Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

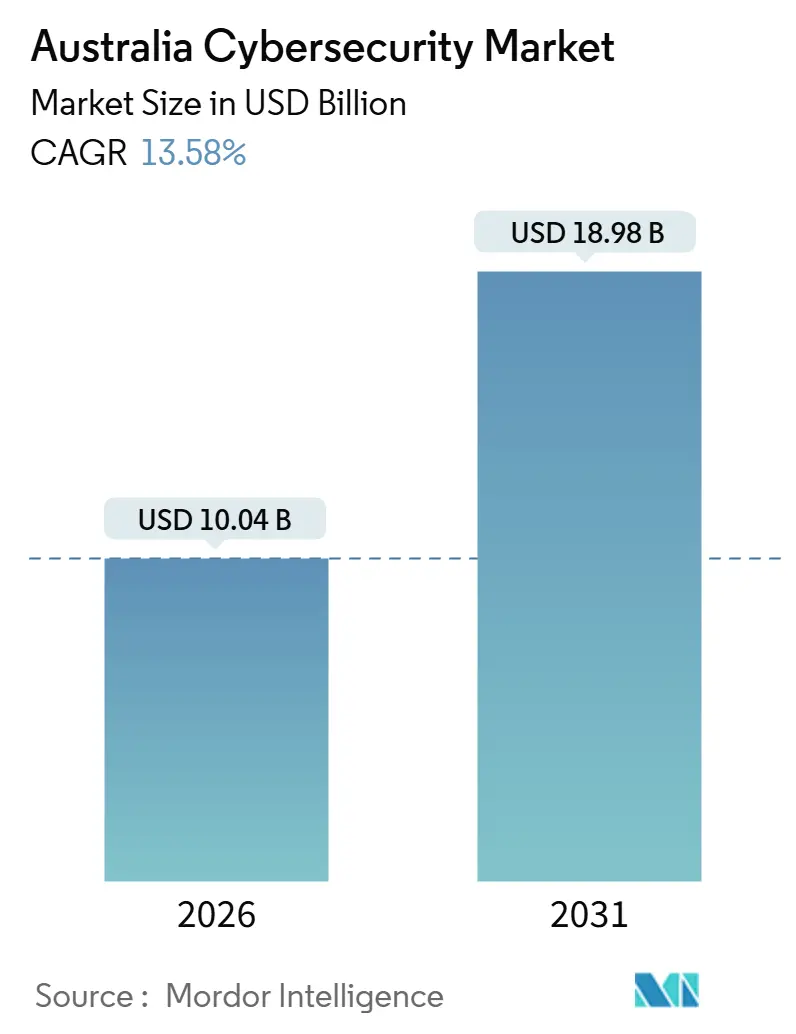

| Market Size (2026) | USD 10.04 Billion |

| Market Size (2031) | USD 18.98 Billion |

| Growth Rate (2026 - 2031) | 13.58% CAGR |

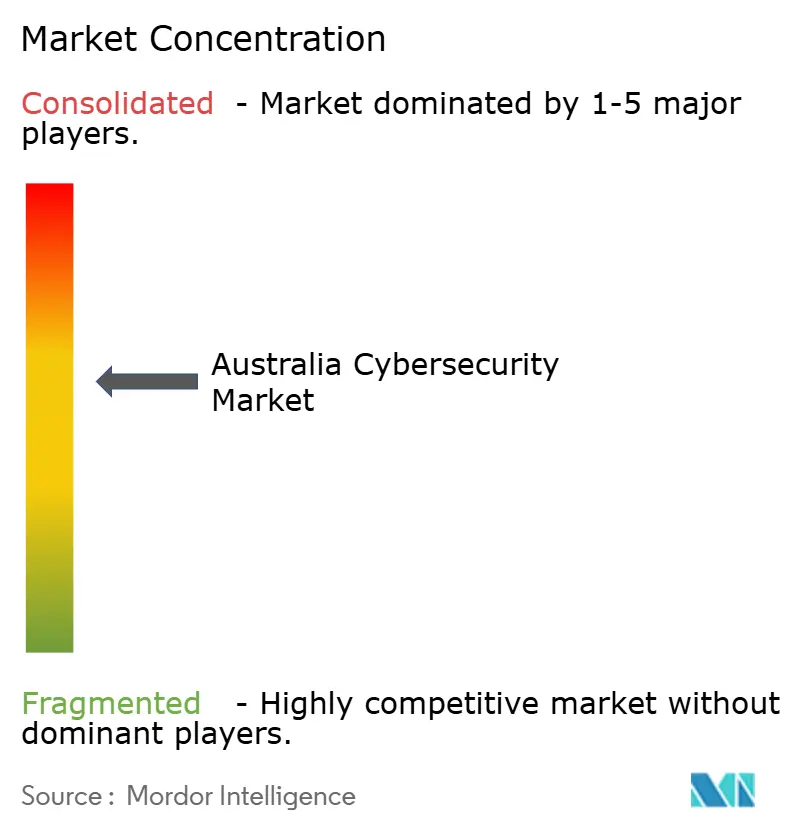

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Cybersecurity Market Analysis by Mordor Intelligence

The Australia cybersecurity market size is valued at USD 10.04 billion in 2026 and is projected to reach USD 18.98 billion by 2031, delivering a 13.58% CAGR over the forecast period. Demand is expanding faster than overall information-technology budgets as mandatory breach-disclosure rules rolled out in May 2025 and broader Security of Critical Infrastructure obligations compel enterprises to tighten defenses. High-profile attacks, most notably the 2024 MediSecure incident, are steering investments toward cloud-native controls, zero-trust architectures, and managed detection and response programs that alleviate the 30,000-person skills shortfall. Spending is also rising because organizations must refresh cryptographic hardware to meet post-quantum standards while aligning with the Australian Protective DNS initiative, which has become a de facto benchmark for government and critical-infrastructure operators. Heightened venture-capital inflows into local start-ups focused on operational-technology (OT) monitoring confirm that the Australia cybersecurity market will retain double-digit momentum for the rest of the decade.

Key Report Takeaways

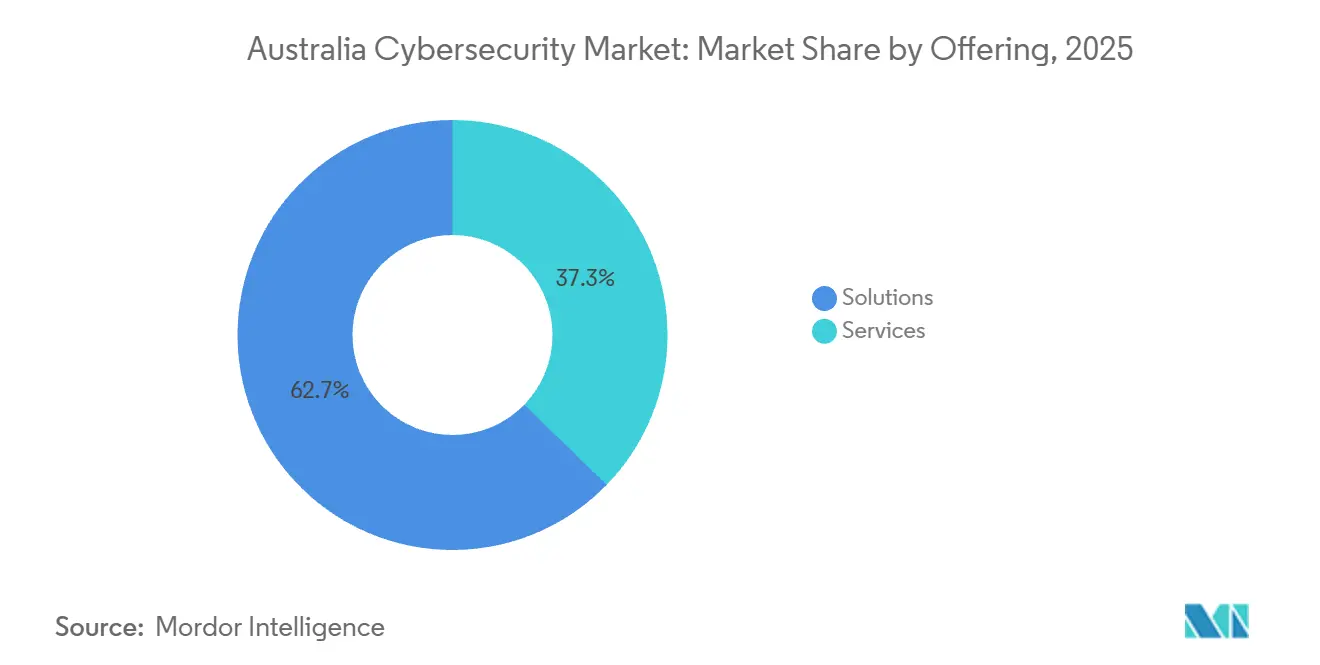

- By offering, solutions led with 62.73% revenue share in 2025, whereas services are anticipated to expand at a 15.22% CAGR through 2031.

- By deployment mode, cloud captured 63.84% of the Australia cybersecurity market share in 2025, and this segment is forecast to grow at a 15.32% CAGR over 2026-2031.

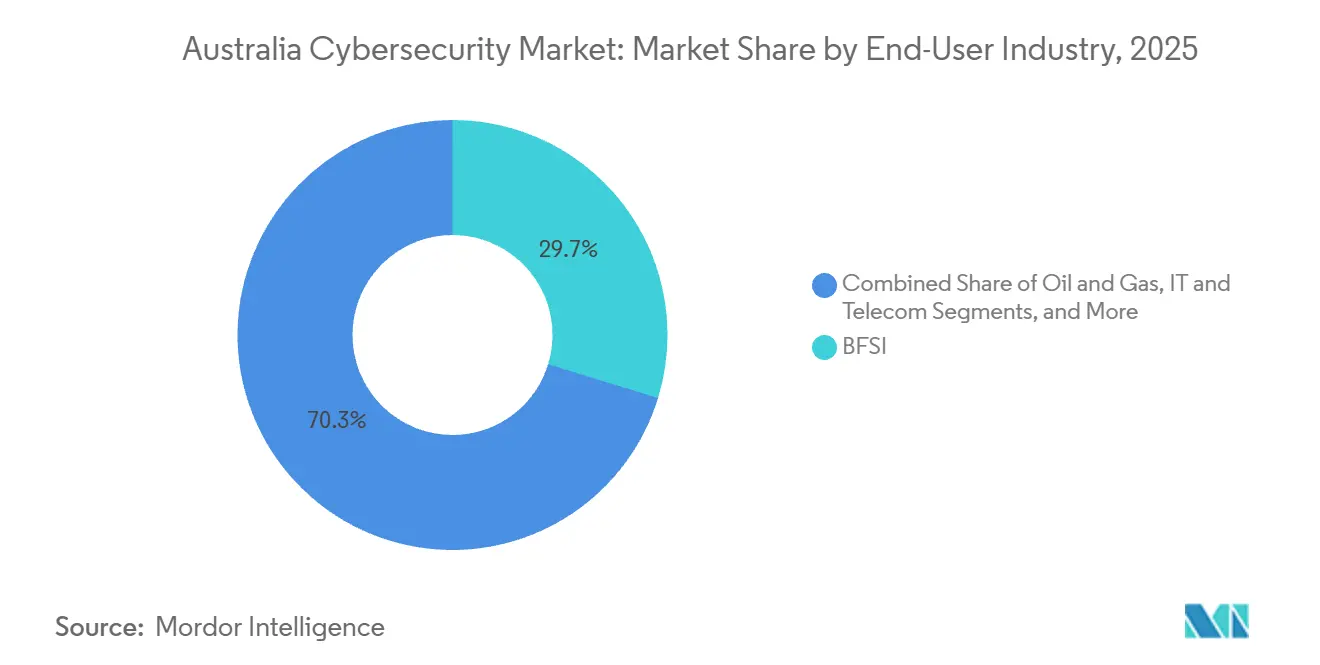

- By end-user industry, banking, financial services and insurance held 29.73% of 2025 spending, while healthcare is poised to rise at a 14.65% CAGR to 2031.

- By enterprise size, large organizations commanded 61.74% of 2025 revenue, yet small and medium enterprises are projected to post a 15.42% CAGR, the fastest across all tiers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume and sophistication of attacks | +3.2% | National, acute in healthcare, BFSI and government | Short term (≤ 2 years) |

| Mandatory breach-reporting and critical-infrastructure laws | +2.8% | National, enforced by OAIC and Department of Home Affairs | Medium term (2-4 years) |

| Cloud adoption across enterprises | +2.5% | National, led by Sydney and Melbourne metro areas | Medium term (2-4 years) |

| Proliferation of IoT/OT endpoints | +1.9% | National, concentrated in energy, utilities, manufacturing and transport | Long term (≥ 4 years) |

| Australian Protective DNS ecosystem expansion | +1.4% | National, government agencies and critical-infrastructure operators | Medium term (2-4 years) |

| Post-quantum cryptography-readiness mandates | +0.9% | National, prioritized in defense, finance and telecommunications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Volume and Sophistication of Attacks

Ransomware notifications climbed 23% year-on-year to June 2025, and 41% of cases involved healthcare and local governments.[1]Australian Cyber Security Centre, “Annual Cyber Threat Report 2024-25,” cyber.gov.au Living-off-the-land techniques now dominate intrusions, forcing organizations to deploy behavior-based analytics and extended detection platforms. Supply-chain compromises jumped 34% in 2024, prompting wider use of software bills of materials and continuous vulnerability scans. Privacy Act penalties, which can hit AUD 50 million (USD 33 million), are accelerating endpoint-security and identity-governance rollouts. Collectively, these trends strengthen growth prospects for the Australia cybersecurity market.

Mandatory Breach-Reporting and Critical-Infrastructure Laws

Amendments to the Security of Critical Infrastructure Act, fully enforced from April 2024, brought 11 sectors under compulsory cyber-risk programs. Entities classed as systems of national significance must report incidents within 12 hours and reach at least level 2 on the Essential Eight maturity scale, boosting demand for automated compliance software. The standalone Cyber Security Act 2024 added ransomware-payment disclosure requirements, creating a public registry that insurers and regulators now use to benchmark sector exposure. Notifiable data breaches rose 19% in the first half of 2025. As a result, budgets shift toward integrated risk-management platforms that consolidate scans, audit logs and incident timelines.

Cloud Adoption Across Enterprises

Multi-cloud penetration among firms with 500+ employees reached 68% in 2025, up from 54% two years earlier. This architecture drives uptake of cloud-security posture management, cloud access brokers and serverless firewalls that fit infrastructure-as-code workflows. Updated APRA guidance obliges regulated entities to monitor configurations continuously and to control encryption keys within Australian data centers, prompting widespread deployment of key-management services. Hybrid estates still account for 47% of footprints, so unified policy engines that span on-premise and public clouds remain in high demand. Certified vendors under the Hosting Certification Framework increasingly dominate public-sector contracts.

Proliferation of IoT/OT Endpoints

Distributed energy resources exceeded 20 GW of capacity in 2025, each adding internet-connected inverters that rarely feature robust authentication. Operators must now segment OT networks and implement anomaly detection, expanding the addressable market for industrial firewalls and secure remote gateways. In manufacturing, 62% of factories had not patched controller firmware during 2024, heightening risk. Essential Eight controls have become mandatory for critical-infrastructure owners, so asset-discovery and vulnerability-management platforms that understand Modbus and DNP3 protocols are enjoying faster uptake. These factors lift the long-term baseline for the Australia cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe cybersecurity-talent shortage | -1.8% | National, acute in regions outside Sydney and Melbourne | Medium term (2-4 years) |

| High total cost of ownership for SMEs | -1.3% | National, firms with fewer than 200 employees | Short term (≤ 2 years) |

| Edge-device replacement lag amid hardware supply bottlenecks | -0.7% | National, pronounced in manufacturing and logistics | Short term (≤ 2 years) |

| Rising cyber-insurance exclusions and coverage gaps | -0.6% | National, revenue between AUD 50 million and AUD 500 million | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Cybersecurity-Talent Shortage

The 2025 Digital Pulse report pegged the workforce gap at 30,000 professionals, with demand increasing 14% annually while supply grows only 6%.[2]Australian Computer Society, “Digital Pulse 2025,” acs.org.au Federal agencies alone will need 10,000 additional specialists by 2028. Median salary for a senior architect in Sydney hit AUD 180,000 (USD 120,000) in 2025, up 22% from 2023. Small enterprises cannot match these pay scales, turning instead to managed services. Although the Cyber Security Skills Partnership plans to train 5,000 practitioners by 2027, the near-term shortage limits deployment of threat-hunting and red-team exercises.

High Total Cost of Ownership for SMEs

SMEs form 98% of Australian businesses but often spend less than AUD 10,000 (USD 6,700) on security annually. Vouchers worth AUD 500 (USD 335) under the Cyber Wardens program attracted only 15,000 registrants by mid-2025. Subscription minimums and integration complexity deter adoption of enterprise-grade platforms, driving interest in bundled endpoint, email and backup services that trade depth for affordability. While these packages reduce entry barriers, they seldom provide advanced threat intelligence, leaving SMEs exposed and slightly dampening expansion of the Australia cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Solutions as Talent Scarcity Bites

Services accounted for 37.27% of 2025 spending yet are forecast to grow 2 percentage points faster than solutions through 2031 as organizations outsource security operations to offset staffing gaps. Managed detection and response contracts, typically priced on a per-node basis, convert capital outlays into operating expenses and guarantee 24/7 coverage. Professional services remain buoyant because Essential Eight audits and Security of Critical Infrastructure attestations must be refreshed yearly. Solutions still dominate the Australia cybersecurity market size, underpinned by endpoint, identity and cloud-security platforms that now bundle extended detection capabilities. Vendors offering static and dynamic code-analysis tools are winning new customers after the Secure Software Development Framework mandated software bills of materials for government suppliers.[3]Australian Signals Directorate, “Essential Eight Maturity Model,” asd.gov.au Integrated risk-management suites that correlate vulnerability scans with compliance evidence are emerging as a standalone category.

Second-generation controls are rapidly shifting to software-as-a-service models. Data-loss prevention is now built into productivity suites, while zero-trust network access is displacing conventional VPNs across remote-work environments. Distributed denial-of-service mitigation and web-application firewalls are consolidating around providers that share threat intelligence via unified consoles. As workforce shortages persist, license models emphasizing automation gain favor, adding long-run elasticity to the Australia cybersecurity market.

By Deployment Mode: Cloud Dominates as Hybrid Complexity Rises

Cloud held 63.84% of 2025 revenue and is projected to post a 15.32% CAGR thanks to enterprises shifting workloads to hyperscale platforms. Multi-cloud estates make policy consistency a top concern, so security-posture management tools that normalize alerts across providers are scaling quickly. Banks and insurers, guided by APRA’s revised CPS 234, encrypt data at rest with keys managed domestically, driving uptake of customer-controlled key-management services. On-premise deployments grow more slowly yet remain critical in defense, where latency and sovereignty requirements prevail. The Australia cybersecurity market share held by hybrid architectures will stabilize because 47% of firms still blend legacy data centers with public cloud assets.

Edge computing introduces fresh risk at factory floors and logistics hubs, so lightweight agents that can run on small form-factor gateways are in high demand. The government Hosting Certification Framework effectively bifurcates the supplier landscape into certified and non-certified tiers, concentrating public-sector spending among a handful of vetted providers. As subscription offerings proliferate, enterprises expect usage-based pricing, reinforcing the structural shift toward operating-expense models.

By End-User Industry: Healthcare Surges as BFSI Maintains Lead

Banking, financial services and insurance retained a 29.73% slice of the Australia cybersecurity market size in 2025, fortified by early zero-trust adoption and stringent CPS 234 oversight. Healthcare spending, however, is projected to climb at a sector-leading 14.65% CAGR after the MediSecure breach exposed systemic vulnerabilities. Government agencies focus on the Essential Eight and the Protective DNS rollout, pulling demand for recursive filtering and log-archival services. OT-intensive sectors such as oil and gas deploy anomaly detection and segmentation to secure industrial control systems labeled as systems of national significance.

Technology and telecommunications firms prioritize secure software-development pipelines, while retail and e-commerce expand fraud-prevention budgets as online sales reach 18% of total transactions. Manufacturers continue to lag on firmware patching despite new obligations, and energy utilities are integrating cybersecurity into distributed resource management systems. Across each vertical, regulatory compliance rather than discretionary innovation drives most incremental spending, amplifying predictable revenue flows for suppliers.

By End-User Enterprise Size: SMEs Accelerate Amid Simplified Offerings

Large enterprises contributed 61.74% of 2025 revenue, yet SME spending will rise faster at a 15.42% CAGR through 2031 as simplified bundles reach price points below AUD 100 (USD 67) per user per year. Many mid-market firms adopt managed detection and response to avoid capital purchases, shifting the Australia cybersecurity industry toward consumption-based contracts. Voucher schemes under the Cyber Wardens program stimulate baseline assessments but have not yet translated into widespread platform adoption. SMEs typically favor SaaS endpoint protection and identity governance because they sidestep appliance procurement.

For large organizations, zero-trust projects dominate roadmaps, with Microsoft reporting 41% growth in conditional-access deployments during 2025. Hybrid SOC models that blend in-house analysts with external playbook automation are gaining traction, moderating total-cost-of-ownership. Over time, maturity-scaled Essential Eight guidance is expected to narrow capability gaps, making SMEs an increasingly critical growth engine for the Australia cybersecurity market.

Geography Analysis

New South Wales and Victoria together generated roughly 62% of 2025 expenditure, reflecting the concentration of banks, insurers and federal offices in Sydney and Melbourne. APRA’s real-time visibility requirements and in-country key custody accelerate cloud-security outlays among headquarters clustered in these states.

Queensland is positioning Brisbane as a secondary cyber hub, requiring all agencies to reach Essential Eight level 2 by mid-2026, which spurs compliance-monitoring purchases. Western Australia and South Australia emphasize OT security for mining and energy infrastructure after distributed resources topped 20 GW in 2025.

The Australian Capital Territory benefits from Protective DNS coverage across 500 agencies, with trials now extending to critical-infrastructure operators. Tasmania and the Northern Territory remain smaller markets but gain from co-funding vouchers that push baseline assessments into regional SMEs. Skills shortages are stark outside major metros; 72% of practitioners reside in Sydney, Melbourne and Canberra, so regional enterprises lean on managed services. Hosting Certification rules and Five Eyes threat-intelligence exchanges influence procurement nationwide, while post-quantum mandates spur uniform hardware refreshes across every state.

Competitive Landscape

The Australia cybersecurity market sits in a mid-consolidation phase, where global platform providers such as Microsoft, Palo Alto Networks, CrowdStrike and Cisco hold sizable footprints while domestic specialists anchor regional relationships. The Hosting Certification Framework funnels most public-sector workloads toward a small cohort of certified cloud and security operators, reinforcing scale advantages for vendors that can fund recurring audits. Even so, stringent local-data and incident-response requirements leave room for providers with deep on-shore personnel and intimate knowledge of Essential Eight controls. Competitive intensity therefore pivots on a vendor’s capacity to blend extensive threat-intelligence telemetry with localized service delivery and audit-ready reporting features.

Domestic champion CyberCX continues to pursue a roll-up strategy, adding OT depth through its September 2024 acquisition of Gridware and later embedding Palo Alto Networks’ Cortex XSIAM into its managed detection platform in December 2025. Telstra Purple leverages carrier reach and a five-year, AUD 120 million managed-security contract from the Department of Defence to raise barriers for smaller MSSPs. Zettagrid’s purchase of Tesserent in March 2025 underscores the capital requirements of scaling 24/7 security-operations-center networks and highlights how access to debt and equity financing can determine survival. Meanwhile, Microsoft deepens local presence by expanding its Sydney Cyber Security Centre and integrating Azure Sentinel and Defender for Cloud into partner offerings, marrying hyperscale telemetry with domestic incident-response staffing.

Niche suppliers are carving defensible positions by focusing on single pain points. Kasada’s bot-management platform protects e-commerce checkout flows, while Fortinet’s FortiGate and FortiSIEM suites remain popular among critical-infrastructure owners that value hardware acceleration and on-premise control. Darktrace differentiates through self-learning anomaly detection that it claims identifies zero-day exploits weeks ahead of signature-based systems. Venture-capital funding is also flowing to start-ups that monitor operational-technology traffic, automate Essential Eight compliance evidence and secure software build pipelines, broadening the competitive field even as top-five vendors still capture roughly 60% of spending.

Australia Cybersecurity Industry Leaders

Accenture plc

Check Point Software Technologies Ltd.

Cisco Systems, Inc.

CrowdStrike Holdings, Inc.

CyberArk Software Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: CyberCX partnered with Palo Alto Networks to embed Cortex XSIAM into its managed detection platform, targeting a 40% cut in mean time to detect and respond.

- November 2025: Microsoft expanded its Sydney Cyber Security Centre, hiring 150 staff and launching an OT-focused practice.

- October 2025: Telstra Purple won a AUD 120 million (USD 80 million) five-year managed-security contract with the Department of Defence.

- September 2025: CrowdStrike opened a Sydney data center to satisfy data-residency demands for public-sector clients.

Australia Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and by phishing in order to maintain data confidentiality.

The Australia Cybersecurity Market Report is Segmented by Offering (Solutions including Application Security, Cloud Security, Data Security, Network Security, Endpoint Security, Infrastructure Protection, Integrated Risk Management, Identity and Access Management; Services including Professional Services and Managed Services), Deployment Mode (Cloud and On-Premise), End-User Industry (BFSI, Government and Public Sector, Oil and Gas, IT and Telecom, Retail E-commerce and Consumers, Manufacturing and Industrial, Energy and Utilities, Healthcare, Other Industries), and End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Network Security | |

| Endpoint Security | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Identity and Access Management (IAM) | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Government and Public Sector |

| Oil and Gas |

| IT and Telecom |

| Retail, E-commerce and Consumers |

| Manufacturing and Industrial |

| Energy and Utilities |

| Healthcare |

| Other End-user Industries (Transport, Logistics, Education, Hospitality) |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Network Security | ||

| Endpoint Security | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Identity and Access Management (IAM) | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Government and Public Sector | ||

| Oil and Gas | ||

| IT and Telecom | ||

| Retail, E-commerce and Consumers | ||

| Manufacturing and Industrial | ||

| Energy and Utilities | ||

| Healthcare | ||

| Other End-user Industries (Transport, Logistics, Education, Hospitality) | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is the Australia cybersecurity market in 2026?

The Australia cybersecurity market size is USD 10.04 billion in 2026.

What is the expected CAGR for cybersecurity spending in Australia through 2031?

Spending is projected to rise at a 13.58% CAGR between 2026 and 2031.

Which deployment mode is growing fastest among Australian organizations?

Cloud deployment is forecast to expand at a 15.32% CAGR over 2026-2031, outpacing on-premise alternatives.

Why is healthcare predicted to be the fastest growing vertical?

High-profile breaches and new ransomware-reporting mandates are driving a 14.65% CAGR in healthcare cybersecurity budgets.

How are small and medium enterprises addressing security talent shortages?

Many SMEs adopt managed detection and response services and simplified SaaS bundles that reduce the need for in-house specialists.

What regulation most influences critical-infrastructure operators?

Which regulation most influences critical-infrastructure operators?

Page last updated on: