2031, expanding at a 4.68% CAGR from 2026.

Which state is growing fastest in transport infrastructure construction?

Queensland records the highest forecast CAGR of 5.94% through 2031, driven by Bruce Highway upgrades and Olympic preparations.

What is the main challenge facing project delivery over the next two years?

Acute skilled-labor shortages combined with wage inflation reduce delivery capacity, subtracting an estimated 1.1% from forecast CAGR.

How are digital twins influencing project outcomes?

Government BIM mandates and digital twin pilots on metro and highway projects improve cost certainty and commissioning speed, positioning early adopters for competitive advantage.

Page last updated on: