UK Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

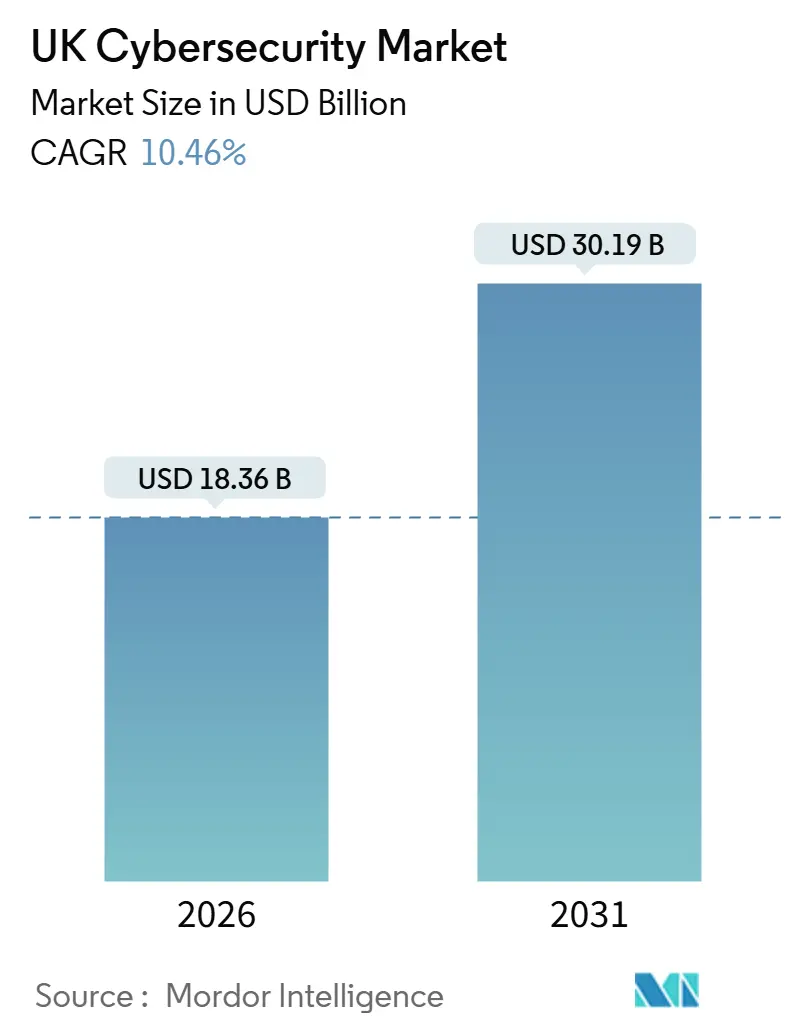

| Market Size (2026) | USD 18.36 Billion |

| Market Size (2031) | USD 30.19 Billion |

| Growth Rate (2026 - 2031) | 10.46% CAGR |

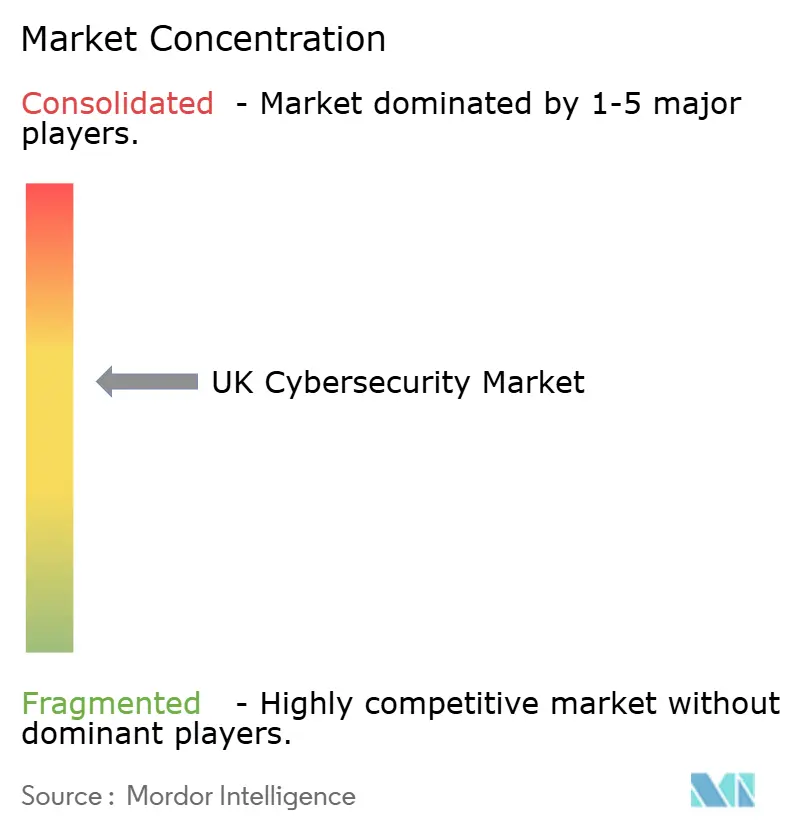

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Cybersecurity Market Analysis by Mordor Intelligence

The UK cybersecurity market reached USD 18.36 billion in 2026 and is projected to attain USD 30.19 billion by 2031, reflecting a 10.46% CAGR. This market size expansion is powered by the rapid escalation of ransomware assaults on critical infrastructure, mandatory zero-trust requirements across public procurement, and stringent compliance milestones under the Telecommunications Security Act and the Digital Operational Resilience Act. Spending momentum is strongest among enterprises migrating to cloud-native security service edge frameworks, while managed detection and response deals flourish as boards accept that 24 x 7 threat monitoring is now a baseline requirement rather than a premium add-on. Competitive pressure from both multinational suites and highly specialized local providers fuels continuous product innovation, particularly around artificial-intelligence analytics that shorten the dwell time of advanced persistent threats. Procurement teams also favor platforms that consolidate audit trails across multiple regulations, which encourages supplier consolidation and multi-year service contracts that lock in predictable cost structures.

Key Report Takeaways

- By offering, managed services led with 62.73% revenue share in 2025, while managed detection and response is advancing at a 12.22% CAGR through 2031.

- By deployment mode, cloud captured 63.84% share of the UK cybersecurity market size in 2025 and is expanding at a 12.32% CAGR through 2031.

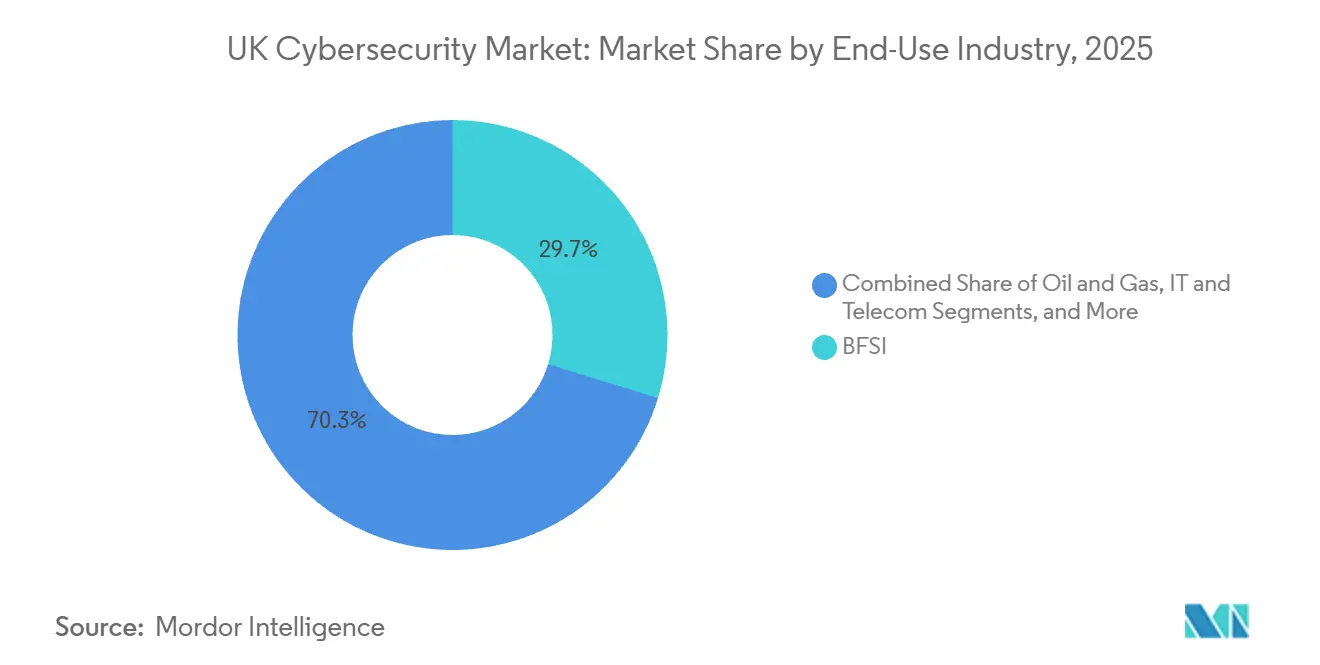

- By end-user industry, banking, financial services, and insurance commanded 29.73% of UK cybersecurity market share in 2025, whereas healthcare is forecast to grow at a 13.67% CAGR to 2031.

- By enterprise size, large enterprises held 61.74% of 2025 spending, yet small and medium enterprises are accelerating at a 12.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UK Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating digitalization and hybrid-work attack surface | +2.3% | National, concentrated in London, Manchester, Edinburgh financial and tech hubs | Medium term (2-4 years) |

| Surge in ransomware and nation-state threats | +2.1% | National, acute in healthcare trusts, local government, energy utilities | Short term (≤ 2 years) |

| Growing UK compliance mandates (Telecom Security Act, DORA) | +1.9% | National, with heightened enforcement in BFSI and telecommunications sectors | Medium term (2-4 years) |

| Rapid adoption of AI-driven security analytics | +1.7% | National, early gains in large enterprises and managed service providers | Long term (≥ 4 years) |

| Government zero-trust procurement requirements | +1.4% | Public sector, cascading to defense contractors and critical national infrastructure suppliers | Medium term (2-4 years) |

| Cyber-insurance underwriting pressures shaping controls | +1.2% | National, most pronounced in SME segment and high-risk verticals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Digitalization And Hybrid-Work Attack Surface

Hybrid work dismantled the traditional perimeter, so organizations now defend thousands of endpoints that sit on domestic broadband with inconsistent patch regimes. National guidance urges secure access service edge rollouts that blend firewall, secure web gateway, and zero-trust network access in a single cloud stack, enabling uniform policies regardless of user location. Regulated firms must also maintain continuous authentication and micro-segmentation, a requirement that effectively pushes cloud-native adoption across finance and technology hubs. Seventy-three percent of large employers intend to keep flexible work patterns, which cements identity-centric security as a long-term necessity. As a result, cloud deployments outpace on-premise alternatives, and vendors heavily promote policy engines that span both remote and campus networks.

Surge In Ransomware And Nation-State Threats

The National Cyber Security Centre recorded a 68% year-on-year jump in ransomware incidents during 2025, linking the spike to ransomware-as-a-service kits that allow entry-level affiliates to execute sophisticated attacks.[1]National Cyber Security Centre, “Annual Review 2025,” ncsc.gov.uk Healthcare systems suffered prolonged outages, while energy utilities confronted supply-chain intrusions traced to Russian and Iranian groups. A government survey found that 32% of businesses endured breaches in 2025, with remediation costs averaging GBP 15,300 (USD 20534.97). Heightened threat pressure pushes enterprises toward managed detection and response contracts that guarantee 24 x 7 coverage and direct escalation to incident-response teams.

Growing UK Compliance Mandates Under Telecom Security Act And DORA

Full enforcement of the Telecommunications Security Act from January 2025 obliges network operators to excise high-risk vendors and adopt continuous vulnerability scanning and encrypted signaling. Parallel preparations for the Digital Operational Resilience Act require annual resilience testing, third-party risk reviews, and near-real-time incident notification in financial services. Banks earmarked more than GBP 1.2 billion (USD 1.61 billion) for compliance-driven security upgrades during 2025, reinforcing demand for platforms that automate evidence gathering across frameworks. Vendors that fuse risk management, penetration testing, and reporting functionality therefore enjoy a sizeable procurement advantage.

Rapid Adoption Of AI-Driven Security Analytics

Artificial-intelligence analytics increasingly supplement signature-based controls by profiling normal behavior and flagging anomalies that signal lateral movement or data exfiltration. Darktrace reported a 42% rise in UK customers using autonomous response modules that can quarantine suspicious activity without human approval. These gains underline a market appetite for tools that compress detection-to-containment cycles from hours to minutes. Yet, adversarial inputs can still poison machine-learning models, so the UK AI Safety Institute continues to develop assurance standards. As best practice matures, enterprises broaden pilot projects into enterprise-wide rollouts, ensuring AI analytics remain a solid contributor to long-term growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute cyber-skills deficit | -1.8% | National, most severe in regions outside London and Southeast | Long term (≥ 4 years) |

| High total cost of ownership for advanced platforms | -1.3% | National, concentrated in SME and mid-market segments | Medium term (2-4 years) |

| Legacy OT and critical-infrastructure systems hard to secure | -0.9% | Energy, utilities, oil and gas, manufacturing sectors | Long term (≥ 4 years) |

| SME under-investment given unclear ROI | -0.7% | National, acute in retail, hospitality, transport, logistics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Cyber-Skills Deficit

Government estimates indicate 14,100 cybersecurity vacancies nationwide in 2025, with senior cloud security engineers in London commanding median salaries of GBP 85,000 (USD 114083.18). Supply shortages inflate labor costs and prolong implementation schedules, prompting enterprises to outsource security operations to specialist providers. Apprenticeship schemes and university investment will ease shortages only in the medium term, so managed services remain the primary stopgap, reinforcing their double-digit growth trajectory.

High Total Cost Of Ownership For Advanced Platforms

Licenses for extended detection and response or identity governance suites often exceed GBP 50,000 (USD 67107.75) annually for mid-sized businesses, and integration projects add another 30-50% in services fees. Small and medium enterprises, which comprise 99% of UK companies, find it difficult to justify such sums when payback depends on avoiding hypothetical breach losses. The Federation of Small Businesses reports that 41% of members cite budget constraints as the main barrier to adopting advanced controls.[2]Federation of Small Businesses, “Small Business Cyber Security Report 2025,” fsb.org.uk Vendors are responding with usage-based pricing, yet overall affordability remains a real drag on wider adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Command Spending As In-House Skills Erode

Services captured 62.73% of UK cybersecurity market share in 2025, and this slice is projected to widen at a 12.22% CAGR. Managed detection and response has become the fastest-growing line item because enterprises can activate cloud sensors within days and receive round-the-clock threat hunting for a recurring fee that is simpler to budget than staffing an internal security operations center. Professional services demand also rises as compliance mandates proliferate and boards commission gap analyses, penetration tests, and resilience rehearsals. In contrast, the solutions segment remains essential but lags in percentage growth, with buyers favoring cloud-native tools that bundle firewall, zero-trust network access, and secure web gateway features into a single subscription. Identity and access management ranks as the most consistently purchased solution because zero-trust designs rest on strong authentication and least-privilege authorizations. Application security tooling attracts software-as-a-service vendors that integrate static, dynamic, and software composition analysis into continuous-integration pipelines. Despite steady interest in endpoint, network, and data security products, spending tilts toward service engagements that wrap expert oversight around these technologies.

The UK cybersecurity market size for services is forecast to accelerate further as public entities mandate that critical suppliers hold round-the-clock security monitoring certifications. Meanwhile, vendors that operate multiple regional security operations centers hedge latency risks, meet data-residency clauses, and guarantee continuity in the event of localized outages. Multiyear outsourcing is therefore likely to reach a higher penetration rate among both highly regulated industries and mid-market firms that once relied on reactive outsourcing on an ad hoc basis.

By Deployment Mode: Cloud Solutions Dominate As Perimeter Dissolves

Cloud captured 63.84% of UK cybersecurity market size in 2025, growing at a 12.32% CAGR, while on-premises deployments expand at mid-single-digit rates. Remote and hybrid workforces require identity-centric architectures, so organizations adopt security service edge platforms that enforce consistent policies across any location. Government and financial regulators endorse multi-cloud strategies paired with centralized identity federation, which further validates vendor roadmaps built around cloud-first controls. Enterprises note that activating cloud protection can take days, whereas procurement, racking, and maintenance cycles slow on-premises platforms. Even industries with strict data localization rules embrace hybrid designs that keep sensitive records onsite but shift analytics to elastic cloud nodes.

On-premises estates persist in segments that run legacy operational technology, such as manufacturing, energy, and utilities. Air-gapped programmable logic controllers cannot interface with external platforms, so asset owners deploy intermediary sensors and network taps to gain telemetry. Vendors blend these deployments with cloud-hosted management consoles, which illustrates the broader trend toward flexible consumption models. However, migration introduces misconfiguration risks, and cloud security posture management is now bundled into most enterprise contracts to check compliance against Center for Internet Security benchmarks automatically.

By End-User Industry: Healthcare Growth Surges As BFSI Remains Core

Banking, financial services, and insurance retained 29.73% of UK cybersecurity market share in 2025, a position underpinned by continuous regulatory scrutiny from the Financial Conduct Authority and the Prudential Regulation Authority.[3] Budgets cover zero-trust migration for trading platforms, continuous monitoring of third-party vendors, and automated reporting for operational resilience tests. Healthcare, however, records the swiftest expansion with a 13.67% CAGR through 2031. Ransomware assaults on hospital trusts in 2025 triggered elective surgery delays and forced a government-backed GBP 250 million uplift program that funds endpoint detection, network segmentation, and encrypted backups. Moreover, electronic health record modernization goes hand in hand with enhanced identity management to protect sensitive patient data.

Government ministries and local councils also enlarge spending to satisfy zero-trust mandates that now form mandatory contractual language for all departments. Telecommunications operators invest heavily to swap high-risk 5G components and harden signaling. Retail and e-commerce entities deploy fraud detection and tokenization to stem an 18% rise in card-not-present transactions. Manufacturing and industrial sectors focus on network segmentation inside supervisory control networks, while energy utilities adopt anomaly detection sensors to monitor power-generation turbines. Despite varied priorities, every vertical now views cybersecurity as a board-level operational requirement rather than an IT line item.

By End-User Enterprise Size: SME Adoption Gains Momentum Under Insurance Pressure

Large enterprises accounted for 61.74% of 2025 spend, supported by in-house security engineering staff and multi-layered defenses that cover endpoints, networks, and cloud workloads. Growth in this tier is steady but incremental, given that many large organizations already operate mature security programs. Small and medium enterprises, by contrast, log a 12.46% CAGR, catalyzed by cyber-insurance underwriters that refuse cover unless buyers implement multi-factor authentication, maintain up-to-date software, and store offline backups. Insurers leverage actuarial claims to adjust pricing in real time, so SMEs quickly realize that even a modest investment in baseline controls can cut premiums by tangible percentages.

The UK cybersecurity market size for SMEs remains smaller on an absolute basis, yet the addressable headcount of 5.5 million businesses makes the collective opportunity substantial. Vendors tailor bundles that fold endpoint, email, and web protection into a single agent, add managed detection oversight, and expose simplified dashboards suitable for non-specialists. Consumption-based packages resonate because SMEs can scale up during peak trading seasons and scale down afterward, flattening cost curves. As compliance pressures, insurance audits, and customer expectations converge, SME adoption deepens, closing the maturity gap versus large enterprises.

Geography Analysis

London and the Southeast dominate UK cybersecurity outlays, representing about 38% of national spend in 2025. The capital hosts a dense cluster of financial institutions, global law firms, and technology unicorns that each operate multi-cloud estates and face high regulatory hurdles. Consequently, suppliers concentrate sales teams and demonstration centers inside the M25 corridor. Scotland ranks second as Edinburgh’s finance quarter and Glasgow’s maturing tech scene secure resources through the Scottish Government’s GBP 15 million Cyber Resilience Strategy, which funds SME security upgrades and university laboratories. Regional managed service providers fill skills gaps by co-locating operations centers near universities to tap graduate pools.

The Midlands and Northern England exhibit moderate but accelerating demand as manufacturing and logistics hubs digitize supply chains. Here, operational technology security drives purchases of anomaly detection sensors and network segmentation gear, reflecting threats posed by nation-state actors probing industrial control systems. Wales and Northern Ireland remain smaller in absolute terms, yet government grants encourage local councils and hospitals to migrate email, productivity software, and security controls to sovereign cloud platforms. Devolved cybersecurity strategies incentivize managed service providers to open satellite offices, ensuring on-the-ground incident response without lengthy travel.

Cross-border regulatory alignment further molds the landscape. Post-Brexit, UK regulators mirror the European Union’s Digital Operational Resilience Act to facilitate trade in financial services, so multinationals insist on tools that satisfy both rulebooks. Participation in Five Eyes intelligence networks provides early warning of zero-day exploits, influencing vendor patch management timelines. Finally, joint exercises under NATO’s Cooperative Cyber Defense Centre sharpen military and civilian readiness, translating into procurement of devices hardened to common evaluation assurance level benchmarks.

Competitive Landscape

The market is moderately fragmented, with the five largest vendors (Darktrace, Sophos, NCC Group, BAE Systems Digital Intelligence, and BT Security) holding a 35% share in 2025. Darktrace capitalizes on machine-learning analytics that automatically quarantine anomalous behavior, winning contracts in sectors pressed by the cyber-skills shortage. Sophos differentiates through a global network of security operations centers that deliver managed detection and response aligned to mid-market price points. NCC Group leverages its deep penetration-testing roots to advise banks and telecom operators on their obligations under the Telecommunications Security Act and DORA.

Second-tier specialists, including Bridewell Consulting, Integrity360, and Quorum Cyber, capture niches by marrying domain knowledge with flexible commercial models. Bridewell helps healthcare trusts comply with National Health Service governance, while Integrity360 focuses on DevSecOps and cloud posture for software-as-a-service vendors. Strategic partnerships increasingly determine success. BT Security wraps Microsoft Sentinel analytics into its managed extended detection and response stack, giving clients unified insight across on-premises and multi-cloud assets. BAE Systems Digital Intelligence leverages sovereign data-handling assurances to secure defense contracts that require classified threat intelligence.

Innovation hotspots revolve around operational technology isolation, consumption-based licensing, and autonomous response. Darktrace’s 2026 product launch that shields programmable logic controllers without halting production exemplifies the trend toward harmonizing IT and OT security. Meanwhile, Immersive Labs trains cyber teams via gamified simulations, addressing talent shortages that otherwise impede technology rollouts. Certification schemes from the UK Cyber Security Council introduce standardized professional tiers, which reduces vendor differentiation based solely on staffing credentials and pivots competitive emphasis to the measurable efficacy of detection algorithms and integration breadth.

UK Cybersecurity Industry Leaders

Darktrace plc

Sophos Group plc

NCC Group plc

BAE Systems Digital Intelligence

BT Group plc (BT Security)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Darktrace expanded autonomous response to operational technology, enabling industrial systems to isolate compromised controllers without stopping production.

- December 2025: Sophos completed the acquisition of Secureworks’ managed detection and response business for USD 450 million.

- November 2025: BAE Systems Digital Intelligence won a GBP 120 million (USD 161.06 million) contract with the UK Ministry of Defence for threat intelligence and incident response.

- October 2025: NCC Group launched a DORA compliance advisory practice that generated GBP 8 million (USD 10.74 million) in revenue within its first quarter.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom cybersecurity market as the yearly revenue that suppliers earn from purpose-built software, hardware appliances, and professional or managed services deployed to prevent, detect, respond to, or recover from unauthorized digital activity across corporate, public-sector, and critical-infrastructure environments. Values are expressed in constant 2024 US dollars and capture spending generated within UK borders by both domestic and foreign vendors.

Scope Exclusions: Consumer-grade antivirus suites sold at retail and stand-alone cyber-insurance premiums are not included in our sizing.

Segmentation Overview

- By Offering

- Solutions

- Application Security

- Cloud Security

- Data Security

- Network Security

- Endpoint Security

- Infrastructure Protection

- Integrated Risk Management

- Identity and Access Management (IAM)

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premise

- By End-user Industry

- BFSI

- Government and Public Sector

- Oil and Gas

- IT and Telecom

- Retail, E-commerce and Consumers

- Manufacturing and Industrial

- Energy and Utilities

- Healthcare

- Other End-user Industries (Transport, Logistics, Education, Hospitality)

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed CISOs at banks, NHS trusts, energy operators, and fast-growing fintechs across England, Scotland, and Wales, alongside MSSP product leads and former NCSC assessors. Conversations validated price bands, adoption lags among SMEs, and the real-world impact of regulatory deadlines, filling data gaps flagged during desk work.

Desk Research

We began with public datasets from the Department for Science, Innovation and Technology, the National Cyber Security Centre breach surveys, Ofcom telecom security filings, HMRC trade codes, and pan-European notices issued under GDPR and the upcoming DORA rules. Company 10-Ks, prospectuses, and investor decks helped us benchmark vendor segment splits, while academic journals such as Computers & Security clarified attack-vector prevalence. Paid libraries, D&B Hoovers for revenue splits and Dow Jones Factiva for deal flow, supplemented open sources when recent numbers were scarce. This list is illustrative; many additional materials were consulted for cross-checks and context building.

Market-Sizing & Forecasting

A top-down model draws on DSIT revenue totals and Customs import data, which are then segmented by offering and end-user through penetration-rate adjustments derived from breach-incident ratios and average security spend per employee. Supplier roll-ups and sampled average-selling-price × volume checks provide a bottom-up lens that guides final weighting. Core variables include (i) number of ICO-reported breaches, (ii) cloud workload share of UK enterprise IT, (iii) ransomware incident count from Police CyberCrime Unit logs, (iv) regulated-sector security budget index, and (v) GBP-USD exchange path. Forecasts to 2030 employ a multivariate regression that links these drivers to historic spend and tests three demand scenarios agreed with interviewees; gaps in granular vendor data are bridged with channel-check derived ratios.

Data Validation & Update Cycle

Before sign-off, independent analysts run variance screens against external revenue tallies, DSIT growth signals, and macro indicators. Outliers trigger re-contacts with domain experts. The report is refreshed each year, and mid-cycle updates are issued when material events, such as the Cyber Resilience Bill's passage, shift the baseline.

Why Mordor's UK Cybersecurity Baseline Is Trusted

Published estimates often diverge because research houses pick different spending buckets, exchange-rate bases, or refresh cadences.

Key gap drivers here include varying treatment of hardware-centric sales, inclusion of adjacent insurance or physical security outlays, and whether managed services are counted separately or folded into solutions. Mordor's scope mirrors government taxonomy, applies current-year average FX, and is updated annually, which limits drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.88 B (2025) | Mordor Intelligence | - |

| USD 11.58 B (2024) | Global Consultancy A | Hardware-heavy scope; refresh every two years |

| USD 15.00 B (2024) | Industry Research House B | Adds cyber-insurance and physical access control spend |

| USD 10.31 B (2025) | Trade Journal C | Excludes managed security services; early-year FX lock-in |

The comparison shows that when differing inclusions, currency assumptions, and update rhythms are neutralized, Mordor's disciplined, variable-linked approach delivers a balanced figure that clients can trace back to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the forecast value of the UK cybersecurity market in 2031?

Spending is projected to reach USD 30.19 billion by 2031, reflecting a 10.46% CAGR.

Which deployment mode is growing fastest across UK organizations?

Cloud-delivered security solutions are expanding at a 12.32% CAGR as hybrid work cements perimeter dissolution.

Why are SMEs increasing cybersecurity budgets?

Insurers now demand multi-factor authentication, patch management, and offline backups before issuing cyber policies, pushing SMEs toward managed service bundles.

Which industry segment shows the highest growth through 2031?

Healthcare spending is set to climb at a 13.67% CAGR due to government-funded modernization and ransomware risk.

How severe is the UK cyber-skills shortage?

An estimated 14,100 roles remained unfilled in 2025, causing salary inflation and longer project timelines.

What role does artificial intelligence play in modern UK defenses?

Enterprises deploy AI analytics to baseline normal behavior and isolate anomalies within minutes, shrinking adversary dwell time.

Page last updated on: