Angola Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.33 Billion |

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

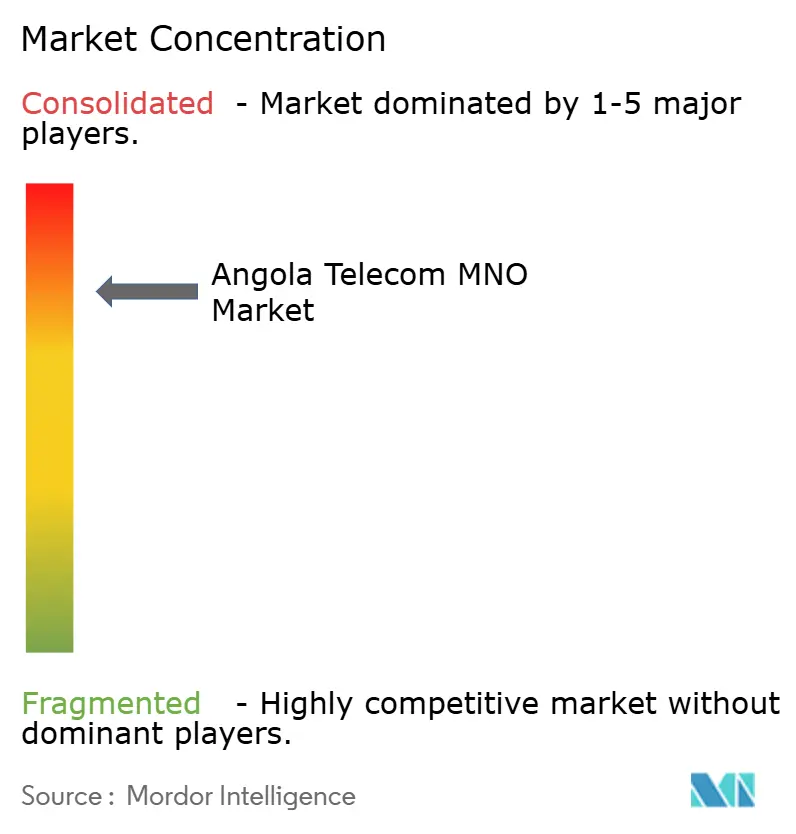

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Angola Telecom MNO Market Analysis by Mordor Intelligence

The Angola Telecom MNO market size is expected to grow from USD 1.33 billion in 2025 to USD 1.37 billion in 2026 and is forecast to reach USD 1.61 billion by 2031 at 3.18% CAGR over 2026-2031.

Infrastructure modernization, the transition toward higher-value data services, and competitive reshaping since Africell’s 2021 entry underpin the moderate growth curve. Unitel’s network scale and Africell’s pricing play continue to draw the most subscribers, while Movicel defends specialized niches. Subsea cable capacity and the nationwide fiber backbone lower operating costs, allowing operators to bundle richer data allowances without eroding margins. Enterprise digitization in oil, gas, and logistics adds incremental high-margin demand that offsets slowing consumer voice revenues.

Key Report Takeaways

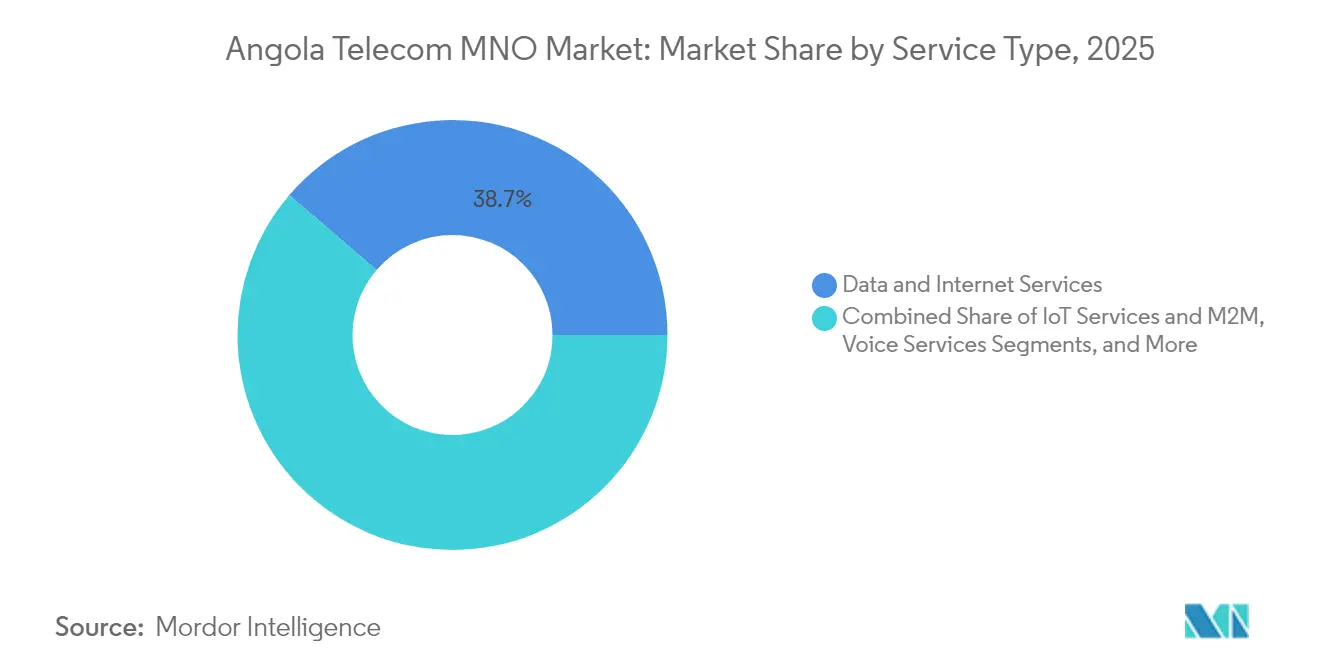

- By service type, data and internet services led with 38.72% revenue share in 2025; IoT and M2M are advancing at a 3.25% CAGR to 2031.

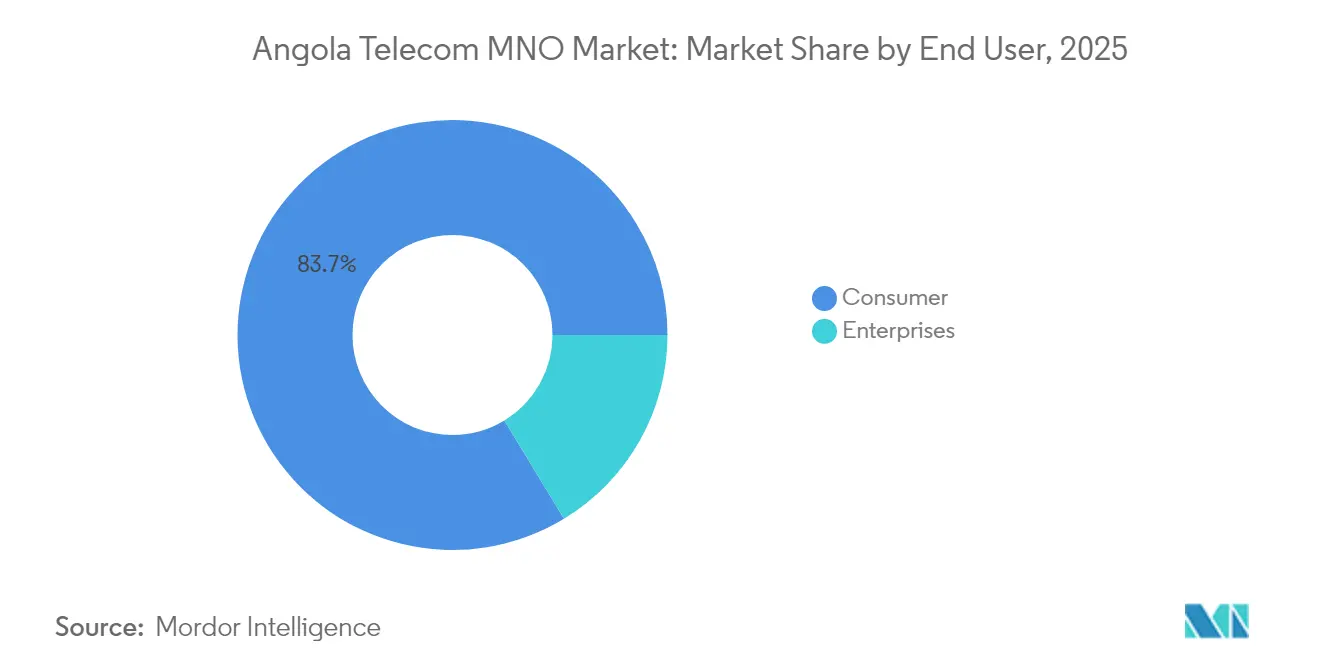

- By end-user, consumer segments captured 83.68% of the Angola Telecom MNO market share in 2025, while enterprise segments are projected to post the fastest 3.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Angola Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 4G and nascent 5G adoption boosts mobile data ARPU | +0.8% | National – early gains in Luanda, Benguela, Huambo | Medium term (2-4 years) |

| Government “Angola Digital” fiber-backbone build-out accelerates FTTx roll-outs | +0.6% | National – provincial capitals prioritized | Long term (≥ 4 years) |

| Africell’s entry triggers price competition and value-added bundles | +0.4% | National – strongest in urban centers | Short term (≤ 2 years) |

| Expansion of subsea capacity (SACS, 2Africa) slashes upstream IP transit costs | +0.3% | National with SADC spillover | Medium term (2-4 years) |

| Oil-and-gas IoT deployments around offshore blocks create private-LTE demand | +0.2% | Coastal provinces, offshore installations | Long term (≥ 4 years) |

| Chinese fintech super-app pilots depend on telco APIs | +0.1% | Urban centers expanding to rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in 4G and nascent 5G adoption boosts mobile data ARPU

Unitel’s 2023 commercial 5G launch, which delivered 450 Mbps LTE-Advanced speeds in trials, signaled a shift toward tiered premium data packages that steadily raise average revenue per user. [1]Unitel, “5G Launch Press Release,” unitel.ao Spectrum made available through INACOM’s updated allocation schedule ensures sustained capacity for both mid-band 5G and rural 4G expansion. Streaming video, cloud gaming, and short-form content drive daily data usage, encouraging operators to add lifestyle bundles that deepen stickiness. Africell upgrades its urban LTE footprint to 5G-ready status, maintaining price differentiation while chasing higher-spend subscribers. Over time, widespread 5G is expected to move heavy data users onto higher-ARPU plans, keeping the Angola Telecom MNO market on a mid-single-digit revenue trajectory.

Government “Angola Digital” fiber-backbone build-out accelerates FTTx roll-outs

The government has rolled out roughly 25,000 kilometers of fiber to unify provincial capitals, giving mobile operators inexpensive backhaul that raises capacity and lowers latency. [2]Government of Angola, “Angola Digital Backbone Program,” gov.ao The public-private build model reduces the capital burden for rural coverage, enabling tower-sharing ventures to light up new sites with microwave-fiber hybrids. A target of 125-150 internet access points per 1,000 inhabitants by 2025 anchors policy direction, and the Ministry of Telecommunications keeps right-of-way fees nominal to spur private participation. Improved fixed infrastructure also shortens payback periods for 4G upgrades in previously marginal districts, boosting long-run addressable demand.

Africell’s entry triggers price competition and value-added bundles

Africell amassed 6.2 million customers and 24% share in under two years on the back of subsidized smartphones and integrated data-voice-OTT packs. National roaming rules allowed speedy footprint replication without duplicating towers, chipping away at Unitel’s urban dominance. In response, incumbents pushed unlimited social-media passes, nighttime data rewards, and zero-rated streaming add-ons to protect loyalty. While tariffs contracted in nominal terms, higher blended usage sustained revenue stability. The competitive spark compelled all players to escalate digital-self-service apps and loyalty wallets, indirectly preparing the customer base for mobile-money roll-outs.

Expansion of subsea capacity (SACS, 2Africa) slashes upstream IP transit costs

The 40 Tbps South Atlantic Cable System cut Luanda-to-São Paulo latency to 63 ms and lowered wholesale transit cost curves by more than half.[3]Angola Cables, “SACS Cable System Overview,” angolacables.co.aoAs a DE-CIX premium reseller, Angola Cables monetizes excess capacity through African peering nodes, passing savings downstream to mobile operators. The 2Africa landing adds route diversity toward Europe and Asia, fortifying resilience against single-cable outages. Lower transit pricing lets carriers raise entry-level data volumes without eroding profitability, broadening inclusivity across lower-income groups.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kwanza depreciation inflates imported network gear CAPEX | -0.5% | National – all operators | Short term (≤ 2 years) |

| Rural energy-poverty keeps 29% of cell sites off-grid, capping coverage | -0.4% | Rural provinces – interior regions | Long term (≥ 4 years) |

| High license and USF levies squeeze smaller ISP margins | -0.3% | National – new entrants | Medium term (2-4 years) |

| Brain-drain of RF engineers to Namibia delays 5G rollout timelines | -0.2% | National – technical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Kwanza depreciation inflates imported network gear CAPEX

Because base-station hardware and core switching platforms are priced in USD or EUR, currency swings directly lift capital outlays. Operators hedge through forward contracts, yet sustained currency weakness erodes headroom for coverage-expansion budgets. Smaller ISPs postpone last-mile fiber builds, leading to congestion on shared microwave links. Although the Central Bank’s managed float aims to smooth volatility, telecom companies still face lumpy procurement cycles that test cash-flow planning, especially when oil revenue dips constrain Forex availability.

Rural energy-poverty keeps 29% of cell sites off-grid, capping coverage

Only 43% of urban Angolans and fewer than 10% of rural residents had grid electricity in 2024, forcing operators to power 3,000-plus towers with diesel. High fuel logistics raise operating expenses and constrain network uptime during seasonal road closures. TotalEnergies’ Quilemba Solar project, with USD 35 million invested for 35 MWp, offers a showcase for renewable micro-grids feeding telco sites. Yet until national electrification surpasses 60%, expanded rural coverage will progress slowly, tempering subscriber growth outside coastal corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Outperform Voice

Data and internet services led the Angola Telecom MNO market with 38.72% revenue share in 2025 as smartphone adoption topped 62%. The segment’s outperformance reflects surging video streaming and mobile gaming traffic alongside subsidized handset programs that widened 4G uptake. Voice still generates double-digit revenue but continues to decline as users substitute OTT calls, while SMS erosion accelerates under social-media dominance. IoT and M2M, though only a sliver today, are on a 3.25% CAGR path to 2031, propelled by offshore private networks and early smart-city pilots. Unitel bundles cloud storage and music streaming to lift effective ARPU, whereas Africell leverages app-based kiosks to upsell data boosters.

Operators also monetize the Angola Telecom MNO market size for OTT and Pay-TV by exploiting new subsea bandwidth and caching nodes that slash content-delivery latency. Chevron’s integrated Block 14 solution illustrates enterprise spending potential where edge analytics require deterministic connectivity. VAS, roaming, and wholesale transit continue to provide steady if mature revenue lines, letting carriers balance portfolio volatility.

By End-User: Consumers Dominate Yet Enterprises Accelerate

Consumers commanded 83.68% revenue in 2025 due to Angola’s mobile-first internet culture. Penetration reached 78.4% of the population, but large rural gaps leave headroom for new prepaid lines once electrification advances. Social-media bundles, pay-as-you-go top-ups, and handset financing keep churn in check among lower-income cohorts. Urban millennials experiment with 5G unlimited packs, signaling a future upsell ladder for operators.

Enterprises, though smaller, forecast a 3.72% CAGR through 2031. Oil, gas, and mining players procure managed connectivity for remote exploration, while government e-services require secure links between provincial offices. The Lobito Corridor rail overhaul embeds digital sensors and track-side LTE, illustrating how infrastructure programs amplify enterprise data demand. Small business acceptance of mobile money will open a mass of mid-ARPU accounts, diversifying the Angola Telecom MNO market.

Geography Analysis

Luanda captured the largest subscriber base in 2024 and logged the highest ARPU, leveraging dense fiber backhaul and proximity to subsea cable landing stations. Operators trial first-wave 5G small cells in Talatona and Ilha districts, bundling premium content to monetize affluent segments. Benguela and Huambo form a second-tier cluster where Africell’s aggressive rollout achieved 42.9% penetration in Benguela within one year, increasing competitive churn in coastal belts.

Interior provinces remain under-served because 29% of cell sites depend on diesel power and long microwave hops, which dampen profitability. The Angola Telecom MNO market size for these regions will rise once Quilemba Solar and similar renewable projects lower operating costs. Provincial capitals benefit from government fiber spurs that reduce backhaul congestion, creating commercial justification for 4G upgrades and future 5G overlays.

Angola’s geographic advantage as an Atlantic crossroads allows operators to peer traffic into Brazil via SACS or into Europe via 2Africa without double-transiting hubs. Cross-border terrestrial links toward the Democratic Republic of Congo and Zambia give Luanda-based carriers scope to market wholesale capacity, broadening the effective Angola Telecom MNO market.

Competitive Landscape

The market remains concentrated, with Unitel holding 72% of subscribers in 2024, Africell 24%, and Movicel the remainder. Unitel exploits first-mover scale, brand equity, and government ties, funding early 5G pilots and network densification to secure premium users. Africell differentiates through aggressive pricing, modern greenfield infrastructure, and youth-oriented digital campaigns that resonate in cities. Movicel focuses on enterprise data and provincial loyalty programs, sustaining relevance despite scale disadvantages.

Infrastructure ownership dictates cost structures. Unitel and Angola Cables jointly anchor capacity on SACS and WACS, gaining lower transit rates. Africell leases high-capacity IRUs on 2Africa and local fiber, avoiding legacy depreciation but facing renewal exposure. All three operators partner with tower-sharing firms to offload passive assets and unlock cash for radio upgrades.

Service innovation intensified after 2024. Unitel rolled out self-provisioning eSIMs and AI-driven churn prediction, while Africell bundled ad-supported zero-rated social apps to widen funnels. Movicel piloted rural solar-powered micro-towers with community revenue-share models, aligning with universal access mandates. Regulatory openness to mobile-money licensing in 2025 positions operators to extend financial-service adjacency, further diversifying the Angola Telecom MNO market.

Angola Telecom MNO Industry Leaders

Unitel

Africell Angola

Movicel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Angola Cables became a DE-CIX premium wholesale reseller, expanding its high-density peering options for regional carriers.

- May 2025: TotalEnergies confirmed USD 35 million investment in the 35 MWp Quilemba Solar project to power 40,000 homes and nearby telecom sites.

- May 2024: CAMTEL partnered with Angola Cables to interconnect cross-border networks, enhancing Central Africa transit routes.

- February 2024: The Ministry of Finance disclosed plans for a Unitel IPO within its privatization roadmap, opening doors for foreign equity.

Angola Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The Angolan telecom market includes an in-depth trend analysis based on connectivity, such as fixed networks, mobile networks, and telecom towers. Telecom services are divided into voice services (wired and wireless), data and messaging services, and OTT and PayTV services. Several factors, including the increasing demand for 5G, will likely drive the adoption of telecom services across Angola over the coming years.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the forecast revenue for Angola’s mobile-network operators in 2031?

Total operator revenue is projected at USD 1.61 billion, reflecting a 3.18% CAGR between 2026 and 2031.

Which service category is expanding fastest in Angola’s mobile sector?

IoT and M2M connectivity posts the highest 3.25% CAGR, propelled by offshore energy digitization and smart-city pilots.

How many mobile subscribers does Africell serve in Angola?

Africell reached 6.2 million subscribers, equal to 24% share, within two years of launch.

Why does Luanda record the highest ARPU in Angola?

Dense fiber backhaul, early 5G small-cell trials, and affluent consumer segments enable premium data-bundle adoption in Luanda.

How will renewable energy projects affect rural mobile coverage?

Solar micro-grids such as Quilemba lower diesel reliance, improving uptime and making rural cell-site expansion financially viable.

Page last updated on: