Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

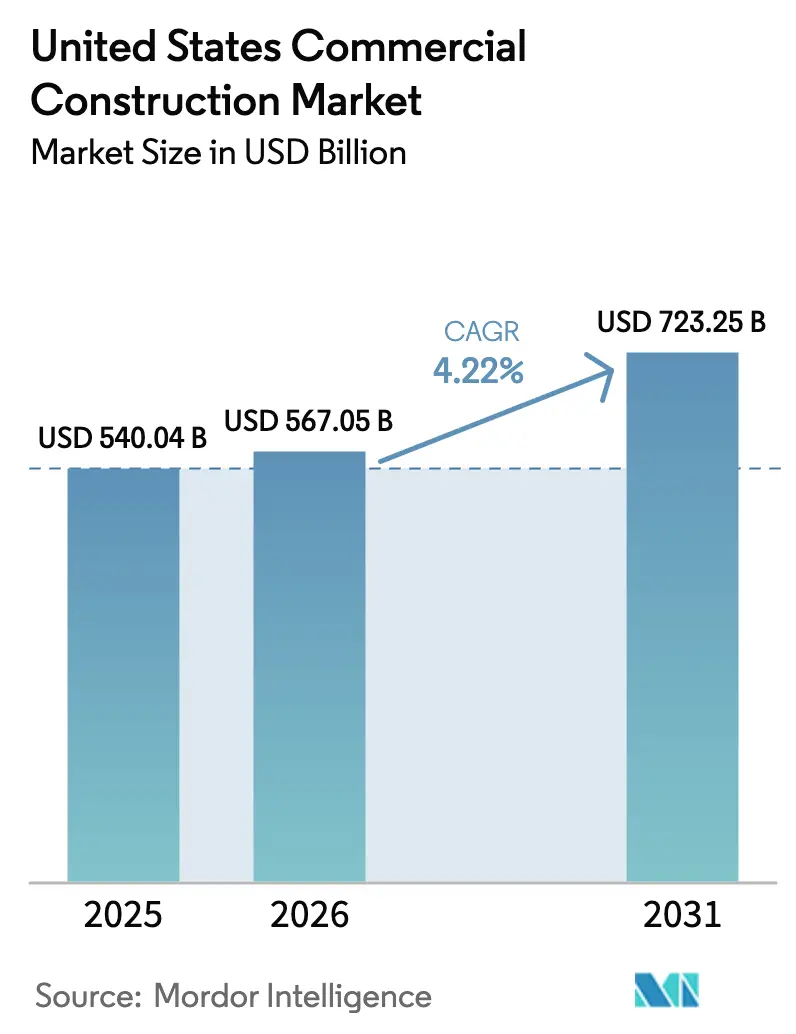

| Base Year Market Size (2025) | USD 540.04 Billion |

| Market Size (2026) | USD 567.05 Billion |

| Market Size (2031) | USD 723.25 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

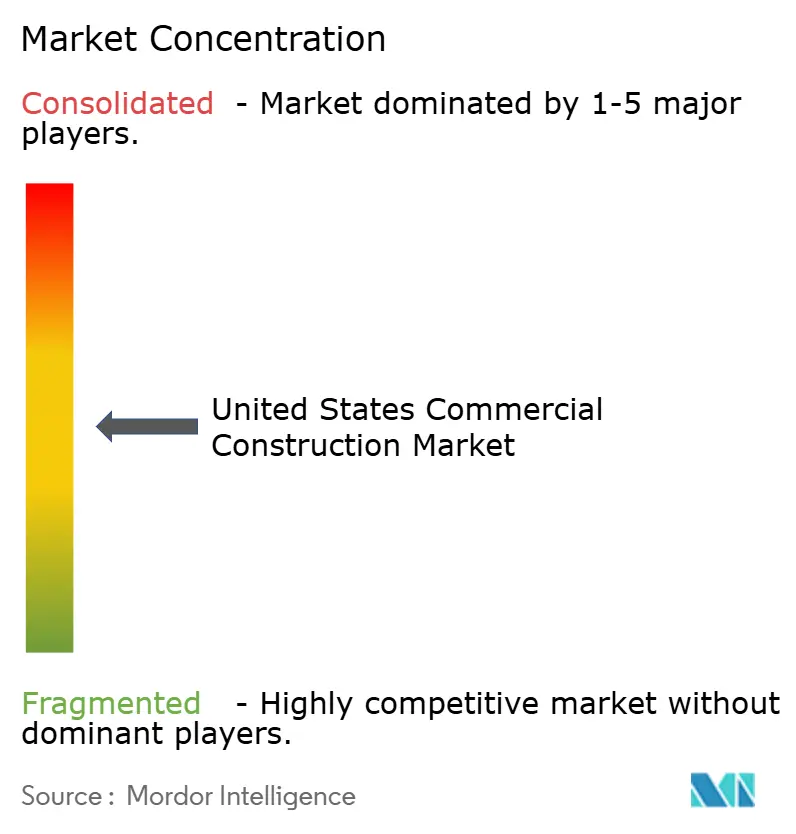

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Commercial Construction Market Analysis by Mordor Intelligence

The United States commercial construction market size is estimated at USD 567.05 billion in 2026 and is projected to reach USD 723.25 billion by 2031 at a CAGR of 4.22% during the forecast period (2026-2031). Growth is supported by a mix of e-commerce warehouse expansion, hybrid workplace retrofits, accelerated data center buildouts for artificial intelligence compute, and federal infrastructure programs that catalyze transit-oriented commercial nodes. Competitive execution is shaped by labor scarcity and input inflation as wages and certain materials rose in 2025, a backdrop that favors contractors with early-purchase agreements, integrated MEP capabilities, and diversified geographic exposure. Project feasibility is also sensitive to financing conditions as lenders maintain tighter debt service coverage requirements, while policy-led sustainability standards push design teams toward LEED v5 and low-embodied-carbon specifications that are now common in public bids. The US commercial construction market is therefore balancing demand-side momentum with execution risks that require disciplined preconstruction, supply-chain hedging, and workforce strategies to protect margins and schedules.[1]https://www.agc.org/

Key Report Takeaways

- By commercial sector type, office construction led with a 35.1% share in 2025, while industrial and logistics are the fastest-growing at a 5.44% CAGR through 2031.

- By construction type, new construction accounted for 68.1% share of the US commercial construction market size in 2025, and renovation is projected to expand at a 5.20% CAGR during 2026-2031.

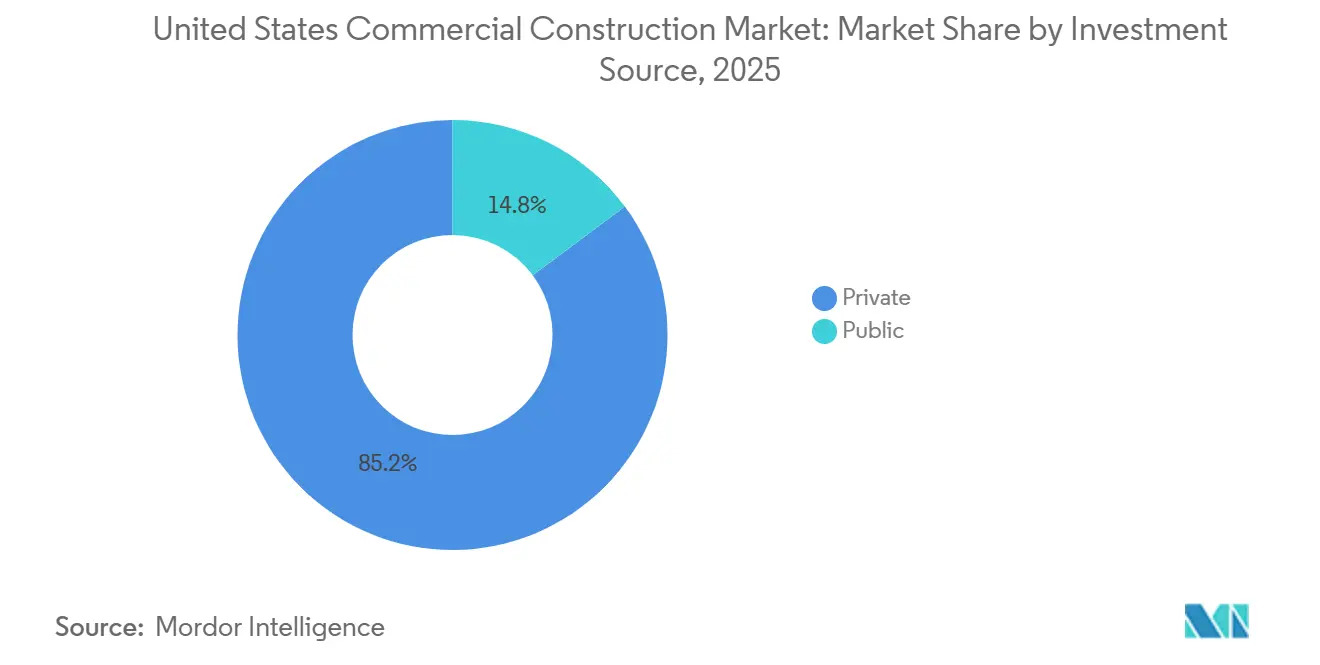

- By investment source, private spending held 85.2% in 2025, and public funding is set to grow at a 5.60% CAGR, aided by IIJA commitments.

- By states, Texas led with 17.0% in 2025, while Florida is forecast to post the fastest growth at a 5.45% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Commercial Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data center growth accelerating with new AI, cloud, and edge computing infrastructure. | +1.3% | National core markets (Northern Virginia, Texas, California, Illinois), expanding to the Midwest and Southeast | Long term (≥ 4 years) |

| E-commerce expansion fueling build-outs of warehouses, distribution centers, and fulfillment hubs. | +0.9% | National, with the strongest growth in Texas, California, Florida, Midwest logistics corridors | Medium term (2-4 years) |

| Public investment in transit and civic facilities sparking construction in infrastructure-adjacent zones. | +0.8% | National, with the highest concentration in states receiving IIJA funding (California, New York, Texas, Illinois) | Long term (≥ 4 years) |

| Office retrofit and redevelopment rising as employers seek more modern, hybrid-ready workplaces. | +0.7% | National, concentrated in major metros (New York, San Francisco, Chicago, Los Angeles) | Short term (≤ 2 years) |

| Hospitality and mixed-use projects are recovering, driven by strong travel and retail demand. | +0.6% | Florida, Nevada, Texas, major urban markets, and resort destinations nationwide | Medium term (2-4 years) |

| Green-building and ESG focus driving new commercial developments toward certified designs. | +0.5% | National, regulatory pressure strongest in California, New York, Washington; voluntary adoption accelerating nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Expansion Fuels Warehouse and Fulfillment Construction

E-commerce continues to steer location and product mix decisions as large retailers expand logistics footprints and push for speed-to-customer gains that require high-throughput facilities in core corridors. Amazon signed 31 million square feet of new leases in 2024, announced a USD 15 billion logistics expansion, adding nearly 80 facilities, and is positioned to capture around 25% of new industrial leasing in 2026. The U.S. delivered 146.6 million square feet of industrial space by mid-2025, with 341.8 million square feet under construction, while vacancy rose to 7.1% and signaled that supply was catching up to demand in select markets. Reshoring and nearshoring patterns amplify demand as 69% of U.S.-serving supply chains are projected to be Americas-based by 2026, up from 59%, supported by stronger U.S.-Mexico trade flows since 2018 and an upswing in nearshoring investment during early 2025. Within cold-chain logistics, online grocery is set to reach USD 100 billion in 2025, yet the nation’s 220 million square feet of refrigerated space trails demand by 75-100 million square feet, a gap that is prompting large-scale investments like New Cold’s USD 300 million expansion in Lebanon, Indiana. This divergence between standard warehouses and temperature-controlled facilities is sustaining rent premiums for specialized assets and rewarding developers with vertical integration or in-house MEP capabilities that manage complexity and cost.[2]https://www.commercialcafe.com/blog/us-industrial-2025-midyear-report

Hybrid Workplace Pressures Drive Office Retrofit and Adaptive Reuse

Corporate occupiers are channeling capital into quality over quantity to support hybrid models, wellness, and energy performance in their workspaces. Only 14% of the global workforce prefers a traditional corporate office, while 60% of organizations plan to increase spending on design, fit-out, and refurbishment, a shift that favors adaptive reuse and targeted upgrades. Retrofit pathways can cost 30-50% less than ground-up builds and speed occupancy, illustrated by JPMorgan’s 270 Park Avenue, a 2.5 million square foot all-electric skyscraper delivered in October 2025 that demonstrates high-performance design at scale. Conversion economics are strengthening as Gensler estimates around 34% of US office buildings can be repurposed to residential use at 30-40% below new-build costs, with Historic Tax Credits mobilizing billions in private capital for older downtown assets. Even as the national office vacancy rate reached 18.6% in late 2025, LEED-certified Class A properties command rent premiums that reinforce the business case for high-performance retrofits and high-quality tenant improvements. These dynamics keep retrofit pipelines active and position adaptive reuse as a resilient lever in the US commercial construction market through the forecast window.[3]https://www.gensler.com/research-insight/gensler-research-institute/global-workplace-survey

Data Center Construction Accelerates Amid AI and Cloud Compute Demand

AI, cloud, and edge workloads are reshaping location, design, and grid interface requirements for mission-critical projects. U.S. data center capacity is projected to grow roughly 10% annually through 2030 to reach the mid-30 gigawatt range, and nationwide electricity consumption attributed to data centers could rise from around 4% in 2025 to 7.5% by decade end. Mega-campuses are multiplying, including a USD 15 billion program for Vantage in Wisconsin and a USD 4 billion Microsoft project in Mount Pleasant, while sector construction spending is projected to peak at USD 89 billion in 2026, up sharply from 2022. Power delivery is the bottleneck as ERCOT expects double-digit demand growth in Texas by 2026, grid operators expand 345-kilovolt and 765-kilovolt corridors, and the Department of Energy advances plans to add or upgrade 100,000 miles of transmission this decade. Execution risk is most evident in utility interconnections and permitting, where 12-24 month timelines are common and local entitlements can add months to preconstruction before notice to proceed, especially for projects that require additional on-site power or storage. These projects remain a central growth engine for the US commercial construction market as developers adjust capital stacks to reflect longer lead times for power and procure switchgear, transformers, and cooling systems earlier in the schedule.

Public Infrastructure Investment Sparks Transit-Adjacent Commercial Growth

The Infrastructure Investment and Jobs Act provides USD 1.2 trillion over five years, which includes USD 550 billion in new federal spending as states move projects through procurement and contracting cycles. By late 2025, the Department of Transportation reported USD 411.5 billion in announced grants and USD 343.3 billion obligated with USD 189.1 billion outlaid, a cadence that signals an acceleration phase in 2026. Highway programs are driving more than 70,000 new federal-aid commitments and pushed contract awards up 36% in 2023 versus 2021, while the General Services Administration allocates USD 3.4 billion to modernize Land Ports of Entry that support cross-border commerce. Transit-adjacent commercial is clustering around catalysts like New York’s SPARC Kips Bay and Willets Point, which leverage public dollars to draw private investment for mixed-use hubs with proximity to rail and subway links. State-level momentum includes a USD 39.92 billion TxDOT budget for fiscal 2026-2027 that underpins backlogs and aligns with a broader decade-long transportation program that sustains contractor activity across Texas. ESG policy is also shaping specifications as California’s climate disclosure mandates take effect in 2026, reinforcing decarbonization and resilience requirements in municipal procurement.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages and wage pressure slowing project delivery and increasing costs. | -0.7% | National, most acute in Sunbelt states (Texas, Florida, Arizona) with rapid population growth | Short term (≤ 2 years) |

| Tight lending conditions and rising interest rates hindering financing of speculative projects. | -0.6% | National, most pronounced in high-vacancy office markets (San Francisco, Chicago, New York) | Medium term (2-4 years) |

| High material and freight inflation compressing margins and delaying budgets. | -0.5% | National, with regional cost variations (New York, San Francisco most expensive; coastal cities face freight premiums) | Medium term (2-4 years) |

| Permitting delays and zoning restrictions prolonging pre-construction phases. | -0.3% | Most severe in California, New York, Illinois; sporadic delays in fast-growing Sunbelt metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages and Wage Pressure Slowing Project Delivery and Increasing Costs

Meeting 2026 demand requires recruiting 499,000 new workers after a shortfall year where most firms reported difficulty filling craft roles and an aging workforce pointed to higher retirements through the decade. Employers report the tightest gaps in specialized trades and estimating, which creates scheduling bottlenecks and increases reliance on overtime, incentives, and per diem policies that push project labor costs higher. Average hourly earnings in construction reached USD 38.76 by March 2025 and were up 4.5% year over year, while the sector paid more than manufacturing and transportation to compete for talent and retain crews on critical paths. Mission-critical work, such as data centers, pays premium rates that can pull electricians and HVAC technicians off other commercial sites and exacerbate staffing challenges for hospitals, schools, and civic projects. These pressures are broad-based, and they have led to measurable delays and potential output losses that reinforce the case for prefabrication, improved field productivity tools, and targeted training pipelines.

Financing Constraints and Loan Maturities Slow Speculative Development

Interest rates remained elevated through 2025 as the Federal funds rate held in the 4.25-4.50% range, and lenders tightened underwriting by asking for higher equity and debt service coverage above 1.25. Under these terms, a USD 100 million project financed over 10 years can add more than USD 15 million in interest expense compared to the low-rate era, which reduces feasibility for speculative starts in office and select retail formats. A loan maturity wall of USD 600 billion in 2024 and USD 500 billion in 2025 forced many owners to refinance at higher rates, and some downtown projects struggled to pencil, prompting ownership transitions on weaker assets. Hospitality financing conditions improved marginally as rate expectations eased, which supported selective new construction and acquisition pipelines in late 2025 and early 2026. Capital costs remain a key swing factor for the US commercial construction market in 2026 as developers weigh interest rate paths, absorption risks, and tighter loan structures against favorable long-term demand in data centers, logistics, and public works.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commercial Sector Type: Industrial & Logistics Claims Fastest Expansion

Office construction held 35.1% of the US commercial construction market share in 2025, supported by hybrid workplace upgrades and adaptive reuse strategies that often deliver occupancy sooner and at lower cost than new towers. Growth is uneven across office segments as companies prioritize high-performance buildings with modern systems and certifications that align with tenant expectations and ESG commitments. Within the US commercial construction industry, the industrial and logistics segment is the fastest-growing, with a 5.44% CAGR through 2031 as fulfillment needs, reshoring momentum, and cold-chain expansion continue to absorb new space and sustain build-to-suit activity. Developers are tracking the split between commodity warehouses and specialized facilities such as temperature-controlled storage and high-power data centers that command premium rents but require early procurement and more complex MEP coordination. This segmentation is converging near rail, highway, and power infrastructure, further tightening site selection filters in core markets.

The demand profile is reinforced by Amazon’s multi-year expansion and broader leasing momentum among third-party logistics, which shape land prices, entitlement timelines, and construction schedules in high-growth corridors. Industrial deliveries and the pipeline reported by mid-2025 were high by historical standards, while vacancy increases indicated a healthier balance in certain submarkets that may moderate rent growth but still favor well-located assets. Data center spending is projected to peak at USD 89 billion in 2026 and has become a core driver of mission-critical work that shapes contractor backlogs and subtrade availability. These conditions keep industrial and logistics at the center of the US commercial construction market, with risk management focused on grid access, long-lead equipment, and entitlements for large-format projects.

By Construction Type: Renovation Gains Momentum Over New Builds

New construction accounted for 68.1% share of the US commercial construction market size in 2025, supported by data centers, industrial facilities, and select hospitality and mixed-use towers across high-demand metros. Renovation is growing faster at a 5.20% CAGR during 2026-2031 as owners seize the cost and time advantages of repurposing existing assets, often with support from Historic Tax Credits that have catalyzed significant private investment over time. Within the US commercial construction industry, retrofit programs are expanding in office, hospitality, and education as corporate and public owners target lower embodied carbon, improved energy performance, and healthier interiors aligned with LEED v5. Brand-mandated hotel property improvement plans and office fit-outs with flexible floor plates are further lifting renovation pipelines and contracting opportunities for interior specialists. Contractors are planning for abatement and structural upgrades common in older buildings, which require disciplined preconstruction to de-risk budgets and timelines.

City-led conversions and incentive programs in New York and Chicago underscore how municipal policy can unlock downtown reuse at scale by combining zoning with tax-increment financing and targeted grants. Large owners also demonstrate the viability of high-performance retrofits, exemplified by marquee projects that align with electrification and carbon goals now common in institutional portfolios. As procurement moves toward whole-building life-cycle assessments, renovation programs that preserve structure and reduce embodied carbon gain an edge in public bids and corporate governance reviews. The US commercial construction market is therefore set to see renovation capture a larger share of pipeline dollars through 2031, with supply chains adapting to the material and system profiles common in deep retrofits.

By Investment Source: Public Funding Surges on Infrastructure Act

Private investment constituted 85.2% of spending in 2025 across offices, industrial, hospitality, and data center builds financed by REITs, private equity, and corporate balance sheets. Public funding is the fastest-growing source with a 5.60% CAGR through 2031 due to IIJA allocations that continue to move into contract awards and outlays for highways, bridges, transit, and ports. Within the US commercial construction industry, these public projects create spillovers for transit-adjacent mixed-use developments as states and cities rezone nodes to capture private capital near rail stations and interchanges. Federal Land Ports of Entry and other civic facilities are also mobilizing design-build teams and specialty contractors, adding to a baseline of work that stabilizes backlogs through 2026. The public cycle helps offset tightening private credit conditions in select property types and supports regional contractors that specialize in transportation and civic work.

Obligation and outlay data confirm acceleration, with USD 411.5 billion in announced grants, USD 343.3 billion obligated, and USD 189.1 billion outlaid by late 2025, which implies strong bid opportunities for the year ahead. FHWA reports more than 70,000 new federal-aid project commitments and higher-than-average growth in contract values compared with pre-IIJA norms, reinforcing a durable foundation for vertical construction near upgraded corridors. Cities like New York are using public investments to leverage private development in life sciences and housing, which supports construction labor continuity and materials planning across the cycle. State programs in Texas add to this momentum with a USD 39.92 billion TxDOT budget that underwrites multi-year highway work and keeps heavy civil capacity engaged. Procurement compliance and Buy America rules remain important schedule variables, which contractors address through early submittals and supplier vetting to reduce lead-time risks on federally funded work.

Geography Analysis

Texas leads with 17.00% in 2025 on the strength of hyperscale data centers, semiconductor fabrication plants, and a USD 39.92 billion TxDOT budget for fiscal 2026-2027 that sustains construction backlogs tied to corridor upgrades. Florida is the fastest-growing state at a 5.45% CAGR from 2026 to 2031, powered by hospitality recoveries and convention center expansions that feed adjacent retail and mixed-use activity. California holds the second-largest share as nonresidential spending advances and IIJA inflows add visibility to public project pipelines across transportation and education infrastructure. New York’s three-year construction spending plan and MTA allocations are tilting the mix toward nonresidential projects while NYCEDC initiatives like SPARC Kips Bay draw private capital into transit-connected clusters. Illinois is scaling mixed-use, institutional, and bridge programs in Chicago that reinforce multi-year activity across commercial and heavy civil scopes.

The US commercial construction market is benefiting from diversified geographic engines where Sunbelt states absorb logistics and manufacturing demand while coastal markets move public infrastructure and select high-specification towers. Texas continues to capture mega-capital projects that require grid, water, and highway coordination, which supports both vertical and horizontal contractors in 2026. Florida’s hotel and entertainment pipeline remains active, and selective supply responses support project returns even as labor and materials stay tight in certain metro areas. California’s pivot toward civic and education projects reflects permitting complexity and cost structures in private development, yet maintains a consistent workload for large general contractors and specialty subs. New York and Illinois both demonstrate how public investment and zoning can catalyze private mixed-use and life sciences proposals around station areas and corridor upgrades.

States beyond the top tier are gaining share in specific niches. Wisconsin and Virginia are building data center capacity as utility plans and land availability align with campus-scale projects that require long lead times and early procurement of key electrical components. Arizona, Georgia, and North Carolina are securing advanced manufacturing investments due to incentive programs and ease of permitting compared with select coastal markets, which shifts supply chains and subcontractor networks toward these corridors. The US commercial construction market size tied to Florida is projected to expand at a 5.45% CAGR through 2031, reflecting durable tourism and convention demand layered on top of roadway and port investments. Texas maintains a stable growth path as semiconductor, biomanufacturing, and data center ecosystems deepen and reinforce commitments to infrastructure and power projects. New York’s public-private model is set to continue as agencies focus on signal modernization, accessibility, and station-area placemaking that unlocks mixed-use towers in boroughs with strong transit.

Regulatory Landscape

The United States commercial construction regulatory environment remains decentralized, with building and energy codes set primarily at state and local levels rather than under a single federal code. OSHA construction safety requirements (29 CFR Part 1926) continue to anchor federal compliance at jobsites, while federally assisted work is shaped by procurement rules and domestic-content requirements, including Buy America requirements for manufactured products as clarified through Federal Register updates in January 2025.

Code compliance complexity increased as jurisdictions moved at different speeds on International Building Code (IBC) 2024 adoption through early 2026. States such as Virginia, Utah, Indiana, Kansas, Maryland, and New Hampshire adopted IBC 2024, while others, including Washington, Colorado, and North Carolina, advanced through rulemaking. For contractors active in public programs, IIJA-driven surface transportation obligations remained material through fiscal 2026, and 2026 federal activity also included Executive Order 14398 (March 2026) affecting federal contractor requirements. Congress additionally introduced major authorization and appropriations bills (H.R. 8870 and H.R. 9497 in May and June 2026, and H.R. 8469 in April 2026), sustaining a live policy pipeline that influences work packaging, sourcing, and compliance planning.

Value Chain Analysis

The value chain starts with owners and developers (corporate occupiers, REITs, institutional owners, and public agencies) turning demand into project pipelines, then moves through planning, entitlement, and financing. Design (architects and engineers) and preconstruction (estimating, risk, and constructability) follow, with general contractors and construction managers leading execution supported by specialty trades, particularly electrical, mechanical, and HVAC. The chain ends with commissioning and handover, and mission-critical sectors, especially data centers, place greater weight on early equipment selection, testing, and integrated MEP delivery.

In 2026, supply-side constraints and trade policy continue to shape procurement strategy. Long-lead electrical switchgear and medium-voltage equipment, often requiring 30 to 52 weeks, and structural steel lead times of about 14 to 20 weeks in many markets in early 2026, are pushing teams toward earlier releases, alternative sourcing, and prefabrication where feasible. Domestic-content rules under the Build America, Buy America Act (BABAA) affect material traceability on federally assisted projects, and the NIST Manufacturing Extension Partnership (MEP) program is used as a practical resource to identify compliant domestic manufacturers. Upstream capacity is also evolving, with Nucor accelerating commissioning of a new sheet mill in Kentucky in May 2026 (about 3 million tons of annual capacity) to support domestic steel availability, even as labor scarcity in specialty trades remains a bottleneck for schedule certainty.

Competitive Landscape

The US commercial construction market remains fragmented as the top 50 firms account for less than 10% of total revenue, yet consolidation is increasing with a rise in private equity-backed roll-ups targeting specialized trades and regional leaders. The ENR Top 400 reported combined revenue growth in 2024, and the largest firms expanded backlogs in mission-critical, healthcare, and education, with Turner reporting USD 20.2 billion in 2024 revenue and a USD 12.6 billion data center backlog. Bechtel, Kiewit, and Whiting-Turner maintained leading positions, while HITT Contracting scaled rapidly by expanding into mission-critical and industrial, a reflection of demand concentration in data centers and advanced manufacturing. Contractors with vertical integration in MEP and sitework are better positioned to manage lead times and mitigate rework, which has become a differentiator in tight labor and material markets.

Firms are also investing in technology to close field-office data gaps and reduce waste. Cloud-based project management, reality capture, and digital twins are becoming standard, with leading companies experimenting with robotics for layout and repetitive tasks that improve consistency and safety. Hensel Phelps launched a venture platform to pilot construction technologies for high-risk scopes, while Windover demonstrated the operational value of digital twins on campus-scale projects. These capabilities are relevant for data center and hospital programs that require rigorous commissioning and systems integration, a theme that is remaking preconstruction and quality control at scale. Process discipline and early procurement are also more common as tariff regimes keep risk elevated across metals and electrical components, which pushes contractors to add North American suppliers and renegotiate pass-through clauses.

Regional competitive dynamics are shifting as Sunbelt metros see deeper bid benches and more cross-market entries from coastal firms. Nashville reported shrinking subcontractor backlogs and greater bid coverage, while Seattle and Portland saw general contractors expand into nearby markets to defend share and balance exposure. Large awards in Texas, including USD 889 million and USD 746 million interstate reconstruction projects for Balfour Beatty, demonstrate how heavy civil work can anchor backlogs and mobilize multiyear teams. Data center megaprojects in the Mid-Atlantic and Midwest are also concentrating activity with multi-billion-dollar campus contracts that require mission-critical specialists and deep vendor networks. The US commercial construction market remains open for consolidation in specialized trades and for scaled general contractors that can operate across regions, navigate compliance, and deliver at speed for owners with complex programs.

United States Commercial Construction Industry Leaders

Turner Construction Company

The Whiting-Turner Contracting Company

STO Building Group

DPR Construction

Clark Construction Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace concentrates where owners commit capital to high-power, high-complexity facilities, and where public programs catalyze adjacent private development. Mega-scale data center programs offer one of the clearest demand signals: Meta expanded its commitment around the Richland Parish, Louisiana data center in July 2026 to more than USD 50 billion, with plans tied to a larger campus footprint and multi-gigawatt IT capacity. This reinforces opportunities for contractors that can deliver mission-critical work with integrated MEP and early procurement. A second proof point is Related Digital's June 2026 groundbreaking for a USD 16 billion data center project in Saline Township, Michigan, which points to continued geographic broadening of hyperscale activity beyond traditional coastal hubs.

Advanced manufacturing-related commercial and support construction also presents incremental opportunity as projects shift from sitework into vertical build phases, pulling along site infrastructure, utility coordination, and specialized building systems. In July 2026, Micron began vertical construction on its semiconductor campus in Clay, New York after an early concrete milestone, supporting a sustained pipeline of enabling works and supplier-driven facilities around major fabs. Across building types, persistent labor shortages and long-lead electrical equipment availability in 2026 raise the value of delivery models that reduce rework and compress schedules, including design-assist procurement, prefabrication, and digital coordination workflows that improve sequencing, commissioning readiness, and subcontractor productivity.

Recent Industry Developments

- July 2026: Turner Construction highlighted continued expansion of Meta’s Richland Parish, Louisiana data center program, tied to Meta’s stated commitment of more than USD 50 billion for the facility and surrounding region. The scale and power intensity of the build reinforces demand for mission-critical contractors with integrated MEP delivery and long-lead electrical procurement discipline.

- September 2025: Hensel Phelps secured a USD 700 million contract for an airport expansion in Boise, Idaho that includes 10 new gates. The award adds multi-year institutional work to backlogs and supports continued activity for specialty trades and systems integration teams through a long-duration construction schedule.

- September 2024: The Whiting-Turner Contracting Company received major U.S. Coast Guard contract awards spanning work in Seattle, Washington and Kapolei, Hawaii, including waterfront/berth upgrades and hangar construction. These federally funded scopes emphasize compliance-driven delivery and steady demand for civil-vertical interfaces that can stabilize contractor workloads across cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of commercial building construction activity in the United States, including new builds, additions, and major refurbishment work that creates or upgrades income generating, nonresidential properties.

Scope exclusions: It excludes civil infrastructure and public works work such as roads, bridges, rail, water, and utility networks, and it also excludes energy and power generation facilities.

Segmentation Overview

- By Commercial Sector Type

- Office

- Retail

- Industrial & Logistics

- Others

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By States

- Texas

- California

- Florida

- New York

- Illinois

- Rest of US

Data Sources, Market Sizing, and Validation

Desk Research

Desk research set the structure of the model and gave us consistent time series to anchor the market in observed construction activity. We leaned on non paywalled official sources such as the U.S. Census Bureau construction spending releases, the U.S. Bureau of Labor Statistics (producer prices and employment), and the Bureau of Economic Analysis for inflation and macro context that affects building cycles. We also referenced sources such as the Federal Reserve for interest rate trends, and the U.S. Energy Information Administration for electricity demand and data center related signals that influence commercial build intensity.

To turn the public signals into usable sizing inputs, we used a mix of association publications, reputable press, company filings and investor presentations for project pipelines, backlog commentary, and mix shifts across offices, retail, hotels, healthcare, and warehouses. Where needed, our analysts also used paid subscriptions for company financials and intelligence, news and financials, patent databases, and contract and tender tracking to cross check construction starts and award activity. This list is illustrative only, and many other sources were reviewed to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on validating what published data cannot fully explain, especially award timing, the scope split between new build and refurbishment, and the commercial portions of construction that are being postponed or accelerated. We spoke with contractors, specialty trade firms, owners and developers, architects and engineers, and materials distributors, then reconciled the feedback against desk indicators so the final totals remain practical and repeatable.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 18% | APAC: 43% |

| Mid tier: 47% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 18% | Managers: 48% | Americas: 21% |

Market-Sizing & Forecasting

Our sizing starts from a top-down reconstruction of commercial building activity using U.S. construction spending series and project award or start signals, and then we adjust to match the commercial only definition. After that first cut, we corroborate it with selective bottom-up checks, including sampled project values by building type, contractor backlog commentary, and observed pricing and volume patterns in key trades, and then we normalize gaps where coverage is uneven.

A few practical fingerprints were used as recurring inputs (not exhaustive), including nonresidential construction spending levels, shifts in building permits and starts for commercial property types, construction material and labor cost indices, interest rate and lending conditions, and major demand drivers such as logistics absorption and data center build momentum. For forecasting, we used scenario analysis supported by trend smoothing, since commercial pipelines can swing with financing and tenant demand, and those swings are better captured with a base case plus upside and downside views. Assumptions on cost inflation, project delays, and mix change across office, retail, healthcare, lodging, and warehouse facilities were aligned to what interviewees reported and what the public time series suggested.

Data Validation & Update Cycle

Before values are finalized, the market totals are checked against independent signals such as construction employment, price indices, and known shifts in major project pipelines, and then the model is reviewed for outliers year by year. When a variance looks too large, we recheck the drivers, revisit the conversion assumptions, and, in some cases, reconnect with experts to understand whether the change is real or timing related.

Quality checks happen in steps, starting with analyst peer review of inputs, followed by consistency checks across historical and forecast years, and then a final pass before release. Reports are refreshed annually, and interim updates are made when material events affect financing, labor, or a large end use pipeline. Right before delivery, the key series are revalidated so clients receive the most current view available at that time.

Mordor Intelligence's Unitedstates Commercial Construction Market Estimate Compared With Other Published Estimates

Published market values for US commercial construction often vary because each publisher draws the line in a different place, and they also use different timing rules for how construction value is recognized. Differences in whether the number reflects contract awards, work put in place, or a narrower building only slice can move the total by hundreds of billions.

Civil infrastructure work (roads, bridges, utilities, and similar public works) sits outside Mordor Intelligence's scope, which is one of the main reasons the study total does not match estimates built from all nonresidential or all construction spend. Another frequent gap comes from how renovations are treated, how mixed use projects are split across building types, and whether prices are kept in current dollars or adjusted with a different inflation series and currency timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 540.04 B (2025) | |

| Industry Database A | USD 298.60 B (2025) | This figure typically tracks commercial building construction as a narrower revenue category, which can exclude several commercial property types and broader nonresidential scopes that include facilities work tied to income generating sites. |

| Construction Economics Outlet B | USD 2230.00 B (2025) | This estimate reflects total put-in-place construction spending across residential, nonresidential building, and civil, so the definition is much wider than a commercial buildings only market and it also follows in-progress payment timing. |

The spread in the table is largely explained by scope and recognition timing, rather than arithmetic differences. By keeping the model tied to commercial building activity and then cross checking it with public spending series plus practitioner feedback, we provide a value that is easier to trace back to clear drivers and update in a repeatable way.

Key Questions Answered in the Report

What is the US commercial construction market size and growth outlook through 2031?

The US commercial construction market size is USD 567.05 billion in 2026 and is projected to reach USD 723.25 billion by 2031 at a 4.22% CAGR, supported by logistics, data centers, retrofits, and public infrastructure work.

Which segments lead, and which are growing the fastest in the US commercial construction market?

Office led with 35.10% in 2025 while industrial and logistics is the fastest-growing at a 5.44% CAGR during 2026-2031 on e-commerce and reshoring demand.

How are data centers influencing the US commercial construction market in 2026?

Data centers are driving mission-critical backlogs as sector spending is projected to peak in 2026, and utility interconnections shape schedules and site selection.

How does IIJA funding affect private commercial development opportunities?

Federal grants, obligations, and outlays are flowing into highways, transit, and ports, which catalyze transit-adjacent mixed-use towers and stabilize contractor backlogs.

Which states are most attractive for commercial projects right now?

Texas leads with 17.00% in 2025 on hyperscale and semiconductor pipelines while Florida posts the fastest growth at a 5.45% CAGR due to hospitality and convention expansions.

What are the main execution risks for the US commercial construction market in 2026?

The biggest risks are labor shortages, materials and tariff pressures, tighter lending terms, and permitting delays that extend preconstruction and increase carrying costs.

Page last updated on: